Federal Reserve and U.S. Treasury Don’t Like You, Nothing Personal: 3 Emerging Economic Trends; Adjustable Rate Mortgages Disappearing, Federal Reserve Wants More Money, and Financial Honor.

In the investing world you learn to expect the unexpected. I think most of us can put our pride aside and realize that we are living in a very different financial world, one that has not been seen in over a generation. In these gut wrenching times, you might as well spend your money on going to Magic Mountain instead of playing the stock market. So many investing philosophies are being turned on their head. Does dollar cost averaging still make sense? Is having your money in the S & P 500 really mean you’re diversified? Is real estate the safest investment? I think these questions are making many over the counter pop finance books seem obsolete.

I hate to break it to you but the Federal Reserve and U.S. Treasury really don’t like you. They view most Americans as hamsters that serve only one purpose, to shop and consume. You will never hear them trying to push an agenda that would encourage Americans to be savers or manage their money wisely. How can they? They don’t do it so for them to say this would be hypocritical. In fact, their policy actions including dropping rates to near zero put us in a perilous situation that now is looking more and more like Japan’s lost decade. We have Ben Bernanke saying this to an audience in London:

“In my view … fiscal actions are unlikely to promote a lasting recovery unless they are accompanied by strong measures to further stabilize and strengthen the financial system,” Bernanke said.”

This guy. He has already taken on over $2 trillion onto the books of the Federal Reserve with questionable assets and he is still asking for more. These are the actions of a monetary policy ideologue. He is going to have a tough time admitting that monetary policy is simply not helping anyone aside from his masters in the crony capitalist regime. The banks have done so well, that we even have Citi and Morgan Stanley merging brokerages. While people are being laid off left and right, we have a $2.7 billion deal going down. And make no mistake, Morgan Stanley is only doing this because the Fed and other government institutions are back stopping $306 billion in toxic assets. Bernanke then gives us another nugget of wisdom:

“Financial markets remain frozen partly because a “large quantity of troubled, hard-to-value assets” is still on institutions’ balance sheets, Bernanke said.

There are several ways to solve this problem, he said, all involving public funds.

The government could simply buy the troubled assets, or it could give asset guarantees and agree to absorb part of the prospective losses, he said.

“Yet another approach would be to set up and capitalize so-called ‘bad banks,’ which would purchase assets from financial institutions in exchange for cash and equity in the bad bank,” Bernanke said.”

Here we go with this stupid bad bank idea again. Keep in mind that Wall Street and banks have hidden the most insidious stuff and are only itching to load it off onto the American tax payer. The premise of the bad bank is such a stupid notion. You want to know a secret? We already have a bad bank. In fact, we have about 8,300 of them!

It Was Good Knowing you Adjustable Rate Mortgages

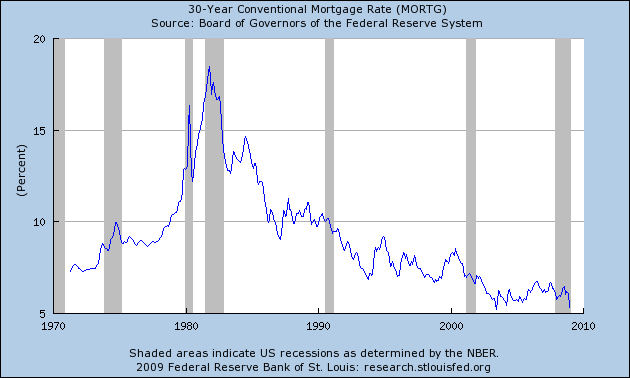

If you haven’t noticed, adjustable rate mortgages especially the pay option ARM variety are probably the most toxic financial instruments ever created. The irony of this all is that mortgage rates are now at historical lows:

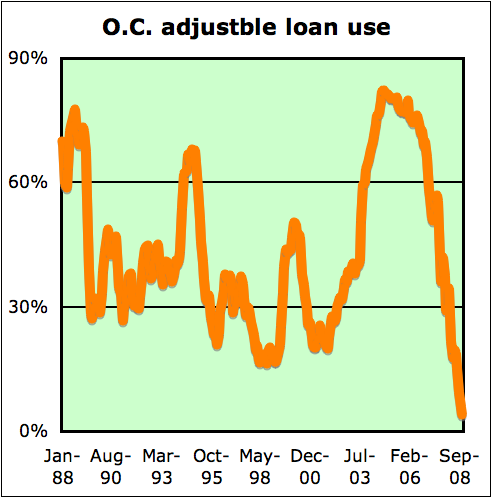

With lower rates, you would expect this to be good for the housing market yet the problem with many option ARMs isn’t the rate, it is the terms once a recast hit. The rate can be zero and it will still send thousands of families on the street. Many on more conventional adjustable rate mortgages may benefit with recent lower rates. Yet this is a very small percentage. And guess what? It looks like we are saying adios to adjustable rate mortgages here in Southern California:

