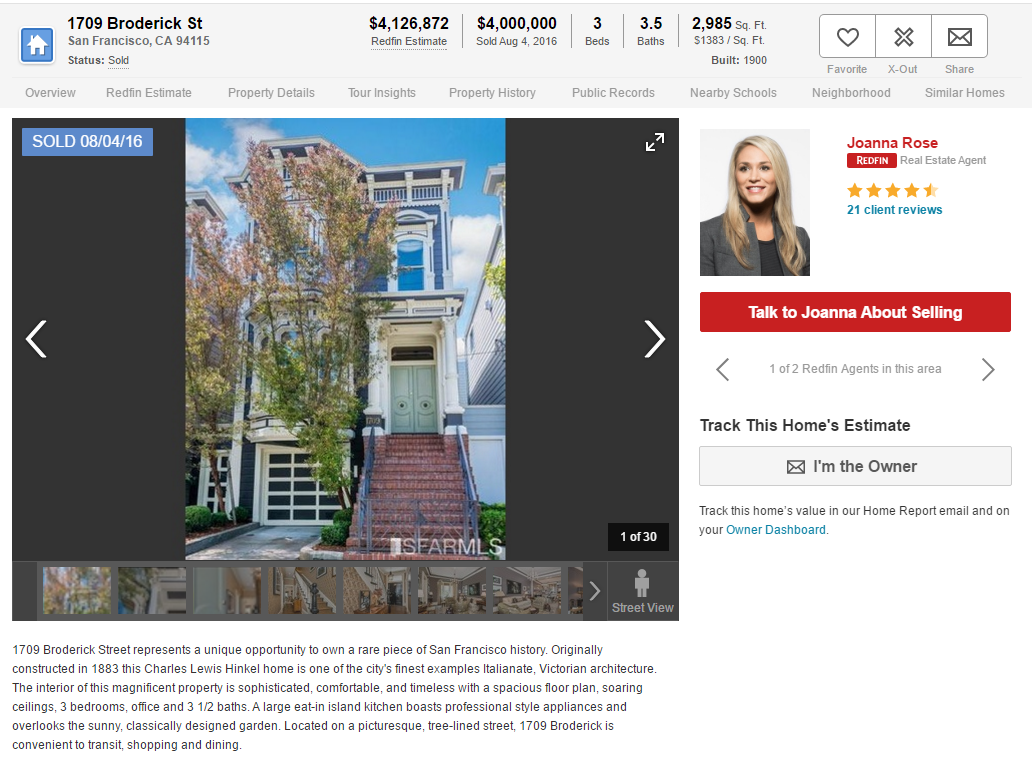

Buying a home without even viewing it: Roughly one in five homebuyers make an offer without seeing home in person. Full House home recently sold in San Francisco.

Buying a home without seeing a property in person is like marrying a person by only viewing their Tinder profile. But house horny people are ready to hump away their savings and lock into a 30-year mortgage matrimony. It is a bit surprising but not all that shocking that nearly one in five home buyers are making offers on homes without even viewing a property, according to new research. When bidding wars ensue and rental Armageddon is all the rage, buying a crap shack may seem like the most reasonable decision. And the psychology behind this is interesting. People will spend hours debating what restaurant to go to on Yelp but are itching to buy a home without even seeing it? This is the manic market we are living in. And in the Bay Area, things continue to get nuttier. The Full House home recently sold for a nice amount of money. Given the occupations of the fictional inhabitants, they would likely live in tents behind a tech incubator instead of that place.

Bidding with a blindfold

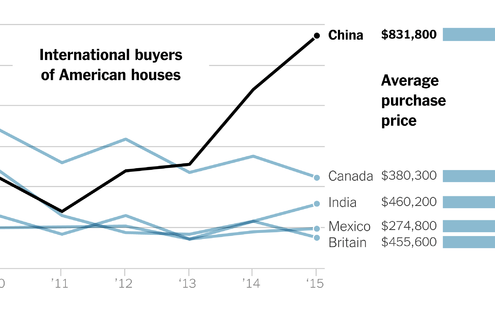

What you find as well is many foreigners are buying homes without viewing the place. Take a look at the research:

“(Redfin) While Jason’s story may seem unusual, new survey data shows that 19 percent of people who bought or sold a home in the past year made a bid on a home before viewing it in person. The survey of more than 2,000 who bought or sold a home in the past year was conducted by SurveyMonkey Audience and commissioned by Redfin. A similar survey conducted last year found that 21 percent of recent homebuyers had made offers sight unseen.

Buyers of high-end homes were almost twice as likely to have made offers on homes sight unseen. Thirty-nine percent of people who bought homes for more than $750,000 made offers without seeing homes in person.â€

$750,000 will get you a crap shack in many parts of SoCal and the Bay Area. It isn’t surprising though that 39 percent of “high-end†crap shacks are making bids, sight unseen. Just go to some of the areas targeted by foreign money and they’ll bus people in, largely from China.  And the data aligns with the above:

I suppose if you are buying a new million dollar home, what is the need to view the place? But this is certainly atypical of your regular buyer, especially those overpaying for shoddy construction and homes that are in mediocre markets. But of course, everything in SoCal is prime.

