Rents and housing prices unaffordable to middle class in Los Angeles: The typical LA renter needs to earn $33 an hour just to afford a basic apartment.

Last year there was a report highlighting that LA and Orange County ranked number one in being the bubbliest housing markets in the US. The report essentially found that people in the area lagged in income relative to housing values compared to folks in New York or San Francisco and most in SoCal basically funneled a large portion of their net income into housing. LA and OC are also expensive to rent in. An article caught my eye stating that that the regular Angelino needed to make $33 an hour just to rent a basic apartment without eating Purina dog chow every night. This post came across my social media feed and I dug through the comments. I was impressed by how many people posted something along the lines of “me and my roommates split the rent in X area for an apartment†and how many other comments from those out of the area were stunned by the basic cost of an apartment. Hey, SoCal is expensive. I think most reading here have the means to buy but rent or own their home outright. Short of you buying a home with a suitcase full of cold hard green cash, you either pay rent to a landlord or a mortgage payment to a bank. The 2.3 million adults living at home with parents are probably not fretting about housing prices or rents. The issue with SoCal is that people are treading on razor thin budgets just to get by even in rentals.

The rent is so…hey, at least the weather is awesome!

The article that caught my eye had some interesting data points:

“(SCPR) You need to earn at least $33 an hour — $68,640 a year — to be able to afford the average apartment in Los Angeles County, according to Matt Schwartz, president and chief executive of the California Housing Partnership, which advocates for affordable housing.â€

I should remind you that most households in LA County rent. That is simply a fact based on Census household data. And most people don’t make $33 an hour so you get many people tagging up with roommates. So is this the hidden group that is suddenly going to push the market up? No. You have folks thinking their local hood is going to be the next London but that is not likely. You still have to live in a $700,000 crap shack. You think having a Chipotle and a Whole Foods is suddenly going to push your home into the $1 million range? The big demand for the last few years has come from wealthy investors and big foreign money largely from China. Yet this money was surgically targeted at certain areas. You can still find good deals in other LA cities and I have shared a few with readers. If you truly believe in the “all of SoCal will gentrify†meme you will be on the ground floor for the next real estate renaissance.

The article goes on to say:

“That’s more than double the level of the highest minimum wage being proposed by Mayor Eric Garcetti, which he argued would make it easier for workers to afford to live here. “If we pass this, this will allow more people to live their American Dream here in L.A.,” Garcetti proclaimed when he announced his plan to raise the minimum wage to $13.25 by 2017.

The $33 an hour figure is based on the average L.A. County apartment rental price of $1,716 a month, from USC’s 2014 Casden Multifamily Forecast. An apartment is considered affordable when you spend no more than 30 percent of your paycheck on rent.â€

I hate to say it but the American Dream ain’t happening in LA on a mass scale. Even if you make $13.25 an hour good luck being able to afford a place in a decent area.

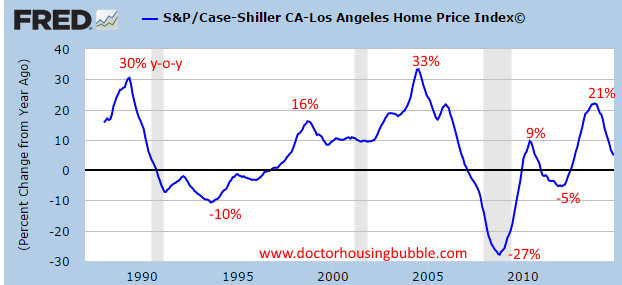

This is a boom and bust landscape. For better or worse, all of us are turned into real estate speculators. Just look at annual price changes for the Greater LA metro area over 25 years:

