Et tu Subprime? Why This Mortgage Proposal is Hot Air…As of Today.

WASHINGTON — President Bush said Thursday concern should be shown to those who’ve lost their homes but it’s not the federal government’s job to bail them out.

“Obviously anybody who loses their home is somebody with whom we must show an enormous empathy,” Bush said. Asked whether he would champion a government bailout, Bush responded: “If you mean direct grants to homeowners, the answer would be `No, I don’t support that.”

“We’re at the very early stages of discussion,” Bush said. “Anything that would be submitted to Congress … would have to be revenue-neutral.”

Today we get the following message from Bush:

“We should not bail out lenders, real estate speculators or those who made the reckless decision to buy a home they knew they could not afford,” he said today, adding there is no perfect solution. “The homeowners deserve our help. The steps I’ve outlined today are a sensible response to a serious challenge.”

And in the same breath they are offering a 5 year rate freeze. You shouldn’t jump to any quick conclusions like the market did today because a study by investment bank Barclays Capital found that of the 2 million subprime ARMs expected to reset from now until 2009 a mere 240,000 would be covered by this freeze. Keep in mind there was a lot of brouhaha when the FHASecure act was issued only a few months back and this program is expected to cover another 200,000 subprime borrowers. Not to be out done, the Democrats have come out with equally irresponsible proposals.

The Democratic presidential candidate proposed several steps to forestall mortgage foreclosures, including a 90-day moratorium on further loan foreclosures on owner-occupied homes and a freeze that would keep subprime mortgage rates from rising for at least five years.

But when you’re President you have more power to get things done. They don’t call you El Presidente for nothing. Here’s a question for all of you armchair economists; if people stop paying or are unable to pay their mortgage, the note holder is still requesting payment, who ends up paying the 3 month moratorium? You need to remember that a primary reason this housing bubble expanded as it did was of the massive amount of easy financing being bought up by Wall Street. No one really cared about the underlying asset as investors trusted hedge funds and rating agencies to ensure that the asset was worth what they were paying for it. Now that we know NINJA loans were more prevalent than anyone wanted to acknowledge, this secondary market is going to dry up quicker than a prune in the sun since investors realize the government can step in and alter loans at any first sign of weakness. Why do you think businesses don’t do so well in communist regimes? Why work harder when at any moment, the government can step in and assume ownership? It has a lot to do with psychological motivation and human nature but suffice it to say that the asset back securities markets are not coming back. We are seeing a sharp jump in many lending companies such as Countrywide and Washington Mutual but this is partly due to the implication that they will be bailed out. One caveat should have been thrown into this plan and the political effect would still be the same. All 48 states except

I understand the desire to help communities such as

Median Home Price:

Detroit: $98,866

Cleveland: $124,812

Los Angeles: $565,000

San Diego: $515,000

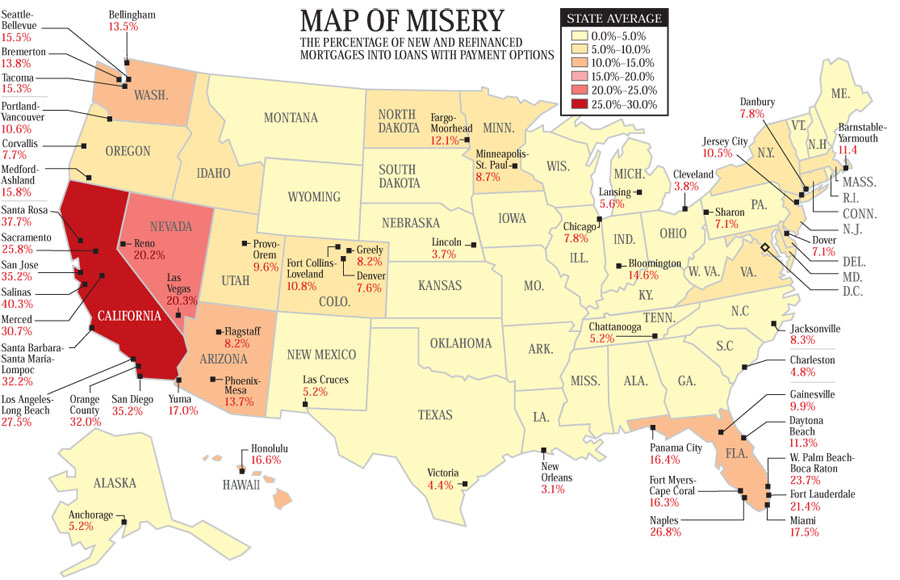

Notice a slight difference? Now you have an idea why these lenders are pushing so hard. And here is a visual in case you need more evidence:

You’ll notice that the plan also specifies that places be owner occupied. There have been so many cases where people bought second homes and lenders “checked†owner occupied to bring in better rates for their clients. Now what is going to happen when lenders start scrutinizing documents (something they should have done to begin with) and realize the owner isn’t living in the property? Will they fudge the numbers again? Thankfully we are allowing the fox to guard the henhouse. This plan is flawed since it gives power to the corruptors that caused this mess to begin with. Now they are asking them to resolve it? If the plan would have more teeth and substance, they would ask a neutral third party to serve as a trustee in reworking the mortgages. But again as you are surely realizing, this plan is designed to bailout the lenders more than the people in need.

There is a source of irony that the same administration that is criticizing “socialized medicine†is socializing corporate losses. I know there are many doubters out there but just take a look at who Paulson has been meeting with and you’ll get the idea. Why wasn’t the OFHEO, you know, the OFFICE OF FEDERAL HOUSING ENTERPRISE OVERSIGHT at these meetings? Bwahaha! We already have a governmental agency that is setup up to oversee housing and they aren’t included in this deal! As the plan stands, it won’t have that large of an impact – estimates range from 10 to 12 percent of subprime loans – and the plan will be more of a political ploy in a hyper political year. Bush doesn’t want to go out with a crashing housing market and Democrats don’t want to inherit a faltering market which they will be blamed for. In the past week we’ve had these great ideas thrown around as well:

Countrywide CEO seeks $625,000 Fannie/Freddie cap

NEW YORK, Dec 5 (Reuters) – Countrywide Financial Corp’s chief executive called on the U.S. Congress to temporarily raise the maximum size of mortgages that Fannie Mae Freddie Mac and the Federal Housing Administration may buy or insure by 50 percent to $625,000.

WaMu chairman says Fed cuts, liquidity needed for housing markets

“I think it will help, but it won’t be the whole solution,” Killinger said during a panel discussion organized by the Office of Thrift Supervision. “If the Fed continues to reduce rates that will increase the likelihood that other interest rates will follow.”

Expect housing related stocks to rally this week and next week with Uncle Ben cutting rates by .25 or even .5 points. If rates are cut by .25, expect neutral movement but expect a major jump if rates are cut by .5 points (the market is betting on this). The bigger concern of course is trying to raise caps since this will only institutionalize bubble prices caused by the housing complex and pass on the bill to the tax payer via government mortgage securitization. Keep your eyes peeled because we are treading on a slippery slope.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

18 Responses to “Et tu Subprime? Why This Mortgage Proposal is Hot Air…As of Today.”

Excellent post! I was wondering why Bush stuck his nose in this. It seems so un-Republican to me. Then I read this:

“The Democratic presidential candidate proposed several steps to forestall mortgage foreclosures, including a 90-day moratorium on further loan foreclosures on owner-occupied homes and a freeze that would keep subprime mortgage rates from rising for at least five years.”

Are they insane? Can you say “implications,” boys and girls? Let’s take the messiest mortgage fiasco ever and make it worse.

“Overcoming Real Estate Losses” at http://WhineCountryRealEstate.blogspot.com/

Well said, Dr.

I’m sitting here listening to Schiff on Fox news, dated 12/4. They’re talking about potential runs on US banks. I share Schiff’s concern. If you pull your money out of bank, what will it be worth?

Peter Schiff December 4 2007 Fox News

@carol,

Both plans are simply political ploys. “He said he would freeze rates for five years. I offer you a 10 year rate freeze!” Such populist messages usually leave the details out.

@Tyrone,

Poor Schiff. I’m not sure why Fox News keeps bringing him on. They clearly use him as a punching bag but he holds his own.

Here is a logical extension of this proposal. We can agree that this freeze will essentially extend the introductory rate for a few more years until it resets. A 2/28 or 3/27 loan becomes a 5/25 mortgage. Now if a current subprime borrower with a NINJA loan cannot make a payment today without rates resetting, what suggests that he will be able to make the payment in 2012? The following proposal assumes:

a) The borrower will miraculously have a high enough income to support the new payment in the future

b) Housing prices will be back on their perpetual appreciation treadmill thus allowing the owner to sell

c) Buying time for more government bailouts

In fact, the irony from the details given to us so far, once the mortgage fully amortizes the payment will be larger in the future than if it simply reset today! Now instead of amortizing over 28 years it is fully adjusting at 25 years. Eventually someone is going to payoff the note. It is current a game of hot mortgage potato. Where it lands, nobody knows!