Fuller House Prices

Remember the show Full House? Well the home sold in August:

The place sold for more than $4.1 million and has some serious renovation work done:

But based on their jobs, it is very unlikely that they would be able to afford this place today. Then again, income doesn’t matter. They could easily go for a PoppyLoan and go zero down. Maybe they can do a zero down loan and buy sight unseen. Why not right? After all, the show is back on Netflix. The old is new again.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

81 Responses to “Buying a home without even viewing it: Roughly one in five homebuyers make an offer without seeing home in person. Full House home recently sold in San Francisco.”

^^That chart up there is why the bubble isn’t as dramatic as one is led to believe. The introduction of new wealthy, international players to the domestic arena drives the price up and keeps them there. They’re all cash buyers so it’s not like we’re gonna have another mortgage crisis en masse like the last one. Our market is on the foreign bidding block more than ever and that has a pretty huge impact on the definition of “normal prices”. We’re moving toward 21st century serfdom.

“They’re all cash buyers so it’s not like we’re gonna have another mortgage crisis en masse like the last one.”

No it really is different this time – when the foreigner’s home countries go belly and they lose everything they will be scrambling with a pack mentality to liquidate “assets” they have stashed overseas (in the good ole USA). It will be a free-for-all race to sell sell sell as quick as they can – chasing the market down…

This includes not only the Chinese and the Indians, but the Canadians, whose RE market is bubbled up even more than ours is. As soon as the Canadians start taking a beating you’ll see RE is in the “Sand Belt” where these “HLOC rich” snowbirds have bought their “second homes” go straight down the tubes.

The sticky point is if the foreign buyer will be able to sell. If they are stuck in the homeland and the homeland decides to claw back assets, what will happen here? If they can sell but can’t receive the proceeds in USD then what? These foreign buyers might end up like the zombie banks, and not have the ability to sell. I am sure the courts will be tied up with claims. What will US policy be if China wants to grab the homes? Sorry no home confiscations while you occupy the South China Sea. The US will gladly let Chinese nationals liquidate in order to collapse the domestic real estate market???Not likely. How long can these Chinese nationals continue to pay property taxes if China closes their ability to offshore funds. It is quite the rabbit hole that is developing. What happens win Canada and Australia also try to rescue their real estate markets? I would hate to be a Chinese national that is not prepared to or is already beyond the reach of the Chinese government. But then the Chinese government has clearly stated that no citizen is beyond their reach.

Is it possible that the Chinese buyers choose to just stop paying their Chinese lenders and start a new life in the US without the intention of ever going back? Could Chinese lenders do anything about that?

@ImnotPOTUS

Most likely these foreign buyers, once having liquidated their RE assets here in the US, will find a way to bring that money back to their home countries much in the same underhanded/quasi-legal/slightly shady-yet untraceable method they used to bring it here in the first place. How does one bring enough paper into the US to make an “all cash offer” on an $800,000 home in California? One way or another, that suitcase of cash that made it through customs will find its way back to Shanghai…

@New Age

Chinese banks can file an international lawsuit to recoup their money as in the case of some Vancouver investments.

This is a very important point Calgirl has pointed out. Yes it is different because of the liquid assets concern. I also have this concern in my portfolio, trying to sell a paid for second home to get most of my cash has proved to be not so easy. Although I have no fear of foreclosure of course I do want to get most of my investment back, I must reduce the price to get interest in the property at my peril, t I will now lose some of my cash in this investment. When a market is as uncertain as housing no matter if you have a mortgage or not in the end we all can get hurt.

Like many, when you see a sold home you must go further into the transaction just what did the seller have to lose to get the deal done, the NAR will have you believe the market is great, yeah sure and a business grosses 5 million but what is their net that?

JJust because somebody

The home prices may seem crazy but it is the new reality, and it is going to stay this way for a while whether we like it or not. Of course, eventually there will be a crisis and will temporally correct it but I genuinely doubt it will be soon. The economy is only getting momentum and can keep this way for a decade or more. Also note that in many other countries people spend much larger fraction of their income to pay for housing, and it is sustainable. It is just a part of a larger trend of the middle class impoverishment.

I see price cuts in both rentals and for sale, all over Los Angeles. I see places offered for lease or buy. I see places sell and then be immediately relisted as rentals. I see places that never returned my inquiry still sitting empty. I see rentals continue to list higher and higher, but sit longer. Actively looking at both all year, hard not to feel the whole thing is a sham.

I see these shams in West LA/Santa Monica too. Sales re-listed as rentals, unrented inventory for half a year or more 1 block from the beach, nothing selling (I track listings on the RE websites which email me when a place sells….one every 2-3 months with 5 new listings a day). Something is OFF.

Many of those countries also have generous social welfare programs (free college, free healthcare, long parental leave, etc) so spending a higher percent of your income on housing is doable.

When will the craziness stop?

Every time there is a potential FED interest hike on the table, the market goes down and provides hope for people to jump into the RE market. Then the FED comes out and says “Just kidding.” I don’t see how the RE market can correct without a decent hike in the next 1 to 1.5 years. I also don’t see a decedent hike from the FED during this time frame. Even after the election, I don’t see a change on the horizon.

I though 2017 or early 2018 would definitely provide an opportunity to purchase a house, but I am seriously reconsidering.

I know it’s not good to time the market, but should I overpay at least 30% to buy now?

