Housing industry would like you to believe that you are too financially naïve to own a home: The psychology of pushing people to buy in the current housing market.

There is a running meme in the housing industry and it revolves around intelligence and home buying. The subtle undertone is that those that own real estate are somehow much more financially savvy because they own property. I’m surprised we don’t see this on LinkedIn as “…and also intelligent homeowner.†On paper, at least nationwide, homeowners do have a higher net worth than renters. Yet this is nationwide and also doesn’t go into the details that most of the net worth is locked in housing which does not throw off income. So are all those young tech workers in San Francisco that currently rent financially ignorant? That is the issue when using nationwide figures to extrapolate onto niche markets. It also doesn’t factor in the reality that for many, buying today at current prices would equate to self-imposing a financial albatross around your neck for many years. That of course assumes you can even buy to begin with. And keep in mind the recent economic upturn hasn’t been all that great. The recent election was driven by frustration regarding the economy. That is how you explain the cognitive dissonance of Republicans “winning†yet many states enacting higher minimum wages. Huh? These things speak to the underlying tone of economic frustration Americans are facing. Then we have the FHFA trying to make it easier for people to get into further debt by making lending standards weaker. Ultimately you have sales collapsing and people on the fence because buying a crap shack today would financially cripple many households for years to come.

Even prime areas have a ceiling depending on the quality of a home

I’m noticing more price cuts in highly selective areas. What you see is good quality homes still fetching solid prices but delusional folks asking for dream prices facing some slowdown. Take for example the city of Arcadia. This is a target area for foreign investors and high income professional families.

This home is your typical entry starter home that is losing traction:

2 beds, 1 bath, 1,032 square feet

321 Laurel Ave, Arcadia, CA 91006

“Charming 2 bedroom home with Bay windows in dining room and bedroom sits on a lovely street with trees. Fireplace in Living Room. Upgraded electrical box. New Sewer line. Some new windows, Central air, New exterior paint, seamless gutters and new roof in 2012. Walking distance to Foothill. It has North Arcadia’s best schools Highland Oaks Elementary School, Foothills Middle School and Arcadia High School.â€

Great! You’ll get a new sewer line which I’m sure is important since you want to flush with confidence. There is absolutely nothing special here. 1,032 square feet with 2 bedrooms and 1 bath. This place will get cramped fast if a young couple moves in and plans on having a kid. Of course this is when the property ladder game begins and you better hope appreciation keeps moving up to build up that delicious equity. Let us look at sales history here:

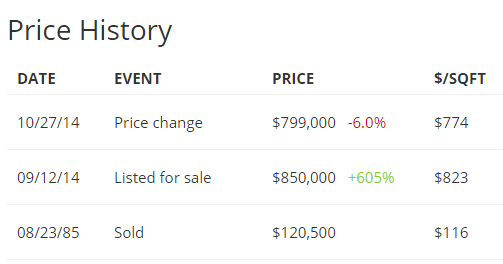

This home recently saw a $51,000 price cut. It was originally listed at $850,000. This is the kind of nonsense we are seeing. Say you bought in September for $850,000. Does $51,000 mean anything to you? 5 percent of $799,000 is $39,950. So that’ll cover the basic down payment right there. People are just lusting that suckers will bite at any price. The rental estimate on this place is $2,400. 20 percent down on this place would require $159,800. Even after the 20 percent down payment, you will take on a mortgage of $639,200.

The folks that bought in 1985 are doing great. They are paying taxes at a rate of $190,810 per year ($2,284 total for the year). Say you buy. Your taxes will be over $8,000 per year, nearly four times the rate of the current homeowners.

