Chicago overtakes Detroit as the worst performing housing market: San Diego outperforms while Los Angeles hits a snag.

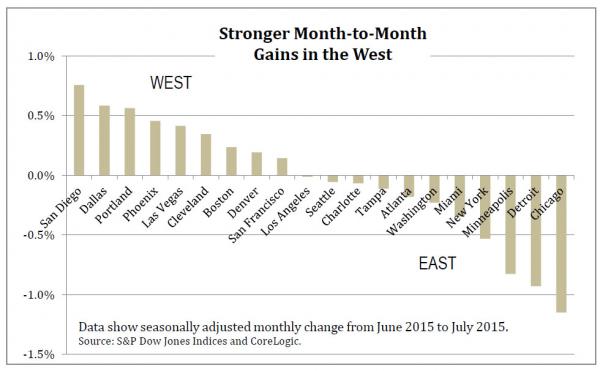

The Case Shiller Index is one of the better long-term measures of housing price changes. It looks at repeat home sales so you know what you are tracking versus say an area where new home sales are jacking prices up while old crap shack stucco boxes lag the market. The Taco Tuesday crowd is obsessed with buying simply because they lack other investment options. Housing may or may not be a good deal. Housing in many areas of SoCal is absurdly overpriced. However, in many parts of the country it is a good (to great) deal. Yet all markets are not created equal. In the last month, Chicago was the worst performing housing market even edging out Detroit. Chicago is a good city but my lord do they have a political system that is fully twisted. Taxes in Chicago are nutty and the pension system has mega problems. Bottom line, buying a home in Chicago is risky given all of these long-term issues. And the market is taking notice. Let us look at the short-term best and worst performers.

The latest Case Shiller Data

I have many readers in the San Diego market asking me “why is San Diego doing so well?†despite the building inventory in other parts of SoCal. The answer is largely embedded with the lack of growing inventory. Where places like Los Angeles and Orange County are seeing big jumps in inventory, this is simply not happening in San Diego. Since people are creatures of habit, are tied down by work commitments, or family and society pressure to buy, those feeling the itch to buy in their loins are going to do so regardless of market timing. People buy largely because of emotions. They also go broke because of emotions. Just watch some of the pathetic behavior exhibit on Canadian housing shows where people routinely jump off the financial cliff with a mortgage that means massive debt for most of their working lives. And somehow being in debt to a bank for 30 years is the pinnacle of financial success.

Let us look at the latest Case Shiller figures:

San Diego, Dallas, and Portland lead the way in terms of monthly gains. San Diego makes sense because of the low inventory available and the house lusting California culture. Dallas is underpriced and with the out-migration of Californians, prices have room to grow there especially if rates remain low. Portland continues to draw outsiders despite anti-California rhetoric.

Los Angeles dipped. Yes, the proverbial unstoppable city dipped. Could it be because people spend 50% of their incomes on rents or 40% of their income on crap shack stucco boxes? That could be one reason. Or it could be the start of a reversal since California is perpetually in a boom and bust cycle.

But look at the worst performers. Minneapolis, Detroit, and Chicago. Chicago by far was the worst performer in what tends to be the kickoff months of the summer. Keep in mind the Case Shiller data is a few months behind because escrow closing and sales data isn’t reflected immediately on a sale. This is why the latest data out is looking at July figures.

What is going on in Chicago?

Inventory is up 8.9 percent year-over-year. However the number of homes sold is down 4.5 percent year-over-year. There seems to be some momentum building to the downside for the summer which seems to be reflected in the preliminary Case Shiller figures.

The median list price of a home in Chicago is $240,000 which will buy you a home in Straight Outta Compton here in Los Angeles. Don’t believe the non-stop hype that buying a home is a no-brainer. You have to run the numbers. The market is frothy and young professionals see their Taco Tuesday parents massively in debt and their ultimate aspiration was to leverage their entire life into a crap box. These parents now see their kids coming back as adults to live in the home. Many young tech workers need flexibility and mobility. Many can’t afford in San Francisco for example. That is okay. Then you have people saying “well I built up so much equity since I last bought†as if they are using that money. You don’t get that equity until you sell and that kind of rhetoric makes you a speculator. There are many better investments on Wall Street that can provide a better yield if you used a bit of research. But the pervasive propaganda of buying a home has left many desperately trying to buy even though there are alternative options.

The above list should also show you that not all areas are created equal. Booms and busts don’t happen uniformly. But the fact that in Los Angeles so many people are stretched thin on the renting and buying front suggests many are walking on an edge again. The minor slow down in the stock market is already impacting the housing market as it enters the slower fall and winter season.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

113 Responses to “Chicago overtakes Detroit as the worst performing housing market: San Diego outperforms while Los Angeles hits a snag.”

How come nobody ever says well this whole economy has gotten out of hand and longshore men and doctors and corporate attys, and the schools that educate, ect … are going to have to recognize it was all a scam and the money owed and the salaries received are just unsustainable based on the 90-10 wealth divide. There just isn’t enough money in the hands of the 90 to keep this game going and compound interest makes it too dangerous to let the 90 have more than they need. If that ever happened in 2 generations most people wouldn’t have to work because compound interest would allow a savings rate beyond what is required to make people need to work. This gets real ugly, the rubber band in now in full contraction mode and building momentum quickly. All budgets continue negative revisions, cap ex is not existent because no-one from the hotel builder to the starbuckx manager to the global conglomerate mining company to Apple have any idea what real demand is going to bring in the years ahead because it’s all been financed for the last 40 years and principal can never be paid back and the interest in still more than makes sense based on future margins.

Me , it is always easier to hold worlds problem under a microscope, we see the bad and propose a antidote, the concern is, we don’t really have a cure? Stay safe

Robert

Thank you for your thought. My point is, it’s not a concern it’s a fact. Metaphorically the patient is going to die and the only antidote is to let the patient die. We are not letting the patient die thereby allocating a lot of resources better used elsewhere. We are so concerned about what happens to the family if we just take the patient off life support. You know what the family will be fine in the long run but the longer we keep the patient alive the more pain we cause and the longer we draw out the inevitable. Why are we so scared to let the patient die. Even if the entire economy collapsed and a nuclear bomb exploded in Manhattan and a tsunami wiped out California mankind would adapt and go on. Why is the fed so concerned about raising rates. Because the fed is trying to create the illusion of control. The fact is the fed hasn’t had control for the last 40 yrs just like the DEA has absolutely no impact on drug smuggling it’s all just rational for bigger govt. we desperately need a collapse so the people running this preposterous economic recovery are revealed for the witch doctors the really are. Wake up people of planet earth. Insist on taking back your country and having an Economy based on real demand and real production not endless credit to borrowers can never pay it back. Otherwise lets keep rates at zero with 100 amortization periods let’s make it thousands year periods to really juice the price while still making it affordable for people who still won’t be able to afford it. This is all just insanity and rather than being distracted by the latest young man who murdered innocent people because his mother allowed him to have 13 guns while she knew he was not only severely mentally disturbed but also on medication, we should all be demanding the media talk of nothing other the the total bullshit the artificially stimulated economy really is until the stock and housing market collapse to a point that represents real value based on people’s ability to consume without credit. If you can’t afford it without credit you shouldn’t be able to buy it.

