Housing Bailout Bill Failure: Examining the Boondoggle Legislation and Populist Uprising against Wall Street. 5 Reason the Bill failed and 5 Easy to Implement Solutions that can be Used Today.

Instead of the House of Representatives sending in a nice sealed envelope a candy gram to Hank Paulson of $700 billion, they instead decided to listen to the people and did a reverse bailout wiping out $1.2 trillion in stock market wealth. Go figure. The House of Representatives actually listened to the massive uprising against this poorly devised bill. You wouldn’t know this from the mainstream media since they of course know much more about the markets than us regular citizens and had already started creating Photoshop templates of “bailout success!” to run for the entire day next to their tickers. In addition, we have a large group of politicians (not economist or those with understanding of the markets) telling us that if we don’t sign off, there would be hell to pay. Guess what? That price tag was $1.2 trillion today.

I was jumping back and forth through various cable news and financial shows and you would think that they went out to the “investment pundit” talking head swap meet to gather the guests for the night. The message was simple:

“How can they allow this to happen!”

“People won’t have access to their credit on Main Street! We must help me, I mean them!”

“These are big problems and we need to get this bill passed now!”

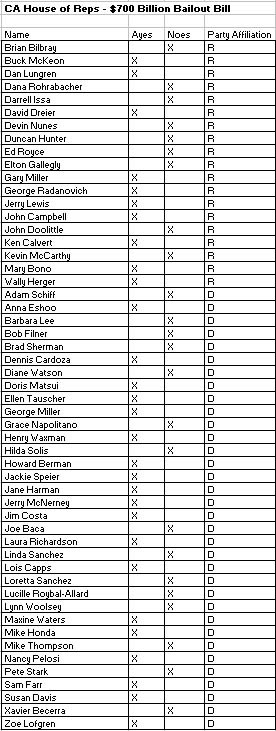

You get the point. To test this theory I went on “Main Street” to my local bank and guess what? Incredibly, they still have the ability to make loans. What a shocker. They don’t however have the power to make option ARM, interest only, or other toxic mortgages but how is this bad? I wanted to compile a list of Representatives from California who voted for and against this plan:

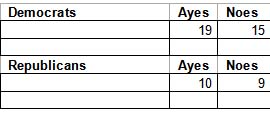

Incredibly, the vote for California was extraordinarily close:

Total Ayes:Â 29

Total Noes:Â 24

If you have a chance, please take a moment to contact your Representative and let them know how you think:Â House of Representatives CA

If you are wondering about the quality of some the Aye votes, you can look no further than that of Laura Richardson. Who better to vote for this plan than a Congresswoman who bought a home in Sacramento with a no money down subprime mortgage from now defunct Washington Mutual? Not only was this her method of helping the housing market, she stopped making payments on the home until a real estate broker picked up the home via a foreclosure.

Maybe she had an incentive to get this bill passed? Okay, maybe she lost one home by mistake. But what about going in arrears 3 freaking times on another home in Long Beach and another in San Pedro! The home in Long Beach is now caught up according to the Press Telegram but she is still behind on the San Pedro home.

Oh, and she also took a loan from a local strip club owner. Thanks for that aye vote Laura! Hope you enjoy your taxpayer funded $169,300 a year salary for voting.

Aside from that there were some shockers on the noes. Again, if you can please take the time to offer your support to those who stood up against the mainstream media, opportunistic politicians, and Wall Street. The mainstream media wants to scare you into thinking that come tomorrow, you will have zero access to credit. Are you kidding me? If that is the case, I’ll go on Virgin Lending and get a loan. If we can make loans to third world countries for seed money, you think we aren’t going to get something here?

And of course I ran a quick tally for New York and out of 29 Representatives only 4 voted no. How shocking that 84% of New York Representatives wanted this Wall Street welfare check to go through.

The bill ultimately was setup as a failure from day one. Paulson handing out a 3 page nasty gram was absolutely pathetic. It essentially amounted to an ultimatum with Czar like powers. The Congress from day one should have rejected the bail out and started from scratch. Instead, they went along with a fundamentally bad idea for political fear and as it turned out after nearly 2 weeks, the foundation was so shoddy that they will need to go back to the drawing board.

This bill was a pathetic attempt at smuggling money to Wall Street from Main Street although it was under the guise as help for the common person. Even with all the new modifications in the 110 page updated bill there were so many loopholes, that it was only a matter of days before Wall Street gamed the system. “Some CEO compensation” or the lack of clarity in how assets would be priced were main sticking points.

