Foreclosures in California: 121,000 Notice of Defaults and 63,000 Foreclosures. Home Values Plummeting on Record Breaking Quarter.

Even though the market is once again enjoying a delusion sandwich covered in toxic mortgage mustard, the reality on the ground continues to become grimmer. Wachovia, one of the nation’s largest banks announced an $8.9 billion quarterly loss and that they’ll be slashing over 6,000 from their workforce. Oh, and the dividend is getting slashed as well. So what happens? The market of course pushes the stock up by 27%! American Express, the uber credit card company also announced problems but the market is believing that the Federal Reserve and the U.S. Treasury have some mythical powers to create money out of thin air. They do only if you own an investment bank.

Yet back in the trenches of reality, Americans are feeling the massive pinch of the world’s biggest housing bubble being pricked by the sharpest needle of all, imploding debt. That is no hyperbole. In no time in our civilized history have we seen such speculation on a global scale stemming from real estate. California is the poster boy of this housing bubble. You would think that the market would be punishing lenders even harder who have created and own such financially destructive loans yet many see this as a time to jump in. Just look at the markets. Tread these waters at your own peril.

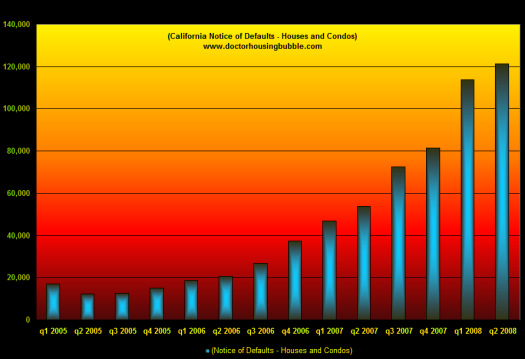

Today, the California foreclosure numbers for the second quarter were released and they are not a pretty site. First, let us take a look at the first sign of future wealth destruction, the notice of default:

As you can see from the chart, notice of defaults have gone sky high in that past few quarters. We went from a relatively mild 2006, to a quickly deteriorating 2007, to the current record breaking problems in 2008. The reason notice of defaults are so important for future predictions is that these are homes that have yet to be taken back by lenders. These are early signs of trouble. What this means is lenders in the upcoming months better gear up for a tsunami of REOs.

We already know that the short-sale option has been a marginal joke in California. Many are so deeply in negative territory that no lender would go for a short-sale and rather would take a foreclosure. They have too many problems trying to stay solvent and avoiding their own foreclosure ala IndyMac Bank. The vast divide between lenders and how loan modifications are being handled is an utter joke. There is no standard. Some lenders are willing to work with you while others are doing absolutely nothing in the area of loan modifications. They are all holding their breath and preparing their turd bucket of mortgages ready for release into the belly of Fannie Mae and Freddie Mac. Bank of America who recently acquired toxic mortgage producer Countrywide recently alluded to the fact that they may not be backing up Countrywide debt:

“(Global Trend Analysis) Bank of America Corp., the second- biggest U.S. bank, said it may not guarantee $38.1 billion of Countrywide Financial Corp.’s debt after taking over the mortgage lender, increasing the likelihood of a default.

“There is no assurance that any such debt would be redeemed, assumed or guaranteed,” the bank said in an April 30 regulatory filing, adding that no decision has been reached. Investors had grown more optimistic the bank would back Countrywide debt. Ratings firm Standard & Poor’s cut the mortgage-lender’s debt to junk today after saying it would raise the grade earlier this week.”

They basically are doing a “it wasn’t me” on the market. After all, would you back up Countrywide’s toxic debt?

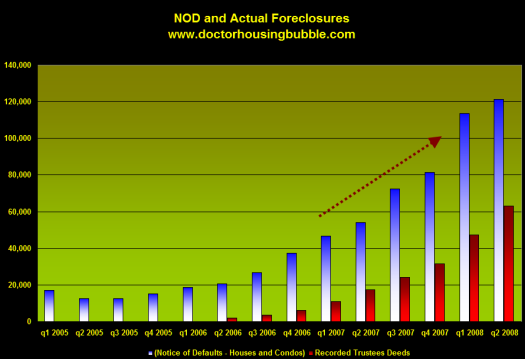

Last quarter, there was an all time record of 121,341 notice of defaults filed in California. This is incredible. Only 3 years ago, the number was 12,408 for the second quarter of 2005. That is a ten-fold jump in 3 years! Yet the more distressing analysis is when we look at the notice of defaults and also combine the actual foreclosures that occurred in the second quarter:

We are now in uncharted waters. The notice of default numbers may look like they are plateauing but this is like arguing whether you are going to jump out of a 100 story or 102 story building. The number of foreclosures in the second quarter hit a stunning 63,031. If you look closely at the chart, even in 2006 many of the notice of defaults where resolved without a foreclosure actually taking place. Well of course this occurred because the massive speculation allowed those who over paid to sell to someone who over paid even more.