Oh yea and why do municipalities and the people who live within them and draw from them continue to pretend the promised pensions will ever be paid. There is

nooooo waaaaaay!!! pensioners are going to get anything close to what they have been promised. I’d say 70% cut. No money can be raised via taxes, people are already broke. Again, everything is going to have to get at least 50% less expensive. Once people accept this we can all move forward. Whyyyyy can’t we just accept the inevitable. We all accept we are going to die some day so whhhhhyyyyyy can’t we accept there is no growth, we have way to much government, we have shipped our labor abroad in search of profit and now we have no economic base for growth. Facebook and Amazon are not the future and really do nothing when you think about it. Gotta have money to spend money.

They’ll screw everyone else before they touch the pensioners.

When San Bernardino went bankrupt, they paid bondholders a penny on the dollar, but zero cutbacks on the employee pensions. http://www.reuters.com/article/2015/05/14/us-usa-bankruptcy-sanbernardino-idUSKBN0NZ2LP20150514

From the article: “The city needs a workforce. And you can’t have a workforce without pensions,” Saenz told Reuters in January.

Which is not true. Most American workers don’t have pensions. They’re lucky to have a 401k, if that. So clearly, you can have a city workforce without pensions.

Public employee pensions are akin to social security, not 401k’s. Just sayin’.

SOL,

Good observation and excellent comment!

All if this assumes there is a tax base and investment growth to pay the pensions. There will be neither. Then what happens. Pensions get cut. They must, they will, and the sooner everyone accepts and adjusts their consumption accordingly the sooner the collapse will come and the better off we all will be. Look what happened in Detroit. Fireman, police and city workers are getting 1/3 of what the were promised.

Public employee pensions are akin to social security, not 401k’s. Just sayin’.

NOT.

Next time, do some research before you’re “just sayin'” anything.

The issue went to court. The court ruled that federal bankruptcy law supersedes, and thus nullifies, state pension law protections. Therefore, state and municipal pensions CAN be cut, or even eliminated, same as with any creditor in bankruptcy — regardless of what was originally in the employee contract.

It’s not even an open question, mm. The courts have spoken. State and municipal pension are NOT legally like social security. (I don’t know if this ruling affects federal pensions.)

The county CHOSE not to cut employee pensions in their bankruptcy plan, and the bankruptcy trustee accepted that plan. But both the county and trustee had the POWER to cut those pensions. And they SHOULD have done so.

I’m NOT “just sayin'”, mm. The court is “sayin’.”

“Look what happened in Detroit. Fireman, police and city workers are getting 1/3 of what the (sic) were promised.â€

Huh? Did you just completely fabricate that number? That’s not true at all.

The biggest cut that the general city workers got was 4.5 percent, and the elimination of annual cost of living adjustments. Police and firefighters received no cut, except for the reduction of annual cost of living to 1 percent from 2.25 percent.

Source: http://www.detroitnews.com/story/news/local/detroit-city/2015/10/02/detroit-pensioners-lose-appeal-bankruptcy-cuts/73212550/

Responder

U r wrong. Why do you believe what you read. R u an academic type, r u a Fed board member who looks at the data rather than actually getting off your ass and actually talking to people. Uncle is a retired Detroit cop. His benefits have been gut by 2/3rds. Worse acces to health care, taxes going up on everything, artificially high exchange rates vs the dollar in Europe, gas artificially juiced by prob a multiple of 5 depending on where you live, cost of drugs going through the roof, I could go on and on but you get the point.

There isn’t anywhere near the money necessary to keep this economic charade going and more QE just makes it worse. The only option is to go backwards on everything 50% aka market crash

Me: You stated with no other clarification that, “Fireman, police and city workers are getting 1/3 of what the (sic) were promisedâ€. Even if health benefits were cut, their monthly pension payments were not. Therefore, overall, they are getting much, much more than only 1/3 of what they were promised. If you limit the criteria to only healthcare, then you are likely correct. But there is a substantial omission in that assertion, which is that they are still receiving 100 percent of their monthly pension benefit (excluding health benefits).

I agree, there is not enough money to keep the pension charade going (or the various other economic charades). I’m really extremely annoyed that my taxes are used to pay pension benefits of public employees. They should have to self-fund their retirement just like private-sector employees do. I would not be opposed to a 401k-style plan offered to public employees just like many private-sector employees receive.

SOL,

I wasn’t speaking to the merits of pensions vs social security; I was referring to how they are paid for. If we didn’t pay into public employees pensions then we’d be paying their FICA. I don’t really care which we pay for, but if we end their pensions then we’ll pick-up their FICA tab. That was all I was trying to get at. Actually, if I was a public employee and was given a choice, I’d much prefer SS over a pension that appears to have pretty dicey prospects.

I wasn’t trying to pick a fight lol

What are the qualifications to be apart of the “Taco Tuesday” club?

Be a card-carrying member of the “I leveraged my soul to get a house the bank said I could qualify for, new cars I got loans on, annual cruises I put on my credit cards, a Harley and other toys also on loan, and borrowed money on the afore-mentioned house I don’t own to remodel it because, you know – granite, and other Keep-Up-With-The-Joneses madness because I didn’t care that I was joining the 30-Years-A-Slave crowd as long as I got mine right now.”

Damn! Beautiful explanation.

Excellent summary. No Taco Tuesdays for me. Grateful.

Beautifully said. Some people need a reminder that “mortgage” comes from the French literally meaning “death pledge.”

AKA the Bud Lite and statins crowd.

But but but but but…. Senor Cardgsge said I could refinance my dreams and get a leg up on the pile!

Alex, there are plenty of Chardonnay-swilling folks doing Taco Tuesdays too. Trader Joe’s sells their Two-Buck Chuck version.

An insatiable hunger for tacos.

Housing To TANK HARD IN 2015!!

Jim, you have 90 days left in 2015. We are now entering the slow selling season where people don’t want to be inconvenienced with a home sale and move over the holidays. They will simply take their house off the market and relist in spring. One of these years you will be right finally, but not in 2015.

everything to tank sept 2015

Tanks will tank hard!

@Jim Taylor,

Housing tanking has been studied by the Federal Reserve. It takes 3 to 7 years, peak-to-trough for prices to bottom.

Here in California, home prices only tank when there is a recession. Banks are allowed to keep foreclosures off of the market for 10 years. The peak years for foreclosures were 2009, 2010 and 2011.