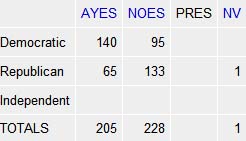

Some of you may be thinking that many of us simply want to punish Wall Street at the expense of everyone else. Here’s the thing, Wall Street should be punished yet the notion that if Wall Street fails then we all fail is patently disingenuous. In fact, the House of Representatives on both sides rose up today to vote this thing down:

From watching the mainstream media, you would think that what the House did was a crime. They simply held their own and represented their constituents. A large group of Democrats and Republicans saw something wrong with this bill. I’ll give you 5 major failures with the initial bill and later in the article offer 5 new sticking points in any bail out.

5 Reasons This Bailout Failed

(1) Mainstream Media: The mainstream media ran by journalist, some that are amazing and some that just want to sell ad space for one reason or another ran with the pro-bailout propaganda since day one. In fact, many were already on the bandwagon with the 3 page proposal from Paulson! How in the hell can you support a $700 billion bailout with 3 pages only? The media being hurt by the down economy thrives on ad revenues. Who pays these revenues? Companies. Which companies? Companies on or that trade on Wall Street. They know which side their toast is buttered on.

(2) Wall Street: Wall Street flat out miscalculated the anger on Main Street. They wanted to scare mom and pop investors that should they not vote, their 401(k) was going to see a big hit. Guess what? Many don’t even have a 401(k). The next fear factor was losing home equity. Guess what? Many people, approximately 30% own their home outright. They don’t have plans on selling and never did. They didn’t play in the Wall Street casino. Many in their 20s and 30s are simply trying to advance in their careers and have had very little time to build a major retirement holding in their 401(k). It is worth repeating the break down of median income households and their 401(k):

401(k) Median Amount

20 year olds

(Salary Range)$40,000 – $60,000 = Â Â 401(k) Median Amount $16,393

30 year olds

$40,000 – $60,000 =Â Â $38,693

40 year olds

$40,000 – $60,000 = $78,834

50 year olds

$40,000 – $60,000 = $99,932

60 year olds

$40,000 – $60,000 = $97,588

As I discussed in a previous article:

“57 million households own stocks directly or through mutual funds. Given that there are 105,480,101 or so households, that means 54% of people will be impacted by a decline in stock values directly in their portfolio. What this also means is that 46% of Americans do not own any stocks.”

They assumed fear was enough to get this thing going and have the public rally behind the cry. Well as it turns out, half of Americans don’t own stocks and the other groups are split into different camps. For example, a younger working couple is more worried about their future job security than losing say 20% of their account value which is probably only $16,000 to $50,000. So the loss ranges from $3,200 to $10,000. One visit to the doctor for a minor injury will cost you this.

(3) Current Administration: Paulson carrying the flag of the current administration did not have enough political capital to get this going even if the bill was drafted correctly from day one. It would need buy-in and not a fear mongering ultimatum drafted on 3 pages. Even if you look at the votes, it is the current administration’s party that revolted in large numbers against this bill. The majority of the noes came from House Republicans including folks like Dr. Ron Paul.

You also had a large number of Democrats including Dennis Kucinich who voted no on the bill. Ironically, it was the polar opposite sides of both parties that came together against this poorly constructed bill. How ironic that the most liberal and the most conservative members where saying nearly the same thing. The left was arguing that this bill amounted to a blank check to Wall Street with no protection for the American tax payer. The right was arguing that this goes completely in the face of free market capitalism and amounts to corporate socialism. Strange bedfellows indeed today. Kudos for those members that stood on conviction from both sides of the isle.

(4) Condescending to Public: It would help if Paulson explained why he needed $700 billion! I mean talk about delusion. The public is furious because they perceived what the mainstream media and certain politicians could not. That this bill was a sham which it is. Paulson and some Congressional members never leveled with the American public. All they kept saying was “if you don’t vote for this, ahhhh man, you don’t even want to know.” Great way to get people to vote. And then they argue about the one reason many Americans view as the root cause of this mess. More credit! Many prudent Americans feel that credit itself was the problem and now they want these folks to use their money to dole out to credit addicted companies? No way. The mainstream media also felt that if it repeated the same message over and over the public would kowtow and it would be a done deal.

Even on Sunday night they were talking about things as if the bill had already passed. This is the same media who was asleep at the wheel during the housing bubble. In fact, they glamorized it with housing bubble porn with flip this house shows and remodeling gone wild shows.

(5) Populist Uprising: People are fed up. People are sick and tired of being treated as a consumerist hamster. There is such a large disconnect from the realities of Main Street from those on Wall Street and the lives of those in the mainstream media. They simply do not understand the silent anger many Americans feel. These Americans despise the fact that we are having to answer to foreign banks because our local representatives cannot manage their Wall Street masters. Many of these Americans fall under the Benjamin Franklin rules of frugality:

“1. A man may, if he knows not how to save as he gets, keep his nose all his life to the grindstone, and die not worth a groat at last.