Think of it this way: Are you really over paying if the interest rates are lower than the 6-10% of decades past?

Yes, you are overpaying when prices take on speculative proportions due to easy and cheap credit. Furthermore, associated costs (taxes, maintenance, etc.) are based on the price of the house, not on borrowing costs. In general, risk and debt rise with the cost of purchasing RE, or any other assets.

Let me re-phrase the question: Are you really overpaying when this has become the norm?

In addition to what Prince notes, there’s also little to no opportunity for future refi.

Not to mention, high rates imply higher inflation which in theory leads to higher income growth, which is advantageous vs. the historical cost of that asset.

In many ways you’re better off with higher rates and lower asset cost than vice versa. If the market cost is just rising to absorb finance savings, you come out behind in lots of hidden ways, even if the monthly payment nets the same.

Hard to compare this time to say the 70’s other decades, but you would need to compare incomes to home prices of the time along with mortgage rates. However, there is the issue with price mania like back in the late 90’s with the dot com jobs in San Jose. I heard a home was bought for $750k and then turned around and sells it for a few million. Home prices were going for the normal mortgage interest rates 6-*% back then and still people were paying top dollar. News at the time was saying the Silicon Valley was generating 64 millionaires a month?

Ah yes, the new norm whereby the Fed has repealed the economic cycle. Low rates as the norm hasn’t rescued Japanese from its collapse as of yet.

Timing the market rarely works. Only buy if you can afford it and plan on owning the house for an extended period of time. If you can check those off, then do a rent vs. buy calculation. If you are anywhere close to rental parity, it might make sense to buy.

You may get your 30% correction, but that will likely come with much higher rates. Your monthly payment might be the same as buying today…all things to consider.

If the rates rise, the price falls, and my mortgage payment would be the same in either of those scenarios, I would have an option to refinance when rates fall again. If i buy now, I probably will never be able to refinance and pay higher property taxes on the higher amount.

The rent vs. buy calculator does not really provide realistic information when considering LA market. My rent for a decent, older two bedroom around Sherman Oaks is $1700. Anything comparable to buy and even remodel would run at least $450,000. Even with 20% down and no PMI (or second mortgage), it is not even close. At the same time, as my income grows, i do not have anything to deduct on my taxes, so I am forced to may more tax to Uncle Sam, not building equity in my own residence, and continue to rent.

I would wait a year or two to buy, but getting disillusioned with what is going on.

Any suggestions…

True, although with higher rates and lower prices, you don’t have to tie up as much cash, taxes are lower, you have the potential to refinance later on down the road, and you can pay off the principal more quickly. I’d love it if rates went up to 6%.

I think your rent vs. buy comparison is much closer than you believe. Paying down principal and accounting for tax savings need to get included in this equation. Comparing gross numbers is never a good idea.

“If you are anywhere close to rental parity, it might make sense to buy”

not even close in my hood. And a correction is coming and worse than last time. Incomes have to mean something. Corporate profits tell us that Q3 2014 was the end of this cycle….and what a cycle it’s been, the lowest interest rates in 5000 years and still no real growth other than in debt. AS David Stockman likes to point out “bread winner” jobs are still below where they were in 2007 which we all know WAS A BUBBLE and now that were back there with WORSE fundamentals many crow here like this time makes sense….it doesn’t just like it didn’t.

my X bought in 2005, just sold in 2016, lost $30K on the sale, this is the reality.

i hope you all stick around and many countries are already getting sick of China printing money and going around the world and buying it up.

If you buy at higher rates and lower price, you also have the ability to buy a second home/condo as an investment/rental in the future because ratios won’t me maxed out. If you pay top dollar (even with lower rates), forget about being able to save or buy a second property/vacation home if your income is not growing faster than inflation.

You can do a rent vs buy comparison all you want, paying more is simply paying MORE for the same house. As of said before, wife and I have already started our family so I’m not going to wait 5 years to buy but I will wait a bit longer to get a better price and I will get it because I will make sure I pull the trigger when enough inventory is available and small correction happens. You don’t need to time the market perfectly but it’s not hard to watch 10-20 properties that you might like and see how they are doing a month later and see the purchase price, to get an idea if seller has wiggle room to drop the price. You may have to add new properties to that watch list later but you will see the trends and eventually make offers, get it at your price or move on.

Now if your rent is like 5k per month well, then that’s your problem but if it’s reasonable, you don’t need to be pressured to buy whatsoever.

A place that costs $450k, with 20% down and a loan of $360k @ 3.6% per Zillow calculator…

P&I: $1,578

Taxes: $450

Insurance: $80

HOA: $250 (?)

Total: $2,358

Assume you pay about 25% in fed/state taxes where you can deduct the $12,700 in mortgage interest the first year. You’d get back about $280/mo when spread out. So you are down to $2078 in cost to buy vs. $1,700 in cost to rent.

Then take into account that you’re putting $7,700 into principal that first year too. So really your cost is $640/month less for that year…putting you at $1,436 to buy it plus maintenance.

Assuming 1% maintenance (which is high for a condo where HOA covers a lot that you’d pay yourself on a SFR)…you’d add $4,500 for the year or $375 per month. Total cost to buy including maintenance … $1,811/mo.