Plus the Federal Reserve via QE1, QE2 and QE3 has done a wonderful job of keeping the stock markets artificially elevated. The Fed manipulated stock market is what keeps home prices artificially high in the Bay Area, 310/626 area codes, Orange County and San Diego (all markets heavily influenced by stock market valuations).

And, in the 310 area code, SFR’s are mostly owned by an aging elderly population who missed the peak in 2007, and are waiting for the new price peak to hit.

Factor in all the above variables and we 2 to 6 years away from home prices tanking. I have home prices tanking in SoCal in 2019.

Why China Is on an L.A. Spending Spree: “It’s Just Monopoly Money to Them”

http://www.hollywoodreporter.com/news/why-china-is-an-la-827975

Good article in that it’s describing the type of behavior that accompanies the run-up in a bubble mania, but it might be a bit behind the curve as the mainstream media tends to be.

Arcadia is sitting at 40% ask reduction rate, inventory is up nearly 100% YoY, and median price is down almost 20% YoY.

https://www.youtube.com/watch?v=YjkkjH0GnfY

The ekonomists at UCLA predict housing in LA has a couple more years to go before tanking (next time won’t be different if you follow the appreciation/depreciation cycles in the article).

“…Building permit applications and housing price patterns show that a collapse is not imminent, writes UCLA Anderson Forecast economist William Yu…”

“…If history is any guide, the L.A. housing price cycle seems to last about 12 years on average, of which 7 years is spent in the bull market with at least 65% real price appreciation, and 5 years is spent in the bear market. We are 3 years into the housing recovery that started in 2012, with 27 percent appreciation so far. On average, there will be 4 more years or 38% more price growth before we reach the turning point…”

http://newsroom.ucla.edu/stories/is-los-angeles-on-the-cusp-of-another-housing-bubble

Only problem I see with his analysis is that the most recent “bear market” in real estate was cut short by manipulation. Low interest rates, investment buying, etc. The bear market stopped, and shot straight back up.

“In the last two years, we haven’t seen that kind of rapid appreciation in Los Angeles.”

And I’m not sure I even agree with his numbers. Using zillow’s price data…median price in LA County bottomed at 344k in Jan 2012. Now It’s at 514k. That’s a 50% increase in just less than 4 years. He said it’s gone up 27%. I’m not adjusting for inflation…but we’re only talking 4 years. Orange County is also up about 50% in that same time.

And this is all with a pathetic recovery, little to no growth in wages. Just doesn’t make sense.

Are his numbers even right? I see 50% increases since the bottom in January 2012, in both LA and OC. I’m not factoring in inflation…but he says it’s only been a 27% increase?

And that’s on top of this “bullish” housing market being driven by low inventory, low interest rates, and investor and foreign buying. To compare this recent run up to anything historical seems silly.

Wholly agree. The UCLA analyst is either disingenuous or ignorant in using free market principles and past trends to explain a real estate market benefiting from the most expensive and widespread intervention by the Fed and government in history.

No mention of exponential price run-ups attributable mostly to investors in just a few years — usually a sign of manic over-leveraging and debt manipulation.

There are differences though! I don’t believe there has been any time in history where affordability has been so low in a place like Los Angeles. This severely limits those that can play the real estate game. For everyone else, it requires either coughing up more to rent, getting inventive about living, doubling up, and spending less in other places. No one talks about government liabilities … revenues may be up currently due to better economic conditions, but the liabilities are still essentially still there, and at any time can create a drag on housing or the economy. If you streets, sidewalks, water mains, are in disrepair, it will ultimately have an affect. I could go on, but there are a lot of factors that are different that can subvert the ‘California Dream’ in a heartbeat!

JNS, that is the type of comprehensive thinking the SoCal housing speculators don’t want you doing. Instead they will try to distract with opinions on the weather/climate, “diversity” that really only goes as far as ethnic dining options, habits of the wealthy, global money tides, population density, government benefits a la Prop 13, and so on.

While everyone is busy pointing and laughing at a place like Chicago or Detroit, our own foundation is forming cracks.

Just wait til this hits the books in the liberal utopia called Chicago ILLANNOY!!!

https://www.illinoispolicy.org/chicago-tax-collector-hath-arrived-with-massive-tax-hike/

Crook(Cook) county is panicking because state supreme court upheld state constitution that forbids pension reduction(even if obtained thru fraud-1 day as teacher and full pension).State without budget for longest time ever and Gov being Venturaed(see what happened in Mn) .8 bil in unpaid bills and underestimates of unfunded liabilities make for a dire situation.I’m leaving for Ind-BYE SUCKERS

With high taxes on almost everything, the Democrat gangsters who run Chicago and Illinois are putting the Democrat gangsters who run California to shame!

Starting next year, Chicago will have the highest sales tax in the country, with state, county and city taxes adding up to 10.25%.

http://consumerist.com/2015/07/15/chicago-will-have-the-highest-sales-tax-in-the-u-s-at-10-25/

Illinois now has the second-highest property taxes in the nation, according to a recent report from the Urban Institute.

http://www.chicagomag.com/real-estate/January-2014/Illinois-Now-Has-the-Second-Highest-Property-Taxes-in-the-Nation/

http://chicago.suntimes.com/politics/7/71/503420/illinois-second-highest-real-estate-taxes-nation

Illinois has one of the highest cell phone taxes in the country, according to a new report from the Tax Foundation.

http://www.nbcchicago.com/news/local/Illinois-Cell-Phone-Tax-Among-Highest-in-Nation-279065641.html

Chicago has the highest garette tax rates in the country:

http://www.tobaccofreekids.org/research/factsheets/pdf/0267.pdf

Thanks to a fiat administrative declaration by Chicago’s Department of Finance, residents are now burdened with a new online “amusement services†tax. That means if your billing address is within city limits, residents are forced to pay a 9% tax for services like Netflix, Spotify, and Xbox Live.

https://www.atr.org/chicago-s-amusement-tax-no-laughing-matter

Starting next year, Chicago will have the highest sales tax in the country, with state, county and city taxes adding up to 10.25%.

Not true.

In 2011, we here in Santa Monica already had a 10.25% sales tax: http://www.nbclosangeles.com/news/local/Santa-Monica-Tax-Rate-Jumps-to-1025–119006679.html

According to the above article, several cities in California have sales tax at 10.25%.

And South Gate has a sales tax at 10.75%.

The people of South Gate LAUGH at Chicago’s measly 10.25%.

Some places in Arizona have sales tax near 13% because red state.

C’mon, Alex. Arizona might be a “red state” and it might have a high sales tax, but it’s not BECAUSE Arizona is “red state.”

On the whole, “blue” areas have higher sales taxes — and higher taxes OVERALL.

What are “red state” Arizona’s taxes OVERALL?

Sonofalandlord…. Pretty high and the pay to expense ratio there is worse than it is in California.

