California Housing Prices: 3 Different Measures Showing Different Prices. Calibrating Housing Prices for California.

Trying to figure out the aggregate housing price decline of a state as large as California is no easy task. For a state with over 36,000,000 people getting a simple statistic on housing is challenging and requires the ability to look at multiple sources of data. During the height of the housing bubble median price reports for the same location would sometimes be off by as wide as $100,000. How can that be? Some sources look at repeat sales while others combine new homes and re-sales in their data.

The major point is now that housing prices are correcting, the major sources of housing price data for California are starting, albeit slowly to come together and are showing a more standard price point.

We are going to look at three major sources of housing price data for California. The three sources we are going to look at are the Case-Shiller Index, the California Association of Realtors (CAR), and DataQuick monthly reports. The Case-Shiller Index to begin with looks at same home re-sales over time. That is, how does one single home do over a length of time? By most industry standards, this seems to be the most accurate and fairest representation of price changes since you are looking at one home and its performance with future sales activity. The index figure is not a price but rather, an adjustment from the base year of January 2000. The base figure is 100 and prices move as a percentage. So for example an area with a 200 Case-Shiller Index point has doubled in price since January of 2000.

The other two measures from the CAR and DataQuick look at new home and re-sales in a given month. For example, we will look at all home sales for the month of May and determine a median price for that month. This data usually gathers sales that occurred 30 to 45 days prior since escrow accounts and tax records take 1 to 2 months to update. This offers a good view of what is occurring on an overall perspective yet may miss some of the nuisances on a single home traveling through time.

First, let us take a look at California as a whole and look at the peak prices from both the CAR and DataQuick:

What you will notice is that in regards to the peak month, both the CAR and DataQuick came rather close at pinpointing the same peak month. April and May of 2007 seems to be the peak month in their data. Yet you will notice a stark difference in the actual peak price. Both report the median sales price yet the difference from both is $113,640! That in many parts of the country will buy you a starter home so this is no minor detail.

However, look at the current correction median price and you’ll see that both data sources are quickly converging on a single point. The difference from both sources is $40,250. That seems like a much more reasonable difference.

Another stunning point in the data is how quickly prices are declining. It is hard to believe, whichever dataset you choose to look at, that the median California home price early last year was nearly $600,000 or $500,000. Now, the median price is starting to hover around $300,000 to $350,000. That is a stunning amount of wealth destruction in one year for a state with 13,170,000 housing units.

Now let us use the Case-Shiller Index data to see if the data coincides with the CAR and DataQuick information:

Unfortunately, there is no statewide measure for California from the Case-Shiller Index but we can look at three of the largest metropolitan areas to see what is going on. The Los Angeles component of the Case-Shiller also includes Orange County.

What you’ll notice is the divergence in peak months for Los Angeles, San Diego, and San Francisco. Los Angeles hit its peak almost 1 year after San Diego. In addition, these peak prices occurred much earlier than the CAR and DataQuick. In fact, we are looking at 1 to 1.5 years earlier. Now why is that? Again, the Case-Shiller Index looks at a single home over time. That is why those that were still arguing that there was no bubble in 2006 and 2007 simply because prices on an aggregate scale were rising were not looking at the emerging trend in the Case-Shiller Index.

For these major metro areas the overall percent decline is from 25 to 28 percent from the peak reached. Keep in mind that this doesn’t factor in inflation over these few years so the actual real price decline is much higher. Let us look at these three areas in terms of dollar amounts from the CAR data:

In terms of percentage declines, the CAR shows a steeper price decline for Los Angeles and San Diego but not for San Francisco. Again, that is why it is important to look at various sources to get a better overall perspective of what is occurring in the overall market.

What is common amongst the three sources is California is facing the steepest and most quick moving housing correction in history. The amazing fact is we still have $300 billion in Pay Option ARMs that were made during these peak points sitting and waiting for a recast anniversary.

The new housing bill now fully signed into law by the President will do very little to help California. Why? First, lenders should they wish to participate will need to have the property reappraised at today’s market value. Given the above data and across the board correction, this will force lenders to take a major haircut. In addition, the lender will be required to cut an additional 10 percent from the current appraised value. Well in places like Los Angeles where the median price is off by 35.65 percent an additional reduction of 10 percent will bring the one year correction to nearly 50 percent! That is astonishing and to be honest, I see very few lenders who will elect to do this (if they even can). It will force them to bring Pay Option ARMs that are current on a low payment looking like they are profitable into major losses were nearly half the balance is now gone. The weak balance sheet of lenders will implode if they elect to go this route.