So it costs you about $111 more per month to buy it. I actually earn enough to get back in tax savings even more, if I were to buy this place. Typically from what I’ve gathered the tax deduction gets you enough to pay the property taxes in LA county so the calculation above is conservative in my opinion. When I work this out with my own tax numbers I end up at even cost to buy/own.

IF you are going to stay long term, your payment will never change, you’ll put more into principal each month, though since you’ll pay less in interest your tax deduction lowers. Really it all comes down to how the market is when you sell, and whether or not rents go up.

I just think that “not even close” isn’t a good way to describe it. To me it’s a close call, entirely dependent on how long you’ll stay and how stable your job is.

There are other factors that one can’t put a number on. Condos tend to be nicer and more well taken care of than apartments, with neighbors who are invested and care more about the well being of the place. Better quality finishes, etc…You can do whatever you want to customize without permission from a landlord. You can’t be kicked out. You can have pets. Etc etc…

You can continue to try and time the market, though. I do think it’ll have a good chance to correct, I just have no guess as to when. You could spend another $40k renting for 2 years. Or you could end up paying now only for the place to lose paper value of more than that in the next two years. Just saying, if you are in long term then really do a good look at the numbers…when you look at the previous crashes, 10 years later the values were always back to where they were before…

@A

The 90-100k as down payment is always conveniently left out of the calculations. Coming up or tying up so much capital in one transaction is a non-starter for most. If you think RE will recover quickly thanks to Fed engineering, why not invest the proceeds in a stock market fund that will similarly rebound quickly and provide higher returns?

@A:

Many HOAs have insurance included in the payment. Maintenance of almost $400/month is excessive. With that being said, it’s cheaper to buy said place with 20% down compared to renting it at $1700/month. The numbers are hard to argue with.

@Prince, I agree you could put cash in either place. In my case for example I went with 10% on a $450k place and my PMI is only $110. In my case it was not enough to tip the scale away from buying it. If one doesn’t have enough for even 10% then buying a place is probably not in the equation at all.

You could instead put it in the stock market. Either one is a gamble, in my opinion. I agree housing is due for a downturn. I still decided to buy a place because I am simply running out of time and the places near work were outrageously expensive to rent. At this point in my life with things I have going on I did not want to spend another 5 years renting waiting for some opportunity to buy, I prefer to settle in now and even if it drops wait it out – I was prepared to live there 10 years. That’s something that works for me but may not work for a lot of others, however the simple math is that there are still places that are close to even when simply looking at the numbers. I just feel that the government, and banks, will be trying their best to keep things as they are, even if that includes more QE, keeping rates the same, etc…I could be wrong, but unfortunately at this time in my life I don’t want to take the gamble of fighting those powers anymore…

But just like housing the stock market could fall. I just think that a home is different in the sense that if the market tanks, you at least still have the roof over your head, the same payment, etc. In fact in financial hardship you could take on roommates for example, while if your money is in stocks in an emergency you have to sell and BOOK the loss…so I guess it could go either way.

Lord Banfein said…”You may get your 30% correction, but that will likely come with much higher rates.”

Even worse, what if your timing is off and the 30% correction you “knew” was coming played out like this:

Year Price

2016 500K

2017 530K

2018 575K

2019 602K

2020 618K

2021 665K

2022 699K

2023 721K

2024 744K

2025 764K

2026 788K

2027 801K

2028 560K (the crash)

Infation wise, it make sense to wait, but few people are happy passing up on 500K, only to pay 560K 12 years later, much less the 250K in rent you paid in the interim.

@A

The Standard deduction for a married couple is 12,600. So according to your calculation/scenario the net tax benefit of owning is only $100. The first year. This will of course go down as principal is paid down so that the standard deduction will be higher than the MID. Your purchase scenario therefore only is a benefit to a single person or HOH.

Miss American Pie:

The MID isn’t the only itemized deduction, you also have state income taxes (I’d say around $6k for a married couple filing jointly making $125k+ to buy that house) plus property taxes of $5k.

MID: $12k

State income tax: $6k

Property taxes: $5k

Total itemized deductions: $23k

(I didn’t even include the property tax deduction in my scenario, that further reduces the buying side by $100/mo)

If you got a $400k loan today, at only 3.5% interest, then in the year 2035 your interest is STILL almost $7,000/year. Yes, your MID is technically lower than in 2016, but how do you think prices will be in 2035, or RENT??

Everyone acts like MID goes down as principal is paid but have you actually looked at amortization schedules?

Anyone who bought a place and took a standard deduction is either an idiot or has the worst tax guy ever…

No one ever mentions this here

Just open a LLC and be a home based office, you can essentially write everything off, in fact sometimes it works better than the Tax and interest write off’s afforded home owners.

Taxes on everything will continue to rise faster than inflation….

Peaks happen, can’t time them so buying now is plain old stupid…..better to buy right before the bottom…

“Assume you pay about 25% in fed/state taxes where you can deduct the $12,700 in mortgage interest the first year. You’d get back about $280/mo when spread out. So you are down to $2078 in cost to buy vs. $1,700 in cost to rent.”