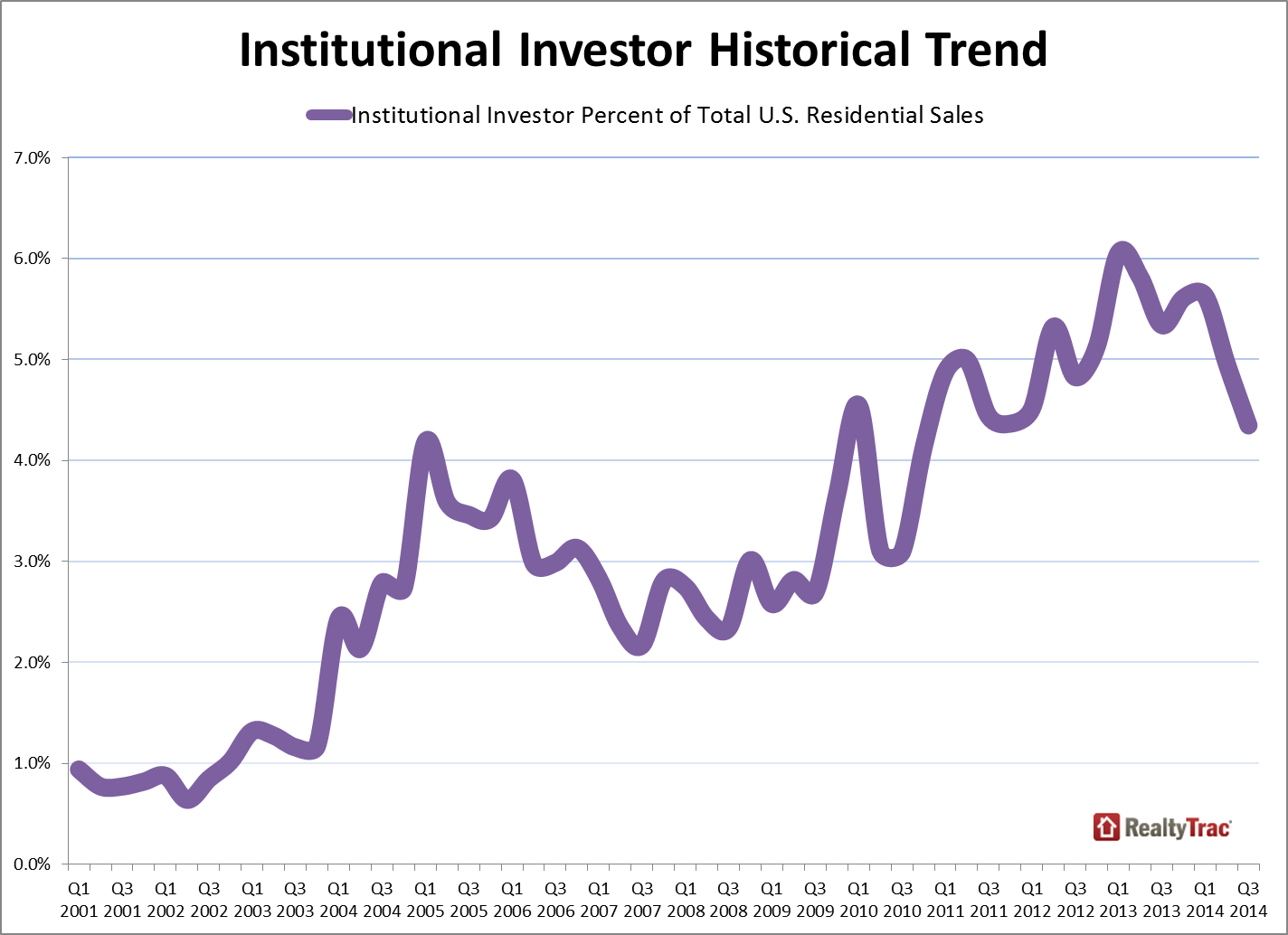

Institutional investors have pulled back from the market for most of 2014:

Source:Â RealtyTrac

Institutional buying is now at a four year low. If deals are so great, why are they pulling back when they are flush with wealth from a record stock market? This is perfect timing to handoff these high priced properties to debt slaves. The reason sales are so weak is because prices simply don’t make sense for current household budgets and prices were pushed up higher by voracious institutional buying. Now regular buyers need to step up but they can only do so if the FHFA opens up its purse again under its new and rebranded name.

You also have this notion that people stay put for long durations (they do not). People want to capitalize on fast equity to move on up the property ladder game. And those that recently bought have to sell to unlock those gains. As many investors know, stock gains are yours when you unload your position or in housing with a check after escrow closes.