Another reason that this won’t fly in states like California is many borrowers even with the new bailout program will not be able to make their payments on a 30 year fixed. How is that? Let us do a quick Pay Option ARM versus 30 year fixed calculation. We’ll use the peak Los Angeles price and current median price as our reference points. Let us take a look at the Pay Option ARM terms:

As you can see from the above, the minimum payment is only $2,053 on a $616,230 loan! Simply insane and ridiculous. What should be a $3,626 a month payment is artificially lowered by nearly half. Keep in mind that data on option arm loans tells us that approximately 80 percent of people make the minimum payment and we are not factoring in taxes or insurance above.

So with that said, let us assume the lender decides to participate and that home valued at $616,230 is now appraised at $396,560. How will the numbers work out now? Well first the lender will need to take off 10 percent off the appraised value plus a one time 3 percent fee from the note to participate in the program:

$396,560 x .13 = $345,007 new 30 year fixed mortgage

According to the Freddie Mac website the current 30 year fixed rate is 6.63%.

So let us assume the borrower now goes with this loan. What does his monthly principal and interest payment work out to be?

30 year fixed new principal and interest payment = $2,210.26!!!

So even after the massive haircut the lender will take from the 35.65% market correction, the additional 10% in reduced appraisal terms, and the extra one time payment the borrower actually has a higher payment than the initial Pay Option ARM payment for a loan that was $271,223 larger.

So for all the e-mails I’ve gotten about the bill and California please read the article looking at the gritty details of the FHA program and see why California is not going to be helped by this bill.

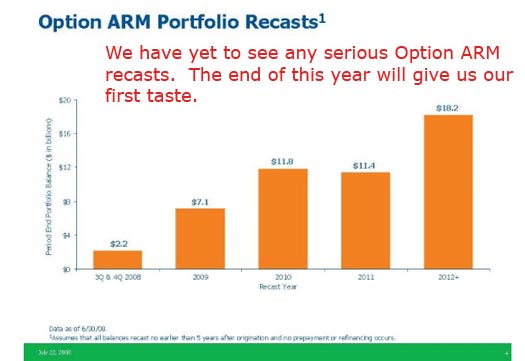

And if you think we have seen the recasts on these loans yet just take a look at the WaMu Option ARM portfolio which is “worth” $52.9 billion with $26.3 billion here in California:

Use the multiple price measures above and follow the trend. Housing prices in California are still nowhere close to a bottom. Even though the 3 sources above don’t completely agree at least they can agree that the trend is heading lower.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

27 Responses to “California Housing Prices: 3 Different Measures Showing Different Prices. Calibrating Housing Prices for California.”

Excellent article. You have hit the nail on the head. I think you might also want to consider that banks may require borrowers to come up with 20% down on refinances in California. That will only make matters worse.

I would also like to point out the Elephant in the room.

HELOC total loss.

Walk away will be the California theme for the next few years.

If you can’t afford a jump from $2000 to $2200, I don’t think anyone can help you.

Yesterday morning on New York’s WEPN ESPN radio there was an ad for Wamu’s small business accounts. They were offering 3.7% on ballences over $50,000. If you had over $1,000,000 the rates were even higher.

How long do you think the game will continue before final finantial Jeopardy is played. and I don’t mean with Alex Treebek.

prices come down in undesirable locations here in LA, the better properties remain the same. say what you will, this is mostly an inland empire / south LA / crap location event.

Just like FHA Secure when it was rolled out…. very, very few people will be helped by this new bill. This part of the legislation was the lipstick on the pig. The real reason this abomination was passed: to “backstop” FNMA and FHLMC so that our Hedge Fund and Chinese debt holders would not dump their holdings.

As for banks taking that big of a haircut….it ain’t gonna happen. These rules take effect October 1st. Check in again in 6 months. My guess is less than 1,000 transactions will take place by then.

A realist in a harsh world.

SEMEPR FI:

Real estate prices will go back to the 1940’s level…

A box of: American Silver Eagles… will soon buy a very nice house….

They plan on taking everything you have this time….

This crash/collapse is NO accident….

As I understand these arms if you just make the min payment the recast comes much sooner. I’am like a kid at xmas I have been waiting since 04.

The banks will continue to try to minimize thier losses. They’ll use the same appraisers that previously overvalued the property, to again overvalue the property. The homeowner’s new payment will likely be much higher than $2200, perhaps $2700 to $3000. Few homeowners will qualify, because income must be documented this time.

