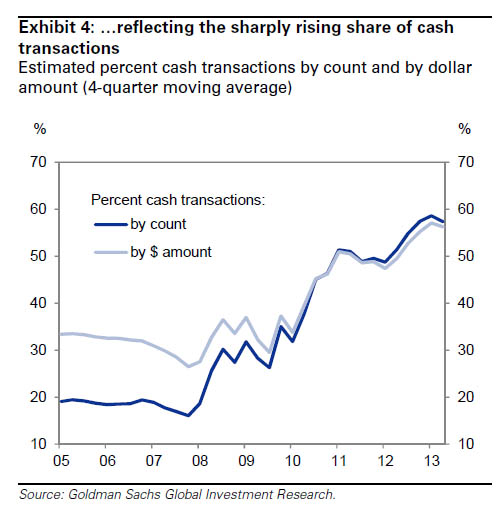

The majority of home purchases are now being done by cash buyers: Destroying the myth that cash buyers are a small portion of the market. 60 percent of homes sold in 2013 came from the all cash crowd.

There was an odd sort of myth floating around the market that the cash buyer crowd was somehow a tiny portion of the market, like a drop of water in the vast ocean of home buying. This delusional dream played into the fantasy that this housing market was naturally rising because of overall household demand when in reality, it is being driven by investors leveraging the artificial low rates created by the Fed. The flood of money from Wall Street has been large. Even anecdotally, it was apparent that cash buyers were driving the market given that housing is a margin driven market. That is, at any given time only a small portion of all homes are on the market for sale. However, an analysis by non-other than Goldman Sachs shows that 60 percent of all 2013 home sales are being driven by cash buyers. That is, the middle class is largely being pushed out of this game and has become the minority in this real estate market. Let us look into the data more carefully.

Cash buyers only a small portion of the market?

I think the myth of cash buyers being a small part of the market fed into the meme that the housing market was “organically†going up on the underlying power of the economy. In reality, the market has been bubbling up because hot money is voraciously fighting over itself to eat up whatever inventory is available. The data now being released confirms how massive the investor portion of the market is:

“(WSJ) More than half of all homes sold last year and so far in 2013 have been financed without a mortgage, according to an analysis by economists at Goldman Sachs Group.

The analysis estimates that around 20% of all homes sold before the housing crash were “all-cash†sales (or around 30% of sales by dollar volume). But over the past seven years, the all-cash share of sales has more than doubled, increasing by more than 30 percentage points, according to economists Hui Shan, Marty Young and Charlie Himmelberg.â€

Think about this more carefully. Even with the median home price of $214,200 families still need to finance the purchase. The above chart clearly shows that investor money is really driving the bulk of the housing market. The low rates promoted by the Fed were cast under the umbrella of helping out regular families but in reality, they have turned into the next hot money play for banks, hedge funds, and Wall Street. The fact that 60 percent of all purchases in 2013 are being driven by the cash crowd is crazy (a 200 percent increase from the 20 percent pre-crash levels). The WSJ article goes on to say:

“There’s no exact way to know who is responsible for all of these cash purchases, though they are likely to include some combination of investors, foreign buyers, and wealthy homeowners that don’t want to go through the hassle of getting a mortgage before closing on a sale. Mortgage lending standards have sharply tightened up since the housing bubble, with banks scrutinizing borrowers’ tax returns and bank statements to verify their incomes and the source of their down payment.â€

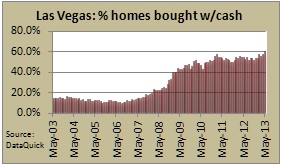

We’ve talked about this for years but the current percentage is stunning. It is safe to say that your mom and pop American buyer is not eating up all these properties for all cash. Just take a look at the cash buying in Las Vegas:

This incredible trend also helps to explain the massive drop in mortgage applications but the rise in actual home sales:

Source:Â ZH

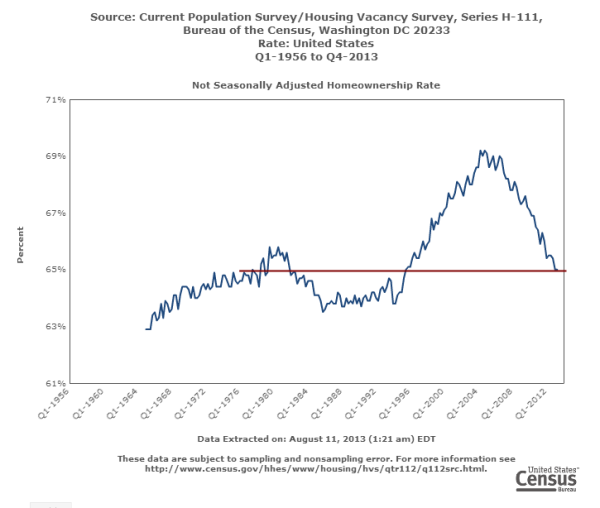

Some have argued that the “all cash†crowd isn’t really all cash which may be true in some transaction but the above chart clearly shows that mortgage financing has fallen dramatically since 2012 (below pre-crash levels). This of course has occurred at a time of record low interest rates. So the idea that low rates would spur your regular Joe and Jane to buy homes doesn’t seem to be occurring.  Unless Joe and Jane have hundreds of thousands of dollars sitting around (which of course, is not the case). Of course this also helps to explain the dramatic falling of the home ownership rate as well:

Yet this unrelenting amount of investor buying has crowded out people in various markets. Even in California where property prices are rising dramatically and some areas are having homes sell at record levels, the cash buying crowd is at record levels (roughly 30 percent of purchases in one of the most expensive states in the country).

So much for the myth that the all cash crowd was a small portion of the market.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

96 Responses to “The majority of home purchases are now being done by cash buyers: Destroying the myth that cash buyers are a small portion of the market. 60 percent of homes sold in 2013 came from the all cash crowd.”

This is all about taking the bad loans out of the bankrupt banking system, along with liquidating the CDOs mortgage instruments fraudulently sold by the big boys, and turning the poor suckers into renters paying way over market levels because they cannot make use of the “cheap” money due to bad credit and/or no well paying job. The Fed has created this bubble by a magnificent whipsaw, free money for the big investors and zero interest rates to drive money out of traditional savings. Greatest robbery done by wealth transfer in the history of mankind, and it is not over yet. There are still a few drops of blood in the stone. However, with interest rates sky rocketing and the Fed losing control, it may all just crash way sooner than most expect.

Most cash investors eventually need to sell in order to realize a return. They can’t just keep selling to other cash investors — eventually they need to sell to an individual with a mortgage. Now that the pyramid scheme is showing signs of cooling, watch what happens.