2. Beware of little expenses; a small leak will sink a great ship.

3. Buy what thou hast no need of, and before long thou shalt sell thy necessaries.

4. A fat kitchen makes a lean will.

5. Many estates are spent in the getting, Since women for tea forsook spinning and knitting, And men for punch forsook hewing and splitting.

6. Think of saving as well as of getting: the Indies have not made Spain rich, because her outgoes are greater than her incomes.

7. Women and wine, game and deceit, Make the wealth small, and the wants great.

8. What maintains one vice, would bring up two children.

9. Who dainties love, shall beggars prove.

10. Fools make Feasts, and wise men eat them.”

1776 where art thou? Many Americans are yearning for a return to a time when our economic prowess was based on our ability to spend and invest wisely. Not what we have now which is Wall Street turned into a casino for the connected and wealthy. The ability for information to travel so fast and people to be informed is fantastic. The fact that many of you contacted your Representatives shows that we are in a new era of politics. It was only a matter of time before the politicians listened to the will of the people. This was one of those rare moments.

They’ll try again to jam something down the throat of the public but hopefully they scratch this bill and start from scratch. Maybe, they’ll even explain to us why they needed $700 billion. Let us first look at the current price tag:

We’ve already put at risk nearly $1 trillion in taxpayer money. We want to put $700 billion more at risk? How well did that last $1 trillion go? The irony is one of the more thought-out plans, the Housing and Economic Recovery Act of 2008 will be utilized only to a minimum extent. In fact, we will use some of the points in this bill for our new proposal. Many of the members will be forced to action so a bailout is going to happen. Let us ensure that they include these plans at a minimum.

5 Step Proposed Plan – New Requests

(1) Mortgage Cram-Downs: It is fascinating that no one is talking about this in the current bill. One of the first things that got thrown to the wayside is cram downs. Mortgage cram downs are the quickest thing that can be done right now to help homeowners in trouble. How so? Let us say in bankruptcy a judge looks at a borrower who has a $100,000 valued home with a $90,000 1st home mortgage and $25,000 in total unsecured debt. The judge can cram down the unsecured debt to $10,000 thus matching the total assets of the borrower ($100,000 home) to the total debt ($90,000 1st mortgage + $10,000 unsecured debt). Why was this removed? Credit card companies and 2nd note mortgage holders would get wiped out with this legislation. They will not volunteer for this since there is nothing in it for them. Clearly they would rather unload the debt to you instead of realizing the loss from their imprudent lending.

(2) Mark to Market Similar to Housing and Economic Recovery Act of 2008: It is amazing that the new legislation actually wanted to halt the mark to market accounting rules. What this did is gives an out for institutions to once again hide the sausage until they unload it onto the public. What needs to be done is what was proposed in the Housing and Economic Recovery Act of 2008. Lenders that want to participate can do so by doing the following:

*Take a current appraisal of home

*90% offer from government of current appraisal

*One-time 5% fee to build up loss fund

*Homeowners participate in equity sharing with government tiered over 5 years

So how would this work? Say one of those craptastic WaMu loans made at the peak for $600,000 is now in trouble. The current home value is $400,000. Should JP Morgan wish to unload this loan, they would get $340,000 and the borrower now has a reduced loan. The borrower now has to share any equity gains with the government for the next X years. This of course will mitigate some of the moral hazard problem. Everyone wins. JP Morgan has already estimated that they will write down $31 billion in loans from the WaMu garbage can so at least they get something here. Borrowers get to stay in their home and the government at least has a way to recoup some losses later.

(3) Zero CEO Compensation on Institutions that Participate: This one is simple. CEOs shouldn’t get one penny for participating in the bailout. If they have managed to run their company into the ground and are asking for taxpayer assistance, we get to set the terms. They are lucky. In fact, we should give them an incentive that should they cooperative for the next few years they won’t be prosecuted to the fullest extent of the law when we have our 1930s perp walk sessions which will happen. CEO compensation? Are you freaking kidding me. How was this even in the bill?

(4) Massive Enforcement and Regulatory Oversight: Agencies like the former OFHEO and the SEC have been so stripped down and starved over the past decades that they simply had no power over a multi-trillion dollar market. First, we need to resurrect a similar law such as the Glass Steagall Act that was repealed by the Gramm-Leach-Biley Act in 1999. You can almost pinpoint the moment the stupid toxic CDO and CDS markets exploded:

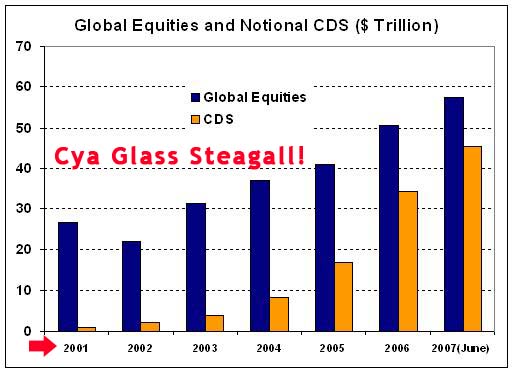

*Source:Â Sudden DebtÂ

For nearly an entire decade, this market went unregulated. Now that things are blowing up they don’t want to tell us where they will use the $700 billion and with utmost arrogance want to keep this market in the dark. They created their own nightmare. The reason for market transparency is that at any given time, you should be able to unload your assets and there will be a market to sell into. Those people that wanted deregulation got exactly that in a black and chaotic hole. Now they want to impose rules on the jungle of debt. With such a hidden world and no transparency, no one really knows what some of these assets are worth in the real world. Given the stunning amount of this out there, don’t you think the public has an obligation to have leaders explain what is going on before they start dumping their money into the abyss?

(5) Liquidation of Lenders: Finally, there are some pathetic lending institutions out there. They need to fail and the quicker the better. We are already seeing some of this. The big are eating the weak.  JP Morgan Chase eats up WaMu. Wachovia gets swallowed up by Citi. You get the point. The reason this needs to accelerate is once the market stabilizes, these institutions will once again inject liquidity. Yet this will be a slow process. Otherwise, more crap will hit the market. How so?

Well in the midst of all this insanity Wachovia was bought out by Citi in what is another government bailout. They won’t call it this but it is absolutely a bailout. First, Citi bought out Wachovia with the full knowledge that they will only absorb $42 billion in losses from the Wachovia mortgage portfolio. The problem? Wachovia with their smart buy move of uber toxic mortgage all-star Golden West has approximately a portfolio of $120 billion in pay option mortgages mostly here in California. Who will assume losses above and beyond the $42 billion? The FDIC. How much does the FDIC currently have? About $43 billion.

Please continue contacting your Representatives since this battle is not over. If they try anything new at least there are some good ideas that can be implemented:

Any idea is better than, “you can trust me with $700 billion. I’m from Goldman Sachs and we’re here to help.”

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

34 Responses to “Housing Bailout Bill Failure: Examining the Boondoggle Legislation and Populist Uprising against Wall Street. 5 Reason the Bill failed and 5 Easy to Implement Solutions that can be Used Today.”

The media ie news channels think hurricanes, OJ and this crisis as content. If you dont step back perspective is lost. The market dropped 7%, the drop on black monday was 22%. That would have been a 2400 point drop today.

This is awesome. Very well put together so that everyone can understand. Leaves no confusion……as Joe Friday would say, “The facts M’am, just the facts”. All facts presented here can be verified on Google.

It is a little long (11min) and goes pretty fast. But well worth the time to see. If it goes to fast, use the pause button to stop on each frame you want see it more fully.

Burning Down The House: What Caused Our Economic Crisis? V2

http://www.youtube.com/watch?v=NU6fuFrdCJY

Now go look at section 106 of the ‘‘Emergency Economic Stabilization Act of 2008’’ http://www.foxnews.com/projects/pdf/rescuebill_First_Draft.pdf .

It still wants to skim off 20% of the profits of each sale to fund this housing fiasco and ACORN. If you object to this, then write, email or call your Representative. Slice the pork out. You can make a difference. According to the vote today, many have.

how did your rep vote? http://clerk.house.gov/evs/2008/roll674.xml

Find your rep here: https://forms.house.gov/wyr/welcome.shtml

Find your Reps website here: http://www.house.gov/house/MemberWWW.shtml

Forward this on to all you know. Let the truth out.

Testify, good Doctor, testify!

An excellent summary of the motivations behind this debacle. I just love:

” All they kept saying was “if you don’t vote for this, ahhhh man, you don’t even want to know.†Great way to get people to vote.”

I could not have put it better myself! Shit, for a week or more, we were told that the end of the world was nigh if the Paulsen 3 pager didn’t immediately get accepted.

I am amazed and gratified that the American people have demonstrated that they do not believe this bullshit. Dr HB, I think you helped, and kudoes to you and everyone like you.

PS – I dole out things, I don’t “doll” them out……

Great stuff Doc. I plan to contact my representative again (he voted for the plan). I tried to cut and paste your plan into an e mail. However, they are apparently being overwhelmed by email traffic…so I’ll try later.

Beyond excellence.

Classic hostage situation, you do what I tell you or else! The public chose the or else option & is willing to take the ecconomic bullit knowing they’re going to take it any way, reguardless if there is a bailout or not.