Culver City with a 9.5% sales tax is not very far behind Chicago, Santa Monica or South Gate.

“What is going on in Chicago?”

How significant is a few tenths of a percent difference between the negative performers in total dollar terms and effective affordability? A 1% drop is a 100% larger loss from $480K than from $240K.

A few things I did notice in the latest Case-Shiller.

Every single top 20 MSA is lower SA vs NSA.

“The only eastern city with a positive gain was Boston, while Los Angeles and Seattle were only western cities with weaker prices in July than in June.”

What is going on in Los Angeles and Seattle?

Inventory peaked in San Diego a month ago, now on the decline, although modest.

Don’t buy in prime areas unless its at rental parity. Buy everywhere else. In Des Moines, the top market for home buying millenials, you can either pay $1,200 rent for a 950 sq ft 2BR townhome, or a quaint 1,400 sq ft home with a $750 mortgage. No-brainer.

In the central valley, higher end homes in affluent neighborhoods are outrageously overpriced, getting 2006-2008 prices. Sellers cashing out, asking for the world.

Hmm I see what you mean about Des Moines.

http://www.theatlantic.com/national/archive/2015/10/des-moines-millennials-housing/408841/

And I agree with your posting back in June 2015, or at least I’m very sympathetic to your view point. >>> What point is there to live in the bay and L.A. if you can never own? Who wants to be approaching retirement with no equity or paid off home and nothing but a measly 401k? <<<

http://www.doctorhousingbubble.com/renting-in-feudal-america-renting-new-american-dream-incomes-study-data/#comment-879842

What point is there to live in the bay and L.A. if you can never own?

“There’s no point to living in L.A. unless you’re involved in the movies, and I mean in a big way.”

— gangster Bo Cattlet in Get Shorty

While we gripe about the high cost of housing, one mansion in Bel Air is spending $90,000 a year just on their water bill — That’s a monthly nut of $7,500 just for the water!

The mansion uses 11.8 million gallons of water a year: http://losangeles.cbslocal.com/2015/10/01/the-wet-prince-of-bel-air-1-home-uses-12-million-gallons-of-water-per-year/

While some parts of San Diego maybe doing well all are not. I live in Alpine and a few years ago our market was extremely robust. But something happened about a year ago that changed things. Starter homes around 1300-1700 sq ft just stopped selling all together. You can’t find any comps whatsoever for homes in the town in that range. The higher end 800 and up stilll sell but they have to be a deal to move. People just put houses on the market all the time at 2004 prices and they just sit there a while then delist them. For the lower end 500k and below, nothing really moves any more because people simply cannot afford them anymore. We have plenty of inventory here but all with absurd pricing. Sooner or later something is going to have to give. God only knows when though.

I am in San Diego and I can definitely see market softening. I am talking about prime desirable non coastal areas where I am keeping an eye.

It is not sustainable for sure but how long the music would go, no one knows

You would never know how badly Chicago’s market is performing in the city’s uber-expensive “green zone” neighborhoods, which are the wealthy and semi-wealthy inner-city nabes ringing downtown. Former worker’s cottages in Wicker Park and Ukranian Village sell quickly for $1M or more, and two bed condos commonly fetch $500K or more.

The outer neighborhoods like mine, though, are still far below peak and not rising in value, while the suburbs are getting hammered, possibly because the suburbs have the most confiscatory property taxes, thanks to the 30 year competition between them to see who can offer shopping mall builders the most tax-funded “gimmes”, with the idea that this will help build the “tax base”. The result is a huge inventory of failing regional malls, strip malls, and power centers, often located across the street from each other, and that pay almost no taxes, while the burden falls on the homeowners. In Schaumburg, for example, a house barely worth $250,000, typical for the town, pays $8,000 or more for property taxes, an unsupportable burden for a family making $50,000 to $100,000 a year, and whose house taxes were more like $2,000 when it bought the house.

Illinois and Chicago are in the mess that happens when you give your politicians unlimited power over your property and your money.

You can live in a Lincoln Park alley home for $1.2mil.

Whoops, forgot the link: http://www.chicagomag.com/real-estate/September-2015/Loft-Living-in-a-Lincoln-Park-Alley-for-12-Million/index.php?cp=1&si=0#galleryanc

@ Laura:

Laura – as I have noted several times on this site – my wife and I had a nice home in Kane Co. 4200 s.f. on a realtively small lot – PUD Development – taxes on said house – just under 20,000 a year at peak. House was sold at 596,000 3 years ago – the couple that bought from us I understand have seen their taxes increase. Reason being as I heard directly from the assessors mouth as I continually protested the rates – Even if your home has a lower market valuation by our standard, we will just raise the levy because we need the money. That was it in a nutshell – they NEED the money.

The burbs are indeed getting hammered. I see now as I drive through Cook Co. , Lake Co north burbs and now in the west near in burbs – Park Ridge, Elmhurst, Des Plaines etc. increasing numbers of For Sale signs. This used to be the season when the signs would start to come down – not so much anymore.

I rent now – and will be vacating this miserable union utopia in 10 months time – heading west to sunnier climes, better tax environment and the great outdoors. 30 years of this crap hole is enough for me.

For a minute there thought you were talking about California … political problems, taxes, pension mess! An article at CNBC said California’s revenues are up, but that 45% of income tax revenue is generated from just 1% of the population! Sounds like it isn’t just the people who are living on the edge!

Except I pay $3K/yr for my little $500K California crapshack. Gotta love Prop 13.

Short sightedness. The costs eventually come to bear in other areas for all of us. There’s no free ride.

http://www.latimes.com/local/cityhall/la-me-0925-valley-crime-20150925-story.html

“As they have elsewhere in the city, crime and homelessness have surged in the Valley. As of Sept. 19, there had been a 17% increase in violent crime in the Valley this year compared with 2014, and a 10% increase in property crime, according to data from the Los Angeles Police Department’s Valley Bureau.

The Valley’s homeless population jumped 8% in the last two years to 5,216 people, according to biennial figures from the Los Angeles Homeless Services Authority.”

I pay less than $3k a year on my Santa Monica condo, which Zillow estimates at over $600k.

Meanwhile, back in Los Angeles, good luck with that gentrification in South L.A. Has anyone else noticed the increase in graffiti this year around the west side? I have.

http://www.latimes.com/local/crime/la-me-1003-banks-lapd-gang-shootings-20151003-column.html

“Crime in the city continues to rise…”

“For many residents, that feels like a return to the bad old days.”

“But the flurry of shootings— 19 last weekend, when five people died — has residents on edge.”

“It’s a spike, and it’s fast, and there’s no rhyme or reason…”

“Many of the people who were shot this summer seem like inexplicable targets, neither robbery victims nor gang-involved.”