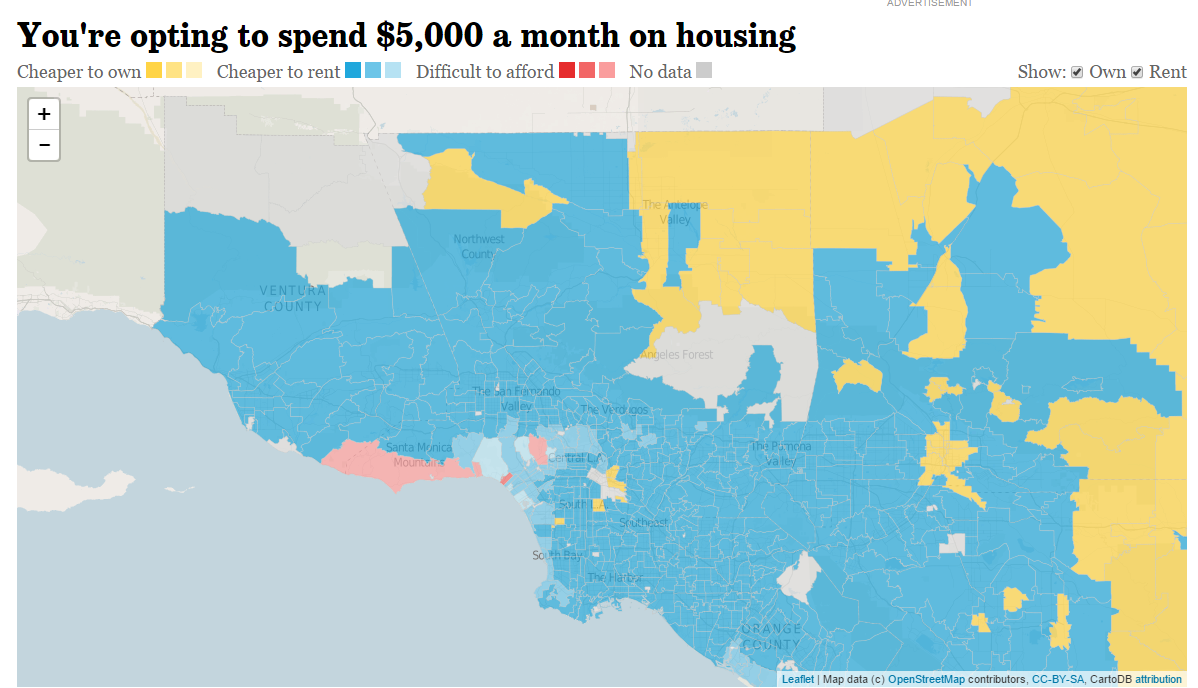

The L.A. Times has an interesting rent versus own map overlay. I put in the following variables:

Household income:Â Â Â Â Â Â Â Â $150,000

Percent of income on housing:Â 40%

Down payment:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $100,000

Mortgage term:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 30

This will cover many households. Take a look what we get:

Unless you are buying in the Inland Empire, you are likely stretching your budget. Then again as we have seen with a few studies L.A./OC are the most overpriced regions in the nation and people wallow in massive debt. All hat and no cattle and even that hat is financed with low interest rate debt.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

56 Responses to “Housing industry would like you to believe that you are too financially naïve to own a home: The psychology of pushing people to buy in the current housing market.”

This Administration did everything they could to artificially prop up the housing market. Now that the midterm elections are over they can allow housing to tank and blame it on both Houses.

Trudedat True. Housing TO Tank Hard in 2014!!

Housing to flatline or gradually trend up in nominal terms as inflation edges up! http://www.nytimes.com/2014/11/08/upshot/evidence-for-optimism-in-the-jobs-report-.html?abt=0002&abg=0

hahahahaha…

hahahahahahahaha…

hahahahahahahahahahahahaha…..

Housing only goes up, never down, right?

Nominal: http://en.wikipedia.org/wiki/Real_versus_nominal_value_%28economics%29

Who is going to buy these homes?

The musical chairs have been put away, the party guests have gone home, and there’s nobody left to play.

I heard Chinese money is buying up crapshacks in Arcadia and turning them into McMansions. Businessweek article a couple weeks ago.

So you what do you suggest people who aren’t willing to move away from the california coast do? Should they rent or stretch to buy?

Curious what your definition of being ‘away’ from the California coast is? 1 mile? 5 miles? 10 miles? 50 miles?