Source:Â Lanser on Real Estate

In November, only 4% of all homes bought used adjustable-rate mortgages. This is the lowest rate since the survey started back in 1988. A couple of things are happening here. First, many of the defunct toxic mortgage shops have now imploded and many were here in Orange County including New Century Financial. So new buyers may not have a wholesale shop to buy from. Second, many people now realize the destructiveness of these products and no longer want to use them. Third, there is no secondary market for this crap anymore. In addition, why would you want to go with one of these products when the 30 year fixed is now at historical lows? If rates shoot up in the future, the ARM is a horrible product. Why not lock in rates at the bottom right now (assuming you are buying)?

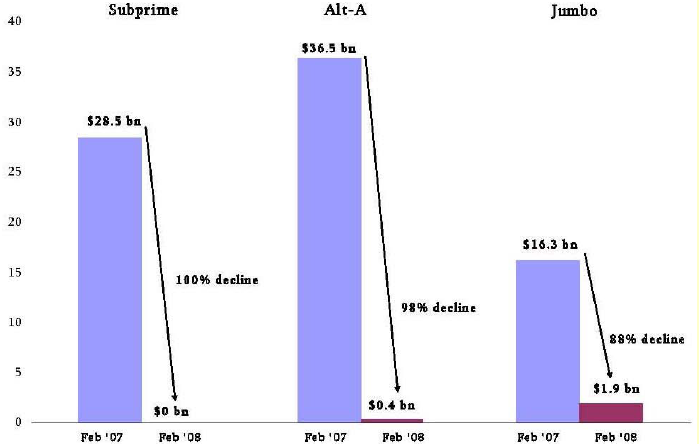

Much of the exotic mortgage financing is pretty much being flushed out of the market:

Subprime is now gone. Alt-A is nearly extinct. And jumbo is a tiny ballgame. Plus, in one or two years we won’t even need to worry ourselves about jumbo loans in California since property values won’t even come close to the loan limits. Get ready for a 30 year fixed world. Adios toxic mortgages, it was fun while it lasted.

The Shame of Finances

Some of you may have heard the story of Adolf Merckle, the German billionaire who killed himself after his empire started having some trouble due to the economic crisis. Keep in mind that Mr. Merckle was ranked as the 94th richest man in the world and his bad bets, mostly on Volkswagen ended up costing him $535 million which still left him with a sizable portion of his wealth intact. His wealth last year was estimated at $9.2 billion:

“His family, which had reported him missing after he failed to return home, said in a statement: “Adolf Merckle lived and worked for his family and his firms.”

“The distress to his firms caused by the financial crisis and the related uncertainties of recent weeks, along with the helplessness of no longer being able to act, broke the passionate family businessman, and he ended his life.”

You know the sad thing here is that he did not do anything illegal. From all reports, it looks like his life was business and he took on a major hit that must have struck deep at his identity as a successful businessman. There are many cases of Japanese businessmen committing suicide because of bad business deals. Shame and honor run deeper in other cultures it would seem.

In our culture, we have people like Bernard Madoff running a $50 billion Ponzi scheme and being out on bail lounging at his Manhattan penthouse.  In the process, he is sending jewelry to family members. Think of the parade of CEOs going in front of Congress, getting verbally tongue lashed only to have their entire financial fortune untouched. They have no shame. They don’t care. Do you think they know what honor is? That is why many in our society will never understand the suicides of some of these other wealthy individuals. They can’t understand how someone can place something so high that it actually crushes their spirit and the only option out they see is suicide. Yet looking at our prima donna wealthy class, I am not shocked that these people have no shame or even honor. They can’t even spend one night in jail!