“Dramatic rise in crime casts a shadow on downtown L.A.’s gentrification”

http://www.latimes.com/local/crime/la-me-lapd-central-20150902-story.html

“Overall, violent crime in the Los Angeles Police Department’s Central Division, which covers parts of downtown, skid row and Chinatown, was up more than 57% through the end of August compared with the same period last year, and property offenses increased nearly 25%, according to police data.”

“The problem reminds him of how bad things were more than a decade ago, when crime was rampant in the area.”

“But authorities say crime patterns have a way of spreading from rough areas to the edges of more prosperous ones.”

“Roger Gendron, a real estate agent, recalled a young woman who moved out of a downtown unit after just three months because she had been harassed and felt unsafe walking to and from her building.”

“It’s going to be a deterrent to people who maybe don’t have the urban backbone to endure coming into a city downtown that’s not yet done and pretty and pristine,” he said.”

“As Lauren Mishkind was walking along 7th Street this summer in downtown Los Angeles, a man pulled a handgun and pointed it at another person standing behind her.

Terrified, she hid behind a car while the assailant tackled the victim.”

“I was just shaking for the rest of the day,†said Mishkind, who lives downtown and works at an architecture firm in the area. “You kind of assume it’s par for the course living down here, which is kind of more shocking.â€

Chicago’s municipal insolvency is a very real prospect.

To counter that, property taxes simply must vault skyward.

Hence, the smarter set is shunning Chicago — purchasing homes outside the ‘blast zone.’

In this, Chicago is aping Detroit.

The trajectory appears irreversible, as it’s based upon popular appraisal of where things are headed.

The wealthy few flee first. To be followed by the rest of the income distribution curve.

Eventually, you see an urbanity that is bereft of talent, income, and civility.

It’s culturally, economically, hollowed out.

it’s always the very poor who can’t afford to move out or even have the sense to think about moving

Looks to me like the wealthy here in Chicago are fleeing last, because the wealthy inner-city zip codes are very, very hot, while the middling and lower-priced ‘hoods are stagnating in prices. The expensive houses and grossly overpriced condos are flying off the shelves in neighborhoods downtown, in the Near North Side hoods like Lakeview, and uber-expensive Lincoln Park, the South Loop, the near west side, and the trendy near northwest side nabes like Wicker Park, Logan Square, Bucktown, and Ukranian Village. It is unusual for a property to be on the market for more than 30 days in these areas, and the prices are now over the 2006 peak.

The far north side, however, is languishing, and in nabes like Portage Park, beautiful Peterson Woods and Hollywood Park, great houses sit on the market for a long time. The middle tier has been knocked out.

Laura is spot on. blert is projecting wishful thinking because of Chicago’s significance to Obama.

The reason for that is simple and we saw it for the past 2 decades – the very rich and very poor feed on the same constantly diminishing middle class till it is completely hollowed out.

When the middle class disapears, the rich are fleeing too because the host is dead. You can’t get anything from poor people.

The cause for this is globalization. Kick out all politicians who support globalists regardless if they have D or R after their name.

Laura Louzader…

Interesting…

The same dynamic holds true for Detroit, New York…

Some wealthy folks — short on children — DO love the city center.

Before the end, even the wealthy bail.

In 286AD Diocletian moved the capital of the Western Roman Empire from Rome to Mediolanum.( Milan ) He parked his pal Maximian there, as he moved off to run the East.

In 402AD Honorius transferred the capital of the Western Roman Empire from Milan to Ravenna.

American cities go south a lot faster than the Roman Empire.

When Leftist brain waves transform American cities into vote plantations you end up with the classic sloth common to the Antebellum South.

The entire city population develops “the slows.”

Real estate values adjust downward, accordingly.

People keep talking about being a 30-year slave to a mortgage. This is not true. California is a non-recourse state. You can always walk away from a mortgage, debt free. Let the bank eat the loss.

You can even live in your house or condo rent-free for months, maybe years, before the bank forecloses. Thus you earn back your down payment, and maybe then some.

Our laws promote irresponsibility. The savers, the people who live within their means, are punished. The irresponsible borrow-and-spenders, rich and poor, are subsidized.

You’re playing a little loose with the concept. It’s being a slave to the fear of loss and the mortgage is solely a vehicle in this matter. The overwhelming majority of people don’t intend to walk away from the beginning.

More news to counterbalance the bears…

(various excerpts below)

http://www.latimes.com/business/la-fi-california-economy-20151004-story.html

…The economic news for California lately has been worrying. Turmoil in the markets of China, one of the state’s largest trading partners. A punishing drought that has left a half-million acres of farmland fallow this year. A “business climate” that perpetually ranks near the bottom in national surveys.

But a recent series of economic forecasts paints a different picture. The economy and job market are growing faster in California than the U.S. overall, those reports say, and that trend is expected to continue over the next few years.

Recent high-profile obstacles to economic growth — whether real or perceived — pale in comparison to the state’s position as a magnet for well-educated entrepreneurs, a hub for trade with the Pacific Rim and the center of the technology boom.

Christopher Thornberg, founding partner of Beacon Economics in Los Angeles, offers a simpler explanation.

“The answer is: People want to live here,” he said. “It’s amazing what you can get away with on that.”

The state’s unique climate and geographical delights continue to attract wealthy visitors and immigrants from around the globe.

The Great Recession sent California’s unemployment rate higher than in all but two states, Michigan and Nevada. But its recovery was swift. Economists’ recent projections call for job and GDP growth that will consistently outpace the U.S. through at least 2017, bringing California’s unemployment rate well below its long-run average.

A recent economic forecast from UCLA projects that California’s unemployment rate will fall to 4.8% by 2017, down from a high of more than 12% in 2010.

U.S. Census migration data show that, despite higher personal and corporate income taxes in California, more people making $200,000 or more are moving to California than are leaving.

The state’s unique climate and geographical delights continue to attract wealthy visitors and immigrants from around the globe.

There is nothing “unique” about California’s climate, nor about its geography. Beaches, warm weather, mountains, deserts — you have these in many areas of the U.S. and the world.

What makes L.A. “unique” is its Hollywood PR machine. Hollywood continues to shoot many films and TV shows in L.A., creating a false, yet powerful image of life in L.A. And Hollywood movies and TV shows continue to dominate global entertainment, promoting L.A. to the world. As a place of glitz and glamour, of fame and fortune, of wonders and possibilities. A place where everyone can become a star, a hero, a millionaire. A place where the people are beautiful and friendly and ready to fall in love with you.

Yes, the world does want to live in L.A. Not because of the weather or the beaches or the mountains. But because of the L.A. they see on TV.