Home ownership used to be something people did when they wanted a permanent place to live. The banks wouldn’t let someone buy a place if they couldn’t afford it. Now home ownership is a Las Vegas casino. Endless outside forces control the game — the Fed controlling interest rates; banks controlling the mortgages; hedge funds controlling the inventory; real estate agents hawking the news (when prices were falling it was ‘the best time to buy.’ Now that prices are rising it’s ‘the best time to buy.’ In case you haven’t figured it out, no matter what is happening in the market, now is always ‘the best time to buy.’)

Who wants to buy a house in this environment? Why not rent a nice place and let this desperation play itself out. No thanks.

actually that’s not true. as long as the incoming rents yoy are making a profit, that’s what matters.

Yoblah is correct, and you and your fellow renters make it work for us investors.

I didn’t pay cash, but did put 30% to 35% cash into two foreclosures that I bought as investments. After I cleaned the units up, I rented them. My net rental income is high enough that I’ve accelerated my mortgage payments so that they will be paid off in 7 to 10 years. After that I will enjoy the net rental income in my retirement. It sure beats earning .25% in the bank! My wife will have the income when I die and our families will ultimately decide what to do with them.

Remember, not all investors plan to flip homes.

It can be more complicated than either of you are leading on. If there are new investment opportunities that arise which offer a better return, and current holdings become relatively less attractive, an investor then has an incentive to lock-in any realized gain by selling and in the case of income property, forfeit the income stream.

you’re exactly right I have been saying and warning people about this since early 2009 that this was all coming down of course back then hardly anyone knew what I was even talking about they were still busy blaming Busboys and waitresses that had the audacity to buy into the American dream as if it was their fault that we had the world financial collapse glad to see people paying attention now it seems almost common knowledge what the banksters did, how they’re doing it, and that it is the greatest robbery ever in the history of mankind at least since the collapse of the Roman Empire my only thought here as to theb all cash buyers, in particular and especially the small mom and pop cash buyers that maybe do have a hundred to two hundred thousand dollars in the bank and then plop it all down on a house that’s over priced due to the manipulation so instead of just losing their mortgage and filing bankruptcy they’re going to lose their cash which of course is the bankers goal!

FWIW, I still do blame those busboys and waitresses and people in general who bought more than they knew they could afford. Without them, none of this could have happened.

It all reminds me of the game Monopoly. Anyhow, it is refreshing to see comments from people showing understanding of how the bankers and hedge funds and such were the main cause, as opposed to all the bashing of individuals that previously occurred.

YoBlah…..You’re kidding right?

If I have 2 million dollars and lend it to someone who has nothing to lose if things go bad…..I the Lender am the ignorant fool, not the person who got to risk my money with nothing or very little to lose themselves. Those who were able to play with my money and take risk with my money (if I were the Lender) but lose nothing to little if it went sour were actually the smart ones.

Suckers, suckers, suckers….everywhere.

The Fed and the banks did it again.

They herded us people to the financial products they want us in. They took away the ability to earn any interest in savings accounts and herded us into their den…the stock market and the housing market.

They love all the cash buyers. It gets all the risky loans off their books onto yours. They know that they are going to pump and dump this housing market. Notice they are not stepping up to the plate to help Americans secure loans in their banks. They don’t need your loans…they got the Fed and they can play the game of trading debt with each other for profit. This is a sure thing…they almost got burned last housing collapse and they are not going to get burned-they know there will not be another bail out for the banks. It’s a big game of “hot potato” and they want to make sure you are holding the potato in the end.

Real estate inventory was held off the market so that entry level homes and condos prices would appreciate and lift them out of the red to the black, essentially making everyone think that we are in recovery. They scare you with a rise in interests rates so they can keep this over inflated inventory moving. They don’t want to be landlords…they want you to feel good about real estate again so they can sell to you. They relish multiple offers and all cash offers, they are back baby!

Their plan has worked. Prices have risen quickly, they have chummed the waters of investors to come in with all cash. The banks don’t want your money sitting in the bank…they want it in their housing market, their stock market. They want you all in. When real estate prices drop again no one can walk away from their loans if they pay all cash. Bummer for you, you just lost equity. No skin off their backs. They know these prices are not in line with any real index out there. Real estate is inflated and they inflated it in the first place and they are wicked good at these games.

Don’t play their game. There will be another housing crash in the next five years and at that time you will be able to buy again with pennies on the dollar when the people will be desperate to sell in order to survive yet another Fed/banking bait and switch trick. If interests rates go up quickly it will implode this market even faster…keep your cash on the sidelines and wait for this to happen.

Watch out for your 401k money and stock money too. This is an inflated market also and when it crashes, it crashes hard. It’s better to be 1 week, 6 months, two years too early out of the market versus a day late…is too late. You don’t have to be all in the market or all out. Take some risk off the table. Cash is not sexy now but it will prove to be a lifesaver when the market crashes. They want you to think that you are stupid not to be in their juiced housing and stock markets where they make the rules.

@Christie S and others — except here’s the thing: you MAY be largely right but your timing could be way off. And that matters.

I’ve been reading ZeroHedge for about 3 years and all of that time their articles and commenters have been saying the sky is falling any minute now. Guess what? They have been flat-ass wrong. And anyone who sat on the sidelines missed incredible gains. The stock market is somewhat a casino but, there are companies trading of real inherent value and growth potential, as there always have been.

Oh, and I don’t recall one blog I read having predicted the real estate inventory shortage or subsequent price run-up in 2012-2013.

So, the track record of most of the online human predictors has been lousy. Food for thought.

Point well taken Prediction Reality Check.

No one should blindly follow anyone without a good understanding of what backs up those beliefs. My entry is only to give a different point of view of my opinion, my results from my research. Even the best of the best can only say something will happen not when. You have to be vigilant.

If you put yourself in the shoes of the banks who want to make money, it is a little easier to see how they may mislead investors or not fully disclose their strategies for making money. They don’t blog on what crooks they are.

Wealth is never gone it is only transfered.

“..Most investors now believe three things about the Federal Reserve, money and interest rates. They think that the Federal Reserve is artificially depressing rates below what would be a “normal” level. They believe that in the process of doing so the Federal Reserve has enormously increased the supply of money and they believe that the USA is on a fiat money system.

All three of those beliefs are incorrect. One benchmark rate that he Federal Reserve has absolute control of is the rate paid on reserves deposited at the Federal Reserve. That rate is now 25 basis points, after being zero since the inception of the Federal Reserve in 1913 until recently. If the Federal Reserve had left that rate at zero t-bill rates would now be even lower than they are now. The shortest t-bills rates would now probably negative.