On Countdown with Keeth Oberman on MSNBC last night there was an interview with an ecconomic advisor to O’bomma who stated the problem was that the bailout was not marketed properly to the public, wich is why it failed. Holy shit! the news media is trying to sell this like Best Buy sells big screen TV’s.

The public is saying NO bailout, infact some have gone a step further by saying if the whole system falls apart don’t fix it. Just let it die & we’ll start fresh.

As for me, I cant support any bailout reguardless of the consiquenses to the econemy, because some how, some way those who created this mess will end up benefitting from it while leaving the rest of us behind to clean up a bigger mess later.

I got a letter from Wells Fargo (my current mortgage holder) offering me a HELOC (actually, practically begging me to borrow), and I took off a day last week to go to the zoo, and there were people peddling applications for credit cards (I didn’t want to be bothered, but now I wish I had found out who was solicting credit card custmoers on the street).

Maybe there is still a ton of credit available – to PEOPLE WHO CAN PAY BACK THEIR LOANS!!!

O, and excellent post as always!

While I don’t rule out the idea of bankruptcy judges modifying mortgages, would it be fair then to make anyone who walks away from their home a bankrupt? That is, you stop paying and you are automatically in bankruptcy court where your assets are opened up and distributed. No more “I guess this loan is inconvenient now” walking away allowed. You want to stay in your house you have two courses of action: pay your debt or you petition for bankruptcy. Further, maybe I’m simple minded but how does a $400K current house value make a $600K loan “craptastic”? Would you expect the borrower to pay the loan if the value were $600K? This is an ethics issue, not a financial one. And it seems to me that California, in particular, would like the rest of the nation to fork over to make up for its collective lack of ethics in the area of paying off contracted debt obligations.

The flip side of bankruptcy modification of loans is the walk away phenomena. Would it be fair to accept bankruptcy modification if the walk away were treated as a defacto bankruptcy petition? That is, no more “I guess this loan is inconvenient” and walking away with money in the bank, stocks in the portfolio, boats in the driveway, etc. For example, with the $600K “craptastic” loan, the $400K house value is no longer is the issue at all: it all boils down to do you have the income to service the $600K? The judge may well look at everything and decide that the borrower can handle $570K. Your loan is still deep underwater, but the court determined that you can pay for it and by God you will. Is that the deal you want?

Hey JB and all:

If you’re talking about Drier I had the same problem. I just resubmitted and then I got a confirmation of receipt. Same thing happened with boxer and feinstein.

I just think they don’t want to hear it and that we’ll just get discouraged give up and go away if they reject it the first time. Probably a lot of people do-

Nice article. Long time reader here, and I swear sometimes that some of the housing blogs have already seen the future 2 years in advance.

But alas, one way or another this bailout plan will pass. I’ve already contacted my representative(who voted YES on it), and my two state senators to think about this seriously. Politicking and fear mongering will prevail and this will pass. Our constitutional republic is crumbling away before our very eyes.

Here’s one of the clearest and most insightful graphs you’re likely to ever see on this topic:

http://graphjam.files.wordpress.com/2008/09/700bil.gif

YES YES YES it is absolutely fair to make anyone who walks away from a mortgage either pay it or bankrupt. Whence comes the notion that you shouldn’t have to pay what you agreed to pay just because your house has dropped in value? This is the mentality that is driving demands for bailouts.

I owe some CC debt, I regret to admit. Shall I be permitted to default without penalty just because the crap I bought is worth less than what I paid? Shall you default on your car loan just because the thing was worth 40% less than you paid the day you drove it off the dealer’s lot?

If you can pay, you should have to pay, no matter how your house has deteriorated in market value.

The Bush/Paulson stinking arrogance is what undid them. The people have risen up against the would-be dictatorship!

Here’s an interesting snippet from an LA Times article:

http://www.latimes.com/news/opinion/commentary/la-oe-goldberg30-2008sep30,0,2477888.column

”

When a reporter for Forbes magazine asked a Treasury spokesman last week why Congress had to lay out $700 billion, the answer came back: “It’s not based on any particular data point.” Rather: “We just wanted to choose a really large number.”

There’s a confidence builder.

”

Keep up the good work,

Jeff

You are SO right on… I think this is the finest discussion I have seen on the matter.

Kudos and … where do I sign?

Once a rational and measured examination of the actual amount required to help ameliorate the crisis has been conducted, here are a few alternative sources of funding:

1. END the Iraq war and save $128 BILLION PER MONTH (abcnews.go.com/International/wireStory?id=4418698 -)

2. REPEAL Bushie’s tax cuts for the filthy rich and make THEM pay for the bailout

3. Legalize marijuana and use the tax revenue from sales to finance the bailout

4. Tax churches that are actively politically involved in violation of their IRS tax exempt status

5. Surcharge executives of failed banks and financial institutions to be helped by the bailout

6. If taxpayers are to borrow the money, rather than GIVE it to Wall Street, LOAN it to Wall Street WITH INTEREST.

The House is limiting e-mails from the public to prevent its websites from crashing due to the enormous amount of mail being submitted on the financial bailout bill.