When I was home searching in 2012, there were a few places where houses were available for under $500K and 15 minute drive to the beach. Either parts of Gardena, Lawndale, (southbay) or Baldwin Vista (adjacent to Culver City). I bought a house in Baldwin Vista which is about 7 miles in actual driving from the beach. This will be a neighborhood to watch if you think home prices will crash again, but homes in Culver City all the way to the coast will never see decent prices again. And mid cities LA has too many rough neighborhoods.

Never! …says the crystal ball…

“All hat and no cattle”, boy sounds like you been to the Republic of Texas. We have that in Dallas, probably the city most similar to the westside. I left that place years ago, when the wells came in. I don’t need that scene. I live in Kerrville and live the life I like and don’t care what anybody says, including the spoiled daughter. Sort of like the old Venice beach, I hear.

One man’s crapshack is another man’s palace.

There are plenty of places where it makes sense to buy, but Arcadia isn’t one of them. This house, which is about two blocks from Trader Joe’s, and a short bike ride to the university and to Whole Foods, has finally gone under contract after being on the market for months. The seller is not only lowering the price, but he is also building the buyers a new two car garage. The historic house is renovated to the nines:

http://www.zillow.com/homedetails/4404-Park-Ave-Wilmington-NC-28403/103765541_zpid/

Perhaps, if those who live on the California coast want to buy viable, investment grade real estate, that they may choose to live in some day, they should look to buy somewhere other than the California coast (where the surf is still decent). After all, spending more than $500,000 on run-of-the-mill, 1,000 sf 1940’s factory worker’s house could someday be construed the act of committing financial suicide.

” homeowners do have a higher net worth than renters. ”

“Net worth” is an interesting term: Capital which loses value/generates maintenance cost isn’t generally classified as “worth” at all, but loss. A house, if not maintained, drops to the lot value or below in 30 years. Same time it takes to pay it.

One thing is sure: it’s better to own a million generating 5% net interest every year than a house “worth” a million, generating nothing but taxes and maintenance cost (or losing value at least 5%/year if not maintained).

House is a good investment only if prices go up and there’s someone to sell it to. To me it looks that prices may still go up but finding a greater fool will be very hard and an investment you can’t sell with profit isn’t an investment: It’s a way to lose money.

Second best thing after making money is not to lose it. Some people put not losing it to first place.

“it’s better to own a million generating 5% net interest every year than a house “worth†a million,”

Please tell me where I can be guaranteed 5% on my money, because my banks pay me less than a quarter of a percent on my savings.

Good stocks

Please let me know of a fundamentally sound economy where a “modest” house can be worth a million and you can’t generate 5% interest relatively safely. This is the ignored paradox.

I got a 21% return in 2 weeks buying 3x ultra S&P ETF when the market dipped a few weeks ago. I know that stocks aren’t guaranteed, but after every “crash”‘in the last few years the market has bounced back to the previous level quickly. I wish I had been buying these ultra etfs all along, but I will be moving forward.

“House is a good investment only if prices go up and there’s someone to sell it to.”

Are we talking about pure investment properties here? Owning a primary residence has and always will be part of a diversified portfolio. Go ask any financial advisor if you should stay in your rental and go “all in” in the stock market. Shelter is a necessity so you will pay in one form (rent or own) regardless. Owning real estate can be an excellent investment due to tax benefits and it being a highly leveraged tangible asset.

Regarding land values, I don’t need to tell you that the majority of value of any desirable socal RE is the LAND, the structure is worth a fraction of the land. This 800K Arcadia crap box might not be a bad deal for somebody who has future expansion plans. Adding a bathroom and additional square footage could be a good investment in this neighborhood.

Just my 2 cents of course. 🙂

And Cap’n Crunch is a part of this complete breakfast.

Major emphasis on the **can be** for tax benefits and leverage.

Tax benefits depend on each filer’s situation so it’s not an automatic given and you can’t count on those benefits not changing…go ahead and ask anyone who used to deduct credit card interest many moons ago…so yeah same plot different title. As long as the MI deduction is around in its current form I’d rather buy at a lower price with a higher relative rate rather than the way it is today with higher price and lower relative rate because the proportion of the subsidy relative to the whole is better. Once you buy in at a higher price with a lower relative rate there’s hardly any room to move lower on the rate side unless one is to think there will become some form of direct subsidy for simply holding a mortgage. In the lower price to higher relative rate scenario there’s much more potential movement to the down side on the rate…just ask any of us who have done just that in the past couple of decades.

