FHA loan guarantees now amount to $1.1 trillion: Upcoming changes to FHA mortgage insurance premiums and the cost of low down payment loans.

FHA insured loans stepped in to take up a lot of the slack when other low down payment loans exited the market in 2007. FHA insured loans are still a low down payment option requiring only 3.5 percent down but at least with these loans, some level of due diligence is done when looking at potential borrowers. Yet over the last few years, FHA insured loans have gone from a tiny piece of the housing market to now being up over $1.1 trillion in loan guarantees outstanding. The housing market is now becoming largely bimodal with all cash buyers picking up better properties while those with barely any down payment funds opt to go the FHA route. Given how expensive FHA loans have become, it is apparent that a large portion of the population doesn’t even have enough to enter the housing market without 30x leverage. Changes are also coming to FHA insured loans that will make them more expensive in a few months. Why are these loans getting more expensive when the housing market is supposedly robust?

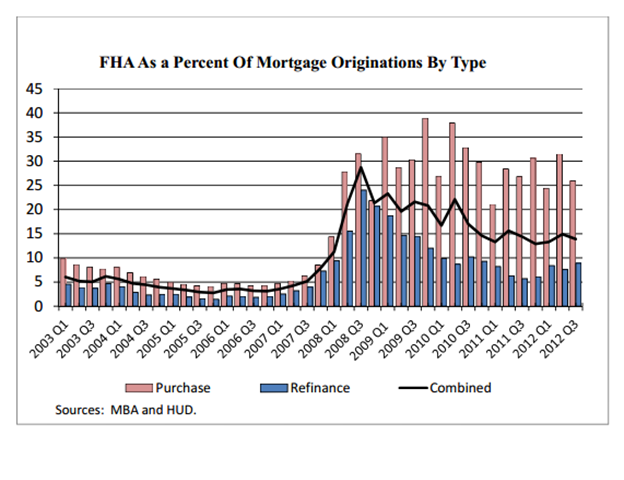

FHA loan volume since recession began

FHA insured loan volume picked up directly as toxic mortgages exited the market:

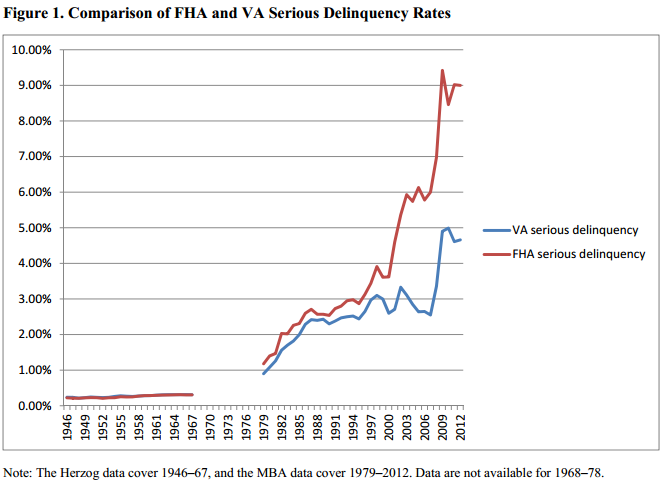

You can see how quickly it picked up in 2008. In some markets like Southern California, FHA insured loans make up about 25 percent of all purchases. In Northern California it is about 15 percent. A large portion of FHA loans are in some sate of serious delinquency:

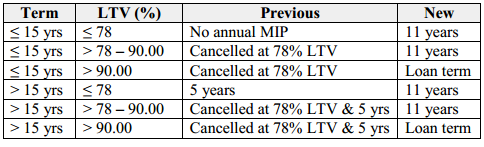

The FHA under GAAP analysis is basically in a -$32.13 billion position on $1.1 trillion in guaranteed loans. Is this an issue? Well it is for these loans since mortgage insurance premiums are going to become even more expensive in the next few months for good reason. One major change is the duration of MIP on loans. This will now be extended for the life of the loan:

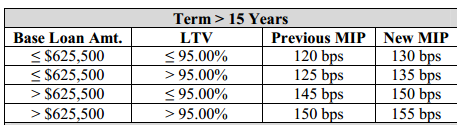

This was typically canceled at earlier times but the FHA needs to shore up its capital position given how many defaults it is facing. If the FHA isn’t in a bad position, then why jack up rates so high? Obviously something else is going on here. The amount paid on a monthly basis is also going up:

Since the vast majority of FHA borrowers go with the lowest down payment amount, we are looking at 130 bps for loans below $625,000. So run the numbers for a $400,000 home purchased with a FHA insured loan:

*Before new FHA changes go into effect later this year

Purchase price:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $400,000

Down payment:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 3.5%

Down payment amount:Â Â Â Â Â Â Â Â Â Â Â Â Â $14,000

Interest rate:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 4.25%

Up Front MIP:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 1.75%

Monthly MIP:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 1.25%

Tax rate:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 1%

Loan amount:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $392,755

Payment 1:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $1,932

MIP:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $409

Total payment 1 and MIP:Â Â Â Â Â Â Â Â Â Â Â $2,341

+Taxes monthly:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $333

Insurance monthly:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $100

Other (HOA/maintenance)Â Â Â Â Â Â Â Â Â $144

Total monthly payment:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $2,919Â

This is no longer a “cheap†loan given what $400,000 buys you in SoCal. Plus, if you look at condos in places like Orange County you are looking at monthly HOA fees of $200 to $700. You can read more about the FHA changes at the HUD website. A few readers have mentioned that there are other ways to extract money from housing and one of them is through all these added costs. Add up taxes, MIP, HOAs, insurance, and other items and you can see that a low interest rate is suddenly masked by higher ancillary costs.

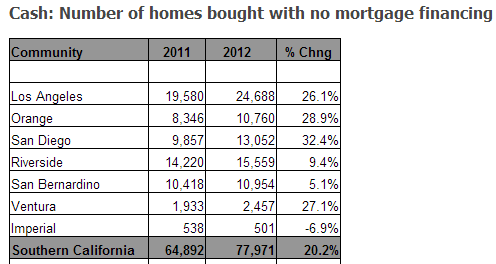

Many current buyers are contending against the jump in all cash buying:

We had a couple of record breaking months of all cash buying in 2013 so the trend continues. FHA loans are becoming more expensive to avoid a bailout on the large number of delinquent loans. In other words, future buyers are going to pay for the mess of the last few years. Yet this is something that is already part of the market. Young buyers saddled with high levels of student debt probably have little alternative for an entry home in high priced areas like California without taking on high leverage loans. Low down payment loans and all cash buyers. Notice how the middle is being squeezed? Not really a surprise given the current state of our economy.

The changes to FHA MIP and duration will start on loans issued on or after June 2013. So if you are eager to buy and are looking for a low down payment loan, you have two months to get on the bandwagon.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

26 Responses to “FHA loan guarantees now amount to $1.1 trillion: Upcoming changes to FHA mortgage insurance premiums and the cost of low down payment loans.”

Regarding purchasing a home before MIP is for the life of the loan, although it begins June 1st, it is nearly over now from a practical standpoint. Meaning, if I were to make an offer on a home and a few days later it is accepted, after the 17 day inspection contingency and then begin the loan process (even if pre-approved) it still will take a couple weeks for the entire loan to be approved, processed, underwritten etc. I would say then that any homes with offers made after about May 10th will eb subject to MIP for the life of the loan. But will this do anything to home prices? I could never imagine purchasing a home with another $300 – $500 per month payment for the life of the loan but perhaps others will purchase anyway.

I went looking at various models this weekend at builders’ offices and was amazed to see them handing out $400,000 houses to 20-somethings with a $500 check to hold it. The salesperson kindly tells them “don’t worry, we have our own lender so there should be no problems.”

Just common sense seems to say this is an unstable situation given the stagnant wages, failure of upward mobility of youngsters these days and the slow economy. So how are these kids going to handle a 30 year, $500k loan? I’d be glad to read comment son this very common situation. It’s close to zero down , no doc.

I know it’s on smaller scale than 2005 due to lack of inventory, etc. but I STILL can’t believe 8 years from the peak and five from the bust that the EXACT same thing is happening AGAIN! Damn we are an ADD nation…

Can’t you re-fi out of the FHA loan at some point?

Not when values drop and you have no equity LOL! Not to mention the intrest rate would likely be higher. Higher PMI will likely exacerbate the next round of defaults!

Yeah it doesn’t make sense that these people who have bought with FHA loans in the past two years haven’t been able to refinance and take advantage of all the appreciation that’s gone on in the past year. Why has the value of their homes increases but apparently the default rate is going up. Huh? Or are they just taking their equity out of the ATM again?

As the trend continues to go up, people will start behaving with more risk. They will use the loan to get the house, with the intention of getting a refi in a year or two, when prices are higher, to get out of the MIP at that time.