They have similar weather and beaches and mountains in nations all along the Mediterranean. Yet there’s no comparable stampede of foreigners from around the world moving to Syria or Lebanon, to Turkey or Israel, or even to France and Greece.

son of a landlord: Although I agree with most of what you stated, I think the climate in coastal So Cal is pretty unique relative to the rest of the U.S. The temperatures are relatively mild all year (see below for Newport Beach as a reference), and there is relatively little humidity or precipitation. There are also not many bugs like elsewhere in the country. I don’t know that you could really ask for much more. It’s a little too hot for me in the summers (especially inland), but overall it’s pretty nice.

Am I missing something? I’d love to know about another U.S. place with weather like coastal So Cal with cheaper housing!

Newport Beach weather:

Jan Feb Mar Apr May Jun

Average high in °F: 63 63 63 64 66 68

Average low in °F: 50 51 52 55 58 61

Jul Aug Sep Oct Nov Dec

Average high in °F: 71 72 72 70 67 63

Average low in °F: 64 65 64 60 54 49

Whenever I leave California for travel, upon my return I always feel happy to be back home. I live in a coastal suburb. You really cannot find better weather. I’d love to find a place to retire to that can match this, but I haven’t been able to. I’m not going to retire to a different country – I love ‘Murica!

Anyway, the deserts of AZ and Vegas are too dry and hot, the east coast is humid and buggy, New England and the midwest get frigid cold – and I’m sorry but I think the midwest is ugly. I thought for a long time about Reno NV, (I love the wide open spaces, Lake Tahoe (heaven on earth), Nevada taxes, and the proximity to Mammoth, SF, Napa, etc. – but the dryness scares me – I already suffer dry eye.

I love the western landscape, the hills, valleys, mountains, lakes, oceanside, breezes, no bugs of this state. Whenever I host guests and relatives from out of town, they go starry eyed at the California gold. Especially young people. One niece remarked, “I feel like I’m in a movie” (speaking of movies). A nephew asked, “how does anyone get any work done.” Others ask “Is the weather always like this?”

Yes, I’m paying the extra taxes to live here – they’re truly “golden handcuffs”.

@Pure_Hapa I’m sorry but that’s pure_crap. It’s been hot as blazes this summer along with a rising dew point over the past decade and a drought does not perfect weather make not to mention the air pollution. Your niece and nephew certainly sound like clueless kids associating the feeling of a fleeting moment in time like a movie to actual day to day life.

Was, Responder, now you have me missing Newport. Lived there as a little kid, a year in high school, then later as an adult for a few years. Great place! The water can be cold but there I learned to love a nice knee deep wade on a warm day.

blertus et al, say whatever you want, coastally it certainly doesn’t get very hot. Are you comparing it to a summer day in the Atlantic seaboard? The AZ desert? The midwest scorchers? Why don’t you visit these other states and tell me how it’s so hot here.

What I said is not a load of crap. YMMV – your mileage here may vary but my viewpoint is real. Both my nephews from Maryland want to move here but know they can’t afford it. Ditto my husband’s nephew in Virginia. We tell them they can’t afford to live in our neighborhood or anywhere near the beach and to sit tight where they are. I fully realize the downsides to living here – I mentioned looking elsewhere for retirement. But the downsides don’t make the upside less real.

They say unique and geographical delights plus people want to live here as supporting evidence but all of those things have always been the case even when things were going the other way. The elephant in the room is this current bubble in tech.

Spot on. And when I lived in SoCal I had people from other parts of the country complain to me about the fake image of the state Hollyweird puts out. They thought they could jump in the ocean like a scene out of baywatch, only to freeze. The traffic, crime, air and water quality – the “coolness” of that image you were sold wears off after a few years, particularly if you are not doing well economically. Who would have ever dreamed that a selling point for a condo/house was its proximity to a starbucks/whole foods?!?

I’m living in tech ground zero and what I see is the middle and working classes being squeezed more and more by falling pay and increasing g expenses, so they’re buying less and less tech. Here in San Jose we tend to use older laptops that were given to us or we got on the cheap, and there are tons of new ones out now in the sub-$300 range. Tons of people out here are using older smartphones, often on WiFi only to avoid a bill.

Payphones are still a thing out here.

The best selling vehicles out here? Bicycles. I’m seeing tons more bike traffic. Bike fatalities, sadly, are up because that many more people can no longer afford cars.

Even as little as a decade ago, internet was 15 bucks a month. Sure, it was slow, but anyone could afford it. Now it more like $100 a month, or even more, so the digital divide is growing. The average person here does not have a high paying or glamorous job. They’re a cheap barber or a lifetime Safeway employee or a janitor or something. Any of those fields, by the way, are a better choice than going into tech where pay has been plummeting for decades.

If it isn’t obvious to anyone yet, the prices of these homes are increasing so rapidly by design. They have to meet or exceed 2006 peak in order to maintain a long term curve. Although most cannot afford these prices the mission of the federal reserve is to inflate us out of this mess top-down. The largest asset most own is their house, then their car, have you seen prices of luxury cars recently? That is where the fed’s inflation party money is going, it’s just a matter of time before the poor start getting some and then you’ll have to add another 0 to our currency. Real estate will continue to rise forever Because the value of the home is a factor of the amount of currency in circulation.

Howard

That is my point. The amount of money necessary to allow the middle class the ability participate in the economy without credit doesn’t exist. It must be taken from the 1% who got it by lending money they know could never be paid back. It’s all just interest and it need to be redistributed to the people it came from

Oregon has every right to discourage mentally deranged people moving up to the territory after that California resident killed our women folk and children. You are lucky that the militia doesn’t close the border to those with CA license plates.

The Pacific Northwest has spawned a disproportionate number of serial killers, without any help from California: http://www.seattlepi.com/local/article/Why-are-there-so-many-serial-killers-in-the-3732021.php

Oregon even exports its serial killers to other countries: http://www.kptv.com/story/23124677/serial-killer-with-oregon-ties-now-linked-to-11-killings

Maybe the rest of the world should ban Oregonians?

I was up in Bellingham, washington for a week and I’ve never been in an angrier town. Everyone was just pissed off.

The PNW can just stay to themselves as far as I am concerned and they all deserve each other.

If you believe everyone from California are mentally deranged murders you sir need to get out of your log cabin/ village and go down south for a while.

“we should all be demanding the media talk of nothing other the the total bullshit the artificially stimulated economy really is until the stock and housing market collapse to a point that represents real value based on people’s ability to consume without credit. If you can’t afford it without credit you shouldn’t be able to buy it.”

Me,

I agree with you, but you lost me with the last statement above.

We live in a credit based system where every single dollar in the economy is created through debt. I am not saying it is a good system. I am just stating the system we live in.

If households, businesses and governments (state and federal) start paying down debt, then the money supply contracts. If it contracts too fast and too much, the system implodes. Now, if that is good or bad it depends on the person and the timing.

Short term, the implosion would be devastating and very painful. Long term, it can be a good thing because of the leaches sucked the whole blood from the system, they will die, too. That can be liberating for the ones left alive. What we see now is a parasitic cabal which does not produces anything which is no longer happy with the golden eggs; they want to kill the goose, too.