Paying interest on reserves combined with the subsidy to the banks of providing free unlimited deposit insurance on non-interest bearing demand deposits is keeping t-bill rates positive. Absent those policies the rate on t-bills would be actually negative. The Chinese and others all over the world are willing to pay anything for the safety of depositing funds in the USA. Already, Bank of New York Mellon Corp. has imposed a 0.13% charge on large deposits.

An investor who believes that interest rates are headed up may respond that the rate paid on reserves is a special case and that the vast increase in the money supply resulting from the quantitative easing must result in higher rates when the Federal Reserve reverses its course. The problem with that view is that the true effective money supply is still far below its 2007 level.

Money is what can be used to buy things. Historically money has first been specie (gold and silver coins), then fiat money which is paper currency and checking accounts (M1) and more recently credit money. The credit money supply is what in aggregate can be bought on credit. Two hundred years ago your ability to take your friends out to dinner depended on whether or not you had enough coins (specie) in your pocket. One hundred years ago it depended on the quantity of currency in your pocket and possibly the balance in your checking account if the restaurant would take checks.

Today it is mostly your credit card that allows you to spend. We no longer have a fiat money system. Today we have a credit money system. Just because there is still some fiat money does not negate the fact that we are on a credit money system. When we were on a basically fiat money system there was still a small amount of specie in circulation. Even today a five cent piece contains about 5 cents worth of metal, but no one would claim we are still on a specie money system.

Fiat money is easy to measure; M1 was $1.376 trillion in 2007 and was $2.535 trillion in May 2013. The effective money supply is the sum of fiat money and credit money. Credit money cannot be precisely measured. However, When the person in California whose occupation was strawberry picker and who had made $14,000 in his best year was able to get a mortgage of $740,000 with no money down and private equity could buy a company like Clear Channel in a $20 billion leveraged buyout, also with essentially no money down, the credit money supply was clearly much higher than today. A reasonable ballpark estimate of the credit money supply is that it was $70 trillion in 2007 compared to $50 trillion today.

The effective money supply is the sum of the traditional fiat money aggregates plus the credit money supply. Thus, despite the clams of Ron Paul and Rick Perry to the contrary, the effective or true money supply has fallen drastically over the last few years.

http://seekingalpha.com/article/1514632-federal-reserve-actually-propping-up-interest-rates-what-this-means-for-mreits

WTH are you talking about!?

Next you will be saying inflation is really low, GDP is really growing, and unemployment is dropping. The Fed has our best interest in mind, and anything can grow to the sky!?

Have you ever heard of our fed/treasury buying its own debt?!?

When Bond holders get wise, it won’t matter what captain Ben and company do..

The game will be over and you will be eating your words!

Well stated fulano. I totally agree with your analysis.

The only controversial aspect of this is: are these cash buyers being funded by the narco-traffickers (banking drug cartel)?

you nailed it greg burton.

Quite possibly, and NONE of the pudgy overpaid federal “regulators” are even looking in that direction.

Certainly for 40+ years here in So-Fla, Central & South American narco profits have found high-rise condo/hotel/office tower projects to be the perfect way to launder large bundles of $20 bills. Think about it–an LLC or other type privately-held corp. is created just for the duration of building the one project, HUNDREDS of millions of dollars flow through this entity in 18 months, and none of it falls under the purview of SEC, FINRA, FDIC, OCC, etc… even the IRS is only interested in the output end, not the inputs.

Duh Trump name may be on 3 (4?) high-rises along Miami-Dade’s posh beach/bayfront, but I guarantee each was erected by a different working corp. (now folded), and no one in Trump’s back office was doing background checks on the “investors”.

Additionally, consider the increased danger/distortion of an inflation caused by narco-profits, i.e. since their margins were so enormous (400%??) on the “dirty” side, even if their front-man (hedge fund) loses 25% on their landlord venture, they’re still way ahead, and can now freely move their “clean” money anywhere else. This would, perhaps, explain some of the overpaying and bidding wars (and related RECKLESS/frenzied behaviors) seen since 2011.

Yeah… no high-rise projects started for 7+ years now… burlap bags of cash literally piling up… security issues… fire danger too, lol. Yep, the more I think about it, the more inevitable it seems that narco-dollars must be flowing to alternate vectors of the RE market.

Wow! This is why I use “What?†as my handle. Financing is financing regardless if it is a mortgage to Joe six-pack or if it is a TBTF bank lending to a hedge fund manager or if it is a short term business loan to a flipper or if it is a personal loan to the rich. How can anyone miss the fact that the balance sheets for all of these folks have the same liability?

The point that everyone seemed to miss is that this housing increase is false because of the financing not because of the cash! The cheap money is financing the bubble more than the cash chasing returns. Has anyone followed the stock market over the past 5 years! What is the cost of ownership of a stock versus a house? I agree the stock market is most likely going to crash in the future but so will the bond market, the housing market, the tulip market, etc. This is why I argue that the Fed can never ease up on free money. It is the only game in town. This is why I laugh at the idea of closing the GSE’s, the only mortgage financing game in town for those who still have a mortgage.

There has been no real change since the crash. There has been no recovery. The market craps in its pants when it thinks that the Fed will taper. We are not talking about the unwinding of this massive monetary stimulus. We are talking about the slowing of the epic growth of this massive monetary stimulus. “Good†economic news scares the be-Jesus out of the bond and stock market all because we are talking about the slowing of this epic growth. Really??? This has just been a real epic game of kick the can.

so are we in a bubble??? will it pop? cash buyers dont use leverage….doesnt leverage cause bubbles to pop??? this market is nuts and it looks like it’s just getting started. New construction projects are pre-selliing out entire phases, phase 2 price is $50,000 higher than phase 1….just go buy 2 new homes sit back 1 year and sell them, you can make $100,000….this is insanity…but it’s not leverage insanity? is it? My head hurts trying to figure this all out….

Blackstone may be using “cash” but it is OPM, not cash they had sitting around.

What is OPM?

Other People’s Money?

Start with the foundation then go from there. I unfortunately took down my website that educated everyone on how this robbery is done. Its done with everything not just houses. Begin with watching the documentary Money As Debt. A good 101 financial education starting place. Prepare to have your world revealed. Kind of like eating the red pill in the Matrix. GL it’s a deep rabbit hole.

If nothing else, the producer of Money As Debt should be commended for the public service provided in sparking the critical thought process of many on this subject matter. On the other hand, there are some holes in the presentation, especially when it comes to banks spending capital from interest earnings back into the economy.

PS I do have the documentary posted in my Playlists on my YT channel @ http://www.youtube.com/TheeLynnChase if you want to check it out.

@Appraiser CA wrote: “…cash buyers dont use leverage…”

Au contraire, cash buyers do use leverage.

