The house broken American: Many Americans believe they will work until they die and the only asset many have is their home.

Americans for the most part are bad at saving money. In fact, the entire credit boom and bust was largely fueled by people and banks living way beyond their means. Even after the recent boom in the stock market and housing market, many Americans are not in a better financial position. The problem with housing is that this is like having golden handcuffs.  You will likely only unlock the wealth when you sell it. As we have discussed many are simply reluctant to sell. So in essence, the wealth is locked away. To sell a home also costs money and real estate for the most part is illiquid. And since the recession ended a large portion of home purchases have gone to investors. Never in the history of the US have we seen so many large institutions dive into the housing market in aspiration of being a landlord. Recent surveys show that many Americans plan on working until they end up in their grave. But what about the boom in housing? Unfortunately many are locked in a granite countertop laden sarcophagus.

Source of income – most will rely on Social Security

Most Americans will rely on one shaky stream of income in their retirement, Social Security:

Source:Â NPR

Social Security was never designed to be the cornerstone of a long-term retirement plan for Americans. It was supposed to be one part of a “three legged stool†of retirement that included savings, pensions/work based retirement income, and finally Social Security. Well look at the chart above. The vast majority of Americans are not approaching this anywhere close to the three legged stool approach. This is a one leg chair and Social Security is the foundation. When Americans were living in homes and having mortgage burning parties this made sense but now we have people rarely paying off their homes. Where is the income going to come from in retirement? And with the homeownership rate plunging, many will be paying rent in their older years as well. And don’t think that by simply owning your home that you get away with no costs. You still pay insurance, taxes, and maintenance costs. Americans have much less saved up than you think.

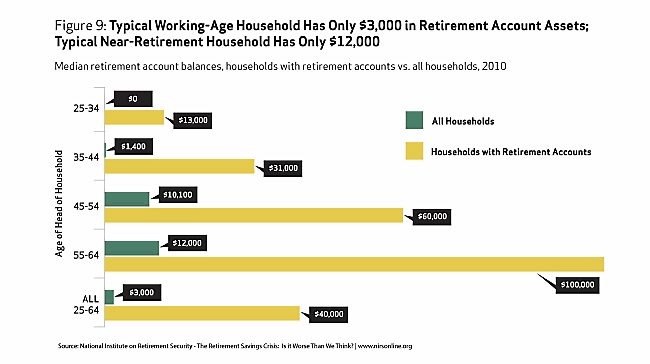

The typical amount saved for retirement less than you think

The money saved for retirement by Americans is ridiculously low:

The typical working household has $3,000 saved for retirement while the household nearing retirement has about $12,000. This isn’t exactly a good situation. And reverse mortgages are not the answer because this is simply another transfer of an asset to a banking institution (and usually the terms are not good in your favor). And if you think this boom in housing and the stock market is helping Americans think again:

“(Forbes) Forget pushing retirement off a few years. A growing number of Americans believe they’ll be working until death.

An alarming 37% of middle class Americans believe they’ll work until they’re too sick or until they die.

Another 34% believes retirement will come at the ripe age of 80. Just two years ago only 25% of respondents felt the same way.â€

And this is for middle class Americans. This isn’t looking at lower income Americans that presumably already know that they won’t retire and will largely be dependent on Social Security if they are lucky enough to make the cut. 37 percent of middle class Americans believe they will work until they kick the bucket. Let us not even discuss the situation of younger Americans looking to buy real estate and have mountains of student debt to contend with.

This is why a massive increase in real estate values driven by speculation and artificially low rates rarely does much for the underlying households in the economy. Say you have a $200,000 home and now the home is worth $250,000. Okay. Are you going to downsize? Unlikely. You want a bigger home in a better neighborhood. Well guess what? Homes in that area went up as well. In this market, a good agent is going to end up costing 5 to 6 percent (split among two or one agent). After that is done, you probably have enough for a down payment but you just reset and now have a new mortgage bill that is likely at 30-years again. This is common for most Americans. The typical holding period of a US household is 7 years before they move from their current home. Mortgage burning parties are as rare as flapper clothing in a hip-hop club.

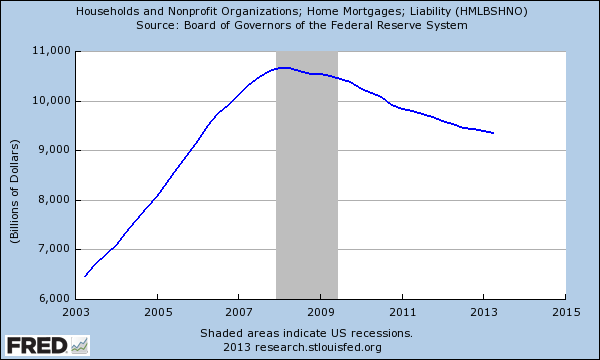

Homeowner’s equity up but mortgage debt down – a boon to banks

What is shocking is that the balance sheet changes are largely being driven by foreclosures and investors eating up a big portion of properties since the housing market crashed in 2007. Take a look at mortgage debt and then equity in homes:

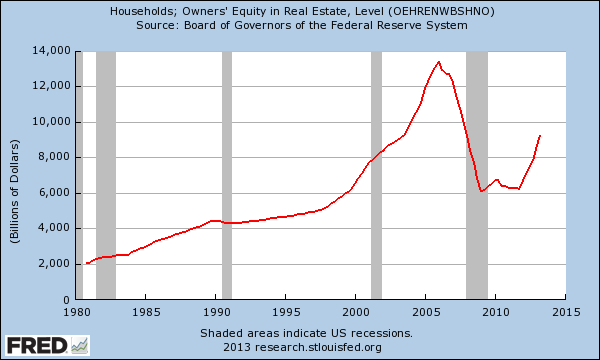

Mortgage debt has largely fallen because of foreclosures but also, a large portion of recent sales (i.e., 50 percent in Las Vegas, parts of Arizona, 30 to 40 percent in California, etc) have gone to investors. If you are buying with alternative financing either cash or other non-traditional ways mortgage debt is going to fall dramatically. Yet is this really a big benefit for local households that now contend with inflated real estate values and no real tangible gains in household income? Take a look at equity in homes:

This big gain is going to banks and large investors. Even the household that has seen their real estate go up will only benefit if they downsize and that may mean leaving a high cost state (and looking at available data most are going to keep those golden handcuffs on and eat cat food before they sell and “down grade†their standard of living based on zip code). Naïve folks think that “well if the Fed is making rates low, then don’t all people have the same advantage?â€Â Of course not. We are talking about billion dollar hedge funds here that trade in bonds and derivatives. The 30-year mortgage is largely for the average Jane and Joe that can’t contend in this market. We’re talking about negative rates on Treasuries that have forced these banks to ignore rates lower than inflation and go after rental property. Why else would Wall Street be interested in rental real estate? For decades being a “landlord†was seen as beneath them. Yet this is what happens when the Fed is quickly expanding their balance sheet to $4 trillion. This formula is working for a very small portion of our nation.