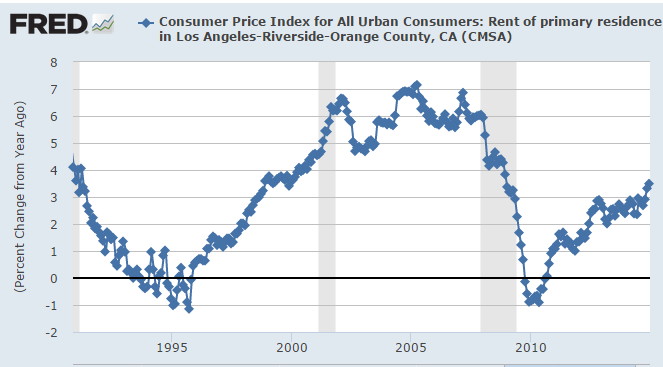

Boom and bust. Some on the fence, are making the calculus between renting in a good area with solid schools or buying a crap shack and rolling the dice that the area will gentrify quick enough before their offspring go off to schools with ratings unsuitable for a crappy Yelp restaurant. Rents rise at a more steady pace since they are paid via net income and don’t have the luxury of being leveraged by low interest rates. Take a look at annual changes in rents for the LA area:

You’ll notice that even in LA, rents do fall although it typically happens in a recession. I love some of the comments from these posts:

Buy now or be gentrified out forever! When I look at the boom and bust chart above, it always amazes me how quickly people forget about recent history. Over one million people lost their home to foreclosure in California in the last decade. That is massive given the number of actual homes bought. Yet the middle class is acting. California had a net loss of 221,325 residents between 2007 and 2013. 73% of those that left earned less than $50,000 per year. A large portion ended up in Texas.

Also, those arguing about rental parity make the convenient omission that you would need to have a sizable down payment to make it work. On that $700,000 crap shack, we are talking about $140,000 just for 20 percent down. Congrats! You now also carry a $560,000 mortgage on a stucco crapper. How do things look after 30 years if you stuck your down payment into a broad base market fund and added the difference between renting and buying? You are also locked into said market. There is mobility in renting and many in places like San Francisco value this (the vast majority in the area rent in an even more zany market). The calculus isn’t all that simple. One thing is certain and that is people are reluctant to move. People would rather eat Friskies out of their cat’s bowl before cashing in on their equity. Plus, many have children just waiting for the moment mom and dad take the long journey out of their HGTV upgraded home and pass their property over. “Hey dad! Time to gentrify out of this home.â€

The beauty of our dysfunctional economy is that you are not locked in to stay here. I know many people that were itching to buy a big McMansion so plunked down some dough and bought in the Inland Empire. They make a horrendous commute to work but at least their family gets to enjoy the place while they idle along the traffic congested freeways and do a number to their health. I also know people that pay crazy rents to live along the coast. But to think that prices in SoCal follow an expected pattern is nuts. The past shows us that we are in a boom and bust market. When people are doubling and tripling into apartments just to get by you know that all it would take is a minor recession to tilt things to the other side again.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information. Â

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

107 Responses to “Rents and housing prices unaffordable to middle class in Los Angeles: The typical LA renter needs to earn $33 an hour just to afford a basic apartment.”

The fundamental problem is jobs, as in the economy of So Cal is falling apart compared to what it was when the Baby Boomers were entering the work force. Aerospace? Gone. Manufacturing and big factories like Van Nuy GM Assembly, Pico Rivera Ford? Gone forever.

Today, it looks like a ghost town for good jobs in technology and manufacturing.

What’s also changed? Lots more illegal or legal but low skilled immigrants from south of the border. Schools filled with functionally illiterate high school kids who graduate with no job and social skills.

Out of control government spending and pension plans that are hopelessly underfunded.

In short, there’s no here here anymore. It’s just one big fantasyland living on its past glory. There are still jobs for the smart kids who graduate from UCLA and who get into a healthcare profession, but there are only a very small number of slots for med and dental students, PT, pharmacists and nurses. And you’ll have to compete with the smart (mainly Asian) kids–how good is your calculus and grades in chemistry?

In short, for the vast majority of young people in L.A., they ain’t much of a future. Once graduating with an engineering degree from UCLA, CSUN or Cal State Long Beach, you were guaranteed a job at Hughes, TRW, McDonald/Douglas or Allied Signal. Then you buy a home in Manhatten Beach or other South Bay city. Lots and lots of my friends did that.