Thank you for your response however you are totally incorrect. There are billions of dollars or wealth that existed before credit was an option. That money needs to be speard around to the masses not credit. The fact is the 1% need to have 99% of their wealth redistributed via taxation.

Perfect example is here in CA we have this insane thing called prop 13 which allows a very small portion of the mostly elderly population to access paper equity while not having to pay taxes based on the market values of the Property. If we didn’t have prop 13 we would have very different real estate market because nobody would allow this crazy speculation because most would not be able to afford to stay on their home. We encourage speculation because that a huge source of income for banks who generate fees based on the process. Total insanity!!!!

“Thank you for your response however you are totally incorrect. There are billions of dollars or wealth that existed before credit was an option. That money needs to be speard around to the masses not credit. The fact is the 1% need to have 99% of their wealth redistributed via taxation.”

The current financial system was created by the top US banks through their union/cabal called FED. It is totaly credit based. The FED was created in 1913 (read the book “The Creature from Jeckyll Island”). IRS, the enforcement arm of the FED, was created in the same year. Both the FED and the IRS control the money supply. The government can work without our taxes – the money are created by the FED and given to the government. The IRS takes the taxes to create the illusion that the money are for the government and eliminates them from circulation – control the supply.

Before this system, yes we had real money, made out of gold or silver. Yes, people borrowed money deposited by others. Today, most of the money are created by the comercial banks via lending. Therefore, ALL money are created through debt – no more gold or silver – just bank notes.

Per Yu”Yet another measure of rational housing value is a simple price-to-rent ratio. The ratio is calculated by taking the median home price over the annual median rent in L.A. If the ratio is high — meaning that home prices are beyond their fundamental value based on expected rental revenues — that points to a bubble. Again, let’s look at history.

Two previous peaks were in December 1989, with a ratio of 14.8 to 1, and in February 2006, with a ratio of 24.4. According to Zillow, the current price-to-rent ratio in L.A. was 17.1 in May, which is far below the 2006 bubble level but still higher than any time before 2003.

That doesn’t worry me, though. A high ratio doesn’t spell danger for Los Angeles because, similar to New York (ratio: Manhattan 25, Brooklyn 23) and San Francisco (ratio: 21), it’s now a “superstar” city. L.A.’s size, amenities, weather and geography make its houses an investment target for the global elite. Wealthy individuals from all over the world don’t care that it might make more financial sense to rent, because they’re not simply buying Los Angeles houses to live in them, they’re also trying to diversify their financial portfolios.

@Lee That’s an idiotic viewpoint because if you go back and look at the valleys you’ll find that LA had the same amenities, size, and weather as it does today. You’re basically saying it’s different this time.

yes, it is different now with all the Chinese. Different people and culture

Yeah but LA’s not making tech millionaires by the hundreds like SF or finance bajillionaries like NYC. The economy is different. It’s mostly low or middle wage. Outside of a few lottery winners you don’t have a strong wage base in LA at all. Why should a house in Encino fetch $700K when I can get a better house in Berkeley for less?

That’s quickly changing, with “Silicon Beach” spawning a new tech interest in the Westside. Santa Monica, Playa Vista, Westchester, Venice, now coming down to El Segundo – there is a fast-growing tech sector full of VC-funded startups and others in the area. Exciting times if you are in the software biz. Is it part of a tech bubble? I don’t know. There’s a lot going on – tons of construction of new buildings, malls, hotels and more. I see it every day. I’m also part of the business owner/entrepreneur milieu – so I’m not exactly objective. Just reporting the anecdotal bright side for y’all.

I’m replying to my own comment because comments won’t nest below this level. Response to Pure_Hapa.

True but there haven’t been any big exits like you see in SV all the time. I don’t think there are many companies in LA tech scene that are on the radar of the big SV players for acquisition or for that matter IPO. LA tech is mostly variations of already existing ad tech and as we enter a world of ad blockers I don’t think the display ad or even native ad business is going to survive. Companies are realizing that ad spending online is not a winner due to bots and users ignoring ads. I am not hight on Snapchat as a business. If Twitter is having trouble, then Snapchat is in for double trouble. The ad business model doesn’t work because it cheapens a great service and so-called smart people can’t figure out a way to make anything else happen. Twitter hired old media execs to run its business and LA is full of old media execs. The way I feel about great services and the ad business model is summed up below with a metaphor about eating in a restaurant:

You go to the finest Michelin star restaurant where the chef has been trained in the finest cuisines around the world. The place is spotless and the food was flown directly from organic farms where the food was lovingly and carefully grown. It was delivered in the speediest jet to the restaurant to be served as fresh as possible. Then, on the way to your table, the waiter drops the food on the floor, picks it up and puts it back on the plate before serving it. That’s the ad biz model in a nutshell.

It is a bubble. Last time between 95 and 2000, there were tech companies in LA, a few older guys I used to work for worked at some, and they were gone without any vestige by 2002. I mean just GONE. There are 0 large homegrown tech companies to provide for a sustaining ecosystem. Yeah sure, maybe Disney buys a couple of companies, but they are horrible at tech and every few years they re-org and layoff their entire digital divisions, hire new people, rise, repeat. The tech leadership and talent just isn’t there like it is in SV or even Seattle, Austin, Research Triangle or NYC. But, you gotta get it while the getting is good, so party on if that’s your thing.

Housing market wil tank hard soon. That is because we do not have enough millionaires to buy these ridiculously-priced houses. Unless wages are going up or aloowing liar loans and other fancy loans to return , there is no way average working folks can afford million dollar houses. Property taxes at that purchasing price alone will be a huge financial burden for most of us. Wall Street investors are now learning it the hard way that flipping houses are not easy. Eventually, they will run out of suckers who want to buy their overpriced homes.

http://fortune.com/2015/09/25/housing-wall-street-investment/

“…we do not have enough millionaires to buy these ridiculously-priced houses…”

Been thinking along the same lines for 10+ years. But, counter to all logic, common sense, and the laws of gravity, $1mm+ homes are still selling. But to who? The space people?

Can’t imagine who is left who has sufficient cash flow.

It’s just got to end. But when? 100 years from now?

Homes as ATMs: It’s starting again

http://finance.yahoo.com/news/homes-atms-starting-again-145711369.html

30% of cash back refinancing is in California. Makes sense as that is were most of the appreciation is.

Interesting read.

http://www.zerohedge.com/news/2015-09-30/80-all-new-home-buyers-irvine-are-chinese

Irvine is the most plastic, soulless place I’ve ever seen. So that makes sense.

WestsideGuest, Interesting. I have been wondering how these REITs that buy single family homes, as rentals, would perform. In addition to depreciation and property taxes, they have maintenance, which must be expensive because they pay managers, who hire someone to do it.