I’ve had a debate with colleagues regarding teaching ethics. I’m in the camp that just because you cannot instill ethics into someone, that does not mean we should not try having some guidelines. If you are a product of your environment, think of what future generations will become? What do you think a nation run on pure consumption will produce? It commercializes everything. In fact, Bernard Madoff is only the whipping boy of a deeply corrupt Wall Street culture with no honor. They are only looking out for themselves and finally, the majority of Americans realize that they have been played. To only know how things will look in 2019. I think even 2010 will look like a vastly different investing world.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

18 Responses to “Federal Reserve and U.S. Treasury Don’t Like You, Nothing Personal: 3 Emerging Economic Trends; Adjustable Rate Mortgages Disappearing, Federal Reserve Wants More Money, and Financial Honor.”

Good post, Doc. We’re in a muck of shameless greed, with no moral compass.

Ben Bernanke is an asshole. He has no right to take our money and give it to other rich assholes. I have nothing but total hatred for these people. It sickens me. They are worse than common thieves because they are educated and know better I cannot comprehend how they can have the audacity to take taxpayers money to write off bad loans that they made in the clear light of day. ASSHOLES.

Madoff is just one bad apple in a barrel full of bad apples. I truly wish that more of them would jump out of their office windows.

If the American people really understood what these pricks are doing with our money, there would be a revolution.

“pre-Madonna wealthy class” – is this a cultural reference I’m not getting (“Living in a material world/And I am a material girl” – but wouldn’t that be post-Madonna?), or a Cupertino for “prima donna wealthy class”?

I’m not excusing his alleged behavior, but Mr. Madoff is being used as a diversion by the elite.

Right on doctor. Only reading DHB keeps me sane in these insane times.

Ethics absolutely should be taught in every level of school from pre-school through graduate school. People need guidelines, and need to be reminded what they do in life effects more than just themselves and reflects not only on themselves but on the society as a whole. When I was in film school I tried to get a ethics class started feeling people should be aware of how their stories effect and influence people. Much of what has gone on in the past ten years in the economy and in housing though really comes down to people doing sketchy things based on the justification: “everyone else is doing it.”

Which should trigger a warning for the sensible.

Real honor includes persisting with strength and purpose after being humbled by fate or events. This was the ur-message of Greek tragedy (and to some extent comedy) and Roman philosophy.

~

From one angle, Mr. Merckle couldn’t withstand a blow to his ego or self-image as “successful businessman.” That is sad…and common enough. But…his identity was challenged?

~

Welcome to what the most of us endure all the time!!! It’s not enough that two or more adults in a household have to work full time or more, demolishing their hopes, interests, personalities, marriages, families, communities, and still fall behind more each year because of eroded wages and the systematic devaluation of the dollar.

~

It’s not enough that we’re supposed to change careers at the whim of those who concentrate wealth, because the career we dedicated ourselves to is not profitable for them at the moment. No, we must be Flexible, Cheerful, Politically Correct, Perky, Willing to Adapt, and ready to go to welding school or skydiving camp or McDonald’s University…because our overlords say to…because profits must be propped up for the rentier class. Then take time off without pay and have our hard work punished while scamming is rewarded. While doing the work of three or ten or 20 people.

~

Hell, we can’t AFFORD an identity!!! (Which is why peddling consumerist identity symbols has been such a lucrative industry. And why they never fill the hole in the heart.)

~

As for death by train–I noted before that Mr. Merckle chose an Anna Karenina death. I did not intend to be trite or mean. Anna jumped in front of a train in despair to close a circle that never should have opened: she’d witnessed the railway worker’s train death the day she met Aloysha/Vronsky. When reality challenged her ego to its roots, she chose to counterfeit the sad demise of a poor man who’d had none of her privileges or life choices. What honor is there in bringing homicide and trauma on a train engineer?

~

Wasn’t it Thomas Jefferson who said that no one can acquire honor by doing what’s wrong? Character and honor rest with the people who maintained it in the good times. They will shine in the bad the same way, only now maybe we’ll be able to see them more clearly.

~

rose

As a long time reader thanks you for your insight doctor. It is hard to imagine how large 50 billion is. Madoff”s 50 billlion take is the size of our entire state budget in Ohio. Our state is not near as large at California, but it would be hard to imagine Ohio with no jails, highway patrol, or other parts of the state budget.

You want to invest? Buy gold. When the dollar and our economy are smoldering in ruins, gold will still have value. And you don’t need to entrust it to anyone. Buy physical gold coins and/or bars for any savings you have left.

Doctor, thank you for your hard work and tenacity.

Too bad so many don’t understand the American Dream is not about the persuit of money.