This is what happened last time. As the market was rising, people just wanted to get in anyway possible with the idea that rising prices would make all things possible in the future.

Agree with CAE, there are ways around the lifelong MIP, especially refinancing soon, a couple years into the loan. So, the lifelong MIP may not slow the market at all.

Don’t you have to have a certain amount of equity before you can refi, like 80% LTV? Going in with only 3.5% down is going to take quite a few years unless people are banking on housing prices continuing it’s upward climb along with paying down the principal. Or what if rates go up in a few years? And you still need to be qualified in other ways for the refi, they still look into your employment and credit history, right? Just some thoughts.

@Forever_Sidelined

Exactly! Today, most refinancing requires 20% equity. So unless these FHA’ers are coming up with cash to bring down the LTV to below 80%, they will not be able to refinance. Freddie Mac and Fannie Mae will not purchase loans with less than 20% equity.

This is one of the reasons why underwater homeowners have largely been unable to take advantage of sub-4% interest rates.

That’s the point of getting in with 3.5% down and then in a year or two the price has risen to the point where the owner has 20% equity. They then refi into a better loan. So they are betting that the loans will be better in two years and that the price will have risen enough to get to the 20% equity position.

Take that $2,919 per month and multiply it by 360 months (30 year note) and you get just a shade under $1,060,000.

JUST FREAKIN’ WOW!

You will pay 2.6 times for that house.

And don’t forget that when that home hit 20-25 years old, even if it is new and out of the box, when first purchased, major items like water heaters usually need work. Additionally, property taxes never go away, either. And forget HOAs, who needs them anyway. Just another way to skim money.

This is going to end well.

Not!

I guess as long as I live in the OC I will just rent and pay the premium, but not have to worry about maintenance or keeping the pool clean. Sure, my rent reflects that cost, but I don’t have to worry about that going any further than my rent cost. And I can always move after the lease is up, usually in a year. I don’t have to worry about a 360-month note.

OCDan, that $400 per month MIP and the 3.5% down completely distorts things. Just like the good ole days, nobody should be buying a house with less than a 20% down payment. Run this calculation again with a 20% down payment and it all points to buying over renting. Many people who are math challenged only look at gross rent vs buy numbers, you need to look at the net numbers (paying principal and writing off interest and property taxes), this is what really matters. Paying one dollar in mortgage prinicpal or interest is not equal to paying one dollar in rent. Moving every year to sign a new “cheap lease” might be an option for you, I guarantee you that is not an option for most people (especially with kids).

Yes, homes need maintenance, insurance and property taxes (that can only go up 2% max per year). When you get hit with yearly rent increase in the 5 to 10% range for several years in a row, that is enough to get many people off the fence. I agree with you that buying with a 3.5% down payment and getting hit with the high MIP doesn’t make sense, but buying with 20% down does.

Lots if factors at play in rent vs buy, many of which aren’t purely financial and weighted differently by others. Even the financial decisions are case by case.

I have been renting forever (and its been one up) and have been itching to buy as I have 20% down and enough to back up 2+years of payments. Ive been in the market hardcore (i know every house on redfin day it comes out/saw over 30 houses in person/lost bids above list, including one officially this morning) in prime spots in LA since November and everything i recently read on here is what ive been spouting to my friends in terms of what is very obvious if youre in the jungle: artificial supply constraints by banks, cash bids, investor purchasers, bidding wars, only ‘ultra-over priced crap that clearly insiders passed on’ short sales are listed, etc. And this is under the backdrop of recent changes to CA foreclosure laws, the facts that banks can hold homes for essentially 10 years, JPMorgan/Blackstone/Cerebus and new banks and funds by the fay either buying properties themselves or encouraging their high net worth individual clients to purchase them using cash supplied to them via a lower than a mortgage interest loan against their stock holdings as collateral and rent them out. But wait there’s more, we have the lowest interest rates in a lifetime and quantitative easing driving up home prices, home equity so HELOCS will be back soon and consumer sentiment may follow….but not higher incomes or new high paying jobs (with inflation secrety happening as well). And then the devil come back and his name is securitization. Banks and funds like making money at a certain return, not specifically holding houses as investments or just making a positive return. They also like passing off risk so they’ll certainly try and securitize the rental payments in investor owned homes and have pension funds, endowments, govts, etc buy them just as rents go down because they certainly dot just go up, up, up. The smart money will peace out of residential real estate and allocate their resources to higher earning assets like stocks, commodities or the next investment flavor of the month.