From The Washington Post…

IT’S NOT 1929, BUT IT’S THE BIGGEST MESS SINCE

By Steven Pearlstein

Washington Post, Wednesday, December 5, 2007; Page D01

It was Charles Mackay, the 19th-century Scottish journalist, who observed that men go mad in herds but only come to their senses one by one.

We are only at the beginning of the financial world coming to its senses after the bursting of the biggest credit bubble the world has seen. Everyone seems to acknowledge now that there will be lots of mortgage foreclosures and that house prices will fall nationally for the first time since the Great Depression. Some lenders and hedge funds have failed, while some banks have taken painful write-offs and fired executives. There’s even a growing recognition that a recession is over the horizon.

But let me assure you, you ain’t seen nothing, yet!

What’s important to understand is that, contrary to what you heard from President Bush yesterday, this isn’t just a mortgage or housing crisis. The financial giants that originated, packaged, rated and insured all those subprime mortgages were the same ones, run by the same executives, with the same fee incentives, using the same financial technologies and risk-management systems, who originated, packaged, rated and insured home-equity loans, commercial real estate loans, credit card loans and loans to finance corporate buyouts.

It is highly unlikely that these organizations did a significantly better job with those other lines of business than they did with mortgages. But the extent of those misjudgments will be revealed only once the economy has slowed, as it surely will.

At the center of this still-unfolding disaster is the Collateralized Debt Obligation, or CDO. CDOs are not new — they were at the center of a boom and bust in manufacturing housing loans in the early 2000s. But in the past several years, the CDO market has exploded, fueling not only a mortgage boom but expansion of all manner of credit. By one estimate, the face value of outstanding CDOs is nearly $2 trillion.

But let’s begin with the mortgage-backed CDO. By now, almost everyone knows that most mortgages are no longer held by banks until they are paid off: They are packaged with other mortgages and sold to investors much like a bond.

In the simple version, each investor owned a small percentage of the entire package and got the same yield as all the other investors. Then someone figured out that you could do a bigger business by selling them off in tranches corresponding to different levels of credit risk. Under this arrangement, if any of the mortgages in the pool defaulted, the riskiest tranche would absorb all the losses until its entire investment was wiped out, followed by the next riskiest and the next.

With these tranches, mortgage debt could be divided among classes of investors. The riskiest tranches — those with the lowest credit ratings — were sold to hedge funds and junk bond funds whose investors wanted the higher yields that went with the higher risk. The safest ones, offering lower yields and Treasury-like AAA ratings, were snapped up by risk-averse pension funds and money market funds. The least sought-after tranches were those in the middle, the “mezzanine” tranches, which offered middling yields for supposedly moderate risks.

Stick with me now, because this is where it gets interesting. For it is at this point that the banks got the bright idea of buying up a bunch of mezzanine tranches from various pools. Then, using fancy computer models, they convinced themselves and the rating agencies that by repeating the same “tranching” process, they could use these mezzanine-rated assets to create a new set of securities — some of them junk, some mezzanine, but the bulk of them with the AAA ratings more investors desired.

It was a marvelous piece of financial alchemy, one that made Wall Street banks and the ratings agencies billions of dollars in fees. And because so much borrowed money was used — in buying the original mortgages, buying the tranches for the CDOs and then in buying the tranches of the CDOs — the whole thing was so highly leveraged that the returns, at least on paper, were very attractive. No wonder they were snatched up by British hedge funds, German savings banks, oil-rich Norwegian villages and Florida pension funds.

What we know now, of course, is that the investment banks and ratings agencies underestimated the risk that mortgage defaults would rise so dramatically that even AAA investments could lose their value.

One analysis, by Eidesis Capital, a fund specializing in CDOs, estimates that, of the CDOs issued during the peak years of 2006 and 2007, investors in all but the AAA tranches will lose all their money, and even those will suffer losses of 6 to 31 percent.

And looking across the sector, J.P. Morgan’s CDO analysts estimate that there will be at least $300 billion in eventual credit losses, the bulk of which is still hidden from public view. That includes at least $30 billion in additional write-downs at major banks and investment houses, and much more at hedge funds that, for the most part, remain in a state of denial.

As part of the unwinding process, the rating agencies are in the midst of a massive and embarrassing downgrading process that will force many banks, pension funds and money market funds to sell their CDO holdings into a market so bereft of buyers that, in one recent transaction, a desperate E-Trade was able to get only 27 cents on the dollar for its highly rated portfolio.

Meanwhile, banks that are forced to hold on to their CDO assets will be required to set aside much more of their own capital as a financial cushion. That will sharply reduce the money they have available for making new loans.