Here’s how the leverage works:

1.) Cash buyer pays for a property with 100% cash.

2.) Cash buyer then refinances to get cash out of the property. Depending who the cash buyer refinances with, they can pull cash out any where from 95% to 80%.

3.) Cash buyer then moves on to the next property.

4.) Repeat the process by going to step #1.

This mortgage quick allows cash buyers to exercise maximum leverage.

What I meant is “quirk” not “quick”.

What I failed to clarify is refinancing out takes many forms. The “cash buyer” can refinance out of a 100% cash purchase by selling bonds, shares and/or getting a loan. This is where the leverage comes in.

So, all cash purchases are not what they seem to be.

What is brewing currently in the housing market is A) Unprecedented, B) A lot different that the 2004-2006 run up with everyone buying 0 down Option ARM mortgages not paying any interest.

The worst outcome that will come from a market of primarily Cash buyers.. is simply to create a HARD BOTTOM in the housing market. Cash buyers don’t walk away from their homes. Cash Buyers don’t sell for a significant loss if they can help it, they will all rent it out before taking a loss.

This is really about screwing those with bad credit or not enough income and forcing them to rent FOREVER.

I’ll bet Section 8 is going to go up 10 or 100 fold over the next decade or two while subsidizing all these new immigrants or the new illegals. I bet the best places to have rentals is near fast food, convenient stores or your big box stores where they need cheap labor to keep the party going. Might need to start checking on the new Section 8 vouchers being created and also how many new landlords are accepting these type of renters. Then we will likely see what the real plan is.

The successful rentals will always be in high traffic areas and is located strategically where they will rarely have a unit un-rented for a long time. Those are your FOREVER rental locations. Other places good luck, but there is only so many places that are desirable rentals.

Now this post makes a lot of sense. The hard bottom is gonna make it tough for many families to buy a home in the future.

I disagree. You forget that house prices are set at the “margin.”

Approximately 15 million units in California and even if this madness goes on for three years, only 1.5 million units will be transacted on (approx sales in CA are 500,000 units a year). Of these, only about 800,000 will be bought in cash over such a hypothetical 3 year, 60% cash buyer streak.

This leaves the other 14 million units that were never bought or sold during this mania, many belonging to aging boomers that will need to downsize.

What is again forgotten here is that houses are priced on the margin and their only hard bottom is set by financing / wages.

Cash buyers will sell at a loss much more easily then mortgage holders. The crash will be much more severe. That is already happening in Europe.

No different than someone buying into the stock market. There is nothing to support the investor if they make a bad bet. Why should housing be any different. Look at Detroit.

“The low rates promoted by the Fed were cast under the umbrella of helping out regular families but in reality, they have turned into the next hot money play for banks, hedge funds, and Wall Street.”

True, but I’d like to see a chart of how many families refinanced at 4.5% or below…this probably has had a dramatic impact on cash flow for millions. Those would-be bag-holders from 2009-2011 should have alters of the bernanke in a special corner of their homes thanks to his antics.

I’ll bet that number is lower than you think. How many qualify for a lower interest rate refi if they’re underwater, or their income doesn’t qualify, or they’re self-employed, etc.?

I suspected this all along but thanks for shining the spotlight on this. How will this game end? This endless supply of free money has to end someday. I wonder how that will happen and what the impact will be on the housing market.

We have enough money saved up for a downpayment but I refuse to play the bidding game (In San Diego). Our plans were to buy a place and stay put for atleast 7-10 years. My fear is that this game is not going to end anytime soon and when it ends, it is going to take 3-4 years for prices to bottom out.

Tensions are running high at home since my better half things we already missed the boat and last year’s prices are never going to come back… Not really sure how to proceed from here…

Appreciate any inputs. Thanks!

It is never possible to guess how speculative games will turn out. Unfortunately, you never know what is the best time is to buy, sell, hold etc. except in hindsight. That is because the price of any asset class, like real estate, is determined by the sum total of the emotions of all the people who are buying and selling that asset class. Think about how hard it is to predict the emotions of one person, let alone thousands of people.

I say go with your gut. In a marriage you have two decision makers. Either one should have veto power over major purchases – especially large speculative ones. If one is feeling too nervous about it then taking a pass is the right decision.

It’s still a good decision no matter where prices go, because the decision process was fair and sound.

I hope this helps.

@Analyst — I read your post after I had written my comment above. You are smart, correct and have a cooler head than most. Please keep posting.

Madison, many people on this blog share your frustration (I did too before finally throwing in the towel and buying). From the last five years, nobody and I mean NOBODY could have predicted how things turned out in the housing market. Who could have predicted low 3% rates, QE on steroids, banks withholding inventory, cash buyers up the wazoo, etc, etc? This tells us that NOBODY has any idea what lies ahead. What you need to focus on is the facts you have in front of you today.

You have a downpayment. You plan on staying for at least 10 years. I assume you have somewhat stable income, good credit and emergency savings. If the area you are looking at is close to rental parity, it might make sense to buy. Rental parity is always a good measure of how under/overvalued properties are. Things didn’t make any sense in 2006, but looked really good in 2011.

Housing is truly a tangible asset, especially in desirable parts of California. This asset looks pretty good when compared to cash, treasuries, precious metals or stocks. It all might be a casino, but at least you can live in a house. Additionally, homeowners will always be favored over renters…this will never change.

My question for you is what would compel you to buy? Lower prices, higher rates, more selection, less competition? Good luck in whatever you decide.

“nobody knows what lies ahead” + “homeowners will always be favored over renters” = does not compute

Joe, I’ll go out on a limb here and proclaim renters will NEVER be favored in our society. How’s that?

In the corner of home owners we have: the fed, politicians, the elite, the connected, lobbyists representing many industries tied to housing, the majority of the country, etc.

In the corner of renters we have…I don’t know.

How does that compute?

It doesn’t because you contradict yourself.

>> In the corner of renters we have…I don’t know. <<

Tenants wield a lot of political power, locally. Ask any landlord in New York or Santa Monica. I recently read that 70% of Santa Monicans are renters. Hence, strict rent control.

In New York City, landlords are required to renew leases, if the tenant so desires. Tenants can leave their rent-controlled leases to their children, grand-children, great-grandchildren … Rent-controlled landlords are essentially married to their tenants.

And it's VERY HARD and expensive to evict tenants who don't pay. Tenants have all sorts of legal delays and protections.

Sure, not all housing falls under rent control, even in rent-controlled cities. But that can always change. Should the economy go bad, should large enough numbers of tenants go unemployed, the pressure to adopt or expand rent control, and the difficulty of evicting non-paying tenants, will increase.