Now, what are the choices?

Good luck, you’ll need it!

I couldn’t disagree with you any stronger than I do right now. You are clueless as to what’s going on in those job markets, I see the complete opposite. Those companies are hiring STEM and paying quite well. No they can not afford a $1 mil home in Manhattan Beach, but those are not starter locations anyway. The money is there though, as are the high tech jobs.

Did you not see the Playa Vista article in the Times this weekend? Silicon Beach is here.

Show me one ad for this mythical new college grad STEM job in L.A. and the pay, idiot. And then show me how STEM jobs there are in L.A.

Put up or shut up–you’ve been talking trash about all of these STEM jobs in So Cal yet you fail to offer any examples. And don’t even mention Google or Yahoo or whatever–those places hire hardly anyone in comparison to what the aerospace industry used to employ.

Unless all of my friends who are engineers and computer types are blind, the so-called STEM jobs in L.A. must be invisible because they can’t find them.

There are only TWO large pharma companies in L.A. and the biggest, Amgen, is going to cut 4,000 from their workforce this year (20% of workforce). So show me the money!

Aerospace has a severe shortage in engineering, and there is no ad. You get recruited.

I’m experienced, and you know nothing.

Hah, I am a senior manager at a defense company. I do really well (for aerospace). I feel sorry for the newer guys.

I know the guys you are talking about. One of the guys that works for me has a master’s degree, wife works, is 32 with 2 kids and is in an apartment in Torrance.

He can’t afford to buy anything because the prices are too high and he doesn’t have the downpayment. He’s also from outside of CA and the stickershock is killing him….he doesn’t want to be that housepoor.

I’ve told him if he wants to buy he just has to suck it up and do it, that things DON”T make sense here.

Most of the guys his age and to late thirties are not buying because of the cost.

Don’t forget, these guys also don’t get pensions. So they actually have to save for their retirements.

So yeah, the house prices are too high. These guys will buy next time prices crash (maybe as the Chinese buyers pull out like what happened in the 80’s with the Japanese). Or they will leave. The rest of the country is mostly still cheap from the last crash.

End of story.

April 2, 2012 at 5:31 am

Like I said before, the days of the plumber and welder and aerospace worker supporting the state in a major way are done. You can make six figures out of school down in the OC being a smartphone app developer, or be one of the lucky ones that make it in entertainment or high levels of engineering…but for most Joe Sixpacks, opportunity exists in Vegas and Phoenix, not L.A.

No one coming out of the state university system is going to work in a meaningful way in the higher paying IT job world. The U.C. system is placing computer engineering people but not enough to move the housing needle.

This article was a real world shot to the gut. $33. an hour minimum to rent into the periphery of the California dream. Not THE dream, but a view from outside.

Silver Spooners are exempt of course as are the newly minted millionaires in China, our future landlords.

Future Chinese landlords? Oh bullshit.

I suspect you’re tongue in cheek, but I’ll put it out there anyway. I know plenty of real Americans not toohappy with Chinese. And don’t forget how different America is not in Cali.

Great post! Agree 100%.

Anyone can afford one of our great rentals. Just bring a cot, share the rent and have panoramic freeway views of Katy Perry, etc drive by in their Teslas, etc.

zzy: >> Today, it looks like a ghost town for good jobs in technology and manufacturing. <<

Yet people on the Westside like to call this area Silicon Beach, due to all the tech, special effects, and video game companies locating here.

@son of a landlord,

Santa Monica, Pasadena and Culver City made a huge effort starting 15 years ago to attract hi tech companies. Playa Vista and Venice did the same about 5 years ago. The end result is those areas are now magnets for hi tech Dot Bomb 3.0 companies. To a lesser extent, you might add Torrance and El Segundo to this short list.

Way back in 1995, hi tech companies were fairly well dispersed over the entire SoCal region. Today, not so much. The employment situation for hi tech talent is mostly stagnant in SoCal. They all happen to be employed in the same small concentrated clusters (see above).