The face of employment in CA is changing rapidly. I work for a large insurance company (not publicly traded). We’ve had a fully funded (over funded) pension plan since the dark ages.

Today we were informed pension plan is being scrapped. 401k’s will be offered in its place – with us footing a chunk of the bill. That’s going to affect about 6000 people in a big way.

I have a friend who’s a police officer. Last year the city decided they were done paying for their Calpers pension. All police employees now have 14% of their paycheck deducted and the city throws in a few bucks as a measure of goodwill. 14% of someone’s salary is a massive hit. We all know the majority of Americans (even well paid ones) live right up to their means, and in most cases beyond their means. Already a ton of officers have started to default on their mortgages. 14% of their pay was literally half of their mortgage payment – zap – gone.

My job and my friend’s job is just a small sample of how things are changing. How these middle class homes – at least in the Central Valley where I live, can keep selling at ever increasing prices, is beyond me.

Indeed. The guy I work for is very well paid, and as I like to put it, he has the financial acumen of a 13 year old. Saving? What’s that? He literally makes 15x what I do, and I’ve had to “rescue” him more than once. Small amounts, enough to buy a few groceries, or soap or to get into the swap meet.

I’d like to think that on the huge pay a cop gets, saving 14% would be easy, but apparently in our culture it is not.

The standard church tithe is always 10% because most people, even those don’t think they can, can generally spare 10% without pain.

“How these middle class homes – at least in the Central Valley where I live, can keep selling at ever increasing prices, is beyond me.”

……not for long!!!!

Because people don’t learn that it is over until it’s been over for at least two years.

It always gets worse better it gets better. In this case, we most likely will get higer rents and higher house prices and higher everything: health care, food, bill… for longer.

Nobody knows till when. I just hope it won’t be much longer after the elections… it don’t matter how much money you make… the rents are nuts.

Since I am a Chicagoan, I will offer my insights here. Chicago real estate prices have gone back to 2006 level prices. Some areas close to downtown have gone past the peak prices of 2006. Prices were down severely from 2008 to late 2011. From 2012 to now prices have increased dramatically. The last few months prices are being finally cut from existing houses that are languishing. From 2012 to mid 2015 it was a buying frenzy. Will the market slow down for good? Time will tell.

Also Chicago has a bad reputation in regards to violence, gangs, gang shootings, etc. That is the picture that the national media portrays. Geographically, most of the violence, gangs, murder and mayhem is mostly in the south and west sides of Chicago. And it is only even there confined to smaller pockets. The south and west sides of Chicago are gritty but there are working class folks there. No the whole city is not a huge ghetto that is full of violence and shootings. Things were much worse back in the late 1970’s to 1980’s. Then by the mid 1990’s Chicago saw a huge rates of gentrification. I am not saying the above just because I am a Chicagoan, but I am giving an objective opinion.

Long term fiscal wise, we are fuc*ed. There really is no way to put it. Politicians being what they are will always do the same thing- tax and tax.

Take your pick – a place like Chicago where most things are on the table for all to see, including the problems – or a place like Los Angeles where a lot of the problems are lurking beneath the surface where many people won’t bear to look.

I live on the far north side of Chicago, the Edgewater-West Ridge- Rogers Park area, and have lived in Lakeview and Lincoln Park. I run all over the north side and clear south to Chinatown with no fear.

The crime pits are the far south and west nabes like Garfield Park, the “wild 100s” (100th to 111th st south), Pullman, Englewood, and a few other pockets in that area, which is 25 miles from where I live, and most likely, you as well

I love this city for its lake, its great architecture, its top-tier cultural amenities and educational institutions, its charming neighborhoods, and its good 24/7 public transit. It sickens me to see it destroyed by the leftist mentality. As in so many other wealthy and formerly wealthy cities, people here tend to think that the public till is a bottomless well of causeless wealth, and that it should be Christmas every day for public employees and anyone claiming a “need”. What is especially dismaying is how difficult it is to unseat an incumbent politician, no matter how corrupt and inept. This city’s dismal financial condition owes mostly to two politicians, former Mayor Richard Daley the Younger, who served (himself and cronies) for 4 terms, and 8th Ward Alderman Ed Burke, who has been Chair of the Finance Committee for at least 4 terms, and whose Irish-Catholic constituents WORSHIP him even though he has offered them abundant proof that he is unfit to serve. Neither these 2, nor the 49 other rubber-stamps sitting on the city council, has been asked by the population to account for some of the worst financial management of any city in the country. We don’t have Detroit’s excuse- we are not a dying city whose only industry left it long ago, but a beautiful, vibrant city that is still a draw for talent and wealth… though maybe not for much longer.

Reply to Me

Again totally wrong. If the government is working without tax money then we have total anarchy anyway and total Marshall Law has been declared. My comment suggests the 99% actually exercise the power possessed. If everyone stopped paying their mortgage at once Banks would have one option which is to recognize they are never going to get their principal back. Yes it is the beginning of total cultural reorganization but that is what is required. We all know how the Fed and Irs were created. More than 50% of the population couldn’t even read back then. Today there is no excuse for any not to know and understand exactly what is going on in the world/economy. Point is we have real money and we have real power but only if everyone acts together by refusing to use credit or pay outstanding credit back in unison. Once that is accomplished we will have real price discovery. Question how come the backs got debt forgiveness but not individuals. Obviously nothing really happens if money is paid back to lenders.

Me, I remember back in 2008 when the banks got bailed out some people tried to start a protest movement. There were some viral emails going on and it advocated people from across the country to close their accounts with the Big Banks and to open up accounts with local credit unions or smaller local family owned banks. Of course it didn’t succeed. Because Joe Six Pack is lazy and is sort of like a cheap prostitute. The prostitute always complains about the pimp but she always comes back to him.

Then in October 2011 some activists tried this move again and in Facebook they got only 50,000 likes. In the end, the man on the street only has himself to blame if he keeps taking it over and over again and won’t do anything about it.

ISN’T paid back to Lenders!!’

“Homes as ATMs: It’s starting again”

http://www.cnbc.com/2015/10/05/homes-as-atms-its-starting-again.html

“The lack of homes for sale has caused many potential buyers to stay where they are, even though they have the equity to move up.”

They’re trapped. Ball and chain. There’s nothing quite like the intangibles of immobility.

“In turn, they are using that equity to not only enhance their home but to add to its value.”

They’re being forced to lower their expectations and spending money to cope.

“Cash-out refinances were most popular in California, accounting for 30 percent of all volume, according to Black Knight.”

Of course they were. Would be nice if Doc looked into this.

“but it is unlikely today’s highly cautious, litigation-leery lenders will allow borrowers to take out more cash than is prudent.”

The assertion is that the lenders are taking on all of the risk. Not sure that’s entirely the case.

And then you have Michael Vick who paid back millions and CHOSE to not file BK.

Leave a Reply