Your own words. You stated there was a $280 benefit to the MID. I’m pointing out that the net benefit is a $100 deduction which makes your original scenario misleading. So I’ll give you your second scenario: couple making 125k with total home related write-offs of 23k. In a 25% tax bracket that’s a net (over the SD) tax savings of $2600 ((23k-12600)*0.25) or $215 a month. Still less than your $280. Either way I’m not even arguing the merits of renting vs buying. Just pointing out the fuzzy math which is often (not just by you) used to justify buying. You simply cannot ignore the SD in calculating Buy vs Rent.

Also you recommended that I look at an amortization schedule so I took your advice and ran your numbers. By year 3 the MID is below 12k. By year 10 it’s around $9600. In this low interest rate environment, more of your payment goes to principal, which is a great thing. Unfortunately it lowers the impact of the MID. And keep in mind the SD does go up as your MID goes down. The SD 10 years ago was $10300 for a married couple filing jointly. 🙂

Miss American Pie:

You still don’t get it. You are assuming the MID is the ONLY deduction available when you buy instead of renting. Which it is not, property taxes are also deductible. When you combine those two PLUS the state income taxes, you will be above the SD for a LONG TIME. Almost the entire term of the loan, look at the numbers.

Here, I’ll simplify for you…In order for the aforementioned buyer’s $23k of deductible expenses to go down below the SD of $12.5k, the interest portion would have to be about $1,500 (since there’s ALWAYS $11,000 in deductions via property tax and state income tax).

It doesn’t matter that the interest is less than $12k after year 3. It’s not until the interest is less than $1.5k that you get close to falling under the SD instead of itemizing. So it’s all irrelevant, no one buying that will use SD, probably ever. The principal won’t lower enough for you to have less than $1,500 in interest until … well …the year 2045 if the loan started right now.

The renters are stuck with only the state income tax to deduct…so about $6k.

Let’s recap with prop tax this time: renter gets $6k to deduct, buyer gets same $6k plus $5k prop tax plus $12k interest = $23k to deduct, difference of $17k; at 25% that’s $4,250 or $354/month benefit over the renter. I even left out the property tax deduction to simplify, so my number was conservative. You’ll actually get even MORE back than I initially estimated when you put that in.

The only “fuzzy” math is from people like you trying to pretend like deductions don’t matter or quickly disappear. I don’t care to justify anything, in fact I think it’s not a good time for buy for most people unless you’re in very particular circumstances, since I think there is a drop coming. I just think it might take longer than we expect due to intervention by TPTB.

I can stay it’s a BAD TIME TO BUY and still correct your bad math.

Oh and I forgot my calculation was for a single person, and you wanted to compare now a married couple that gets an additional $6k deduction (thereby reducing the benefit of itemizing and thus the benefit of MID according to you)…but for the sake of doing your scenario in addition to mine let’s change it to a married couple using the SD or buying (and this time adding in the property taxes that I left out to be conservative since you want to be more detailed):

Couple renting deductions: $12.6k

Couple buying deductions: $23k

Difference: $216/mo @ 25% effective rate

So buying the 2/2 condo that started the discussion above:

P&I: $1,578

Taxes: $450

Insurance: $80

HOA: $250 (?)

Total: $2,358

Tax savings over the renter: a “measly” $216

Effective payment: $2142

Principal first year: $570/mo

Cost to buy: $1,572+maintenance

Let’s call maintenance $250 because LB is right, my estimate of $400 is way high considering there’s HOA covering most expensive structural things and we’re trying to be detailed here after all.

Total “lost” buying: $1,822/mo

Total “lost” renting: $1,700/mo

I hardly consider this “not even close.” But maybe you do and you think that since you’re married the $64 monthly difference in tax savings between you and a single person is enough that you should rent it. Then rent it.

Just make sure you itemize, otherwise you’re leaving money on the table.

Let’s assume the SD goes up every year and your interest+prop tax+state income tax equal the SD in 15 years instead of the 29 it might take if SD didn’t go up. You lost your MID by then. Guess what, in 15 years that rent is sure as hell not $1,700 anymore – and your principal balance is much higher.

Again, it doesn’t matter when the MID goes below the SD, it’s when MID+prop tax+state income tax does. Keep that in mind.

If you want to bet that the decrease in MID due to principal payoff will outpace the rent increases in coastal SoCal, go right ahead…just don’t say the MID makes little to no difference.

I am an investor. Over the long term the rate of inflation is around 3.5 percent. Over the long–term my investments to up by about that much. Oh sure…there are exceptions. Point is if you overbuy, eventually inflation takes care of the problem. I bought a house in 2003 for 219000 paying around 15000 too much. Now that it’s 13 years later, it’s worth maybe 400000. Ok so I overpaid way back when. Who cares?

Magic inflation eh KarenL. Forever gainz eh. It’s been on the flood of global monetary loosening to extremes, and general inflation itself actually means people have less money for housing. Only wage-inflation gives people more money to pay higher prices for housing (excluding the other phenomenons we’ve seen like global investors all QE’d up). Anyway all the investors who rely on forever house price inflation need to be hard shaken out of the market.

Not only are there lots of foreign buyers, there is also very positive news in the industrial real estate market. I mention this because ‘industry’ is doing well and industry needs employees. According to Transwestern 2nd quarter of 2016, the industrial space vacancy rate in metro LA was 1.2% which is an ‘ all time low’. Rental rates for industrial space have hit highest rates ever. Employment in metro LA up over last year.