If you are to consider as ‘tech’, things such as unproven app/mobile/location platforms, subscription services for the minority with plenty of disposable income, and immature support services for the same, we’ve got a burgeoning tech industry on the west side.

There has become a good bit of Silicon Valley spillover down here and VC burn rates nearly as impressive in some cases. Right now it’s good times. Longer term is anybody’s guess. At the moment, housing on the west side has hooks in that. Going medium term on housing in that area is somewhat subordinate to staking the same position on above mentioned activity. As someone right in the thick of it who was also involved in Y2K and dot com bubble 1.0, it feels eerily familiar as being the same old remade song for a new generation. You already know the lyrics.

Excellent post, zzy. You are correct.

People blather SoCal is filled with high wage earners, etc., lots of opportunity, etc.. It’s a joke. Most RE is owned by people who bought decades ago, couldn’t buy the house they live in with current incomes. Most young people in SoCal are average. Most likely won’t make $100K+/annual incomes in their lifetimes, many will get stuck living with Mom/Dad/Grandma in sub $15/hr jobs until they wake up age 40 and think, what happened? By then, probably too late…only choice to stay in family home, hope for inheritance, hope home won’t be sold to pay for medical expenses and/or assisted living for parents. Hope siblings gets along with other siblings who were more independent/successful…hope other siblings don’t hire attorney, demand house be sold/money divided because “failed to launch” sibling won’t move out, etc. Those situations aren’t unusual, and can get very sad and ugly.

Most ambitious young people I knew who wanted to advance careers, marry, have kids, buy a house, etc., moved away to places with lower cost of living/better quality of life. Becoming a independent adult far more important to them than surf, climate, culture, being dependent on Mom/Dad forever, etc. It’s a trade off. Just my humble opinion.

You are so right! I cannot wait to see the rich cry when the collapse comes! Me? I will be fine in a damm Tent!!

This Slate article says that gentrification rarely happens: http://www.slate.com/articles/news_and_politics/politics/2015/01/the_gentrification_myth_it_s_rare_and_not_as_bad_for_the_poor_as_people.single.html

Does anyone have any data on month-to-month price increases or decreases in LA? Is the market trending up or down? I’m not interested in year-ago comparisons — I’m interested in the direction right now.

At some point this market is going to crash. It might be later this year when interest rates rise. Or it might be sooner. First time buyers don’t have enough money for down payments; incomes are flatlining; college graduates are starting out deep in debt. If you need to make $33/hour to afford a place to live, that’s $68,640 a year. No way.

Rents are increasing a the fastest pace in years, and they are not going to stop. Landlords are the new oil compaines, they know people have to pay so they are jacking it up til the wheels fall off and charging high rent. Simple economics.

What about home prices in LA? Still going up, or topping out, or softening?

Right…because you can jack up rents to whatever you want and people will pay it. Oooor, rents are limited by people’s income…and you can only increase them so much.

Guy asked for data, not your opinion.

yea,i know the type.when you come across landlords like that make sure you get him to fix everything.assholes think that collecting rents is all they need to do.ask to get whatever fix if landlord doesn’t get it fix within a reasonable time hire outside contractor then deduct said amount from your rent.nothing like getting your landlord straight from the get go. of course things won’t be good between you and your landlord but assholes need to be treated for what they are assholes.

June 13, 2012 at 5:27 am

I see rents falling by about $100 per month, and the price per square foot for home sales up about $10/sq ft.

May 16, 2012 at 9:45 am

Rents should come down eventually, it’s popular to rent right now as so many can’t obtain a mortgage because their credit is destroyed

Been paying the same rent for 5 plus years. No increase, not to say it won’t happen.