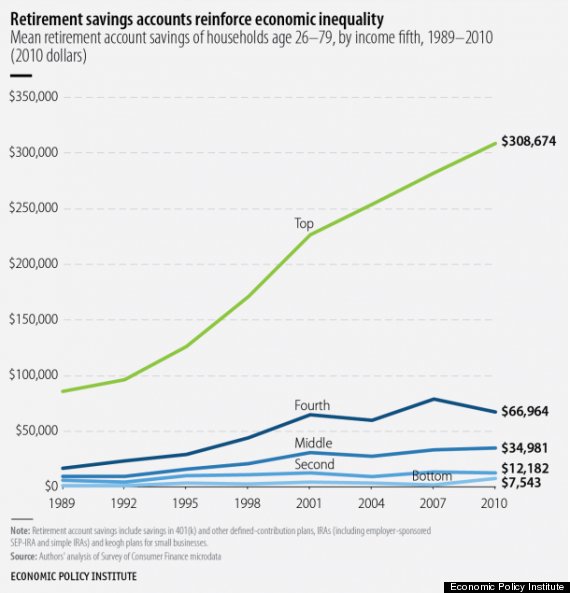

The big divide in wealth

As many of you know income inequality is rising dramatically in the US:

This is simply a fact. It is also a big reason as to why the US is becoming a larger renting nation. In many prime locations hot money is accessible to not only US investors but the world. It is hilarious to hear some “loyalist†talk about how much they love their area as if they will only sell to “Americans†but will sell their property to whoever comes in with the biggest bucks. This is part of a global market. If you think the Fed is looking out for the regular US household you have something coming to you. The facts show a very different reality. Those surveys we mentioned where most are going to rely on Social Security and how many are going to work into their graves were conducted recently. That is, these were done in year 4 of the recovery. Many of the jobs that have come after the recession ended in the summer of 2009 have been lower paying jobs. Certainly not enough to support a mortgage in prime locations.

Many Americans are house broke. Some are so broke that they have lost their homes to foreclosure (over 5,000,000 and many are still losing homes) but many of these homes are going into the hands of banks. The little inventory out there is trading hands in a very tightly controlled range. Supply is restricted and thanks to accounting rules being bent to the will of the banks, the win is very clear for this group. But looking at other metrics of “wealth†most Americans continue to lose out even with this boom in housing and major rally in stocks. Frankly, most don’t even have enough to purchase a seat at the current inflated table. That flood of homes is unlikely to come because those golden hand cuffs are too enticing to take off.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

88 Responses to “The house broken American: Many Americans believe they will work until they die and the only asset many have is their home.”

Here in Pennsylvania, many sellers are finding that their home will need tens of thousands in repairs. The stucco exterior walls on most homes built in the past ten years were applied cheaply and by unqualified workers.

The inspector who I hired told me that ninty percent of the stucco homes he sees need to have the stucco torn down and replaced with siding.

Fortunately we only had a minor problem in that area, costing twelve thousand to repair. But we were victimized by a “reputable” septic system company who failed our septic system and wanted thirty thousand to put in a new system.

The seller has to run a gauntlet of inspections. We’ve spent forty-five thousand so far to get the house back on the market and listed at six hundred thousand. And this is after having spent one hundred eighty thousand in maintenance and upgrades in the past fifteen years, so it wasn’t as though the house had not been kept up.

So from my experience in my location, one reason the inventory is so low is because the poor construction methods require expensive repairs. A seven hundred thousand dollar home five years old near me had to have all the windows replaced, over forty windows.

Excellent summation of one of the emblematic, overarching diseases–i.e. shoddy construction by shoddy contractors–that made up the larger Housing Bubble Sickness.

It’s really unprecedented, and I wonder if DrHB & Commenters have any ideas on how to QUANTIFY it, both macro (region/nation-wide) and micro (individual developments/units)? It’s a real deal changer, and I hope these hedge funds are getting bitten hard by it. By the same token, they probably have the best data on it.

PS: Here in So-Fla, stucco has long-standing use, over concrete “cinder” block (CMU)… even so, the art and skill are in decline.

I had no idea it was catching on (unwisely) in PA… I can imagine it is problematic in freeze-thaw cycling, esp. over wood frame. Go with systems proven in your local climate.

Great post… the small investor should take note. If you cant beat um,…join um!

Nothing stopping you from getting in the game. Plenty of affordable homes to choose from here in the Inland Empire. Now is the Time to purchase a second and third home and rent them out jest like the big boys. An investor (or family) in their 30’s should own at least three rental properties. Rents will cover the payments at the current fixed rates. In 30 years ( retirement age) the homes will be paid off. One can live comfortably on three times local rental rate.

People have to live somewhere, and SoCal is near top desirability worldwide. Interest rates are still near historic lows and likely wont get much better… Home prices in the IE are still below replacement in most areas…

Thirty years from now, the properties will be free and clear.

Example. When I was 20, and still enrolled in college, I bought a new condo For 80k. 5% down and bond financing 9.9%! (start rate was 6.9% gpm). Today I’m 51 and the unit is nearly paid off (refinanced a few years later). I lived there thru college and have had it rented out since. It has had a positive cash flow for the last twenty years. Now it rents for $1,750. It could be sold today for 250k, or I could just keep the cash fow for retirement. Could have sold it for $300k at the peak market, but didn’t…

Point is, you don’t have to be a huge hedge fund to take advantage of these low rates and opportunities. If more people will be renters in the future, it seems to me that It makes sense to be a landlord!

If you have to lever up to be a landlord, there is nothing in your future except a Chapter 7 filing. Keep dreaming, amature.

And homes in the IE are minimum 10% over priced right now, with prices currently stagnant to slightly falling. No major income sources exist in the IE and desirable pockets (like north of the 210) rely on LA commuters to exist.

please don’t feed the trolls 🙂 Much like 2007-8 on housing panic and other sites, all these shills will disappear when the SHTF

I believe your wrong PapaNow

less than 5 percent of IE residents commute to LA.

And… The IE is WAY more affordable than the Santa Monica example. For $1mil you get over 5,000 sf on a half acre a few miles from Victoria Gardens… And 45 min from LA, beaches, mountains, Palm Springs, skiing, lakes.

“Ametuter” ? Well, you are entitled to your opinion. I was born and raised in the IE, and actually like it here. Also own homes in Newport Beach and Hawaii. Not trying o brag, but I really do love the IE.