“(DQNews) Of the homeowners in default, an estimated 22 percent emerge from the foreclosure process by bringing their payments current, refinancing, or selling the home and paying off what they owe. A year ago it was about 52 percent. The increased portion of homes lost to foreclosure reflects the slow real estate market, as well as the number of homes bought during the height of the market with multiple-loan financing, which makes ‘work- outs’ difficult.”

This is not good and only reinforces the obvious which the overall market is ignoring at the moment. What this tells us is 78 percent of these notice of defaults will end up in foreclosure. Now the precipitous decline in prices is ensuring that many of those 121,341 notice of defaults will further add REO inventory for the remainder of the year and cause future losses to these banks and lenders. Now how is this going to be healthy for the market? If anything, it assures us that prices will be falling for the remainder of the year and will put a vast amount of inventory on the market during the worst selling times which are the fall and winter. This combined with the $300 billion in option ARM loans will be a destructive combination. We have yet to see the massive recasts in the pay Option ARM market. You can do the math and any lenders with large exposure in California are going to get hammered.

Paulson saying we are months away from a bottom is absurd. Senator Jim Bunning was right when he called him out and stated that Paulson will be out in a few months, but the rest of us will be here to deal with any of the consequences of hasty actions. The bottom is in…but for Paulson’s career.

We have just cut the umbilical cord of reality from Wall Street. Look at the action with WaMu announcing a $3.3 billion loss:

“SEATTLE—Washington Mutual says it swung to a loss in the second quarter as it increased to more than $8 billion its reserve to cover sour loans.For the April-to-June period, the Seattle-based bank says it lost $3.33 billion, or $6.58 per share, which compares with a profit of $830 million, or 92 cents per share in the year-ago period. Results include a previously disclosed, one-time reduction of $3.24 per share related to the company’s capital raising in April.

Thomson Financial says analysts, on average, were expecting a loss of $1.05 per share.

The bank says it increased its loan loss reserves by $3.74 billion to $8.46 billion during the quarter, as it continues to face mounting losses stemming from bad mortgages.”

Shares of WaMu went up and down in after hours trading as if there really is any doubt about the data. Not only did WaMu miss their target, they missed it by multiple times! Bwahahaha! And the freaking stock barely moves. Do you know where most of WaMu’s loans are? In California. Just let the above charts sink in with their vivid colors and try to take a guess what is going to happen. They’re going to need all those loss reserves for the army of Real Homes of Genius they have in their portfolio. Companies should just announce a $1 trillion dollar loss and you’ll see their stock rally by 50%. Apparently bad news is now good. Hello George Orwell!

What we are seeing on main street is not being reflected by what is occurring in the stock market, which should at least reflect what is going on in the real world (aka, look at the above charts). Yet what do we expect from a government that tells us we are not in a recession, unemployment is not bad, and inflation is contained? Their panacea of course is drilling for oil we won’t see for at least 5 years! I didn’t realize subprime mortgages ran on 89-octane. All you need to do to verify this reality is take a trip to your local grocery store, fill up your tank of gas, send your kid to college, look at your mortgage, and try booking a trip out of the country and you’ll quickly realize that something is rotten in Denmark.

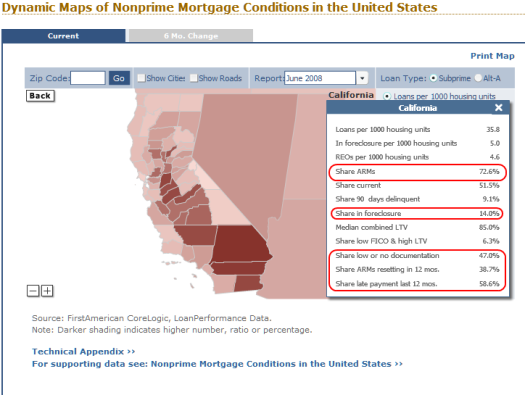

Let us take a look at another data point that shows us how far we are from a bottom here in California:

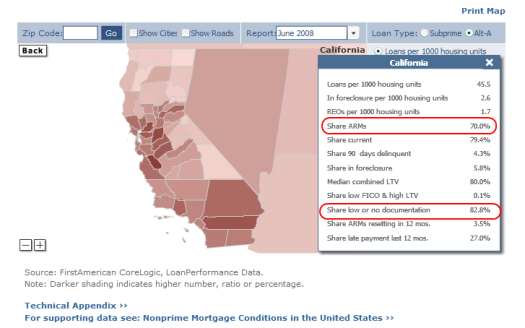

The above is a look at subprime loans in the state. As you can see, there are still plenty out there to cause damage but take a look at the Alt-A products which most pay Option ARMs fall under:

And this should make you feel warm and fuzzy all around. The Congressional Budget Office came out saying that the rescue of Fannie Mae and Freddie Mac would cost approximately $25 billion but no one really knows how much. Heck, WaMu and Wachovia combined dished out losses of $12.2 billion in one quarter and they are peanuts to the issues confronting Fannie and Freddie. Yet they are also seeking in the legislation to increase the public debt limit by a stunning $800 billion from $9.8 trillion to $10.6 trillion:

“(WSJ) The $25 billion cost estimate from the CBO for the rescue plan was downplayed by Democratic and Republican lawmakers. “Everyone knows it’s just a wild guess,” said Sen. Jim DeMint, (R., S.C.). He called the plan a “huge gamble,” but added that, “it’s kind of: Guarantee a little now or pay a whole lot later.”

Lawmakers plan to raise the public-debt limit as part of the legislation to $10.6 trillion from $9.8 trillion. Congress must vote to increase the limit to account for additional borrowing, something it is loath to do, although it would have had to take that step this year even without the rescue plan for Fannie and Freddie, Democratic aides said.”

This is flat out absurd! What a disgrace. You need to get in contact with your Congressperson or Senator and say you will not stand for this absurdity:

Give Senator Jim Bunning some support to filibuster this piece of toxic legislation

Can you see what is happening? You’ll also see in the legislation that they are trying to raise caps to $625,000 which of course will make it convenient to off load this crappy Alt-A California mortgage junk onto the public debt. If you needed any more evidence that Washington is trying to offload this entire mess on the U.S. taxpayer, you need not look any further than this piece of legislation. What a shame.

There are more Alt-A loans in California and these actually have a higher concentration of no-doc loans! Can you take a wild guess how these are going to do now that the state has a median price of $328,000, down 31.5% from the peak price of $479,000? If you look to Washington or Wall Street for your answer, don’t expect one that reflects the reality on the ground. We are living in two separate universes here. If you would have bought a median priced home in California last year at the peak, you would now be down $151,000. Is this really a reason for a rally especially in lenders that fed into that speculation that is now clearly bursting with an onslaught of foreclosures?

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

21 Responses to “Foreclosures in California: 121,000 Notice of Defaults and 63,000 Foreclosures. Home Values Plummeting on Record Breaking Quarter.”

Bungee jumping? Sky diving? Swimming with sharks?

So called “extreme sports” are for wimps! If you want a real edge of your seat experience, try owning a home in California!

“…delusion sandwich covered in toxic mortgage mustard” ! You are indeed the Doctor of the Housing Bubble!

The rally in bank stocks was amazing till you remember how intensively they had been shorted. When the SEC forbade ‘naked shorting’ of these stocks, and I’m no Warren Buffet, all it took was big institutional holders of these stocks to prohibit the hypothecation ( loaning to short sellers) of the shares they owned to start a panic amongst the ‘shorts’. My guess is this is what happened and it is good example of how Wall St. can ‘rig’ the market to generate some short term profit. As you note the actual earnings reports are awful to horrendous and are propped up as much by customer gouging and accounting fantasy as anything else. The bank reports I perused all admit that expect an acceleration of defaults

in the third and fourth quarter ( because they hid them in the second?). Now why

hide or understate non performing mortgage loans for the 2nd quarter? Wells admitted they extended by 30 to 60 days the time a loan is delinquent before they call it delinquent. Others performed the same or similiar financial ledgerdemain. My guess is they were all waiting for the Congress to foist this monstrosity of a housing bill on the nation. Let the government, both federal and state, come and buy up the ruined REO in collapsed neighborhoods. Provide new ‘incentives’ for 1st time buyers to pick through the garbage in bank portfolios

and provide a place for the banks to send zombie loans to. Just my ‘guess’.