After the next economic crash, these all-cash buyers, renting out their houses, may wake up to find themselves living under suddenly enacted "emergency" rent control and tenant protection laws.

if you believe last year’s prices will never come back again, then you should have confidence to buy right now. You don’t want prices to go back to last year if you’re buying this year.

Analyst is right, it’s hard to predict what is going to happen in a speculative market. We won’t see the kinds of defaults we saw last time, so probably you will just see the market slow down or stabilize.

Also markets are different, and price ranges are different. I’m in central California looking at 3bd/2b SFH in the 150k range. There are 20 offers on every move-in-ready home. And homes in that range have gone up 20% in less than a year. But 250k homes are not escalating as fast.

I would be very concerned about buying a 750k + house anywhere in California right now, but we haven’t seen the top yet. It’s just A matter of what happens after we get there.

Ultimately your decision should be based on 1) your available capital 2) your budget 3) rent values compared to mortgages in your budget

Thanks everybody for your responses. I will start looking at rental parity for the places that we do see in the future. I should’ve done this math in 2010-2011 since that would’ve given me the confidence to buy (without the current challenges or rising prices, multiple cash offers etc.)

My main concern at this point is to not buy high and then watch helplessly as prices start to crater. This is what is holding me back. I do quite a bit of reading on the current state of affairs of the global financial system and bought into the meme that the next crash is round the corner due to all the leverage floating around. I was happy when rates started going up since that would mean prices will have to come down. I don’t see it happening in San Diego.

So to summarize, we have a downpayment, have emergency savings and reasonably stable jobs. This fear of another downturn and falling values is not letting me commit :-(. Like Analyst, MikeB and LordB pointed out, I have to learn to accept the fact that no one can “really” predict what comes next. Look at the existing facts and come to a decision. Thanks again guys.

Madison,

I’m in the same boat as you. Here’s a very, very interesting blog from a respected player in the mortgage market – http://mhanson.com/blog. Mark Hanson says what is already happening with the huge rise in rates will negatively affect the RE market much more than the Homebuyer tax credit back in 2010 (the existing homebuyer chart above in this article shows how the market tanked in Summer of 2010 after that credit expired). He believes, as I do, that what is unraveling now is the greatest monetary experiment in the history of the world (QE, Twist etc.) and its reprecussions are very likely enormous. However, he also says that the data will not show what is currently unraveling until the fall because of lag time in reporting. Everyone should take a look at this blog.

Not all cash buyers are really cash buyers:

“Blackstone, the largest real estate private equity fund, just consummated a $2.1 B loan via Deutsche Bank AG. Blackstone has already invested over $3 B into the purchase of single family homes since 2012 for use as rental properties. This new loan will allow the group to take down another $2 B of inventory over the next 2 years.”

The biggest buyer, of course, is the Fed. The Fed has been buying up $40 billion in impaired Fannie and Freddie MBS, at full face value, every month, and it has been keeping the houses that collateralize those toxic MBS off of the market. This has been a boon to the TBTF banks and hedge funds. For instance:

“The biggest hedge fund winner in 2012 is the New York-based Metacapital. Its “Mortgage Opportunities Fund†has squeezed a 520 percent profit on the year by betting on housing price increases owing to the Fed’s purchase of Fannie Mae and Freddie Mac mortgage bonds.”

“Some have argued that the “all cash†crowd isn’t really all cash which may be true in some transaction….”

I have heard this as well. Anyone know more about this?

I’m a SoCal refugee…retired…sold my paid off home of 25 years for way more than what it was worth to a guy who paid $25k over his 100% VA appraisal. I then bought with cash in Idaho a much, much nicer custom home. Reading Dr. Bubble helped me a LOT with timing my sale.

I have another retired pal ….also a CA refugee…..who cashed out a sizable chunk of his 401-k and took the tax hit simply to put a bigger portion of it into an all cash transaction for a new home purchase in CO. With 10,000 boomers per day turning 65, you’ll see more retirees abandoning the paper asset markets featuring high-risk piddling returns and turning to hard tangible assets. It’s an especially compelling strategy if your next unplanned move is to the undertaker’s.

I hope this is helpful to your understanding of one overlooked segment of the all cash trend.

That does help a little, but it was implied to me that a number of these cash purchases are made where the cash may not exist (ie. loans). In the case of cashing out a 401k, at least that money is had…somewhere.

I call BS on this story! Complete BS! Unless the “cash buyers” are the Federal Reserve/US Government. The entire housing market is a rigged casino right now.

Thanks, really interesting and I knew the percentage was somewhere in that range locally in northern Calif. but had no idea the national figure was that high. I experienced this first hand, tried to buy for a year and my offers (20% down, at or slightly above asking price ) were ignored in favor of 100% cash bids every time, gave up a year ago. Have seen the arguments that the money isn’t really all cash as it was borrowed somewhere but this makes no difference to the seller and does not help anyone who needs to buy with a mortgage.

It makes sense why cash buying investors and flippers are snatching up these homes all-cash. When a cash buyer will pay 5-10% over comps and appraisal, it leaves the conventional and FHA buyer hanging and left to bid on the next property that can piggy back that sale as a reason to mark up their home to new unbelievable heights.

This means when this bubble crashes, there won’t be as many defaults as last crash, which probably means prices won’t crash as steep as previous. But it has once again put the middle-class family in a position where they have to over-bid and over pay for these homes and are the ones most at risk when this market slows down. Cash buyers definitely tartget the bottom price ranges for homes and that again leaves middle class families out to dry and forced to pay insane, irrational mark ups to get into a home.

I’ve been in the market for the past 8 months as an FHA buyer in the 150k range in California and of my 20 or so offers (all above asking price), at least 14 of those homes went to all-cash, sometimes not even as the highest bidder, though. It was clear early on that irrational forces (cash, speculation) were driving this market and the prices up at insane rates. How is it good when assets change in “value” by 20% in less than a year? The same house in January for $140k is now 170k. I’m not going to play the game anymore.

Check out this graph that shows a HUGE drop in mortgage applications!

http://www.silverdoctors.com/get-ready-the-great-transfer-of-wealth-in-gold-silver-is-coming/

From Silverdoctors:

Furthermore, the housing market is about to hit a brick wall, “Mortgage Activity Plunges 50% to April 2011 Levels.†We can see from the Zerohedge chart below, that existing home sales (shown in brown) are about to fall in a big way as mortgage applications have dropped to three-year lows:

The continued health of the housing market is based on low-interest rates. However, bond rates have been rising substantially over the past 3-4 months which impacts the mortgage rates for the housing market. Since May, the 10 year U.S. Treasury yield has increased a staggering 63%:

FNF will probably be there to save the day or maybe not?