It feels like the bubble is happening again because everyone and their brother and mother is now into talking about real estate. Most of my friends in CA, NJ, MA and NYC talk about buying because they don’t want to ‘miss out’ (peoples salaries are not up that much, btw). I have a friend who wasnt flipping, flipping again in Miami. I have other friends talking about buying multi-unit properties and being landlords…none with experience. Sound familiar? In fact, go watch the documentary Inside Job again and you tell me if its not eerily similar to today….

….and all that being said, what if these insiders have won and now control real estate like stocks for the time being, driving up prices for like 5+ years and rents along with it? I feel like the fed may never be able to raise rates (unless he we can fudge employment numbers eventually) because then house prices drop and ARMS reset and its more foreclosures. Is the solution to just keep renting and wait for a crash? It feels like I may be heading that way after my latest overbid and loss (I lost today to a cash bid after I bid $975k on a $935k house), but I’m just wondering if you just overpay now and go with the game even though its rigged because smart money needs house prices to go up for now at least.

Lots of rambling, but lots on my mind. Comments and thoughts appreciated as I’m trying to figure this stuff out myself as an active, overthinking, buyer.

Hey LordB. Definitely agree its smarter to put down the 20% if one does buy, but, unfortunately, the ‘net costs’ many of us calculate when determining the costs of ownership are incorrect due to Alternative minimum tax. Therefore, you often can’t just multiply your effective tax rate by your interest and property tax payments and count those as savings when comparing vs rent. I know I’ve been stuck in its deathgrip, as are many of my friends in the Northeast and Cali.

Also, regardless of political affiliation the mortgage interest deduction certainly may be ‘adjusted’ somehow, on its own or via an overall cap. Lobbyists will fight it, but it would effect the game for sure in terms of deductions (as well as home prices) if it did somehow pass. Regardless, you should account for it in terms of your expected return as assets should ideally be valued on a risk-adjusted return basis.

In terms of Cali property taxes being locked by referendum, that has history on its side for sure….and I admit that I love it personally. That being said, lots of Dems in all branches of Cali govt, demographics shifting, state be broke because so many out of staters live here, etc so I wouldn’t neccessary rely on it like a comfy blanket as a definite fixed rate.

Lastly, in many of your rent vs own comparisons, you don’t mention home appreciation or depreciation. Even if not realized gains or losses at that moment, not everyone can hold forever to get above heir initial deposit and at the very least it changes the equation in terms of comparison vs rent.

I think you mentioned you bought in 2012 earlier so you’ve probably been catching some upside already in terms of equity. Curiously, would you still buy today knowing that each week, new high prices are coming out on Redfin…and then you’re bidding another 5% on top of that…and losing. 😉 I didn’t see my income go up 25% unfortunately in the past 18 months, but it definitely has in prime LA. I make decent money and I know SO many people just don’t work out here in LA and certainly don’t make $200k plus, which is really where you should be to buy in these spots at a minimum. I mean the top paid lawyers at the AMLAW 200 haven’t gotten raises in over 5 years.

Im only playng devils advocate with you btw because you clearly pro buying right now and i almost want you to convince me as im tired of renting. Do you trust the foreign and investor money to stick around now bc America is the new safe haven forever? Are you bullish on big income increases/lots of new high paying jobs coming to LA? Is it the game is rigged on the up/citizens will forever be paying more in housing costs as a percentage of income? Convince me buddy!

First time buyer, I’ll try to answer what I can.

Regarding net costs in the rent vs buy equation, the AMT can definitely throw a wrench in the calculations. This needs to be accounted for along with fluctuations in income.

I highly doubt the mortgage interest deduction will ever go away, but it definitely might get scaled down. I would not stray too far away from a conventional loan amount (417K)…if there is a line in the sand, this might be it.

I am not a big fan of Prop 13 in California and wouldn’t mind if it went away, but that’s wishful thinking on my part. Prop 13 is a huge reason why certain areas have such sticky prices, people won’t sell strictly for the property tax basis. Prop 13 might get ammended for businesses, rental property, inherited property but I see it set in stone for primary residences.

I wouldn’t count on much appreciation for quite some time so I usually don’t factor this into the rent vs. buy equation. Any appreciation is just icing on the cake. Your question of would I buy now? Yes, but with the following guidelines:

1. Only buy in a premium or near premium area.

2. Plan on owning the house for at least 10 years.

3. Keep housing DTI around 25%.

4. Be at or below rental parity.

I don’t see any huge drop in rents (especially for the premium areas). Add this to the influx of foreign money, the local entrenched money and all the people who come here every year to get that slice of the California dream. Bargain prices will likely not be seen ever for certain areas.

