Foreclosure Shrugged: The Issue with Finding an Exact Foreclosure Number.

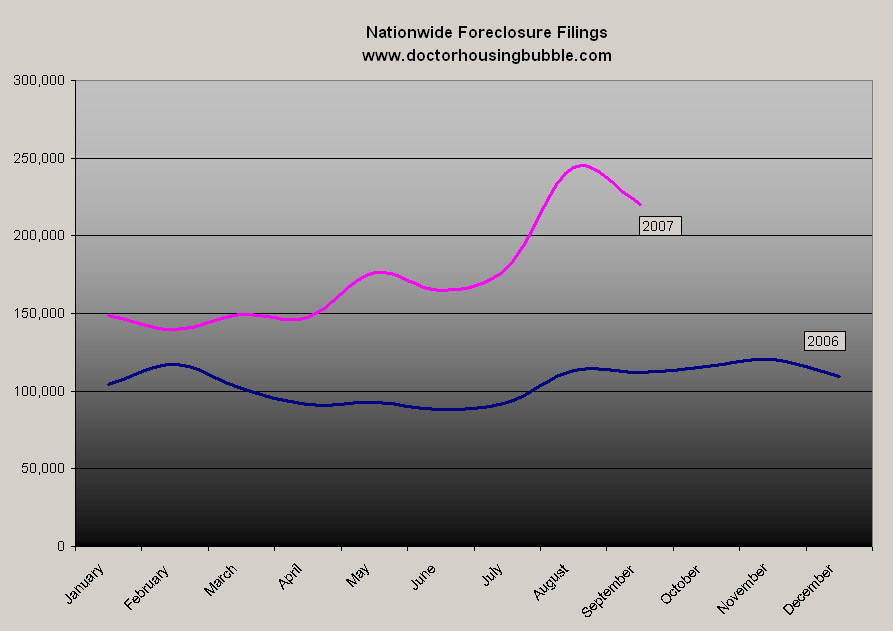

As you’ll see on the chart, the average monthly foreclosure filings in 2006 was 104,927. The average monthly foreclosure filing for 2007 is currently running at 174,376. What is more alarming is we saw 243,947 filings in August and 219,850 filings in September. These numbers have come under recent scrutiny by the Orange County Register with good reason. So how do they figure these numbers after all? RealtyTrac gets their information from various sources including auctions, real estate owned, and defaults to name a few. At times, there can be multiple filings on one single place. As you can imagine, the stages of foreclosure don’t necessitate exclusion from one another and sometimes commingle. Recently, RealtyTrac is now tracking unique property addresses in relation to foreclosure filings that should improve the quality of data reported.

With all the rhetoric about subprime you would think that the majority of the problems are occurring in smaller states being hit hard by manufacturing layoffs and less diverse economies. This is not the case. In fact, five states make up nearly 50 percent of foreclosures for the third quarter of 2007:

Of course,

Foreclosures Sitting on the Market

In a healthy housing market, there isn’t an abundance of foreclosures because demand and supply usually even out the market. A foreclosure hits the market, inventory is at sustainable levels, a buyer comes along, and the house is sold. The problem right now isn’t so much that foreclosures are hitting the market, they hit the market every year and this isn’t something unique to 2007, but the ability of the overall economy to recycle foreclosures into the housing supply stream is now stifled. When prices are up, even if you bought with no money down, a slight six percent rise may allow a seller in trouble to get out quickly with no problems. With a seven-year boom, this was the case for this entire decade. Now that prices are decreasing, a large amount of people buying with no money down or very little, there is no equity cushion and buyers are faced with short selling or foreclosure. The foreclosure issue splits into a few areas here. In high priced markets like

2 Million Foreclosures by 2009? Says Who?

The art of predicting foreclosures is just that, an art. The Joint Economic Committee released a report in late October highlighting that “2 million subprime borrowers will lose their home to foreclosure through 2009.†The report suggests that a 20 percent drop in housing prices is all that is necessary for this to occur. According to the Case-Shiller numbers released this week, housing is already declining and in some areas is already in double digits. The Case-Shiller numbers are regarded as better barometers of market sentiment since they track the sales of a single home where the median price typically used only reports comparable sales in a general area. Going back to the subprime report, again the premise is that the housing mess is caused by these rogue subprime homeowners. What they fail to account for is many “prime†borrowers are on the edge as well and will fall into foreclosure once the economy goes into recession. Also, their report goes only until 2009 while we show another massive wave of mortgage resets hitting in 2010 and 2011, that of option ARMs. This week, Citi announced potential massive job layoffs of 45,000 due to the credit issues hitting the market. These are very high paying jobs that once gone, will never return. The same goes for brokers and agents who are now leaving the industry. This is an issue that is rarely discussed. So much of our economy is dependent on real estate, in some estimates approximately 30 percent of all employment created since 2000 has some sort of linkage to real estate. So the numbers look good so long as housing is good.