As a result, some constituents may get a ‘try back at a later time’ response if they use the House website to e-mail their lawmakers about the bill defeated in the House on Monday in a 205-228 vote.

“We were trying to figure out a way that the House.gov website wouldn’t completely crash,†said Jeff Ventura, a spokesman for the Chief Administrative Office (CAO), which oversees the upkeep of the House website and member e-mail services.

That’s the OFFICIAL explanation…

I still stand by my original hypothesis…

And the DJIA’s up 485 points/4.68 percent today. Third biggest point gain ever, everyone’s reporting. So all yesterday’s Awful Terrible No-Good Catastrophic Meltdowny Crisis was…speculators cashing out on recent gains. Not the sky falling after all.

~

But the newsmedia report the fall as panic about no bailout, and the uptick as optimism about the bailout.

~

There are some saner voices:

http://www.marketwatch.com/news/story/struggling-industries-want-piece-bailout/story.aspx

~

On page 2, it reports that the automakers are tincupping for $50 billion. So they can build fuel-efficient cars, they say. Which is really odd coz yesterday I read that, now that gas is so incredibly cheap (???), or anyway, people have gotten used to $4+ a gallon, they’re rolling out the new SUVs and trucks. John McCain filmed a campaign ad in Michigan talking about the importance of getting Americans back into 3 gallon per mile steel behemoths again. Like a Rock, yep, that’s the brains behind that scheme.

~

Lennar and Toll Brothers are also dialling for pork dollars. Lennar wants $20,000 in tax credits for each house they build. We’re already clogged up the nostrils with inventory…and these nitwits want welfare so they can suffocate us entirely. So now we give the builders pork to add to the oversupply of housing, AND we give the financiers pork to get more people into mortgages they can’t afford? When the real problem is: it’s the income, stupid. We need to employ people in productivity that doesn’t involve building houses we can’t need and people can’t afford.

~

Blaming the Community Reinvestment Act and Clinton for the excesses of Wall Street these past 28 years is a partialistic view that seeks to substitute politics for economics. We can cite as many examples “going the other way” as well.

~

Clinton, you might recall, had a Republican Congress.

~

Prior to his terms, Republicans led the charge to pass the Depository Institutions Deregulation and Monetary Control Act (1980), which weakened Glass-Steagall, then paved the way for the S&L fiasco. It took away the Fed’s powers to do things like regulate savings account rates, which led to the shift from savings accounts to money market funds.

~

It was Phil Gramm and James Leach–both Republicans–who introduced the repeal of the Glass-Steagall Act.

http://www.occ.treas.gov/ftp/workpaper/wp2000-5.pdf

~

Republicans were the majority in the ratification of NAFTA, which sent so many American jobs abroad and undercut unions’ efforts to protect wages.

~

And on and on and on, so let’s not make this discussion stupid by claiming that one party is tsatan and the other is SuperFluffyBunny. That kind of Karl Rovian polarization needs to be taken out behind the barn and shot in its empty head. We are all in this together, no matter who we did or didn’t vote for. This was class war, not politics, though politicians generally side with the moneyed over the masses.

~

The House will entertain, vote for, and approve another bailout bill, probably Thursday. My read of the situation is that a) those facing tough elections listened to their constituents and voted Nay, b) there is more gloryholing than we can imagine going on at this moment as Bush/Cheney/Pelosi/Paulson et al. try to squeeze another 20 Republicrats to change their vote, and c) we can expect a bailout of some form, the question is, what form.

~

The panic got reined in by Americans mobilizing. The real issue is sustainable and well paying jobs, and rebuilding this nation’s infrastructure and public commons. I plan to keep my iota of pressure on my reps.

~

I disagree with DHB about the “loss of 1.2 trillion in stock market wealth.” This loss was in price, not in value. Part of the reason financial institutions are playing Manhattan Hold ‘Em with each other is that they don’t KNOW anymore what stocks and companies are actually worth! Valuations have been so disrupted by mark-to-myth accounting and inflated prices that NOBODY KNOWS! You want to borrow a billion from me, and I want to borrow a billion from Kim or Laura or Andy or JB, and they want to borrow a billion from Erik K or Sean…and we’re wondering who’s the sucker at the table, and who’s the liar…when we all suspect we all are, because we know our balance sheets are as gaseous as a Wisconsin cow pasture.