Wow! No one is getting the ramifications of what I am saying. It is still an almost all financed bubble just not through the mortgage market. This crash will be just as bad because funds will dump the asset without foreclosure laws to slow them down. The banks will be looking to socialize these upcoming losses. And to add insult to injury, your 401ks and pension funds will be holding these new toxic assets. NOTHING HAS CHANGEED!!!

We all know that the big guys aren’t going to take the losses and that they will be socialized to the people. I think it makes sense is that the investments, and subsequent losses to come, are in people’s 401(k) funds.

Yes, at the end of the day it’s still financed money and repercussions will be felt by all users of the system. This is why it’s so important to one’s financial health to question, seek out information, and most importantly – be skeptical when something doesn’t make sense or seems too good to be true. One problem with the housing market is that it provides easy emotional prey. Impatience is rarely rewarded.

What happens when they want/need the cash for something else?

Alright, so you guys think since they bought in cash they won’t sell. Let’s suppose you are right. But if prices fall do you think they will keep buying? If they just hold onto what they already have that is not a floor. We still have millions of homes to underwater and to be foreclosed on. Who buys those? If the cash crowd just blew their wad, they might not even have the money when the true bottom hits. There is also the danger that they do sell because the recent crash is still fresh in their memory. Nobody wants to get stuck holding the bag. They know the home they just paid $165k for was only selling at $50k two years ago and sitting on the market for months. They know they overpriced. It is better to take their losses and chase the latest hot trade where they can make it back in weeks…..

All I know is the Federal Reserve keeps saying deflation is the threat. Why buy a depreciating asset? One that was a bubble and never went back to pre-bubble prices? That is the danger of deflation. Too many people spend their cash and then don’t have it. It’s a downward spiral.

Sam, I agree with what you outline in your post!

It is interesting, again just anecdotal; however, in the past three days, I have received three alerts from Trulia/Redfin over homes which have had a recent price [reduction] in the Eastvale/Corona area of the IE. Moreover, one builder I subscribe to, alerted me to a price reduction on one of their homes in Lake Elsinore, just this a.m.

It will be interesting to see, just where the market is, right after the first of the new year, and going into next spring?

Agreed. It’s a heavy assumption to make that these more recent investor buyers (i.e. “cash” buyers) are all on a buy and hold strategy. Where are commenters forming the basis of this idea from, wishful thinking?

“One that was a bubble and never went back to pre-bubble prices”

I think of it as the SoCal housing price level that has not yet reverted back to its mean. It was on its way, and then the tax credit introduced noise, it then started back again, then ZIRP introduced more noise.

What?… Why would the funds just dump the assets? Inflation and cost of capital are interrelated. Inflation increases rents, fixed asset value and replacement costs. Low inflation and cost of capital bolsters asset value thru cheap financing.

Oversupply of product due to huge amounts of defaults is what destroyed values. But now a majority of bad loans …gone. sub-prime… gone. “0” down HELOC and ez qual… gone. The remaining ALT-A arms that hung on are now enjoying the benefits of super low rates and 20 yr amortization. With less and less people underwater there is a very limited supply of distressed sales… Couple this with the loan mods done and we are unlikely to see massive defaults for a long time.

This will constrain supply and Buyers will continue to turn to used and rehab homes (flips) until prices make sense for new construction again. However, here in SoCal the barriers to entry and increased cost of new constuction dictate value for existing housing stock.

Funds bought homes at the bottom of the market and the reverse “bubble” of artificially low prices has now popped. We are entering a more normalized market in the coming months and years where the Frenzied cash buyers exit the market and the routine “family” buyers are the majority. The “funds” of the market will fill the entry level buyer segment, and probably sell mostly to their existing tenant base.

Fore these reasons it is very unlikely that they will have to “dump” their assets. Quite the contrary.

Sorry Lebuilder you are missing the misdirection. The sorcerers trick. Still thinking the collapse was because of subprime borrowers. The myth that was sold to the masses that do not understand the real game being played. What? Is correct.

Another interesting observation regarding the current market conditions and the historic disproportional share of cash buyers.

In a “normal” stabilized market, it should not take 10 days to sell a house. 90-120 days is about average in most areas for the median priced home. I believe when we see this return to normal, there will be less cash buyers in the market and more traditional buyers. As the numbers of cash buyers begins to decline… And i believe it will, it does not mean a bubble pop, …merely a return to stabilization.

As others have pointed out, where is this “cash” coming from? Odds are it is a loan, just not a mortgage. But, theoretically, must be paid back to the lender. Leverage, is leverage. Unless you’re a member bank of the Fed.

PS. We are at the financial equivalent of when you get to the end of your grapefruit and you squeeze the last remaining drops into your mouth. The banksters are squeezing and we are the grapefruit the government is the garbage disposal that will eat any remains.

Yes!! People that do not understand the financial markets and the monetary system still don’t get that the housing market is manipulated they don’t understand that housing prices are higher due to the low interest and fake manipulated low inventory (banks still have millions of empty homes and millions still in process of foreclosure. Millions and millions and millions of houses) they don’t understand that Goldman Sachs in JP Morgan Chase etc are now securitizing the leases on the homes. They don’t understand how money is created what gives its value, none of that. so I can tell by some of the comments here that they think that because now people are buying homes with cash that that means the housing market is more stable, that is not the case what it means is people will lose their cash instead of just their mortgage when everything collapses again like it always does as the poster by the name of what? So clearly pointed out. Also I am so sick of people blaming their local real estate agent. That is so far off base it’s embarrassing to read as I feel sorry for the ignorance of the person that wrote it. It’s like blaming the guidance counselor for the student loan scam. That’s Another tulip bulb financial scam robbing everyone.

PS the large institutional all cash buyers have done so through a special Fed program only offered to large institutional investors. They must hold these properties as rentals for 5 years. The large institutional investment banksters are securitizing the rent rolls now. Hello? This bubble will pop like every other one. This time people will lose their cash.

Thanks for this.

Makes total sense- without an improving economy -an economy as measured by something other than rising stock and real estate markets- like employment, there can be no real widespread sustainable inprovement in the housing market.

I started reading this blog every day since 2009.

I was one that sold too early when the market went up in 2002. I thought I would never be able to buy again in LA. I hated myself for over 6 years for selling my 4 unit building.

In 2009 I was blessed to find a great job again (long story). I had money in my 401k and at that time my 401k was not doing anything for me. So I decided in 2009 to cash out 85K to buy a 2 unit building.

I would have to say 2009 is when I notice that people were buying place with all cash. Every place I put a bit in I would miss out because of cash buyers. All I would hear from my agent is “Cash is Kingâ€.