Either way, foreclosure numbers are growing and no one really has a sense of how deep this will go. What is clear is that we won’t have a better assessment of the market until the toxic waste is flushed out of the system but that won’t occur until 2009. The fact that the stock market rallied simply because the Fed “hinted†at a rate cut shows how desperate this market is to jump on any news that will keep the credit flowing. It also shows our addictive codependency on easy money.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

13 Responses to “Foreclosure Shrugged: The Issue with Finding an Exact Foreclosure Number.”

As always an excellent article. Question–Has anyone compiled the figure of all the forclosures plus the homes and condos that were counted as sales and failed? This number logically should be added to the unsold inventory. Is It?

“In high priced markets like California, there may be no option except foreclosure. With prices so incredibly high and tighter credit markets, the demand has definitely dropped thus increasing inventory. In Los Angeles County sales have dropped by nearly 50 percent from a year ago. Short sales may be unrealistic since a 15 percent drop here is equivalent to $75,000 to $100,000.”

What a great way to synopsize the current market in California! The drops here have been, so far, insignificant for those who have not been able to afford CA properties in the past. Real estate prices will have to fall much lower to get rid of the ever burgeoning supply.

“Overcoming Real Estate Losses” at http://WhineCountryRealEstate.blogspot.com

You discuss 2005 and 2006 vs 2007 foreclosure numbers. How close are the 2005 and 2006 foreclosure numbers to the historical average? The reason for my question is that during those years it was still fairly easy to get out from under your home by selling quickly before the foreclosure process started. For example, I was able to sell in July of 2006 with just one month on the market. Had foreclosure been on the horizon, I would have easily dodged the bullet. Because of this, the numbers of foreclosures were probably lower in 2005 and 2006 than the historical average. When prices started to soften the ability to escape foreclosure disappeared quickly and thus you would expect to see a sharp rise in foreclosure numbers. I am just interested in seeing more of the big picture taking into account “normal” RE times, if it is available. I guess my ultimate question is how much above historical foreclosure rates are we right now in 2007.

Doc,

I have a perfectly good credit but want to experiment and make money at the same time. What problem do you foresee if I take a 125 loan right now and walk away? Is there a catch?

Carol is absolutely spot-on. A $75K drop on a $1.2M 900 sq ft home in Santa Monica is not going to suddenly bring a throng of buyers to the door.

Drop the home price to $750K (which is still absurd) and maybe there will be some activity.

Unfortunately sellers are in denial right now. It’s hard to face the music, we are all susceptible to the temptation to put our heads in the sand. But the storm is coming — no, it’s here already — and those with the b***s to at least sell now (probably at a loss) and get out before it worsens are the only ones who will avoid tremendous misery.

The story about builder Lennar a few days ago on Patrick.net (http://patrick.net/wp/?p=537) shows just how Pollyana-ish the sellers with skin in the game are. FInd the paragraph starting with “Lennar CEO Stuart Miller” and read it. Is Miller delusional, angry & frustrated, full of crap, terrified, or all of the above?

They’re terrified because they are literally powerless to control it. Like a tsunami headed for a small island, the housing crash is coming and it can’t be stopped. But the (potential) victims can face reality and do their best to get out in front of it, or hunker down and *hope* the wave doesn’t crush them. Hope doesn’t stop a million-ton wall of water, and it doesn’t stop a market correction.

I live in Reno,Nevada. And like what you said…

“Arizona and Nevada are also facing rising foreclosures. Arizona and Nevada offer an interesting market since many California Equity Giants (CEGs) bought 2nd homes in these areas to flip or to rent out. With abundant land and less regulation than California, builders provided the perfect Mecca for aspiring investors. These markets are the first to retrench when times become tough because CEGs revert to focusing on their primary home before focusing on their secondary investments. Not everyone did this but this was fuel that added to the speculative flame.”

California buyers who got large sums of money from their California homes did invest in Reno(heavily). I was looking at some numbers from the University of Reno’s demographics, and majority of which came from San Francisco and L.A.

Well, by and large I really don’t think it was bad for Reno to have our neighbors live here. But the problem was the we locals gambled along with them- the high rollers of Cali. We just can’t keep up. That’s why this happened to us… :

http://renomarketblog.typepad.com//reno/2007/08/reno-sparks-m-2.html

and as a result both parties are losing tens of thousands of dollars. Hard lessons learned.