According to Colliers, office space is also showing higher rents, lower vacancy…..

These figures tend to indicate no slow down in the LA economy.

Of course, housing will correct but does not seem likely on the close horizon.

Go China! I hope they buy every last home in America, and then start competing among themselves to drive up prices 5-10x today’s levels. Soon every American will be renting from a Chinese landlord. Why not? California will finally be rolling in property tax, thanks to all of the boomers selling their $2m ranch houses in Palo Alto and Orange County to Chinese investors.

After all, I legend was there was this Pacific island nation that almost bought up all of America in the 80s. And look at them now! That gravy train never stopped and their economy never corrected!

“At the same time, as my income grows”

lucky cuss, my income hasn’t grown in decades. But i have to compete with China who can somehow build the whole job for less than just the steel costs in the USA.

Yes, I fully agree with all of the posters above–the business cycle is dead. We will likely never have another downturn or correction in any market, least of which the stock market or real estate.

Yellen has solved the age old mystery of business cycles. By keeping rates at zero and buying trillions in bonds, her invisible hand has managed to keep production at full capacity indefinitely. Even the Soviets couldn’t centrally plan their economy so effectively!

Personally, I’m taking every last cent out of my 401K, IRAs and savings accounts to buy as much commercial and residential real estate in LA, SD and SF as possible. With 3.3% interest, no price is unjustified. Zillow says prices in SF are dropping, so I’m buying the dip!

Laughing all the way to the bank baby!

I can’t tell if you are serious or being funny.

You guys better vote for Trump. Not only would he destroy our economy, but the stocks too.

We can all jump in once he bankrupts our Economy.

I don’t play the stocks but if I did, I’d sell everything ‘two days’ before the election and assume that whoever is elected, the market will go down 1,000+.

Then after four days, consider re-enering. By then the market will have re-adjusted and you can make a more informed decision.

Nah, I’m gonna vote for Hillary because at least we all already know she’s a disease-riddled, sociopathic, lying crook owned by the bankers. She may be complete human garbage, but at least we all know that she’s human garbage, and there’s something to be said for that.

I’m in a similar boat….neither Trump or Hillary will get re-elected in 2020…I think the country can recover after 4 years of Hillary better than 4 years of Trump. Both will be awful. But Hillary is Stage-3 cancer and Trump is full blown AIDS.

I’m voting for Trump.

Hillary is more likely to get us into another expensive, pointless war. Trump gets along with Putin — a good thing.

Trump cares more about the American people than does Hillary. Trump may not care like your mother does, but he cares more than Hillary. She’s a cold-blooded reptile.

Trump’s a loud egomaniac. Hillary’s a full-blown, murderous psycho.

For Rent: http://www.zillow.com/homedetails/1709-Broderick-St-1709-San-Francisco-CA-94115/2097476740_zpid/ Only $13,950 a month.

Full House? oh you mean Mullet-Fest!

Many are missing the “doomsday” bunker mentality entering into many foreigners minds when buying in the US.

Here in South Florida, Miami in particular many overpriced condos are being bought by South Americans. Buying a condo gives them several advantages.

1. They now have a greater ability to enter the US, and if they spent enough access to a green card.

2. They have a doomsday bunker to retreat to if poop goes down in their home country.

3. If prices do go down, they may still be in the black depending on what the fiat in their home country did. Plenty of Brazilians can lose 20% on their condos, and still be up 50% in their local currency.

4. A good vacation home if all is well.

If you were a wealthy Chinese business person parking a few million in the US real estate market is safe, even if you loose 50% of it in a market correction. 50% of something beats having the CCP taking 100% of your worth in China.

This is not to say the market will go up forever, there is a limited supply of rich people looking for country bunkers, (Miami is starting to run out/every one may have already bought) But many of the overseas buyers are not looking for rental parity or even appreciation, they are buying a hedge.

“…Many are missing the “doomsday†bunker mentality…”

Yes, but.

The “bunker” mentality has been around since the end of WW1.

So why all of sudden the influence of foreign “bunker” money on R/E?

This is a good point. You can see this behavior all over the world: millionaire Russians and Arabs buying in London, South Americans in Florida, Asians on the West Coast. For them, an overpriced bubble housing purchase in the Developed World (even if there is a bust and the value goes down 20%) is still a more secure bet than keeping your gains in the shady state-run bank of your home country.

I was living in Brazil from 2010-2013, tons of wealthy Brazilians were buying places in Miami at that time while their economy was still hot. Now the Brazilian Real has gone from 1.5 to the Dollar to something like 4.2 and their economy is in the sh*tcan. Seems like they made the smart move by investing outside their own country… In essence, these foreign RE purchase are like safe deposit boxes for the global 1%

I just read today that USA incomes were up 5.2% in 2015, all the way back to a level not seen since 1998 …. !! Surely this is bullish for housing ! ( sarcasm intended )

The interesting news about that, going back 50 years, is there’s always a recession after those kind of numbers.

Maybe the people who are buying sight unseen are just interested in the land. They wouldn’t care what the house looked like if were just going to tear it down.