~

rose

Has anyone heard anything about the DTCC? I guess they own 99% of all securities – a technicality for convenience sake, but noe the less a mechanism for Fascism:

http://yourmortgageoryourlife.wordpress.com/2008/09/30/who-really-owns-your-money-part-one-the-depository-trust-clearing-corporation/

Check it out.

Can you believe what the latest proposal is? Our brilliant public servants have decided to try to ram the bill through AGAIN, this time including a clause for a TAX CUT.

HOW DOES THIS MAKE THIS BILL BETTER?!?!

I understand that they’re trying to get the Republicans to defect to the other side by offering that amazing carrot, “the tax cut”, but how stupid are they? They asked for $700 billion, we said “we can’t afford that”. Now they’re saying “Give us $700 billion, but we promise that we’ll charge you less”. HUH? Do they really think that we’re stupid enough to believe that? Who else is going to pay for it? I’ll give you a hint: it won’t be Wall Street. They’re the ones we’re giving money TO.

Once again, our representatives have their gaze firmly planted on ground, not up at the horizon.

All the representatives from Arizona voted no – Republican and Democrat alike. Folks here are ticked and telling their Congressman that they had better REPRESENT them if they want to keep that cushy job.

Fight the Wall Street Bailout

This bailout is nothing but bad news. There is no real crisis, the market sell of is a result of fear mongering by President Bush

The bill allows for foreign banks to dump all of their bad assets into American banks, who can in turn sell the debt to the treasury.

THE AMERICAN PEOPLE SHOULD NOT BE PUT ON THE HOOK FOR WALL STREET, AND ESPECIALLY NOT FOR COMMUNIST NATIONS LIKE CHINA!

Stoopid jackasses now want to raise the FDIC limits to $250K.

Great idea since FDIC doesn’t have enough money to cover its obligations as it stands: why not raise our obligations almost threefold???

I’m not quite so sure that it was Incredible at all that the vote in the house by California representatives was extraordinarily close, after all from what Representatives were stating to the press all day Sunday, it seemed like much of the voting had already been carefully agreed upon and was set to be orchestrated in such a way as to not make anyone party or single group look to have pushed it through (just incase it didn’t work).

Unfortunately for them (lucky for us) Pelosi derailed the whole thing when she just couldn’t resist spilling out her diatribe to the House on how Bush and the Republicans are all to blame for the crisis.

Near as I can tell from listening to the Representatives themselves over the weekend the vote was evidentially planned and orchestrated to be cast and narrowly passed by letting key representatives and friends of the Speaker vote No as well as allowing those that could not afford to take the blame somewhere down the line in their local districts to opt out and vote No as well.

With California being one of the major housing crisis contributors, I could easily see California’s representatives purposefully splitting their votes so as not to appear to have had any effect on the bill one way or another in order to protect themselves.

Very soon in November, it is our turn to get justice and democracy by casting our vote.

Let’s vote those Wall Street buddies out of their DC office, please.

Read more at my website:

George, Be a Good Boy! http://activerain.com/blogsview/716998/George-Be-a-Good

What’s Next After No Bush Trash “Bailout” Plan!!! http://activerain.com/blogsview/714627/What-s-Next-After

Here’s another handy link :

http://www.stopthehousingbailout.com/

Steve is right the bill is BACK ALREADY. Now it’s in the Senate (of course, it does still have to get through the House again eventually):

http://www.nytimes.com/2008/10/01/business/01bailout.html?_r=2&ref=&oref=slogin&oref=slogin

With a tax cut. Even worse. Let’s increase the national debt by EVEN MORE than 700 billion, might as well eat drink and be merry!

Of course the Wall Street losses were all just based on fear mongering. In the short run (and I’m sympathetic to theories about this being the case in the long run also 🙂 ) Wall Street is governed by pure irrationality. But the media propaganda depends on people not realizing this and pretending the verdict of Wall Street really matters.

In truth, if someone so much as says the economy is bad Wall Street tanks. And so of course it works, it’s psychology, not economic fundementals (they may be bad also, but the bill doesn’t fix that).

FDIC has is also covering any losses over $42 billion that Citigroup has to eat after taking over Wachovia. Wachovia has $300 billion in debt.

By putting the FDIC in a vulnerable position, the fed now has more leverage to get their $700 billion ransom.

Alert Alert Alert: McDonalds cant get credit for installing coffee bars to some restaurants. We should have passed the bill. Why God Why. Help us please. I have a friend who just got a job delivering dog food to peoples houses (Pet Chef) and I have another buddy that has a business that he will pick up your dogs crap (doggyduty.com). Tough times? Maybe society is taking a dump.

No seriously

can anybody explain why they’d want to increase the FDIC limits when from all indications they don’t have enough to cover the obligations they have @ $100k each depositor???