To: bobabooey

Why are you reading this site if you’re not concerned about prices going down in ‘prime’ areas of LA? The prime areas are shrinking every day. All we have to do is look at Brazil to see the future of California.

To: BabaBooey: Dude – check again. Even the best neighborhoods are already 15-25% down from the peak. In the last housing bust durring the 1990’s, the less desireable properties crashed first. The higher end properties crash later, but ultimatley took a bigger percentage loss, than those that were cheaper and more affordable. Do you honestly think we will still see tiny 2+2, 1,000 sq. ft. homes, on the L.A. West Side still selling for $1,000,000 a year from now? I highly doubt it.

I agree that if you can’t make the jump from $2000 to $2200 you are in deep stuff. I would jump on this in a minute. I can see how the banks might not be so happy but they do get the 30 years of interest to make it back.

Anybody know what a 10 and 2 ARM is?

Will the new prices, if the banks follows the rules, be reflected as the NEW price? Or will the old price still be listed?

Bababooey, don’t believe much in high end prices staying high. My personal observation is that in exactly this moment prices on west side are going down very very fast. You are right that prices in the gheto have crashed first. What is happening from here , there in the getho sales start to pick up a bit and this is “demand killing” on the more afluant areas. What I mean buyers in Beverly Hills will start to pay atention to faster falling prices in Santa Monica, in Santa Monica at Torrance, in Torrance at Carson, in Carson at Compton, Compton at …. There is demand killing at cities which have kept the prices intact. Ultimately the proportion of the prices will have to remain the same. I mean in Beverly Hills 3 times more expencive than the gheto. Otherwise “the invisible hand” is coming and will produce this ripple efect to adjust prices. Watch and see how the slump in East LA afects Santa Minica. This is waht explanes the fact that thru the last RE downturn all started at East and ended at West side.

I believe this time there will be a lot of fraud, but not to prop the apraisals , but to supress them. Some people “our people” will arange aginst the interst of the banks lower apraisal and refinance in very beneficial terms. For most of the FB there is no hope as the doc pointed out.

look, i am not advocating these prices, quite to the contrary, but i check the MLS almost daily, and sure you see a property reduced $15,000 dollars that is about it. so don’t get so damn defensive. the fact is people want to live in LA and their is alot of hollywood money and old money, money that will allow a 28 year old to buy a 1.8 million dollar house because his/her parents can afford to foot the bill. further complicating matter are the legion of foreigners who, with the currency debacle are buying everything up. one need only look at what is going on in westwood. that dont call it little persia for nothing.

I heard two bank ads on my drive home today in the southland:

example 1:

I think this was an ad for bank of the west: “you carefully guard your money and we understand, we are careful in our banking philosophy also, we have x amount of assets etc.”.

example 2:

“we will give you free concert tickets! free concert tickets for banking with us! ‘feel the woo'”. This was obviously an ad for wamu.

Now for all I know the other bank may be just as insolvent as wamu, but what a difference in the tone of the ads. I think I’ll go for free concert tickets and a free FDIC bailout thrown in for good measure. On second thought, no I won’t.

People worried because nicer areas aren’t coming down as quickly have to remember a lot of them are option arm and alt-a areas.

What is your opinion about this response.MMM

Thank you for contacting me regarding the current foreclosure crisis. I appreciate hearing from you.

I am pleased that the Housing and Economic Recovery Act of 2008 has passed Congress and was signed into law on July 30, 2008 as P.L. 110-289.

Although this legislation will not solve all the problems in the current crisis, it includes wide-ranging measures to help stabilize the housing market, provide help to homeowners and renters, and help get our economy back on track. The new law also helps communities that have been hit hardest by the foreclosure crisis by providing $3.9 billion in emergency assistance to purchase and redevelop abandoned and foreclosed properties.

I am enclosing a document of frequently asked questions , which I trust will explain the way the bill will work.

All of the costs of this legislation are covered by revenue-raising provisions within the Act, ensuring that P.L. 110-289 meets pay-as-you-go standards. The Hope For Homeowners program is narrowly tailored to keep families in their homes. No speculators, investment properties, or second or third homes will be refinanced. Similarly, lenders will have to take a significant loss on the original loan, waive any penalties or fees, and help pay for the origination and closing costs of the new loans.

The goal of this bill is to help keep families in their homes and stop the further deterioration of the communities we hold so dear. I will do everything in my power to make sure this bill does that job, but if more legislation is needed I will not hesitate to fight for it.

Again, thank you for writing to me. Please do not hesitate to contact me in the future on this or other issues that concern you.