But an amazing thing happen for me a place that I had bit on came available again because the cash buyer decided to pull out of the sell. My agent just so happen to know the person that was handling the short sale for this place. I was the next person in line so they sold the place to me. I was able to put 20% down and got a 5.0 interest rate. I got the place for 472K.

Since then I refi this place in May 2013 and was able to get a 3.75 interest rate.

Check this out. The rates started going up 1 week after I closed my refi.

I say all this to say only God allowed me to get this place.

Good thing God likes you more than other buyers.

What’s your secret?

With the rates going up close to 5% now and probably 7% once the fed starts tapering its purchases of MBS this fall, prices are going to have to go down if they want to sell these over priced houses. Wall street is not going to buy any more with inflation going up and workforce participation in this country is at its lowest point in decades. Regular working people can’t pay these prices. I don’t know if we will have enough Chinese money launders to cover the housing market. Its going to be interesting.

Yes, of course, there will be a crash again. When? When the interest rates rise to the historical norm. It will happened when the fed stops printing money. When it does, the whole house of cards collapse…

what if the fed never stops printing money?

50% of modified mortgages are re-defaulting.

Reading the comments from the housing shills brings back memories of patrick.net and housingpanic.com in 2006. How time has flown… Then just as now specuvestors touted a new normal where gravity could be defied indefinitely. Posts full of bombast and bullish outlooks, and then late 2007 happened. even the foreign oligarchs pumping up SoCal RE are hopelessly dependent on a failing system. Technology, debt deleveraging and demographics spell a multi-generational deflationary cycle. There is no escaping this reality. As Orwell rightly sated technology renders class distinctions far less broad than at anytime in human history. The 30 year debt binge was for the sole purpose of maintaining a divide for the upper classes. They have fought off gravity for quite some time, but their ability to do so is waning. See Bitcoin, the growing libertarian movement against the banking cartel, etc. the jig is up and more people than ever know it.

Are you factoring into this equation money-printing?

The ads on the side of the blog are hilarious: 1) A guy who claims ‘three cataclysmic shifts are going to bankrupt 97% of RE investors’; 2) A company stating, ‘Your home is the biggest purchase of your life – shouldn’t it come with a ‘money-back option’?; and 3) a place trying to sell silver coins.

Amen!! And/or I rest my case your honor!!! 😉 Yep, the feel is that of 2006, at our doorstep again!

……and when the music stops…..???? 🙂

Thank you Dr. HB, for your great forum!!

“….Then just as now specuvestors touted a new normal where gravity could be defied indefinitely. Posts full of bombast and bullish outlooks, and then late 2007 happened. even the foreign oligarchs pumping up SoCal RE are hopelessly dependent on a failing system….”

I have been watching these cycles and I have a hairbrained idea. The cash buyers are buying to hedge against inflation and to generate some cashflow in the interim until its time to unload.

I’m doing some back of the envelope math and if you buy a house for $240,000 and it rents for $2000 a moth that’s a 10% return and you still have your equity. If the value drops, think of it like a bond. The value dropped but your return just went up as a percentage of the paper value. If you pay $480,000 for this house your still making 5% which isn’t shabby in today’s market.

I think investors are taking a long view. These houses selling for $240,000 sold for $35,000 30 to 40 years ago. They are looking at all the QE and are thinking inflation MUST come back at some point. Would they rather own the gold they just sold? No, because it has no return and it could go back to $300 an ounce just as easily as the house could drop to $150,000. And that is less of a drop – and there’s still a return every month.

Wise readers – please poke my thoughts full of holes. Happy investing.

I agree that these investors are buying for those reasons you listed, but I do want to poke holes in your inputs you used to calculate the return. A $240,000 house in today’s value in Sacramento will not get $2000/mo in rent. It may get $1200/mo in rent. $200/mo in property taxes, you need insurance, there is upkeep and you usually don’t rent out your unit 365 days/yr year after year. You are getting like 4.5% if you chose a great house, plus it takes up time, and there is a legitimate downside risk of falling home values. If you can get $2000/mo rents where you are, then that is great. Sacramento/Las Vegas/Reno are the hot spots where investors are buying and the rent/purchase price ratio looks more like my calculation than yours.

To get 2k for rent a house has to be in a more desirable areas so prices there is not 240k but more like 300-400k (unless you buy at 240k a long time ago). So 24k/350k is 7% minus 1.25% tax and 1% maintenance. That’s 4.75% returns, you can get the same buying a portfolio of dividend stock or where the 30 year UST will be shortly when the FED stop buying!!!!The market over time rise around 7-8% year with dividend so RE will still under perform. With worsening job prospects, demographics, and debt load in the US. RE is shaping up to be the perfect gift for the long term bag holder at current prices. At least in 2006, the economic prospect (fake) was much better. When these debt bubbles pop there will not be inflation but deflation waiting as all the electronic money will simply vanished and people will stop paying down their debts forcing many debt based investments to take massive hit destroying at lot of paper wealth in the process. Just look at the student loan debts, many of these kids will spend a decade or two paying it down and will not create any more “nuclear” family. Combined with the older generations down sizing, future demand is shaping up nicely!!! Population will eventually peaks in the US for the middle and upper classes (already did in Europe and Japan) taking down all economic activities and asset prices due to lower demand. This is the long term future awaiting for RE and it’s not pretty. That just make the we can not create more land argument fall flat on its back.

Your math doesn’t hold up: stocks have embedded leverage, too. It’s just hidden.

As for bonds and notes: they provide anti-protection against money debasement — which is going on gangland style at present — globally.

Many of the California buyers are Chinese, fleeing a truly insane real estate bubble in Red China. By their standards, California premium real estate is just being given away.

We saw this same logic in the late 1980s with Japanese buyers. Like todays Chinese, they were ALWAYS all cash buyers. Heck, they’d just flown in to town.

Like all other ethnics, the Chinese only want to buy in certain, socially safe, locales. It’s no coincidence that these markets are the hottest of the hot.

Since these buys are almost panic purchases (politics drives all in Beijing) the Chinese are stepping up and paying even over the ask — from time to time.

This process has long ago occurred in Vancouver, B.C. and in Australia. Both markets have been on rocket rides. Some pricey neighborhoods in Vancouver have flipped from 100% White to 100% Chinese over a fifteen-year period. They simply over bid every other prospective buyer! Naturally, the sellers were more than happy to take the deal.

More generally, the Hedge Funds commonly represent/invest institutional monies that are the exact opposite of hot money. They may move from one manager to another, but will stay in play.

What’s driving everyone is the LACK OF ALTERNATIVES — at a time of rampant money debasement. The official inflation statistics are total hogwash — and every serious investor knows it.

This means that ‘buy and hold’ for bonds is ruinous. Even 12% nominal returns don’t cut it.