Up here in N. Cal. it’s obvious that the banks are hiding defaulted loans by not foreclosing on them. All over town there are houses with boarded up windows and weedy yards that aren’t being cared for. Meanwhile the population of homeless wandering around downtown or living in thier cars grows daily.

When the weather cools down these houses will start to be occupied/destroyed by the homeless and the same neighbors that aren’t mowing the lawns won’t call the police until it’s too late. The police will have other problems.

The ownership of properties by absentee entities has to stop. Build on it, rent it out, sell it or tear it down. Don’t leave fire traps for the locals.

Well, Bush has flip-flopped, and HE IS GOING TO SIGN THE HOUSING BAILOUT BILL INTO LAW!

Speculators win again! Savers and responsible citzens continue to be trampled!

Great passioned article, doc!

It will be very helpfull if you raise the profile of the president candidate , thirth pary or independent , which is not obssesed with this bailout maddness of the mainsteam politicos.

Doctor:

I hope you include the impact of the new housing bill, I mean LAW, on the current housing events…

Thanks for the information. We get a lot of California buyers. Looks like we will be getting fewer is they can’t sell their homes. The Bend Oregon real estate market is in the same condition. To date we have had a 410% increase in Notices of Default. There are currently 155 short sales in our MLS.

WaMu employees of my acquaintance are blaming working class people for these woes…and the derivative ones (like cities facing bankruptcy). Not the greed orgy (most of these friends went from dot-coms to WaMu, btw). Not the fact that CA law forbids taxation. Not the fact that they don’t want their own taxes raised, and their goal in life was to run prices up, make a killing, run away and live the rentier fantasy.

Doc wrote:

“We are now in uncharted waters. The notice of default numbers may look like they are plateauing but this is like arguing whether you are going to jump out of a 100 story or 102 story building.”

Doc, you’re intuitively correct. The number (100 vs 102) isn’t the point. Without going into a bunch of statistical theory (or calculus), it’s the area underneath the curve/line that’s the issue. The top points tell only part of the story.

To put it another way, say you have 9-12 pints of blood, and you have three episodes of heavy bleeding. In the first you lose three pints. You’re fine. In the second you lose three. You’re wobbly. In the third you lose three. Bubbye.

Like Jim we’re glad Californians increasingly can’t sell and bail on their home state. They were gentrifying our city’s housing market to the point that we lost six families on our street alone who could no longer afford the doubling of their property taxes thanks to the vicious run up in assessments. We couldn’t be happier to hear property values are going down…though our house and land haven’t shown that trend yet. On our street alone of seven houses four are now occupied by “‘forniacators,” all of whom paid from 30-70 percent over the assessed value. Cheap for them. Costly for the rest of us.

rose

Doctor,

Once again you have hit the nail on the head. I read an article back in 2004 that described the current housing bubble as a “Middle Class Ghetto” based on the fact that people were not living off of their income but instead their credit. I started selling new homes in the I.E. for a large national home builder in June 06 and was able to experience this first hand. I was amazed at how much home people were willing to buy with their current income. In my community we closed 36 homes in March of 07. By May 07 we were selling the same homes in the same community for $100k less. In less than 90 days everyone of those 36 homes was upside down and 90% of those that bought have a 5 year ARM which I believe they won’t be able to refinance out of or sell even in 2012! It is astonishing how a brand new neighborhood can go from middle class opulence to a “Middle Class Ghetto” within 18 months. At the end of the fiscal year in March 07 our division closed over 2000 homes, the projection for the fiscal year ending March 09 is 425 homes closed. This is an amazing drop and the total divisional employee count is currently 73 down from about 410 in 06. Before it’s all over I’m pretty sure there is going to be 2 or 3 large national builders going bankrupt (it happened in the auto, airline, steel etc. industries and currently banking) simply because no one was able to see the writing on the wall and they continued to build and sell into their future. Greed is NOT Good

So, today I heard a NAR commercial on the radio as I was driving to work. It said that on average a home DOUBLES in price every ten years. This kind of information sucks if you aren’t following what’s going on in the market today and your completely clueless to the facts. Whatever happened to ethics in this country?