Obviously, this is just my anecdotal experience and doesn’t speak to the overall trend in the area, but my Los Angeles rent has increased from $1,500 per month to nearly $1,900 per month in the last three years (same apartment during this time). Prior to that, the rent was pretty stable. It doesn’t help that because I have a two-bedroom apartment, I have to pay a larger share of the water bill (which is divided among the tenets of the 150 apartments on the property – the amount each tenet owes is based on apartment size and whether or not there is a washer/dryer in the unit, not actual water/gas usage, which blows because 1. my boyfriend and I are incredibly water/energy conscience and use no more than we have to and 2. we don’t use that piece-of-shit washer/dryer unit because it simply doesn’t work worth a damn). Anyway, as soon as we signed our current lease, I noticed that the property managers updated the rent prices for the next year (which will affect out lease renewal this year), and ours will increase yet again. It will be over $2,000 per month. Our incompetent property managers/owners here don’t care about the tenets or the property except to make sure that the pool area always looks good enough to attract 20-something would-be tenets (one property manager told me, when there was a bunch of needless work going into the pool area that they were hoping to rent to fewer families and older people and get more young, “hip” kids to rent). It’s ridiculous.

My comment seems to have disappeared. Use http://WWW.dqnews.com for monthly data and use analysis from this site to get a more accurate picture.

December sales data for Southern CA:

http://dqnews.com/Articles/2015/News/California/Southern-CA/RRSCA150114.aspx

@seriously, overall home prices have largely been flat in SoCal since May 2014.

What is happening is gyrating (yo-yo) year over year prices. One month prices can go up 10% year-over-year in a specific zip code, then next month home prices in the same zip code go down 10% year-over-year.

The exceptions seem to be the prime ($1MM) and super-prime ($2MM and up) locations. These areas defy gravity.

Everything reaches a high point and then crashes, this time is no different. Once the market reaches a certain point demand ceases then some people start cashing out, prices then start to ease, panic ensues which causes even more panic selling and the retracement begins.

Ding ding!!

Speculation travels up and down stream.

i wouldn’t be able to buy the condo i sold in april ’14 at my selling price since i make less than 50k a year without maintaining my current standard of living. since i’m doubling up with my parents, we get to share limited family resources and not live paycheck to paycheck.

STEM jobs pay more than $33 an hour to start, and the companies are bringing people in topped out to retain talent. When you combine that with the perfect weather and endless entertainment opportunities, you have a demand that is so strong that people are willing to double or triple up, and/or make horrendous commutes to get a piece of the action.

You can hate all you want, but the proof is in the pudding. The people ARE doing just that to live here, because it’s the greatest city on earth.

I don’t know why you don’t just enjoy it and go with it. Have some fun!

June 13, 2012 at 12:49 pm

I have also accepted that prospects, when measured in $ per sq/ft, are even better in Phoenix. Or any Midwest city. And yes I’m aware of the weather and less entertainment, still fine though.

July 19, 2012 at 7:05 am

Just another reason SoCal sucks, the “weather tax†is so high. I’ve lived other places and housing is cheap. You get the nice place to live, and the entertainment too. Here it’s one or the other unless you are rich, or are a “legacy resident†with passed down wealth/property.

LA the greatest city on Earth? Are you serious? The entertainment capital of the world? LA is a cultural wasteland (unless you’re talking about MTV culture). LA Opera? The symphony schedule sucks; the theater is sub par to any major US city (especially to NY). The museums are hardly world class (the Getty museum, supposedly the crown jewel is a joke outside of the architecture of the facility itself) and don’t even stack up against other West coast city museums. Hell, LA is the 2nd largest city in the states and doesn’t even have an NFL team. It’s so hard to get in and out of Chavez Ravine that your lucky to catch 5 innings of any game. I guess if you call nightclubs culture it qualifies as a top 10 city.

There is no other city on earth with the combinations that L.A. has.

You have the weather, the food, the amusement parks, the sports, the boutiques, the beaches, the malls, the music stores, the music venues (from Whiskey all the way to Staples and Forum), Hollywood, movie studios, world class golf, surfing, skiing, mountain hiking and waterfalls, ATV’s, ocean fishing, and the jealousy of the world.

Can you beat that? Please try

Dude, what are you talking about? LA has waaay more cultural events than most other cities. You sound like someone who came with a prejudiced view to LA for 2 days determined that you weren’t going to find anything worthwhile.