The troll got me, I’ll admit. 🙁

But there is clarification due on their response.

Over 40% of the IE commutes. If it was 5% the 91 would not be a parking lot.

http://www.redlandsdailyfacts.com/general-news/20110313/inland-empire-residents-commute-outside-the-region

@PapaNow – You the amateur because you really didn’t pay attention to his post. Notice that his investment was long term not short. It’s a very simple formula really. If you look at the models for income property over the last 30-40 years, it was a rare occasion when you could buy something and the rent would cover the payment. Right now, interest rates are so ridiculously low, that rent will cover payments, property taxes and even leave enough left over to bank for emergency repairs. The trick is to buy in the right neighborhood. Great schools in California are a very rare commodity, but if you buy in the right district, you will get the best rent to cover your investment. If you pay 20% down and keep it for 30 years, somebody else will buy the other 80% for you. YOU ARE TOO FIXED ON CURRENT PRICES. You are not paying current prices if you buy right now. You are only paying 20% of current value while someone else buys the rest of it for you. There is NO STOCK or other investment that can give you that kind of return. Investing for the long term is great right now. That’s why investors are doing it. However, if you are a flipper and plan to sell in 5 years, then you will likely be disappointed because interest rates will rise and prices will correct. The long term investor doesn’t care if the prices correct in the next 5 years because he’s only paying for 20% of the property anyway. Unless the demand diminishes rapidly and rent collapses, rent will likely hover at current levels for awhile and eventually over time it will rise.

If i remember correctly, didn’t you buy a home out in Fontana recently? Now your bagging on housing?

“When I was 20, and still enrolled in college, I bought a new condo For 80k.”

No, you didn’t buy the condo. Your parents or your grandparents bought it. You were just in the room in between frat parties to sign some papers.

Please read my post again… I bought the condo with 5 percent down. $3500 plus non recur purring closing costs. Builder paid the rest. No financial help from relatives.

…LO56 is correct PNow…think long term. Young people should take advantage of the low 30 year rates.

Oh, yeah, sorry. The American taxpayer helped you buy that condo, by backing that low interest, low down payment loan to a 20 year old with what had to be a very slim credit history. You were only two years into legal manhood, after all, right?

You sure maybe mum and dad didn’t at least co-sign for you? I mean, I know that anybody breathing could get a loan from 2000-06, but, we’re talking around 1983, right? Different times.

Actually interest rates were hardly low in 1983 – around 13% for a 30 year fixed IIRC. This is what made it a good investment. High interest rates suppressed prices so the well capitalized investor who could stomach high payments for a few years could re-fi when rates went down and cash in.

This BTW is exactly why I think real estate is a much more dubious investment in today’s low rate environment. There may still be forces driving prices higher, but the potential for a windfall after a big rate drop is now gone.

The devil is in the details. Being a landlord can be very challenging.

“Rents will cover the payments at the current fixed rates.”

Right now they will. The future of rents is unknown. Rents can move in two directions.

“In 30 years ( retirement age) the homes will be paid off.”

Assuming no equity cash-outs or refinanced re-amortizations take place. If one is to truly take on landlording as a business, leveraging existing assets for future potential profits would be tempting.

“One can live comfortably on three times local rental rate.”

Agreed, although this assumes cash-flow is not being impacted by leverage repayments, delinquencies, vacancies, and expenses.

“People have to live somewhere”

As well they have to live somewhere when RE values move downward.

“SoCal is near top desirability worldwide.”

Right now it is. We don’t know what will happen in the future. Fortunes can turn on a dime.

“Interest rates are still near historic lows and likely wont get much better”

If rates were to move up enough, we would have an incentive to sell RE holdings and move that capital to higher interest earning investment vehicles. If that happened, supply would increase and the price level of RE assets could fall.

“Today I’m 51”

The realities of the world that got you to this point are different than it is for young adults today.

“If more people will be renters in the future, it seems to me that It makes sense to be a landlord!”

Demand is but only one input out of many that factor into a profitability equation.

Apparently, IE Landlord did not read the first post by the person from Pa. Recently built houses are money pits and good luck with owning a house built today in the IE in 30 years time.

I am with you. I am 62. . Like you I started with my first investment condo at around 35 years of age. Now, I own 4 rentals yielding a total of $7,600 per month, and I love the depreciating part against my pension income. Can’t wait to start receiving SS!

As you well said if you can fight them, join them.

Gd luck.

@Dr. Housing Bubble, the “golden handcuffs” analogy is a good one. I know of numerous elderly couples in the Culver City/Westchester/El Segundo/Mar Vista/Palms/Cheviot Hills areas that were looking to sell around the year 2007 as soon as prices for their SFR hit $1.2MM. That never happened. They are still waiting for SFR’s to shoot up to $1.2MM before they will even consider selling and relocating. With GDP, employment and the housing markets all softening as we speak, it appears these people will be waiting a long long time unless hyperinflation shows up.

And this, in a nutshell, is why many of us who were prepared to buy during the 2009-2012 downturn did not. The vast majority of ‘desirable’ properties stayed off the market since those wealthy enough to own those desirable properties were also wealthy enough to delay selling until the market recovered.

Even now as higher prices are starting to pull more of these pent up sellers off the fence I’m finding that inventory is still very constrained. In the area I monitor in eastern Ventura county I’m now seeing two types of move up homes: 2007 time machines (priced near the 07 peak and never selling), and a much smaller number of realistically priced homes (up maybe 15% from the 2011-12 low) that sell quickly. In practical terms the former homes do not affect the available inventory as nobody will buy them while the number of the latter is not much more than were around in the inventory drought a couple of years ago.

Perhaps overall prices will continue to increase enough (and sellers eventually grow desperate enough to move) that the inventory of homes with realistic selling prices will grow significantly – but at least in my neck of the woods it hasn’t happened yet.

The big question mark is interest rates. Before the recent shutdown/debt ceiling idiocy forced the Fed’s hand I would have said that rates were inevitably rising and prices were about to stagnate (leaving the low effective inventory unchanged). With the increasing likelihood of QEternity I could see a return to the very low rates of last year, another leg up in prices and more pent up sellers finally trying to cash out. We’ll know more early next year after the next pissing contest in DC and the transition in Fed leadership.

I wonder how many of these people can realistically “work untill they die” ? That is given the poor job market, age discrimination, and the deleterious effects of aging.