And it doesn’t stop there. CDO losses now threaten the AAA ratings of a number of insurance companies that bought CDO paper or insured against CDO losses. And because some of those insurers also have provided insurance to investors in tax-exempt bonds, states and municipalities have decided to pull back on new bond offerings because investors have become skittish.

If all this sounds like a financial house of cards, that’s because it is. And it is about to come crashing down, with serious consequences not only for banks and investors but for the economy as a whole.

That’s not just my opinion. It’s why banks are husbanding their cash and why the outstanding stock of bank loans and commercial paper is shrinking dramatically.

It is why Treasury officials are working overtime on schemes to stem the tide of mortgage foreclosures and provide a new vehicle to buy up CDO assets.

It’s why state and federal budget officials are anticipating sharp decreases in tax revenue next year.

And it is why the Federal Reserve is now willing to toss aside concerns about inflation, the dollar and bailing out Wall Street, and move aggressively to cut interest rates and pump additional funds directly into the banking system.

This may not be 1929. But it’s a good bet that it’s way more serious than the junk bond crisis of 1987, the S&L crisis of 1990 or the bursting of the tech bubble in 2001.

Dr- another fine analysis. You know, I am not hard hearted. I feel for a lot of these people who are in over their heads and facing financial ruin. A common theme I hear is that these folks trusted their real estate agent and mortgage broker. The single mother who felt pressured to sign the papers quickly. The 80 year old about to lose his one and only home due to a resetting ARM. They expected that these “professionals” had a fiduciary obligation to them. They did not realize that in fact their only obligation was to churning inflated mortgages. The common refrain: Trust. But here’s the thing… when did it become American to sign legal documents for massive amounts of money on blind trust? What’s the reason for this trust to begin with? I mean, why is this assumed by so many of our good citizens that you can trust these guys – instead of assuming that anytime you’re dealing with money there lies a potential swindle? This may be a stretch, but I think we as a society are just so used to purveyors of bad products/services facing justice, that there seems to be an automatic backdoor to escape or make right bad consequences. If I can sue a doctor for malpractice then why not the professionals Crisp&Cole or Countrywide? I think not only were people swept up in the general exuberance, but also just sorta expected in the back of their minds that there would be redress if it all went wrong. Moral Hazard 101.

A bit hypocritical, is it not, to have the whole first paragraph of your (good) article covered by an advertisement for mortgage refinance?

Not only is subprime falling apart but now it appears that auto loan deliquency rates are climbing. This whole debt bubble is going to end very badly. Unfortunately we will see more government intervention in the markets that will just prolong the adjustment process that must take place. Expect the goofy ideas from Washington to grow as the deliquency rates grow.

i think the term “hot air” is commendably polite 🙂

and to think i could’ve gambled, gotten myself a house i couldn’t afford, and qualified for an extension of terms better than my neighbor

and, from what i’ve heard, the pre-payment penalty was left untouched; perpetual debt slaves? or oversight? hmmmmm….

If I had a $500,000 mortgage on a $400,000 house that I could rent for half of my mortgage payment, a foreclosure would be a blessing. It would get me out of a bad financial situation. Of course once I stopped making payments my lender would have to take the $100,000 loss. They wouldn’t want that. If only there was some way they could keep me from going into foreclosure….

“Is the media afraid to admit we are in a major housing bubble?”

Of course they are, Dr. HB! This is the advertiser paid msm we’re talking about here ya know. One example from the chyron at cnbc:

BREAKING NEWS

“Paulson says US needs affordable mortgages”

No, Mr. Paulson, what the US needs is affordable housing. This scheme, while pandering politically big time, can’t and won’t work. Its true intent is to try and keep house prices propped up until election. Would-be buyers, now subject to strict underwriting standards (quaint, isn’t it?) can’t afford these houses at these nosebleed levels. Easy credit is what drove this bubble (as you point out in almost every post) and its going away is what’s popping it.

Dr. Housing Bubble,

By definition if President Bush introduces a program it is free market in nature. For you to say otherwise just illustrates how far left and partisan you are. Why don’t you move to Venezuela if you hate market economies so much?

“A 2/28 or 3/27 loan becomes a 5/25 mortgage.”

I was wondering about that. My understanding is that nothing would change in the loan except the interest rate being charged at the time and that you would still have to start paying back principal as originally scheduled. If what you write above is the plan then they are not just prolonging the popping bubble, they delaying it and making the eventual pop even greater.

If the problem is the adding on of the principal that makes the mortgage unaffordable, then they should have looked at making the loans from a 2/28 or 3/27 to a 2/30, 3/30 or even 5/30.

Not that this is going to stop people from defaulting. If anything more people will default in the short-term just to avoid being caught up in this mess.