I agree with A and Lord in regards to the rent vs. buy calculations. We moved back from Toronto in 2013 and bought a house in Simi Valley for 540K. Our mortgage is $3200 a month and to rent the same 4/3 house would be roughly 2900-3100 a month, so for use, buying was the better option. I’ve only rented once in my life and never liked the ‘insecurity’ of being told to move, etc.

I think timing the housing market is next to impossible. Will there be a correction. It could happen but when? Who knows? I remember reading bubble blogs back in 1998-99 talking about a imminent crash. Sure it happened but not for almost 10 years of crying the sky is falling. If there is a correction, I really don’t believe it will be anything like we saw in 2008. If you were lucky enough to buy in 09-10, you really timed it well. I had moved to Toronto in 07 and if I had thought that I would end up back in So Cal for even a second, I would have flown down and bought a house in 09 for sure, but at the time I had no intention of returning to California.

I look at my house as a place to live and raise the family and not as an investment. We’ve been in the house now for almost 3 years and the same model a few houses down just sold for 660 (asking 675) and it sold in a week on the market. I’m in the house for the long term, even though I can retire in six more years, but will stay put for decades to come.

Good for you Rob, I have been a long time poster and invested heavy in Simi Valley from the $1 down days to the Wood Ranch disaster. I held on and in the end Simi Valley made me a rather financial Independent investor who now wouldn’t invest in anything anywhere. You should enjoy the roof over your head and hope someday to have a paid mortgage and enjoy life. take care

their were no housing bubble blogs in 1999 as the internet blogging just started….blogging didn’t even begin in Earnest until after 2001….

Heck, Calculated risk was first blog to really address re bubble and it didn’t start to churn until 2006

USENET was huge by 1990 and covered every imaginable topic. How soon they forget.

The thing left out is the huge down payment aside from the monthly nut required to own a home and expenses like taxes, insurance and stuff that breaks which gets super expensive after the home warranty expires. Take that down payment and invest in stocks for much better return and less work.

If you want to talk about investments, housing is highly leveraged…stocks are not. The tax breaks you get from housing (while living there and when selling) are hard to beat. Unless you plan on living in your car, housing (shelter) is a necessity.

As has been said umpteen times, long term renting strategies in places like socal are BAD ideas. History has proven this, do so at your own peril.

Overall no matter who gets elected this country is in for a very rocky ride. Banks are still strung out from the subprime fraud they created, the Feds are still playing the everything is fine and like many folks who are taking principal to pay bills or lines of credit this house of cards is ready to crater all the way down and nothing I read or see can stop it now. I have been the all-time optimist, now I am the all-time realist, I hope I’m wrong?

I am confused on how there still seems to be a supply of people that can afford these ridiculous housing prices and still afford to pay down student loans, car debt, etc and not be on the brink of financial failure. My husband graduated from Harvard Law and we have the debt to show for it along with the income. He makes over 300,000 a year and we have managed to pay down half of his loans and save a down payment for a house but after crunching the numbers numerous times it simply doesn’t make sense to spend our life savings on a crap shack. Until prices go down we will continue to live in a tiny but affordable place. Stash cash, pay off loans, build up our retirement account and wait for people’s bad choices to bring down this housing market to a realistic and sustainable level.

In the Bay Area. It’s Indian, Chinese and Filipino families with 3 generations under one roof. Maybe one “bread winner” and the rest is all just supporting staff. Grandparent(s) gave their life saving for the down payment, their Social Security if they get it just goes in the pool. Wife works a lower quality job in food service, hair, nails, etc…grandparents baby sit…etc..etc.

I’ve gone to a few open houses in the East Bay in nicer areas like Dublin, Alameda, Milpitas and that is all of what I’ve seen. Three generations of Indians and Filipinos looking around.

Confused, We have a rather large country and overseas buyers in the market for homes at any one time. Even if 1 or2% can afford such prices it leaves a pool of more buyers then houses on the market. That said, when the pool of buyers who can afford such prices lessens to let’s say .05% because fear of investing or world of crisis in stock and oil markets for example than you get a stagnant luxury scenario which causes the 1% of sellers to dump their overpriced investment, they can afford such a hit, banks than devaluate to a point the surrounding inventory which creates price drops.

The question going forward for most buyers will the drop be enough for affordability even in the event of severe bubble?

Most likely not, because this is not a 2007 sub-prime concern, but banks who still will not be willing to loan 30 years at under 4% and can’t turn a Bay area housing market into a free for all of housing drops of 40% or more.

Prices will have to drop yes, but that just mean the very rich swoop in and buy, for the avg. Joe think about relocating to towns where a price drop means you really can afford a home, otherwise unless you win the lotto it won’t happen in the BAY AREA for most. Good luck

Smart choice. I’m in a similar situation; well, plus a few years. No debt, good savings, high income, but renting an affordable place. Rent vs. buy (as some discuss above) is not even close for me. BTW, you may know, but at your combined income levels, mortgage interest and property tax are likely not even tax deductible given high Calif. income taxes and the total limitations on deductions. Keeping deleveraging, saving and investing wisely. I also believe prices will normalize, but I stopped caring. Having the option to retire whenever I want (in my 40s) is priceless.

“Neighbor versus Neighbor” (in Playa Del Rey)

there has been talk on this blog about AirBnB and the dilemna in many LA neighborhoods (and SF neighborhoods probably).