I wonder the same thing. Now Medicare and Social Security are about to be cut how will people manage? I am a healthy 78 year old and feel the affects of aging already. I don’t think I would be up to working a 40 hours week now especially some boring job. If you work is something interesting and stimulating no problem but people who really need to work the rest their lives are generally not working high end jobs in interesting fields. They push paper or dig ditches. Our national standard of living is way down and I can only assume it will sink further compared to other rich countries. Our life expectancy will drop too – perhaps that is the real plan. We may be the richest country in the world but only for the few. We have no representatives in Washington because all of Congress – except a few – works for the rich or they won’t get reelected. In just over 30 years I have seen America just sink and sink. Now that the corporations own us we don’t have a chance. As the governor of Ohio said this AM – it’s as if there is a war on the poor – and the middle class. For a Republican that is enlightenment.

Life expectancy IS dropping. Recent research shows that life expectancy for white women has been falling for the last few years in America.

NAR: Pending home sales *down* 5.6% in September and fall 1.2% below year-earlier level. This is the first year-over-year drop in 29 months.

Now, all of us that follow charts could have seen this coming. Mortgage Purchase applications falling slope chart doesn’t look good

http://loganmohtashami.com/2013/10/24/mortgage-purchase-applications-falling-slope/

The decline in pending sales could very well be the first sign of Wall Street investors pulling out of the residential home market. Pending September sales would be been for transactions that begin in July or August (and theoretically June although those would be outliers) under the (marginally) higher interest rates of 4.5%.

I was a visiting a friend the other day whose brother was in from Dallas. The brother was crowing about having paid off the mortgage. He said his coworkers were absolutely astounded that he wasn’t planning to cash out and buy something bigger or in a better part of town or on a golf course or something. (He’s quite a good golfer, apparently.) He said he told them he was going to enjoy not having the monthly payment, and they looked at him like he was speaking Swahili. The modern American mindset never ceases to amaze me.

I could pay off my mortgage tomorrow, but don’t since I can get a better return on the money elsewhere. Even so, I am significantly more conservative than some of my colleagues and have about 40% of my assets in bonds while they are much more heavily weighted in stocks. Though this allocation makes sense for me as I am nearing retirement, my friends look at me like I’m some sort of village idiot (and, given the returns on equities vs. bonds over the past few years, perhaps they’re right).

My point is that we all need to carefully determine the appropriate asset allocation to balance risk and return. Just stuffing money in the mattress (or equivalently in the mortgage) may work for some and may help one sleep better, but isn’t necessarily the best approach for all.

Those are valid investment options. Although, very few people are using the level of financial calculus you have described when it comes to deciding the opportunity cost of paying off the mortgage. Most of them just have housing fever. Also, I doubt many of them have the monetary wherewithal to pay their mortgage and invest in any significant way even if they wanted to–as Dr. HBB points out with the statistics above. For most working class Americans, being able to age in place without a significant monthly housing payment is about the best they can hope for. Then they can pray Social Security and Medicare cover the rest.

I’m sorry but it’s rude to generalize and say Americans are “bad at saving money” and “living beyond their means” in such a condescending manner. We are a family of four living in so cal on 70K. I stay home with my kids and that’s my choice. I NEVER buy anything for myself, like clothes, cars, vacations. All of our money goes to living expenses like mortgage, gas, food, insurance. Unless purchasing fresh fruit for my children is “beyond my means.” No I don’t have any savings but it’s not due to frivolous spending. It’s expensive to live in the US and in CA and to act as though us regular folks just have spending problems is ridiculous. The 1% have spending problems. Anyone who spends a thousand dollars on a purse, a million on a yacht, 500 to eat out, THEY have a spending and a stealing problem, not me. I have a 7yo purse, I have crappy shoes and an old car. And NO savings.

You’re not alone and you’re not bad by any means. A lot of us are in this same boat.

I think the general point here is that–no matter what your inclination is to save–the government provides the tools to ensure the majority of Americans (who don’t save) are enabled to “leverage up” and spend beyond their means, either through FHA, Fannie/Freddie, expanded conforming loan limits, etc…

Where I live in Florida, a lot of folks don’t spend more than 3x income on their house. As we all know in California, it’s more like 5x or 6x. How did California get there? California once was closer to national averages, but politicians got involved in order to “help” the middle class by creating all of these exotic rules and regulations in order to make expensive housing “more affordable.”

Whenever the government gets involved in anything, there are winners and losers. In this case, that generation (Boomer) was the winner. The losers are the succeeding generations, who now need to fight such rich valuations, which are taken as being “normal.”

What would have been better is if the market had to clear itself decades ago. Expensive housing circa 1978? Those who can afford to buy do, and those who can’t rent. Fewer qualified buyers (sans government assistance) means that the housing supply would have had to price itself lower.

IMO, if you’re making $70k/year, have no savings, and need to think about retirement one day, it might make sense to move. $70k here in Florida affords you a wonderful lifestyle with margin enough to save. Again, saving is a decision–you can’t say that you can’t afford to save when there are other markets available that offer a more affordable lifestyle.

You can’t move if there are no jobs. Likely the amount of 70k per year jobs in Florida is MUCH lower than in California.

You are exactly like the people that have an expensive purse. If you can’t save you are spending to much on other items. Which means you are living in an area beyond your means. Purse = Expensive rent. You just have a taste to live in a high end area where your income does not justify it. I would love to live in Beverly Hills but I can’t afford to live there and still have savings….see how this works?

Housing isn’t an entitlement it is earned. And clearly you have champaign housing taste or area and a beer budget.

#1 Rule to live by: Pay Yourself First.

You’ll barely notice the money is “gone”.

Hello Doc

My 82 year old mother is an example of real estate rich and cash poor. She owns (free and clear) and lives in a 90 year old house with a tear down value of around $2M. She had been watching all these reverse mortgage ads on TV and thought it would be a great idea to get a reverse mortgage… until her children explained to her what a reverse mortgage really is… then she was mortified when she heard the bank takes ownership of the home. Fortunately, we (the family) have found other ways for her to stay in her home without hurting our finances and without getting the banks involved. Just for a little perspective on homeowners in my mother’s age bracket: many of them (my mother included) have never owned a credit card and every one of their possessions (cars included) were purchased for all cash.

At her age why is she worried who ownes the home? See would have the $2MM dollars and the bank can have the future headache and risk or return if it goes up or down in value.

Seems you scared her on purpose to swindle her out of a better life so you can get the home.

Nice to know you let your family live in a tear down home.

“Nice to know you let your family live in a tear down home.”

Yea, throw mom out of her house to the old folks home immediately and sell the house. Right?

“let family live in” as if it were the kids to decide where mom wants to live? Or how.

You can try that on my mom and she’ll shoot you without hesitation: Moving or changing anything is totally out of question.

You seem to be too greedy to see that some old people don’t want changes and see only greedyness instead.

Mom thought it was a good idea to get a reverse mortgage. There must have been something that sparked her interest in the need for money? Maybe mom wants to live in a retirement home. Instead she is in a tear down shack that is probably infested with mice with only 10 cats to keep them under control because the family is ready to pounce on the home when she dies. If they love mom so much rebuild the home on the 2mm lot.