This was just sent to my three lovely “representatives”:

FDIC insures depositors against bank failures. It provides in its present state insurance for up to $100K each depositor.

The latest brilliant idea is to up the limits from $100K to $250K each depositor.

FDIC DOES NOT HAVE ENOUGH MONEY TO COVER THE DEPOSITS IT ALREADY HAS AND NOW THE PLAN IS TO INCREASE ITS (WHICH MEANS OUR) OBLIGATIONS AND EXPOSURE ALMOST THREEFOLD.

Check out the amount of money FDIC actually has versus how much it will have to pay if only a few more banks fail. It doesn’t even have 1/10th of what it could need. And many more banks WILL fail guaranteed.

This seems like just another back door way to trick us into bailing out big money players.

Don’t let this happen to us!

Our representatives are not supposed to be our enemies

*You’re welcome to copy and paste should that inspire you to actually make contacting them happen-*

What I’m reading about “Plan B” makes me nauseous.

~

Nauseous like the Spanish flu…vs. nauseous like gagging up one’s own bloody entrails from “the Ebola virus” of credit default swaps.

~

CDSs–next financial crisis

http://money.cnn.com/2008/09/30/magazines/fortune/varchaver_derivatives_short.fortune/index.htm

~

rose

Dr. HB

Is it possible that the “bailout” is nothing more than a smokescreen designed to buy time to forestall the innevitable? It seems that regardless of what way the vote goes on the bailout, the fundamental problems in the economy, equity markets, and credit markets remain. Might this not be nothing more than a distraction, a way to put the credit crisis in a temporary state of suspended animation? While everyone debates whether or not the bill is good or should be revised, Rome is burning. The water this bill might throw on the fire doesn’t even slow it down, much less extinguish it. I think this is a distraction. The market could not content with the crisis so the market threw the crisis over to congress, knowing that congress could do nothing aside from igniting a national debate about something (the bailout) that appears important but is in fact impotent in the face of the great credit unwind. It appears to be the kind of tactic a magician on stage might employ… create a distraction in order to divert attention in order to pull the strings and create the illusion. Except in this case, there are no strings left to pull. The markets (market makers) are hoping that with the time purchased in this pointless debate, they may find one last string to pull to complete the illusion. The problem is, there are no strings left to pull and so the distraction becomes the show.

Anyway, here’s a big stinker for you; and I need some quick investigative help and loud questions to be asked. This should be a factor in our Senator’s decisions today regarding the bail out deal. Here’s what I just e-mailed and faxed to Senators; including John Ensign, as seperate e-mails (This is Ensign’s copy) : URGENT**** Per your Vegas office, I am sending you the web address to the website for the Las Vegas Real Estate Brokerage tied to Frank Raines: http://prosofrealty.com/ Also, Google Farrah Gray and Frank Raines, and Ronald Branch and Frank Raines for more links between them. I believe the evidence I am collecting shows that Frank Raines was funneling the Fannie and Freddie foreclosures to this group to list for resale. I talked to a broker who worked there briefly. He heard their names mentioned, but more importantly; the commissions paid to the ‘brokerage’ were maybe 3% of the sales price, but the sales person or selling broker only got maybe $1,500 or less. The brokerage was then funneling the money back to the owner/investors. There is a shell company in the middle, but I am picking up ties to Raines all along the path. One thing I am, is persistent. Don’t vote yes on this bill today, Senator Ensign. There is a tie between Frank Raines and this company, and it will blow up this topic shortly. Any one of our politicians who votes yes to this rescue bill today is going to look as though they didn’t look hard enough at the details before they voted. You can’t vote on this without knowing the facts. You need to say that you are not voting for a 700 Billion dollar or more bill to taxpayers without all the information. Also, I talked to a broker who was working there. He said that basically, this gave Freddie and Fannie execs a reason to foreclose, secretly. They made more money this way, taking these houses back and selling them via these shell brokerage groups; rather than working with any borrowers. This bail out bill profits these lenders even more. Many were complicit. I’ve had the misfortune of looking some of these people in the eye across the negotiating table in the last few years. They did this on purpose. I can promise you, my tax dollars won’t pay for this. I don’t care if I have to cut my income by 50%, because it’ll only mean a reduced net of 10%, I pay so much in taxes. But, at least I know I’m not working to pay off their FRAUD. I can get a home loan today, my kid just got student loans 30 days ago, and this is a lie about the credit crisis. If someone is creditworthy, can show the ability to financially handle the repayment, and has a downpayment, they can borrow. I’m not handing anyone a fresh shovel; least of all the people who got us into this in the first place. And, Main Street has been paying for this for two years. We’ve already figured out how to live beneath our means, save, not use credit, and survive. I’m not buying that these poor, poor fraudsters need me to give them $700 billion.

Leave a Reply