As for leverage that comes at a cost and is only as good as you can arbitrage the differental after all transactions have settled which is easier said than done.

As long as you have lived in your primary residence at a minimum the last 2 years and you then decide to sell, the first 250K profit (if single) and 500K profit (if married) is tax free. The last I checked, this is available to everyone regardless of filing status. There aren’t too many investments that compare to this from a tax perspective. Correct me if I am wrong.

I was referring to the MI deduction. The capital gains exclusion is often overrated. One can obtain a true benefit from it only if there’s a net profit from the sale and a replacement primary residence is obtained at a lower cost level (after factoring for any material differences between the two) or there is no replacement. I don’t believe that either of those are a common scenario for most people.

This exclusion rule has also changed over the years so it’s difficult to count on it for long term positioning.

@A

You are correct that tax rules regarding housing have changed over the years. Until they change again, this is the best info we have.

The MID is a very powerful tool if you aren’t in the ~150K plus incomes where the tax deduction is gradually eaten away by the AMT. Could this be another reason why sub ~150K incomes lever themselves up when buying a house…this is most of LA (obviously not the prime areas).

Regarding capital gains exclusion when selling a house. The law was changed in 1997 to favor homeowners in a big way. Like I said, if you have lived in a primary residence at minimum the last two years, the first 250k profit (if single) and 500K profit (if married) is TAX FREE. There are no restrictions on using the profit to repurchase a house. This money goes into your pocket TAX FREE and there is no limit to how many times this can be done.

Until tax laws regarding housing become less friendly towards owners, expect the shenanigans to continue. When such generous tax benefits are placed upon a necessity (shelter), there will be much manipulation and irrational behavior.

Just my two cents of course. 🙂

I wouldn’t consider the MID a very powerful tool these days as the low rates of the past few years have taken a lot of wind out of its sails because the standard deduction ends up being of greater benefit for more people than it was when rates were higher…that is completely aside from the AMT for high income earners scenario.

As for the capital gains exclusion the TAX FREE part matters if you arbitraged the difference between the house you sold and what you ended up with afterwards. That is not a common scenario so we can put TAX FREE in bold and all caps until the cows come home but that doesn’t change the devil in the details and no it’s not really as generous as you characterize it to be. This is precisely because we’re dealing with shelter as a necessity. You don’t profit until you sell and you need another place to live. If you profit on a sale and replace with the same thing at the same price level, you haven’t truly realized a gain. The only thing the capital gains exclusion does for you in this situation is keep your transaction costs down. So yeah, it’s nice that you’re not getting screwed on the taxes but that’s not generous, that’s simply fair.

The only way to realize a gain is to sell at a profit and then buy a replacement (adjusting for any differences in kind) for less or never replace. That’s not common. Most people don’t sell to never buy again and most people also don’t sell high and immediately buy the same thing low unless they move to a different market. Even if they move to a different market there’s normally something given up which impacts the net value of said profit.

There really ought to be a “fix” with the current property tax structure. Perhaps it should be a regressive tax?

Classic sales tactic. Don’t forget the fact that renters in China can’t even get a date… Sex sells… I guess…

Hi What? 🙂

http://www.thedailymash.co.uk/news/society/people-who-dont-buy-a-house-will-never-be-happy-2013082178832

Wow. That little blob of orange in the sea of blue, is San Bernardino and Colton. Very, very few neighborhoods in that area are livable (by middle class standards).

fwiw, there are a couple nice areas around the San Bern country club, and the University.

Flippers are currently getting flushed out of this market, with many running for the exits. Let’s see when the Chinese exit the market. Any updates on the Chinese buyers clubs/real estate tour bused in places like Arcadia? Methinks the Chinese of the 201x might just become the Japanese of the 198x when it comes to California Real Estate .

Thanks for the excellent article, Doctor!

I don’t expect the Chinese to exit the RE market anytime soon. They’re not flippers. They didn’t buy for profit, but for wealth preservation.