@Sean

“Tear down” doesn’t mean what you think it means. The 90 y/o house is worth 2 million only for the land. Anyone willing to pay 2m for it will tear it down and build a mansion. It doesn’t mean the house is decrepit or full of mice.

“That flood of homes is unlikely to come because those golden hand cuffs are too enticing to take off”.

I hope that statement is correct Dr. I am very concerned that the fiscal hole the government and FED have dug and are digging deeper every day, could eventually lead us down the road of massive asset deflation, when the whole Ponzi supported scheme comes crashing down. I can easily imagine the foreclosures we had in 2010 being nothing compared to what will happen under a certain set of circumstances. Paying off a home is about the smartest thing a person can do IMO. Financial winter may be coming, so get prepared people.

I see no reason in not paying off a house. As part of my portfolio asset allocation I have 10% in cash earning nothing. It is part of my overall financial picture. In a deflationary period, earning nothing beats losing money leveraged in a depreciating house. When assets finally stop dropping, my cash can be put to work at the depressed prices.

Not paying off a house and keeping it leveraged does not account for the fact that in a deflationary market, you can lose value quickly.

I’m very curious to see whether we get strong inflation or deflation first. I could see either scenario…if Yellen pretends to be a hawk, it could be the latter. If she lives up to her dovish roots, the former. It’s going to be quite a balancing act.

The irony, of course, is that anyone in the stock market is benefiting from Fed policy. I can’t stand what the Fed is doing, but I’m profiting from it. The Fed already skipped one QE off-ramp, and I don’t see any reasonable scenario in the near future to suggest that exiting QE will be–all of a sudden–prudent.

If she does suddenly pull back, I think you could get the deflation you’re counting on. That would be very ugly, particularly to the highly leveraged housing sector.

In a deflationary scenario, it is better to be in cash than it is in anything at all, because all assets, including real estate, fall in price.

However, having a paid-for house is the next best thing and is a hedge against the hyper-inflation the Fed is working so diligently to produce.

Yes it is sadly true that most Americans have nowhere near enough saved for true retirement and will work until they are too old, sick or disabled to do so or until they are dead. If you live in an expensive area where you can’t put away any money, move. If you don’t have the skills to command good income, get educated. If you spend money on the latest gadgets and gimmicks, for God’s sake stop. I know plenty of people (including myself) form humble backgrounds who have gotten educated, made responsible financial decisions and generally avoided acting the fool, and are not high IQ types smarter than the average Joe. who are financially secure or on their way to it. That is why I have no patience for whining.

Anyone who is living in free and clear million dollar house but who has no other assets is so far ahead of the average Joe it is ridiculous. Worst case scenario is to sell and downsize, move away, rent, etc etc. Take your first $500K tax free, what a beautiful thing.

Housing might not be very liquid in rural Alabama, but it is extraordinarily so in SoCal. Liquidity is simply not an issue here.

Over the long run values in coastal SoCal have and will continue to go up. Talk to the guy who bought property here 30 years ago who owns it free and clear and ask him how he feels about his purchase. Talk to the guy in 2043 who bought his property yesterday and you will get the same answer.

If you are not living beneath your means than you need to change that immediately and take whatever steps necessary to get to that situation.

I totally agree with your assertion that if you can’t afford to save, move. I just made a similar argument above.

What I’m not as sure about is that coastal SoCal real estate will continue to appreciate. We’re both speculating, but here’s my thesis that this may not be the case:

a. Business friendliness. Compare when Southern California “boomed” in the 1980s to now. Look at the pool of jobs available and cost of doing business to employers. It’s a night-and-day difference. Unless you’re a two-income doctor/lawyer/entertainment industry/trust fund set, you probably won’t be buying coastal So Cal in the future.

b. Foreign investment. Remember when Japan was going to take over the world? That was before the lost decade…errrr, two decades. You don’t hear about Japanese money anymore. But we hear about Chinese money. I wonder if anything could ever go wrong with that regime…

c. “Fairness.” Life just isn’t fair, and California is working really hard to even things out. If you’re making too much money, the state will work hard to ensure you pay your “fair share.” That will only continue to escalate, and as that happens, other housing pastures will be sought.

Anyhow, I really do enjoy your great post. Just thought I’d add some conjecture.

I should probably add the footnote that “won’t appreciate” means “won’t appreciate relative to inflation.” We all know what’s going to eventually happen, thanks to the Fed…

You can’t compare California to a country like Japan. Try comparing SoCal to Tokyo. Now how does the property value theory hold up? It doesn’t.

For the most part property is very cheap in the US. We have a few expensive markets on the coastal cities but that’s true everywhere.

If people want cheaper housing look in a different area. In order for SoCal to become cheap it will take an act of nature powerful enough to push people away. Yearly typhoons or very powerful earthquakes might do it. Until then, it’s not going down to an average income affordable level.

You make valid points but raise serious questions as well.

1. How about the older generation that has millions, yet won’t spend? I have family that can shove charcoal up their rear and produce diamonds in 1 week, yet they won’t even take a trip because they have to “spend money”? And they see their kids, grandkids, and great-grandkids living below a standard they were able to achieve by default? (post WW2 boom) I say it’s only right to share a bit within the responsible family and give them the boost that is required. One thing I notice about SoCal, everyone “in the club” had some help or the rate Ivy league education.

2. I agree with moving to a cheaper area, but not necessarily with higher education as a panacea. Too many kids in too much debt, and degrees are getting watered down. At the very least I say pick a hot area and try to guess it’s longevity as best you can. And don’t forget we still need plumbers and welders, nothing wring with those at all.

3. Not buying gadgets is a tough pill to sell to the younger generation. I understand the importance of the message but they don’t. World = gadgets.

4. I do SERIOUSLY question the 2043 property value theory. Possible? Yes. Probable? Things are changing way to much. Interest rates are as low as possible, $17 Trillion in debt and growing, Obamacare premiums coming up, and the ever growing shortage of water. These 4 things make me question rising values.

Living beneath ones means is a key factor. BUt how many people realize it takes $100k household income just to LIVE in SoCal? Granted that could be 3 guys making $15/hr each as roommates, or a couple making $25/hr each, etc etc but that’s the bare minimum for what’s a normal middle class life at least in “flyover country”. The reason flyover country is a valid gauge is many cities in that area score a flat 100, which is middle of the road average, on the cost of living index. Versus Los Angeles 144 for example.

P.S. Let us not forget education. Example – Minnesota, Wisconsin, and Iowa all have the best K-12 schools in the nation, and they are “free”. Where do you have to live in SoCal to get that same quality, and how much does it cost? It takes Cerritos, Torrance, Manhattan Beach, etc.