Watch, two years from now, those with frozen rates will be screaming because interest rates are down and their were fixed due to the ‘Freeze’.

Hello. I have been reading your site for a while now. However I never posted. I just want to say you write some great stuff! Keep up the good work! Anyway, my two cents in all this mess just goes down to basics. Prices of houses has gotten way out of hand for the average person. The average Joe has reached its threshold and cannot afford the home prices anymore. In come the exotic mortgages to help out! However, that was just a band-aid over the real fundamental problem of house prices had gotten far away from incomes for years and now the two needs to be brought back in alignment. The housing crash most likely would have helped to accomplish this but now it looks like the government and the banks etc. are trying to forestall this natural cycle and prop up houses again. So I have no idea where this will all end but could it be that we may end up like Japan’s housing crash that lasted for many years?

@Fred,

Looking at the data more carefully, it only seems like a a very small subset of mortgages outstanding will be impacted. I need to make a correction, many of the loans fall in the 2/28 category so the 5 year freeze will in effect turn them into 7/23 loans. From what I am gathering, it is simply delaying the inevitable unless the market recovers or the buyer can make up the income to support the new payment in 5 years.

How this will work out is yet to be seen.

You guys will love this. MarketWatch has a brief Q & A section regarding the new proposal. Take a look at it and tell us what you think. So 600,000 people in foreclosure do not qualify leaving a pool of 1.2 million. From this pool of 1.2 million only 150,000 to 200,000 qualify. This is exactly why the government should stay out of the free markets. I can see it already on the mainstream media, “How can a person with horrible credit get a rate freeze while I have good credit and an adjustable rate mortgage and can’t get squat! Give me my piece of the pie!” If it were to stay, I would be fine with the plan but you are all smart and intelligent people and know exactly where this is heading. Make sure your local Congress person and representatives know exactly how you feel about this. Here is a sample question from MarketWatch:

I thought this was going to be a blanket freeze on all interest-rate resets? Why not just freeze everybody’s interest rate? Wouldn’t that prevent more foreclosures without having to evaluate each loan?

Freezing everybody’s rate would violate the rules for securitizing mortgages, which typically allow modifications only when the loan is in default or in danger of going into default. The goal of preventing foreclosures was balanced with the goal of maintaining a functioning securities market, which could be decimated if the accounting or tax treatment of securitized loans were changed ad hoc.

Mortgage Plan Q & A

@debbie,

You bring up good points that will be wrestled with shortly. This is merely a tiny fix for a few people. All it does is prolongs the inevitable for a few more years. This will seem like a distant story once the fever goes down and reality sets in, in particular when Q1 has an amazing amount of loans resetting and people will have credit card payments coming due from holiday shopping. Remember the head spinning with FHASecure? The housing sector rallied for a week but then the foreclosure numbers, median price decreases, and fraud started hitting the table and folks realized this is a structural problem that runs much deeper than simply subprime. I’m sure next year we’ll start hearing the lawsuits hit the table. The problem is that many of the brokers selling horrible mortgage products are now defunct. People will need to go after someone higher up in the food chain such as hedge funds or Wall Street but good luck there. The issue with this plan is it is essentially a ploy to allow people to unload horrible mortgage products into government sponsored products. This is not stated but the idea is eventually housing will go up and these subprime borrowers will be able to sell their home to an unsuspecting diligent person on a prime government mortgage and all will be well. The note is moved off the risky secondary market and now has an implicit guarantee by the government. The only question is will future buyers want to buy homes at current prices? My guess is the answer is no. In fact, rates are at multi decade lows, productivity is still high, employment is supposedly good so why do people need banana republic mortgages to purchases homes? Simple. Prices are in a bubble. Is the media afraid to admit we are in a major housing bubble?

Just in case you were wondering, Southern California short sales are up for the 22nd consecutive week:

http://www.doctorhousingbubble.com/forum/viewtopic.php?p=330#330

Looking at the details of the agreement at http://www.americansecuritization.com it seems that there will be no delay in the date when the borrow should start paying back the principal. This agreement will only effect the interest rate charged:

“For loans that require payment of interest only prior to the initial reset, followed by amortizing payments, the rate would be kept at the current rate during the modification term, but the borrower would be required to make an amortizing payment beginning after the reset date.”

Also, it seems that if it is certain that you qualify, it might be best NOT TO SIGN an agreement to the new terms freezing the interest rate because your rate may still be lowered if it would have been lower under the original loan agreement. This would in effect cap your interest rate. How do you like them apples… (They probably need to do this to avoid being sued for failing to honor the original loan agreement)

Leave a Reply