However, rental incomes have some prospect of tracking monetary debasement. Most still remember the financial dynamics of the 1970s.

But the price move has maxxed out — for rental cash-flow investors. From here on up it requires plenty of greater-fools — and the Fedsury is removing the punch bowl.

Ever so gradually, this nation will become a nation of renters. That’s the long term trend — extending out for at least a generation.

Without question the investors win and the middle class loses. Even if values halt and even plumment, you still are getting a return every month and you’re not paying a mortgage. That gravy train never ends, no matter how much the value decreases (and they won’t wipe out most investors equity that have bought the last 3 years. It’s either monthly income + equity or just monthly income. Some investors are going to flip their investments in a couple years when they feel prices can’t go up any longer, but most of them, like you said, are taking a long term approach. It only makes sense to do so. Why, if you bought a 200k house in 2011 and getting $2,000/month would you sell in 2014 for $250k. You made less than $100k, which is nice, but you’ve ended the gravy train. I think investors realize after getting in near the bottom, their equity is safe and even if the market falters, they will still be in a prime position regardless of whether they sell or continue as landlords.

Being a landlord is gravy?!

In what planet are vacancies, repairs, and lease violations gravy? That’s just a few of the more benign aspects of owning a rental property.

Well, fensterlips — at least you’re thinking and trying to understand things. Plenty of people don’t bother and they make bad decisions.

Here is one poke — your yield (return) on the hypothetical house you purchased does not go up if the underlying value of it declines. Your yield is based on the original purchase price . And you must tabulate all of the additional expenses related to owning real estate….then deduct those costs from your incoming rent to get a true yield. Lastly, unlike a bond, real estate does not have a stated maturity date when the face value is paid off at par.

I would like to see he stats on the number of people who have purchased or refinanced with 30 year fixed rate loans below the 4.5 percent mark. Also include those who completed loan mods in the 2-3 percent range. Add to this the true cash buyers since 2009. Then add to this the people that hung on to their option ARMs originated ten years ago. I think you will see this is a large portion of current households. If rates go up, this will further constrain supply because people will not want to give up their current loans. The prospects for another huge oversupply in SoCal are slim.

SoCal is a different marketplace than most of the rest of the country. It’s very expensive to entitle and build new. Replacement cost should be factored in when analyzing from an investment standpoint.

With respect to those “overpriced houses”, in my experience, many sellers do not really need to sell. Many test the waters or are of the opinion that if we can get X for the current house, I can pay Y for the replacement one… Otherwise we just stay put.

Flippers will generally push the market to the max and leave room to negotiate if needed. It’s better to lower the price if a property doesn’t sell within 60 to 90 days, than to leave money on the table. Replacement projects are difficult to come by as the market improves.

I have been subscribing to this blog since 2006. It was obvious at that time that a housing bubble burst was inevitable. However, the bubble also presented one of the greatest opportunities in our lifetime to purchase real estate. The other such opportunity occurred in the 80s during the S&L bust. There is nothing new under the sun so all these boom/bust cycles have happened many times before. People think what goes up will keep going up is delusional but so are those who thinks what goes down must keep going down.

My formula to invest in the real estate market is the rent has to be able to sustain all expenses for a SFH or condo property in a good area with 25% down and at a fixed 30 year interest rate. We target newer SFH or condos in developing areas at good location with prices that are more than 50% to 70% off their peak value. Based on past historic data, it is observed that a bust is more severe in newer development (better bargains) and a boom always picks up from where it left off (better increase potential). That bust and then boom newly developed area was Orange County of California in the 80s.

From 2010 to 2012, we bought a couple of places in Las Vegas and Downtown Los Angeles. We financed the cheaper SFHs in Las Vegas and paid all cash for the condos in Los Angeles. There was no bidding war at the time; in fact, there were hardly any buyers. As for where our cash came from, it is not from refinancing our properties or taken out from our 401k, but rather, from years of hard earned saving. We are just middle class professionals who are conscientious about money. My sister and a lot of my friends are in the same situation. I know there has to be a much bigger picture of who the cash buyers are and I just hope my experience helps filling part of this puzzle.

I have retrieved from the market as we are expecting a correction. As for how we will respond should there is another mini-crash. We are not here to flip. People need a place to live so unless it is like Detroit where there is absolutely no employment which leads to a massive exodus of residents, we are ok with just collecting rents. At this point, if the market goes higher, we are happy knowing that our properties are accumulating values. If the market goes lower, we are ok with it also as we can purchase more bargain properties.

I stopped looking at the *momentum* of the market and focused on the ROI of a point-in-time sale. I took a “median” property value over a “median” rent in Zillow, assumed no financing needed, for my target area. I then factored in water, sewer, property management (more than collecting rents mind you, good full service affordable), insurance, taxes, repairs and stuff estimated and averaged out from several sources… came up with a final gross cash flow over asset price of about 3%. Patrick.net I recall had a nice rule of thumb 3, 6, 9% yields tell you what to do. However it’s really 3% with a 20-40% downside upon market crash. It’s not time to make the play yet.

If cash is king, then cash *flow* is the queen.

According to DataQuick, cash purchases accounted for a record 32.4% of California home sales in 2012. The range was from 24.2% in San Mateo County to 42.9% in Merced County. Multi-home buyers – those purchasing two or more properties – accounted for only 28% of the cash purchases.

Multi-home buyers are 28% of all cash purchases? Granted it’s not like everyone is doing it but 28% sounds like nearly a third of purchasers are cash and nearly a third of those are buying multiple properties.

Isn’t this a rather large percentage compared to previous and more nominal markets?

I’m not trying to build my case backwards but I wonder if we’re seeing signs of the flight to returns and the flight to safety in our crazy market today.

I purchased an SFD in Southern Riverside county on a short sale in 2009 for $230K with the hope of moving in. Since we couldn’t move at that time we’ve been renting for a little under $2000 a month to a stable tenant on year to year leases.

I’ll grant that this could be a one off I’m unlikely to repeat but I sure wish I had bought 2 or 3 more houses and multiplied this success. This doesn’t sound like it could have been repeated in Sacramento – per the OP but it can be done in some places here in Cali. These places sold new for $50,000 plus in the mid-80’s.

I don’t know enough about Las Vegas. It’s tempting but I’m not smart enough….

I’ve been reading through here for quite sometime. Just put offers on our 5th and 6th place over the past year and, yep, you’ve guessed it – the seller took all cash offers over ours. At least on one of these recent ones, the seller said we were the second best offer. This BS is so frustrating. I have a super steady job, perfect credit, a forgivable second of $150k from my employer, but it’s nearly impossible for families like ours to buy.

Leave a Reply