Great point about education. Actually, in general, I think Southern Californians are ignorant about life outside the area’s borders. (I was.) Here in beautiful Florida (I’d argue better weather for 9 out of 12 months of the year, but I digress…), my $5k/year in property taxes gets me:

* A better school system than at my $12k/year in property tax San Diego house.

— Free breakfasts, cheap lunches.

— Free bus service. ($1k/year in San Diego.)

— 17 students/classroom. (30ish in San Diego.)

— An arguably better education.

— More arts and PE and music classes, etc…

(Same goes for top-notch, LA-area districts, where I grew up.)

* No state income tax.

* Better maintained roads.

* Libraries open seven days a week.

* Better services overall.

You get the idea. Sure, I have to drive for twice as long to get to DisneyWorld as opposed to Disneyland, but it ain’t the end of the world.

I still wonder who’s going to buy/occupy all of these homes once the golden handcuffs are released by the grim reaper. Those inheriting? Yeah, to some extent. But, really, let’s say that’s even half of the market, that means you’ll still have millions of units coming on the market in the next decade…and pretty much ready for the wrecking ball. Where is this great influx of well-capitalized buyers going to come from, ready to put cash to work to build contemporary McMansions…in Torrance, Gardena, Lawndale, etc…

Double yes.

Where are all the buyers going to come from? That’s my question exactly.

In about 5 years, we should start to find out.

Good follow up points above. Regarding education, if you are a journeyman plumber, electrician, etc, then you are educated and have a marketable skill, same as a doctor or lawyer but with lower relative pay. Also regarding Florida, I have lived there and currently have family there and pay is low which has more than wiped out the benefit of no state income tax, and regarding education it is lacking in quality at the college level – a state with almost 20 million people and no real serious nationally recognized schools, UM probably the best, whereas in Cali we have many many excellent institutions. Cali pumps out well-educated grads that populate the state, you do not have that in Fla. I like Fla but it’s not where the smarties are setting up camp and building careers.

When looking at the investment angle you should have RE as part of the portfolio along with domestic and international stocks, bonds, commodoties, cash, collectibles, etc. You can scour the country and look for the cheapie hot up and coming areas (maybe…) or you can go blue chip and get into SoCal coastal. To each his own but I am taking my chances with SoCal coastal. It is desired world-wide, as well as locally, regionally and nationally. You are competing with more and more sources of money these days, not less. There is an ongoing race to devalue currency and parking money in US RE is a widespread strategy.

There are 1.3 billion with a “b” Chinese, even if only the top 5% are parking money in US RE that is 65 million people, that is a staggering number. Not to mention upper middle class and wealthy from other areas globally. Cali is a top destination.

The regular Joe has been priced out of many metro areas around the globe for a long, long time. This is not a SoCal phenomenon or Cali or even US issue – it is global. Sure there are always going to be pullbacks from time to time but the overall trend in places like SoCal coastal is up. Like I said, RE should be part of your assets, and you get huge tax breaks and ultimately can own the property outright to greatly diminish housing costs. Good luck to all, I will take my chances in SoCal coastal as far as appreciation goes.

Regarding education, I was speaking of public schools, where most of us are from. In that respect, for middle class, CA is not the choice. Yes, CA universities are great (if you can get in, ever) but most in the US period are fine. My goodness, how do the 250, 000, 000 non-CA people do it?

They do fine.

If you live in St Louis, Minneapolis, Omaha, Dallas, Nashville, Charlotte, or countless other million plus metros, you dont have these cost of living problems. You actually have less problems overall.

You sound like some kind of chinese elitest. Bullshit in my neck of the woods. And I ain’t alone.

You reiterate the point I made in my original post where I suggest relocation to a cheaper area for people who do not have the earning power or financial wherewithal to live the life they desire in SoCal. My point on education was directed at CA vs Fla and the dearth of quality at the college level and as a former resident I believe it has an impact on the state, demographics and opportunities there. Contrary to being Chinese or elitist, I worked hard to earn my way to an advanced degree and watch with dismay as Chinese are buying up much of the RE in my area and driving up prices for everyone. Nevertheless I recognize that as I have educated myself and work hard I can afford expensive SoCal RE and I believe that my money is better parked here than in suburban Omaha.

Going by some recent surveys, University of Florida is roughly equivalent to the average UC, so I am happy with that for my kids. (Cheaper, too.) Yes, there is no tech sector like there is in Silicon Valley, but really, Southern California is not the brain hub it used to be in the aerospace days. Roughly speaking, I would say both are primarily service sectors, overall.

I am a bit spoiled in that I started my own company and simply have a BA, so my kids can continue that one day, if they wish. Honestly, I am ignorant on how advanced degree programs compare between the two states, but a lot of the elite of California head to the Ivy Leagues, anyhow. (Just like Floridians.)

Exactly. I live in Houston. I’m 26. In August 2012, I bought a brand new 3 bedroom, 2.5 bath, 1700 ft^2 townhouse for $90k. It’s in a nice, safe neighborhood. Not exactly living in the ghetto. I live 20 minutes from work.

My income also isn’t some paltry amount either. I make right around $100k. I fully intend to have my house paid off by the time I’m 30.

Let’s see you do THAT in California!

Good post Falconator. Coastal California RE has always been and will always be desirable. The amount of foreign money that has flowed into CA RE the past few years has even surprised me. As you mentioned, the race to devalue currency is on in a big way, that along with economic uncertainty make hard assets look really good right now. All the dollars used to buy the cheap shit from Asia is coming back home via millions of rich Chinese who want to own a piece of the promised land. Same with oil. Every time you fill up that gas guzzler SUV with cheap gas, those dollars are coming back home via super rich middle easterners. They too want a piece of the action here too. For anybody waiting patiently on the fence hoping for the big collapse so they can score a deal on desirable CA RE…good luck.

“Coastal California RE has always been and will always be desirable.”

When they run out of water it won’t be so desirable any more. It won’t take long by current speed.

China is being held hostage buying our debt, and whether they detach from the dollar, or they continue to let us rack up debt and play the game our way, they are extremely fragile. They have no consumer economy, because of their low-paid workers; everything is set up for the elite. As someone else on this page hinted, those who are gaga for “Chinese money” will soon sound as dated as the people in the 80’s who thought Japan was about to take over the world.

I gather there are some spoiled Chinese kids coming over here and buying houses, sure, but to extrapolate from this to “coastal CA. will always be desirable,” that this is where the big money will always come, is a stretch. This is a heavily populated area and it’s not just the houses in Beverly Hills that are outrageously overpriced. As the economy continues to deteriorate, and jobs fly pell-mell out the window, you think this is all going to be bought by Chinese or Russians? All over the world, there is an ever-diminishing middle-class, and a small elite — this puny elite is going to buy all the coastal CA. real estate? And what is going to make them want to live there when the inevitable urban decay, by which Los Angeles will be hit very hard, starts getting worse?