The debate is: do homeowners have the right to turn their homes into vacation rentals (in order to continue to afford living in their home) OR do homeowners have the right to prevent such vacation rentals (in order to preserve the quiet neighborhood without the comings of goings of constant vacationers).

Here the debate is hot and heavy in Playa Del Rey, esp, The Jungle which is a small patch of homes and condos and apartments where Jefferson meets Vista Del Mar.

http://argonautnews.com/neighbor-vs-neighbor/

I think the debate is hot and heavy elsewhere, including Venice, SM, etc.

I am curious what you’all think of this debate.

[I have a friend in SM Canyon who turned his garage into a 1 bedroom unit and was renting it out for about $1800 per month. Then when the tenant left a few years ago, he posted it on AirBnB and is now fetching about $5K per month to vacationers with 1 week minimum stay. He intimated this to his neighbor one day in a moment of trustful conversation and guess what – his neighbor told him he was doing the same thing with his garage…. I have another friend in Culver City she has turned her garage into a bachelor pad and is fetching about $1K per month for various vacationers (3 day minimum).]

I haven’t been down to the Jungle in PDR in almost 30 years. That place was a drug, alcohol fueled party back in the day with lots of renters. Did it get gentrified if owners are now complaining about Air BnB short term rentals?

Regarding using residential neighborhood properties as short term rentals, in my opinion this should be illegal. A residential property is zoned residential, not commercial and therefore should not be treated as such.

Not to mention the callous disregard for the noise, lack of parking, etc. that doing this can bring to a residential neighborhood. As we all know on this blog, finding and paying for a decent house in a nice community is hard enough these days without then having to watch one’s hard earned homestead turn into hotel row.

LB: PDR is nice, it was the last reasonably priced location in the area IMO in about 2012. It’s all gone up a bunch now though. I would easily live there over Venice, personally.

Looking Forward has it right: zoning exists for a reason. Airbnb is basically doing away with zoning laws, when you can turn a house or garage into a hotel. This is why zoning laws are there in the first place. I think it should be regulated, it has the potential to ruin neighborhoods for residents if half the homes are vacation homes. I for one would be pissed if all of a sudden my street was overrun with vacationers and parking became an issue, not to mention noise. It’s one thing if you buy knowing you’re next to a business. It’s another when the zoning laws are just not being observed.

Time and again history has shown, in many sectors, certain economic structures which were once considered inviolable by the masses, were quickly broken up when change and need suddenly came along. “If something cannot go on forever, it will stop”.

My view is the major banks are positioning. They allow those who can best take the brunt of a correction to keep piling in. Then, when everything in place, the authorities change things to shake out greed and bad positions, and allow good money and opportunity in.

I hope you are right!

Interesting little tidbit that appears to validate what is going on with housing prices.

http://www.theglobeandmail.com/news/british-columbia/incomeless-students-spent-57-million-on-vancouver-homes-in-past-two-years/article31892652/

I am so offended by the inventory I am seeing in my market that I’m near an emotional breaking point. I’d best describe the inventory I am seeing as dog excrement with a pitched comp shingle roof.

The good news it that flipping is back to its 6 year high!!!!! (sarcasm) http://fortune.com/2016/09/15/mortgage-rates-housing-market-flipping/

Chinese money is moving to Seattle: http://www.seattletimes.com/business/real-estate/seattle-becomes-no-1-us-market-for-chinese-homebuyers/

A growing wave of money from China and other foreign countries is pouring into the Seattle-area housing market, helping drive home prices even higher. And since July a new tax on international buyers in Vancouver, B.C., long a popular market for home seekers from China, has focused even more global interest here….

Historically, Seattle had attracted less real-estate money from China than Los Angeles, New York and San Francisco.

But the region’s upward shift only accelerated after British Columbia enacted a 15 percent tax on foreign buyers in the Vancouver metro area. Searches by Chinese home seekers for Seattle have more than doubled, while they’ve been cut nearly in half in Vancouver, Juwai says….

Overall, buyers from China bought about $1.6 billion in homes across Washington last year, according to the National Association of Realtors. The state drew 6 percent of the $27 billion that Chinese spent buying U.S. homes last year, putting Washington behind only California, New York and Texas.

More on some PDR properties. This one in particular doesn’t make sense to me. Help me out here. It sells for about 1.6 million then goes on for rent for $6,000? How does that cover mortgage and everything else? When the zip code is full of price reductions which area appears to topped out. Where can the money be made here?

Check out the price history, interesting as well.

http://www.zillow.com/homedetails/8257-Rees-St-Playa-Del-Rey-CA-90293/20385597_zpid/

Assuming no mortgage, a tax rate of 1.2%, insurance cost of at least $1,200 per year, and no vacancies, the ROI at $6,000 per a month rent will be approximately 3-3.5% annually depending on maintenance, upkeep, and incidental costs. That equals approximately 50K per year. This calculation does not take into account appreciation.

A 3% return on a 1.6 million dollar investment. That doesn’t sound too wise.

From march 2015 thru april 2016 international home buyers have bought $10 billion dollars of texas real estate,to read the story google:houston chronicle real estate news

8.2 percent more homes were sold in august 2016 than in august 2015.july home sales were down, because of less inventory to choose from in houston,google:houston texas home sales report.

Leave a Reply