(Reposting, I don’t think the first time took)

Hello, Doctor. I admit I’ve become a bit addicted to your site. Great analysis. Thanks. I make real estate software for a few Socal brokers, so it’s really interesting to see where things are heading and why.

I was wondering if you might provide some insight to the Hawaii real estate market, especially, Honolulu county (Oahu island). It has similar economic fundamentals to Socal (60K median family income, 650K avg SFH price), with a similar run up in prices, but prices are unbelievably continuing to rise. It’s truly a mystery. All the articles I read are still so bullish. High energy prices are going to dampen the economy (all goods imported + major industry tourism) and prices will fall then, but I just can’t figure out why folks are still so upbeat and why people continue to pay the prices.

DRHousingBubble… Loans

I have a friend at Washington Mutual (LA County area) who tells the bank has issued an edict that they will not issue loans for more than $417k (obviously conforming limits).. Have you heard about this and if so have you hear that other banks are taking the same stance?

Certainly there are obvious outcomes if this is true.

Real Situation: My wife and I decided to sit out the market until late next year (when prices hopefully will be more reasonable). We were driving to relative’s house and saw 3+2.75 fixer house with “pre-foreclosure, short sale” sign. Decided to check it out. Listed on Zillow at 805K, but price had been reduced several times (760 to 719 to 700). It had been in escrow at 700K, but fell through due to buyer problems (no can get financing?). Anyway, have made offer for 525K (417K conforming + 20% down, all we can afford). Next day, agent says there is 550K verbal offer, will be followed up with written offer, Never happens. Our offer is the ONLY one. Seller has agreed (what choice do they have?), now up to their lender. Lender “Appraised” value is 650K. If they say no, fine, keep it and try and sell it or go to auction. We can wait. Price history: 1991 @ 320K, 2000 @ 385K. Methinks large equity extraction that lead to this.

Hello John:

It is since they get their data via lenders filing defaults. A mortgage isn’t going to discriminate between a home and a condo.

But if you want to see the extent of the housing shenangians take a look at this article:

“Floyd is in no position to drain the pool or improve his property. He’s in eastern Kentucky serving a 78-month federal prison term for conspiracy to sell hundreds of pounds of marijuana. He was indicted two days before he borrowed $825,000 for the 4,300-square-foot home in the Woodlands subdivision. Through contact with the prison’s administration, Floyd declined to be interviewed for this story”

http://www.detnews.com/apps/pbcs.dll/article?AID=/20071128/BIZ01/711280404

Selling weed and flipping houses. And you thought you had an exciting career?

Nice article – and, I like the fact that you said ‘…no one really has a sense of how deep this will go…’.

Every time you pick up a newspaper or read a web article, the same ‘expert’ who once said ‘…there is no housing bubble…’, then said ‘…the worst is over and the bottom is in site…’ is now saying ‘…it will never happen in the high-priced coastal areas like Newport Beach and La Jolla…’, will eventually be saying in June of 2008 ‘…I have always said that real estate is cyclical and I am not surprised that this has happened – it always does – but, 2009 will be a HUGE buying opportunity…’!!!

As the old saying goes – ‘History always repeats itself’ and, it is those 2004/2005/2006 real estate ‘virgins’ (much like the stock ‘day traders’ of the late 1990’s) who drink the Kool-Aide, thought prices ALWAYS went up, and then blame everyone else for their bad decisions…and ask for the government (taxpayers like you and I), to bail them out!!!

Hey Doctor,

Thanks for the great site. I’ve been renting and waiting for a correction for the past 4 years. As far back as 2003, I was working at a bank in Chicago where everybody knew flippers were driving up real estate prices and creating a bubble. It was obvious to EVERYBODY even back then. So I’m more than a little shocked that Greenspan has so far pretty much gotten away with pretending they didn’t know they were helping to create a bubble. I thought it was obvious at the time that prices would eventually come down. We’ve been saving our money, driving a used car, not eatting out often, and have managed to save up a significant about as our salaries increased. Still, I see only shacks on the market in our desired price range, and I’m now hearing that Paulson, Bernake and Bush have come up with a master plan that basically rewards all the idiots (and well, maybe they’re not idiots anymore), by magically somehow declaring that all ARM’s will not reset for maybe another 7 years. Apparently, people who are conservative with their money will not be rewarded, and one way or another, we will have to give it up.

Is it time to throw in the towel and buy a $500M shack?

hi doc, really nice article. i have a similar question as mr. john b’. i also do think that the figures of all the foreclosures including the homes and condos that were counted as sales and failed should be logically added to the unsold inventory. would you agree?

-brian

Leave a Reply