Also, do you know how easy it would be for China to tip over into chaos? Just one little “black swan” event could crash this country and China together. I have opined before it will be riots in Europe caused by the deindustrialization and unemployment that is being exacerbated by the Euro, but it could be a natural disaster or something else.

@OutofCalifornia, +10 for your comment.

Since 1997 real estate prices in the heavily populated urban areas of California have escalated by 250%. Almost all of the price increase is attributable to the Federal Reserves’ ZIRP (zero interest rate policy) in effect since 2002.

Shadow inventory is kept off of the market due to the Fed’s ZIRP. (i.e. banks borrow from the Fed at zero percent to cover their foreclosure inventory while “official” inflation is at +3%)

The Fed’s ZIRP means that interest on certificates of deposit, money market funds and short term bonds is basically zero. Therefore investors chase after things that have yields at are at or above inflation (i.e. real estate, stocks, commodities). This creates more asset inflation.

Current “golden handcuffed” homeowners are psychologically conditioned by the market manipulation by the Federal Reserve’s ZIRP into thinking their properties will increase at 10% to 20% a year, every year, forever! This Pavlovian response engineered by the Fed means lower inventory levels. These “golden handcuffed” people are not going to sell when they have been brainwashed into believing their property will be worth 25% more next year.

SoCal’s U-3 unemployment number is at +10%, and the U-6 underemployment number is at +20%. These are depression level numbers.

I think what we can all agree on is that there will be greater bifurcation. The number of ZIP codes appealing to rich Chinese or Middle Easterners is a handful. For the rest of the market, fuggetaboutit.

Which raises an interesting point: it seems like the healthiest segment of the future So. Cal housing market will be dependent on seasonal residents. Heck, I’ll be honest, I’m toying with the idea of getting a condo in one of those ZIP codes in order to avoid Florida’s July and August.

So what happens to a city when the wealthiest spend a few weeks/months a year there and have no voting power? And the rest of the community is told to blame their sorrows on those that are rich. That’ll be interesting to see…

it seems by reading some of these post that some people will always be renters and others landlords.

On the snotty Westside.

Two years ago it was the banks who were holding the homes and we waited for the pent up foreclosure inventory and they were going to collapse and we shamed them…today the banks are buying up the homes and becoming landlords. Either way we seem to blame the banks. Ironic.

Seems we are a country of whiners that live beyond our means. And that goes for the people living in SoCal on an income designed for Florida.

@Sean wrote: “…Two years ago it was the banks who were holding the homes and we waited for the pent up foreclosure inventory…”

The phase for today: “Vampire Foreclosure”

The shadow inventory is still out there. Over +55% of California foreclosures, the former “owners” still live there. Banks can keep foreclosures off of the market for a maximum of 10 years per Federal banking laws.

http://blogs.marketwatch.com/capitolreport/2013/10/02/vampire-foreclosures-are-whats-keeping-bank-inventory-high-analyst-says/

Do you know why it’s called shadow inventory? Because shadow inventory will disappear the second somebody turns the light on.

“today the banks are buying up the homes and becoming landlords”

No, banks are mostly selling to other (non-banks) investors as they run out of private citizens to swindle.

Bank won’t buy real estate, they get it for free from defaults: FED pays the losses and bank gets to keep the property as FED is not taking it.

Something you got for free is quite easy to sell with huge profit. Even I can do it.

How did the bank get it for free? They buy your home. That’s what banks go. They own the home until you pay it off. So most of their business comes from purchasing property.

What they get from defaults they paid for in the first place. They average joe make about 1 year of 1% interest rate payments then defaulted.

And now Wall Street is going to cash in which consists of people buying stock funds. If the action and profit is all that great buy the stock funds.

Personally I think it’s all a scheme. Bt it’s the only game in town so if you want a home these are the rules … But the rules suck and are not good for long term stability.

Anyone else looking ahead to the increased tightening by the banks due to Frank Dodd on Jan. 1, 2014? As I understand it, loan ratios and ownership % will make the banks more restrictive on loans and, I may be wrong, but I’m under the impression that interest only and negative amortization loans will go away. If that happens, I figure all the current heavily leveraged interest only folks will be in trouble when they go looking to refi….

Meanwhile, the rich Hollywood elite are putting moats around their mansions and their cars are armored and electrified to protect them from the hordes of the poor in the gangland slums of LA:

http://www.hollywoodreporter.com/news/moats-las-newest-extreme-real-651043

http://www.hollywoodreporter.com/news/hollywoods-new-favorite-cars-are-629413

Thank you Dear Leader Obama for taking care of the Banks. Since everybody will be so dependent on Social Security, how can our Dear Leader Obama propose to cut it so the military will not get cut? The military maintains the empire for the financial elites which according to our Dear Leader is more important than the people having more than a mere subsistent standard of living. All hail the Chief Obama.

This may be true that Americans are bad savers, but can you blame them in this inflationary environment and manipulated market?

What’s going to happen if they don’t pay their debt, are they going to get a free hot and a cot in debtors’ prison? Don’t hate the player, hate the game.

I honestly haven’t seen a flood of “big” investors buying …. Or banks renting out homes in my area. Rentals that are available still appear to be mom and pops for the most part on SFR’s. maybe it is happening in other states across the nation but not here so much on the west side IE.

I’m just saying if its true we are becoming a renter nation, then I suggest those with the capability should become landlords!

The whole concept of “retirement” and being a “pensioner” are really recent in human history. Probably a one-time event due to circumstances and timing. For most, if not all, of human history people worked until they keeled over. Welcome back to reality.

But don’t you dare call a Boomer “lucky” for happening to be born from the mid-40’s to the mid-60’s, the “one time event” era of the pension, rising median incomes, affordable housing, affordable education, affordable health care, etc. Now, with Boomers running the country (government), they have no idea what to do about the emerging global economic and competitive issues, and are also leaving their children with the worst inheritance (debt) in our nation’s history. Thanks, Boomers!

Well, we got to keep our cheap educations – that’s true. We were very lucky that way. But everything else is long gone. When you’re 60 you won’t feel lucky about things you had when you were 25 that were all taken away.

Yeah, I had great health insurance once, when I was young and healthy and didn’t use it, but I haven’t had it for a while. I had a pension once too, but they took it away and gave me a 401K when I was already 40; then there was the crash of 2000 when I was 50; then there was the crash of 2008. Gee, lucky me. Once I had pension.

And I run the government, too! Oh wait – I don’t run anything. But the people who do run it are the same age I am! Isn’t that wonderful for me?