***

ABCs of the “Housing and Economic Recovery Act of 2008”

On July 30, 2008, the President signed into law the Housing and Economic Recovery Act of 2008 to address the ongoing housing crisis. Although the crisis will not end with this legislation, it is an important first step to help keep families in their homes and stop the further deterioration of the communities being hardest hit.

Q: How will the law help struggling homeowners keep their homes?

A: Through the Federal Housing Administration (FHA), an estimated 400,000 borrowers in danger of losing their homes will be able to refinance into more affordable government-insured mortgages. The program offers government insurance to lenders who voluntarily reduce mortgages for at-risk homeowners to at least 90% of the property’s current value.

Q: When will the program begin?

A: The program will begin on October 1, 2008 and sunset on September 30, 2011. H omeowners in danger of losing their homes before October 1, however, should not wait to contact their loan servicers and should begin applying for federal ly insured mortgages now.

Q: Who is eligible?

A: To be eligible to participate in this program, a borrower must:

Have a loan on an owner-occupied principal residence. Investors, speculators, or borrowers who own second homes cannot participate in this program.

Have a monthly mortgage payment greater than at least 31 percent of the borrower’s total monthly income, as of March 1, 2008.

Certify that he or she has not intentionally defaulted on an existing mortgage, and did not obtain the existing loan fraudulently.

Not have been convicted of fraud.

Q: How can a homeowner access this new program?

A: Homeowners or a servicer of an existing eligible loan need to contact an FHA-approved lender. The FHA-approved lender will determine the size of a loan that a borrower can reasonably repay and that meets the requirements of the program. If the current lender or mortgage holder agrees to write-down the amount of the existing mortgage and make the new loan affordable, the FHA lender will pay off the discounted existing mortgage. Loans provided under this program must be 30-year fixed rate loans.

Q: Are lenders required to participate in this program?

A: No. The program is completely voluntary for lenders, investors, loan servicers, and borrowers.

Q: How does this law help neighborhoods that have been hit by the foreclosure crisis?

A: The impact of the current crisis has not been isolated to individual borrowers or investors, but has been felt broadly by neighbors, communities, and governments across the nation. The law strengthens neighborhoods hit hardest by the foreclosure crisis by providing $3.9 billion in Community Development Block Grants to states and localities to buy foreclosed homes standing empty, rehabilitate foreclosed properties, and stabilize the housing market.

Q: Will this law be a bailout for speculators, homeowners, investors, and lenders?

A: No. It is narrowly tailored to keep families in their homes. For example:

Only primary residences are eligible: NO speculators, investment properties, second or third homes will be refinanced.

Investors and lenders must take big losses first in order even to participate. The owner of the old mortgage can get a maximum of 90% of the current value of the home (which presumably will be considerably less than the value of the original loan). In many cases the loss will be significantly greater, but 10% is the minimum.

In addition, lenders must waive any penalties or fees, and help pay for the origination and closing costs of the new loans.

Most homeowners will have seen the equity in their homes disappear before being able to refinance under this program. In addition, the FHA will get a portion of any future profits on the house, to make sure the government recoups its investment over the long run.

Q: Will this law reward families who bought homes they could not afford?

A: Many homeowners facing foreclosure were misled, were deceived, or were in other ways the victims of unfair lending practices.

To prevent future abuses by lenders, this law will establish a nationwide loan originator licensing and registration system to set minimum standards for all residential mortgage brokers and lenders. It also strengthens mortgage disclosure requirements to help ensure that borrowers understand their mortgage loan terms.

Q: How will this law make it more affordable to own a home?

A: There are a number of provisions that will make homeownership more affordable:

Creates a refundable tax credit for first-time homebuyers that works like an interest-free loan of up to $7,500 (to be paid back over 15 years).

Grants states $11 billion of additional tax-exempt bond authority in 2008 that they can use to refinance subprime loans, make loans to first-time homebuyers and to finance the building of affordable rental housing.

Raises conforming loan limits for the FHA, Fannie Mae and Freddie Mac to $625,500. Because of the high cost of housing in California, a majority of the state’s residents were previously shut out from these programs. Raising these loan limits will lead to lower interest rates on some loans, greater refinancing opportunities, and enable more borrowers in high cost areas to avoid the type of nontraditional and frequently abusive loans that led to the current crisis.

Provides couples using the standard deduction with up to an additional $1,000 deduction for property taxes ($500 for individuals).

Q: Does the law provide help to those who still cannot afford to own a home?