Doctor,

I love this Blog!

Here in Switzerland (and in many other countries) we don’t have the “benefit” of the artificially constructed 30year mortgage that allows the borrower to bet way long on interest rates rising, but allows him to break the contract at his convienience if it falls. People typically finance part of their housing debt with 3-5 year notes when rates are low, and they finance another part with variable bank notes or 3/6 month floating libor rates. I currently have a 3mo libor at 1.6%! My 5yr fixed is at 3.25%.

These mixed, shorter term mixed mortgages don’t stick the bank with all the interest rate risk, and they also force the borrower to consider if he could afford the loan if rates shot up to 8-10%.

Another possible advantage is that the Central Bank has much more control over liquidity and growth expectations through changing CB interest rates that quicky impact housing payments.

I just want to point

Great article. Everything comes down to the moral aspects.

By the end of 19th century – many ideas about responsibility

of the economy were transformed into reality. They were

supported by many representants of the economy, politics and science.

Many CEO’s today are living in a completely remote world which

has in reality nothing to do with business.

It is a soviet-like nomenclatura of decadent parasites

where everyone in the company (except from nomenclatura)

is a replaceable commodity and they are convinced that the company they

alledgedly “manage” belongs to them. They can do with it

what they want – without any regret or fear.

So there is implicitely no place for any responsibility.

This was exactly the hallmark of soviet companies.

We saw that US/UK companies which existed over a century were

distroyed within a few years by tie wearing, greedy liars.

The decent work of millions of responsible people was washed away like litter.

The people sitting at the top had to just to be cronies.

One year they sat at the top of company X of industry I, next

year in company B of industry J. They had no idea about

I and J … this was just a bunch of “Führer’s”.

Before the truth came out, they fired people to increase the

share price.Then they get the golden parachute, and

they successors which come from the same sort of “culture” whine

today for baylouts, and fire even more people.

If this system won’t change – then all the baylouts are lost

money – and people will be punished for generations, IF

the damage can be repaired at all.

“There are several ways to solve this problem, he said, all involving public funds.”

Please note: when all these people on all these issues (housing, finance, healthcare, education, etc…) all propose the same solution (more government) you must conclude that they are more focussed on their solution than the problems.

And as people look to someone to promise them the easy answers more government is what we will have. More money coming out of the private sector to pay for it. More from the producers to pay for the non-producers.

It’s like one of those dreams…

I forgot to mention the effect all this debt is gonna have on the rates we (as a state and nation) pay to borrow and on the kids and grandkids of the next generations.

Michelle Malkin calls the proposed stimulus package the “Intergenerational Theft Act” and THAT’S as honest assessment as you’re ever gonna get-

I think America has become a saloon. People around the world come here, party, play the financial system, and then leave. Players here and around the world know that there is no accountability and they have no God. They are merely egotistic, immature fools who have no regard for the damage they have created.

Just like the baby boomers overwhelmed the social norms in the 60’s, the dollar doomers of the 2000’s have overwhelmed the world financial system. Nobody knows where we go from here, but you can bet it will never be the same world again. Most people can feel the tension and that the dam is about to break. It won’t just be McMansions that are underwater….

@ Rose — Very nice writing. Sorry it is such a rant toward despair, but that is indeed our lot.

Great blog, is the answer foreign wealth funds?

I am starting up a new company. If I can get 10 investors each contributing a million each and then we can borrow another 10000000 from a bank. We the start loaning the money to anyone we want without any proper due diligence and secure the loans with mortgages. We make 9000 on each loan we make and then sell the loans to Fannie Mae, Freddie Mac or some investment bank who will pay us back in full our monies expended on the loan so we can make another 9000 per loan. Oh oh, people aren’t paying back the loans. Huh, we have just loaned another 20 million to consumers who are buying 800 sq. ft. homes for 750000 with no docs. We cant sell those loans? We cant pay ourselves 1000000 a year. Oh, the Federal government will bail us out in full cause if we go under the system will fail.

Well the system did fail and my question to you is how much does the government have to bail us all out? Eventually their will be inflation if we continue to print money without any stability.

When the books are written you will read that 2001-2006 real estate price run-up was a dream to the people that bought before 2000 and didnt sell prior to 2007 and a nightmare for those did purchase during that period. Prices are going back to 1999 levels before this is over. Trust me I know and so does this the good Doctor on this site. Dont buy unless the numbers work for you.

Leave a Reply