Good luck!

@ First time buyer

According to my arithmatic, you must have over $300,000 in cash on hand if you are going to put 20% on a million dollar home and have two years of payments put away.

Do you have any idea what kind of risk you are taking by paying this kind of money for a home in Californai? You could buy the same house for cash in any number of fine locations. Think for over a minute what it means to have a home free in clear in a low tax state that is not bankrupt like California.

Is it true that, because of some recent changes in laws, banks can now be landlords?

If so, and banks become competent at landlording, what’s to stop them from encouraging buyers to take on risky loans? If the buyer defaults, the house goes back to the bank and they can rent it for a profit. It’s win win for the bank.

OCDan – I hear you! The financial debacle that we are still in has really not awakened enough people. You cannot make an ECONOMIC case for owning when using the #’s that Doc provides above or anything similar.

There is SO much addtional money that goes into home ownership than just the monthly nut. I think the $144 allocated for HOA or maintenance is conservative. And just wait til you sell, folks. The sums of money you will forgo to sell it will make your head spin….home prep, commissions, buyer closing costs, warranties, etc.

Here’s how I figure it: when you get up from the closing table you are basically 10% in the hole. (you’ll spend some $$ right away on move in…to fence the yard, finish the basement, repaint interior, whatever… there’s an avg 6% comm to sell, you’ll likely front a few thousand to buyer to cover their closing costs, ETC….you get the idea)

I come across For Sale homes often that were just purchased 4 to 6 years ago. Even in a rising market, they would have to get lucky to break even. Real estate only works economically in a long term ownership scenario. It’s way to expensive to trade!

Seriously OCDan, there is alot to be said for renting — especially if you’re single and your ego doesn’t require lots of swanky bells & whistles so you can receive approval from your friends/family.

I was recently calculating my parents cagr on their home investment. Bought in 1983, down payment $30000, house is now worth $650000 (actually $850,000, but for the purpose of this exercise I’m deducting the additions at cost). So 20x over 30 years, or a 10.5% compounded return, if we just look at the capital appreciation. That’s not bad . . . but we have to remember that a) this was in a RE boom market with declining rates (rates declined from 13%), b) in a great market (NoVA) and c) in a great neighborhood. So this was pretty much the ideal circumstances, and it did about as well as the stock market. Not terrible, but not going to make you fabulously rich. I think people forget the effect of inflation and compounding when they hear stories like “I bought this house for $100,000 twenty years ago.” Well when you look at inflation, that actually isn’t so fantastic. A lot of things were really cheap 20 years ago.

Another good reason to go 15 year fixed, instead of 30. Even if you can’t eventually refinance, you can pay off the house before you need a new roof and most of the appliances are shot.

30 year and prepayment would be a better option for many. That way if income stream is disrupted, the prepayment can be not made while things are tight.

Even though a 15 year gets a slightly better rate, I see the 30 year with prepayment roughly as partial insurance against the unforeseen.

My wife and I recently purchased a home with an FHA loan. My credit is awful due to some bad real estate debts, but my wife is solvent and employed. Anyway, we had trouble getting a 3.75 conventional mortgage so instead got a 3.25 percent FHA loan. The half percent drop in interest rate covered about a third of our monthly mortgage insurance. So my effective interest rate is something like 4.75 for the first five years, which in the bigger scheme of things isn’t so bad.

I ended up having to put up a pretty big down payment to get the house, about 15 percent, because the FHA loan limit in our area is $271,000. If FHA truly wants to protect the program they can start by lowering the loan limits. For me personally, I wanted an FHA loan over a conventional mortgage, even if it cost a bit more, because of the fact that it is assumable. I think interest rates will go up eventually, and being able to offer a 3.25 percent mortgage will be a bonus.

FHA Assumability is overrated. Lenders know that it is but will talk it up especially to first time buyers as if it’s some sort of given that you’ll be able to use it when that day comes to sell. Of course they’ll say anything to get you into an insured product in an uncertain market.

You’re assuming that buyers are going to have the cash to pay you the difference between the contract price and your principal balance.

Can’t you just do a rent to own or similar? The buyers don’t necessarily have to assume the mortgage to get the same rate. The bank doesn’t have to know who is *really* making the payments.

The spring realtor hype is going full blast in Denver too.

http://www.denverpost.com/business/ci_22903895?source=bb

Leave a Reply