A: Yes. The bill includes a number of provisions to increase the supply of affordable housing, which has been a major problem in California pre-dating the current foreclosure crisis. For example:

The bill creates a new permanent affordable housing trust fund – financed by Fannie Mae and Freddie Mac and not by taxpayers – to fund the construction, maintenance and preservation of affordable rental housing for low and very low-income individuals and families nationwide in both rural and urban areas.

In addition, the legislation provides a temporary increase in the Low-Income Housing Tax Credit and simplification of the credit to help put builders to work to create new options for families seeking affordable housing alternatives.

Barbara Boxer

United States Senator

Give it another 6 months and the REO’s that are sitting around empty

will be “given” away. I have got one of those dumps around the corner

from where I live. It looks ugly on the outside and has been completely

gutted inside. The dumbest thing they could have done was to put

a sign in front of the house stating that this an REO.

Every homeless bum in town has been to the house and took

whatever valuable metal items they could find and/or manage to

pry out off the walls. No wonder the REO’s are getting cheaper and

cheaper…

Gael, that’s a very tall man with a bloded morggage weight around his neck. LOL

Sorry Gael I couldn’t resist. I don’t know, I’ve never herd of that before. Sounds like tipical morggage mumbo jumbo that got us here in the first place.

L A is in for a price shock as is the rest of so. Cal. One of the major reasons is what the econemy is based apon. Cities like San Francisco, Chicago, Boston & New York are not totally dependent on real estate & visitors from out of town to support the econemy. Now don’t get me wrong, every city can benifit from tourests, but some places like Los Angeles are overly dependent on it. Same could be said for real estate & all that comes with it.

Because this area does not have the corporate foundation that the other cities I posted above have had for decades, the 8 county region needed to build welth in some other way. Freeways, malls & housing tracks as far as the eye could see, were the corner stone for the whole area’s existence. Now that foundation is coming undone, & people are not prepared for the aftermath.

Trust me on this one, all you need to do is look at Las Vegas right now. The city that could is now in a tailspin. Unfinished housing tracks, bankrupt highrise condos / hotel towers, an 80% occupency for current hotels when it was near 95% a few months ago & 12% of all flights are being cut by the airlines. no matter how you slice it, it is not pritty.

We are one of those unfortunate Californian families that got into one of those nasty option arm loans. We got ourselves into this mess. We don’t blame anyone but ourselves.

When our loan resets in February, we are either looking at a foreclosure or a short sale. Based on what I am reading, the housing bill is not going to help us much. We owe a little under $360,000 on our home. Todays value is probably about $225,000 That means we are upside down $135,000.

Like I said, there is nobody to blame but ourselves.

Does anyone miss Gray Davis now?

I would if I was living there.

Arnold cuts back on wages.

That’s gonna throw a lotta people upside down.

It’s diabolical.

Pissing gasoline on the campfire.

Government is supposed to cut in good times and spend in bad.

Wow!

I’m glad I live in Canada.

Walking away from a property may not be advisable because of the tax effects. Assume the value of the property drops from $800K to $400K and the note is for $800k. The homedebtor walks away, jinglemail. The bank sells the property and takes a $400K hit. At this point, the bank has given the homedebtor a “present” of 400K. This is taxable income. The IRS will demand the homedebtor pay tax on this present, maybe $125K. If they cannot pay come next April 15, interest on the delinquent tax accrues at 12-18%. So even if you can take a hit on your credit by walking away, you will still have to come up with a sizable chunk for the IRS almost immediately.

Mike P,

To my knowledge it is only forgiving if it is a short sale. Remember California loans are non recourse and the house is the only collateral.

@Mike P

Not necessarily. California is a purchase money ‘non-recourse’ state, meaning that if that loan was used to buy the house (and was not a refinance) there is NO 1099 issued. The bank eats it. Also, in 2007 some IRS rules were changed regarding when banks can issue 1099’s. Ask your accountant – since it’s August, he’s probably getting ready for a fishing trip and isn’t overly burdened by filing tax returns.

All these government bailout attempts? I just get this image of a drowning man underwater, trying to gasp air through a straw, and the ‘rescuers’ come along and just attach another straw, so he can sink even lower. Meanwhile, the rescuers buddies are going through the backpack left on the beach and taking the drowning man’s wallet and Maui Jim sunglasses.

Not true. President Bush signed a bill that already amended the tax code in January 2008 so that the homedebtor no longer has to pay the IRS for the “Phantom Tax” on a primary residence.

http://www.govtrack.us/congress/bill.xpd?bill=h110-3648

Leave a Reply