So Cal is like a 3x stock ETF…the middle class is disappearing here faster than the rest of the country, the wealthy are getting wealthier, and the poor class is growing larger.

What that means for So Cal housing is fewer middle class neighborhoods for the middle class, more apartment complexes for the poor and middle class, and the wealthy enclaves becoming more and more entrenched in tight inventories, with just the Prop 13 lottery winners leaking out lots by attrition

The formerly “middle class” neighborhoods are DISAPPEARING along with the middle class and turning into gentrified “upper middle class” neighborhoods forever.

You make a good point that ties in with the risk of buying “elite” coastal property that only goes up in price. I can show you real estate in Mexico City and Sao Paulo that is more expensive per sq. ft. than Coastal Cal. However, I do not think you could put up with the life style of body guards, armored car and helicopter rides to your office downtown to avoid the traffic and gun fire. The loss of the middle class will kill, literally, the Cali life style. What made Cali an attractive place to live was the very middle class that the elites belittle. Go ahead and buy that expensive house, it probably will continue to go up in price just like Mexico City and Sao Paulo but watch your back.

Let me preface this statement as a former Californian, I love California but left in 92 when the recession hit to take a job in St Louis. Fast forward 21 yrs and after living in 3 different cities I’ve settled into Indianapolis for the last 10. I own a 2500 sq ft home on the north side of Indy that set me back 275k in an middle upper class neighborhood. Resale value now is 350 +- my 15 yr note will be retired this December as I’ve worked to pay it off early.

My plan was always to return to California but with costs being what they are, I just don’t see it. I make almost 400k a yr and my standard of living here is way higher than what I could have in Cali. I’ve been able to buy investment property in Colombia and Buenos Aires, along with most of my wealth in PM’s. SoCal is in such a huge bubble something has to give. I’m 43 and all my friends there are still renting, they’ve pretty much given up on ever owning anything.

Yea I don’t have mountains or ocean and I got winter coming but I also have some security and have been to 53 countries since I left Cali, something which I would have never been able to do living in SoCal. There is life after SoCal, but yeah I understand the draw.

Bla bla bla I make 400k year

bla bla bla I’m 43

Bla bla bla I’ve traveled to 53 countries

bla bla bla

You are a show off. If you can’t buy a nice home in SoCal on 400k a year you clearly are doing something wrong. Enjoy the snow and showing off to all of you midwest friends who I am sure would love to hear less of how great you are and have you move back to CA.

Note to everyone in CA, this is why people from other states think we are full of ourselves.

Jerkstore, good for you on your extraordinary income and modest lifestyle. However, you are emblematic of the myth that the 1% plow their post-tax dollars back into the American economy. Exhibit A is Columbia and exhibit B is Buenos Aires. I’m sure there are other exhibits.

When people complain that 47% of Americans don’t pay federal income tax, remember that they spend every. single. last. dollar back into the local economy.

Seems there is no shortage of former California residents that are content with not moving back. Perhaps the rest of the earth’s inhabitants aren’t missing out on much after all.

Being originally from Indiana, but having lived in LA for the past 15 years, I see where thejerkstore is coming from. I don’t make the kind of money that he does, but I make six figures (can work anywhere from home,) and, if it weren’t for family and friends, we’d be moving to a place like Indianapolis in a second. The problem is, my wife’s family is from LA, and my entire immediate family eventually moved to LA, so it’s a real balance between money/lifestyle and family/friends, now that we have a 2 year old son who is so close with his grandparents.

We’ve been looking at Indy, Portland, Denver, etc., and it’s insane what you can get there for the money, comparatively (especially Indy.) My goal was to move to a city that the grandparents all like, because they can sell their homes and make quite a profit by buying in a smaller market, but it seems that our baby boomers parents living in SoCal would prefer to stay put. It’s all very frustrating.

Regarding the poor saving rate, it is a bit different in Latin America, and other poor counties. At first, when I saw all the rebar jutting up out of the roofs of houses, I was a bit perplexed. I later came to find out that houses are often built in stages.

Houses are built with the ultimate height in mind, but not all floors are constructed at once. The ground floor is constructed with enough heft to support a 2nd (or even 3rd) floor. But if not enough funds are available, they just leave rebar jutting up so that they have something to anchor the base of the 2nd floor walls.

When more money is available, they complete the 2nd floor.

I’ve heard another interesting thing about those half-built houses. In some countries, this is actually to get around property taxes. In some locales, you don’t pay taxes on a house that is currently under construction. As long as they have the rebar jutting out the top, they can classify the house as a construction project. Thus, the house might be “under construction” for decades!

People make their own choices. I don’t see where there is a problem?

They chose to spend their money on stupid shit.. let them do it, we are not a fascist or communist society to dictate people on how their money should be spent.

It’s not that hard to live within your mean and save the money if you want to.

You can blame media, marketers, government, etc.. but at the end of the day it’s all in your hands.

Buy a home you can afford…

Keep at least 1 year of expenses in reserve

None of these concepts are hard to comprehend or achieve. And should you choice not to do it? It’s your choice (and this is why we get this statistics).

it’s not good or bad, it’s just is.

This article is about retirement as a thing of the past. People will not leave their jobs until they die. This means that their will be fewer jobs for the younger people, which means fewer babies will be produced by responsible people. “The poor you will have with you always.”

FHA type appraisers do not appraise the homes at the prices that cash purchasers pay, so the “middle class” purchaser has to put much more than 20% down. Gone are the days of the 3% down. Middle class purchasers need to consider this fact when they consider purchasing. They need to save up more of a down payment and reduce their sights to cheaper homes in el cholo (or el chuco, if you prefer) land.

Just a quick fact check, here are the numbers on millionaires and billionaires in China for 2012. Everybody needs to stop with the millions and millions talk.

“The number of Chinese people boasting personal wealth of at least 10 million yuan ($1.6 million) hit 1.05 million in 2012, up 3% over the previous year, according to the report. The number of “super-rich†Chinese – those will wealth of at least 100 million yuan – increased 2% to 64,500 in 2012.”

Source: http://blogs.wsj.com/chinarealtime/2013/08/15/chinas-millionaire-population-grows-less-quickly/

@MrSmith in KTown, LOL!

Yet according to some of the rocket scientists posting here, there is an endless horde of money laden Chinese nationals buying up all the available properties on the west coast leaving nothing for the locals.

@ Ernst – I think we have seen statistics before where the percentage of Chinese (or maybe all Asian) buyers in Cali was about 10% of the buyers. Perhaps that is a total average. If you take percent of Chinese buyers in San Gabriel Valley maybe it 75% and if you take percent of Chinese buyers in Barstow maybe its 1%.

Leave a Reply