The Chinese (and many foreign nationals) buy American RE as a place to “hold” their wealth. As a means of preventing their home governments from confiscating that wealth.

I don’t think the Chinese are too concerned with whether their SoCal homes go up or down 20%. Losing 20% value is better than having the Communists confiscate 100%.

I know whereof I speak. I know the mentality. The Communists confiscated much of my grandparents property in Eastern Europe.

In the 1970s, my father (by then living in New York) made a lot of money helping wealthy Thais and Indians move their wealth into American RE. It was the era of the fall of Vietnam, Laos, and Cambodia, and wealthy South Asians were genuinely worried about a Communist domino effect reaching their countries.

So I know the thinking of foreigners trying to move their wealth into American safe havens.

We keep getting told by everyone but the actual Chinese buyers as to why they are buying. There’s yet to be any solid evidence that some significant amount of these buyers are not making shrewd speculative plays. I could be wrong or I could be right on this but something about it doesn’t smell right.

Well, this happened in the 90’s with a lot of Taiwanese students and wealthy people coming to California. A lot of them overpaid for rents and housing like crazy. Eventually it subsided, as did the Japanese buying frenzy of the 80’s.

Generally, people coming from other places to CA tend to overpay since they don’t really know the historic prices. New Yorkers are quite easy to rip off as are Asians since they’re used to paying so much more.

Even today, after 2 years of big price increases, you can still buy a home and have a lower PITI payment than rent is in central San Diego, if you will move about 1 hour away from the ocean. I am sure it is the same all along the CA coast. Property in that 30 minutes from the beach zone is pricey and the closer you get, the more it is. Makes me wonder why people pay it, as few ever go to the beach to justify the additional expense. I am trying to talk my oldest into buying in Temecula, but she would rather rent in San Diego. Whatever.

>> Makes me wonder why people pay it, as few ever go to the beach to justify the additional expense. <<

There are benefits to living near the ocean, even if you never go to the beach. The air is allegedly cleaner, less polluted.

And not as hot. During the summer, temps are often in the 70s along the coast, and rarely above the 80s. On those same days, temps in the valley can reach the 90s or 100s.

That’s the rub jim…most of southern cal is nothing all that special compared to a lot of other competing areas so there’s no point in paying a premium unless you’re near the beach. Even if you don’t use the beach you can feel like you’re keeping up with the Kardashians and get a bonus temperature moderation effect.

Exactly. To live in an LA suburb far from the beach, you pay insane prices. Makes no sense.

I am fascinated by the psychology of Californian’s, especially those who call So. Cal. home. As this article illustrates, except for the top 15% – 20% of households, living there is a toxic blend of financial suicide and forfeit of your future! Is it worth it? I sold a ocean view home out there earlier this year, but haven’t lived there for years. But, I was a frequent visitor and always was a little shocked and amazed that people seemed totally oblivious to common or financial sense!

I did a reality show for the Discovery Channel a few years back (I-Cavemen…possibly worth a watch) and out of the 10 folks on the show, 7 were aspiring actors/actresses. Super nice people, I still maintain contact with most of them, but I was kind of stunned by how most lived. 6-8 people crammed into a shitty apartment…but driving a leased 100K car/SUV what have you. The “keeping up with the Jones'” and status wheel is pretty amazing to observe from the outside. I see a lot of that spill over into all areas of life, including owning a home.

Yes, I knew an aspiring actress many years ago. Drove a new, red convertible sports car. I forget the make. When she wasn’t living with her parents, at age 30, she was sleeping on friends’ couches.

Don’t you worry Fennie and Freddie will offer 3% down to college graduates so they ca own a house and still pay their $30.000 student loan back!

Murica is always #1!

Inflation is a given. The FED will make sure that inflation happens. If you run the numbers, and you adjust for rent and for leverage, and for tax incentives, the coastal SoCal housing market has outperformed the equity market by a substantial amount. As long as the SoCal population growth continues, and the FED keeps cranking out inflation, coastal housing appreciation is a sure thing, over the long term. If you hope to retire when you hit your 60s, a coastal house is a must.

Because past performance is a guarantee of future results..right, jt?

Always!

Prices usually seem high, but most of the listings I’ve seen are bordering ridiculous. Renting at this time makes sense as it did in 1988-1993 and 20043-2008..