You wrote eluded. It’s funny when dimwits try and use big words. The correct word is allude. Of course, this mistake is simply representative of your overall poor logic. That’s the problem with the Web. Any idiot can create a blog…

Non US citizen – been watching FedUpUSA.org has a video which shows this isssue well.

The only one who wrote the word “Eluded” was you, mr. mortgage. So guess what? Using your logic, that makes YOU the only dimwit on this blog.

We long-time readers of Dr. HB’s blog, also find it humorous when some mortgage schlepper (aka Troll) come and bash the truth presented on this blog. We know it must hurt, knowing that this was only another bubble (the overextension of credit) that lead to this real estate bubble, which is slowly fizzling back to reality, on foreclosure at a time. Actually over 100k mortgages went bad this past quarter alone in California.

Indeed, it just goes to show that any idiot can post a stupid comment on a well written blog.

What truths from this blog do you want to challenge? Give us some facts, instead of just name calling, mr mortgage. Or are your posts just signs of the bitterness that a once in a lifetime run up of real estate will now become a once in a century deflation of real estate?

Hoping for a response…………………

Hombre

I agree South Bay…I sense a bitter, broke, frustrated, and lets add incompetent man in Mr. Mortgage. I think he is upset that he is no longer able to lead the lifestyle he had during the boom. Maybe he is upset at Dr. H because what he was preaching has all come true in spades. I have a friend who worked in the mortgage business. Gosh how I remember the bragging, the condescending tone of voice, the naivety, and the ignorance. I always asked him, “How can this go on any longer?†He would always reply by explaining how this time its different and how California is so desirable. My wife and I make roughly make about 170K as teachers. He would say, “I make what you both make in 6 months.†Well now we are making about 7% more and he is down 90%. I don’t get any pleasure by seeing him struggle. To the contrary I asked him to read Dr. H’s blog and told him he should save for rainy days. He laughed every time. I hope you saved for rainy days Mr. Mortgage.

Well, we already know the ‘real’ Mr Mortgage (http://mrmortgage.ml-implode.com/) is not the realtor troll who claimed his name. Ignore the troll and eventually he’ll return to the bridge under which he lives.

Doc – since you like charts, have you ever considered tracking the run up and following decline in property prices, and then correlating it to the run up in NOD’s and/or NOT’s? I think it might be very informative – and possibly predictive – of the duration of the plunge down this side of the roller coaster.

median price of $328,000, down 31.5% from the peak price of $479,000.

I’ll buy in when the price of that house hit 79K.

I wouldn’t worry too much about typos. Blogs are no different than newspapers or Main Stream Media sources like AP and Reuters. The mistakes in grammar and spelling are so commonplace one learns to simply get by on understanding the intent. So relax dude.

I still keep looking at average income vs. price here in Los Angeles and home prices are still unrealistic for the average income. All these bailout plans and new laws cannot unfreeze the market unless that issue has been addressed. If the government really wants to prop up home prices or bail out banks they are going to have to come up with a plan to shower ‘consumers” (geez I hate that label) with money. Without additional money, everything else will eventually crumble won’t it?

Hi,

Does anyone out there know if the “housing panic” blog is dead?? It has not been refreshed for over a week and I can not recall any time in the last two years when that has happened.

Thank You

Tom

Just when I was beginning to warm to your blog ( Mr Mortgage) you come up with this BS:

by mr mortgage

You wrote eluded. It’s funny when dimwits try and use big words. The correct word is allude. Of course, this mistake is simply representative of your overall poor logic. That’s the problem with the Web. Any idiot can create a blog

Whether or not elude or allude is used, we don’t need a grammar nazi to obfusicate with minutae.

The above article is thoughtful and helpful in understanding the current economic situation and is consistant with other articles by the Dr.

Get over yourself, Mr Mortgage- you ain’t that great.

Perhaps we should all realise that when we ‘dream’ we eventually ‘wake up’. When the dot com bust hit and the bottom fell out of the stock market the “get rich quick group’ realised that the only people who had not lost their shirts at that time were people who had made sensible investment in real estate. So what did the ‘greedy’ get rich quick do? Decide to get into real estate for the fast buck and now they are finding that the bottom can fall out of that too. The sensible investors, those individuals who worked hard for a living, invested in property that required work and made sense, purchased stock at prices in line with reasonable return, are now apparently about to lose their shirts bailing out the reckless quick buck characters. What a wonderful world!

Leave a Reply