People who don’t buy a house will never be happy

21-08-13

According to new government statistics, anyone still renting their home past the age of about 39 is going to die alone and unloved, in the knowledge that they have failed on the most fundamental level.

continues: http://www.thedailymash.co.uk/news/society/people-who-dont-buy-a-house-will-never-be-happy-2013082178832

(satire/parody stories)

so what is wrong with the Chinese bringing back the dollars that we happily send to them. the way i see it they happily sell us crap for our dollars and then they come back to the USA and buy nice homes.now unless you have “skin” in the game with friends in wall street or government we will always be reaching for that “piece of the pie”.look,things have changed and not for the better.

I will use the L.A. Times chart to convince my renters that a 10% rent hike is very reasonable.

Ah the landlord life; Put down a small deposit and then get a conveyor belt of 9-to-5 sweatshop monkeys paying off the mortgage over the course of 30 years. Rinse and repeat. Easy.

And Fed who can be relied upon to crank out ‘inflation’ making your mortgage smaller all the while (stupid banks / gov not wanting to preserve buying power of money) whilst you also get continual house price inflation, and of course natural house price inflation… oh and the population growth as well meaning forever HPI. Stupid e-con-o-my. Some people need to be hit by the hardest house price crash of all time and wiped out their fantasy view of the world.

20% rent increase for you.

Brain of E.,

You make landlording seem so easy. It looks that you were never a landlord. If it would be as easy as you make it look, then everybody would become a landlord and strike it rich.

The reality of it is that most people becoming landlords lose money. There are lots of things you have to know and be aware of. I am not saying it can not be made profitable. It can be for those who know a lot about it. The state legislation also plays a big role in determining winners and losers.

And, don’t worry – there are landlords being hit by recesions all the time and “lose their shirt”. Then, others come in who believe that being a landlord is a sure path to riches (like you believe) and discover the hard way that most of the time it is a money pit. The cycle repeats itself. Like in all areas of life and in all businesses there are winners and losers even in landlording.

BoE, “continual price inflation” you say? Shall I take that to the bank? I had no idea you could see the future.

I’ll remind myself of that the next time I clear the gunk out of a renter’s dishwasher drain. I had no idea that landlords were such bad people. And here I thought I put my hard earned money into a tangible investment, rather than the casino aka Wall Street.

Brain, it’s true that over time there is an increasing amount of profit margin to be made on a rental, and while the Fed’s interventions have helped me to some degree as a landlord I tell ya, my costs don’t stay too far behind as the years go on and they do rise along with inflation. A house is a money pit and I think a lot of folks learn this the hard way. There’s almost no better way to find this out than being an honest landlord of a SFH. You can’t defer maintenance or forego certain things as you could if it were your own residence. You also don’t get the scalability benefits of a multi-unit. All that said I LOL when hearing and reading a lot of the things fellow homeowners who’ve never been a landlord come up with on how owning is a zero sum advantage over renting.

BofE is being sarcastic, get a grip.

Thanks Joe K – yes it was sarcasm. I was paraphrasing the ‘GOOD/EASY’ view from this recent landlord’s blog entry – although it is from a UK perspective – I imagine it is very similar for US landlords… not entirely stress free whatsoever.

_____

What You Should Know Before YOU Become A Landlord…

20 Oct 2014 / Buying & Investing in BTLs / 41 Comments

http://www.propertyinvestmentproject.co.uk/blog/become-landlord/

>Take it from an average landlord that’s been scratching around in the game for several years, being a landlord is actually a lot of hard work and it can be extremely exasperating, even for an energetic playboy such as myself. Not consistently hard, but periodically. But those periods are some of the worst I’ve experienced in a professional capacity, and believe me when I say they come around far too quickly and I’ve often been left feeling suicidal. The money definitely doesn’t come easy, and there are easier ways of making a lucrative living that’s attached with far less stress.<

I agree with you Flyover. xxx

Got Water!

$5000 per month seems a bit high; depending on assumptions, it could range from the high $800K range to over $1M. If you set the budget at $3.5K to $4K per month, then you’re looking at $650K – $750K range. What does the map look like for that? (That’s around what my DINK colleagues typically look for).

Leave a Reply