The Getty is just one museum and it’s mainly for tourists or for taking your mom to on Mother’s Day. The MOCA, Hammer, LACMA (with BCAM) are all awesome museums with cool exhibits. There are tons of small, underground galleries in N. Hollywood, DTLA, Culver City, Silver Lake and Echo Park and probably more in surrounding areas too. Theater scene is awesome since actors between film and tv gigs put on shows at small theatres all the time. Music scene is wide and ubiquitous – punk, Latin, jazz, orchestral. The dance scene is crazy too – you just have to know a few people and they tell you where all the impromptu professional dance performances happen. Photography – yup. Ethnic festivals – yup. In total, it’s way more than any city I’ve lived in and I have lived in SF, NYC, and a few European cities as well.

LAer, it doesn’t matter how many great things there are to do in L.A., because traffic is so brutal that it’s rarely worth the hassle of getting there.

I live in Santa Monica. Years ago, I drove to events in Burbank and South Pasadena and Hollywood, trying to catch a 7 p.m. start time (i.e., during rush hour). I no longer do that. I sometimes even avoid driving as far as Culver City or Westwood during rush hour.

As has been discussed before on this blog, L.A. traffic compels many people to stay in their local bubbles. All those great cultural events beyond your bubble? If it’s across town, it may as well be across the ocean.

Sounds like you don’t get around very much

I’ve been almost everywhere in this hemisphere and have no urge to visit any others.

STEM in LA is a joke. When there’s a lot of money being thrown around some makes it’s way to NYC and LA but it’s really a Bay Area thing. Last bubble there were startups in LA and they all crashed hard when it burst. Same thing will happen this time around. The tech leadership that can sustain and grow tech companies does not exist in LA. It’s hard for LA companies to attract talent because the possibility of getting rich in tech is much lower than it is in the Bay Area. LA companies also lowball you for tech jobs. Getting above $30/hour is hard in LA and they expect the world. In Bay Area and NYC, you can get $100/hr no problem with a smaller skillset.

Are you having a hard time finding an affordable place to rent? I suggest looking at these cities in Los Angeles: Pacoima, Harbor City, South LA, West Adams, Bell, Bell Gardens, Leimart Park, Paramount, Florence Gardens, Inglewood, Compton, Watts, Huntington Park, Lancaster, Westmont, Palmdale, Arleta, Lynwood, Maywood, Pico Rivera, Vernon, Del Rey, Cudahy, Crenshaw, and West Adams.

There is nothing wrong with Cudahy, look at the crime stats. It is very low, the city just has a bad rep from it’s geographic location. I’d live there.

Ha! Some would rather live instead. And not try to fall asleep to gunshots. Got out after 30+ years in Canoga Park. For you weather freaks, a little snow will not kill you. Living in those hoods could. Peace.

THANKS for leaving….can ya get some MORE to do so….Midwest BITES…..

Canoga Park is bad? It borders Woodland Hills. Does Woodland Hills get sketchy at any point?

I assume anything south of Ventura Blvd. is good. How far north do you go before Woodland Hills starts to worsen?

I’m in Woodland Hills. I have no experience of it being sketchy.

and don’t forget your pepper-spray.

Very unsafe areas to live. Super high crime.

Hey,

What are your thoughts on the downtown loft market currently for buying? It looks like the lofts downtown are going for $450-$600 a SF. Is this market too hot or is their still value for the next 2-4 years with the new luxury units coming on the market?

DT Los Angeles is great if you don’t mind the aroma of urine and bacon-wrapped hot dogs. Then while you carefully step over the bum sleeping in front of your new condo building with a $500 HOA, you can think to yourself, “Isn’t life grand?”.

lol, exactly

that is a perfect description…

i don’t get the attraction to DT LA at these prices. it’s mind boggling really.

So… still doesn’t really answer the question about value. Just because you think it smells like urine doesn’t mean that their is or is not value. Unfortunately, it does not look this website has many commentators that can actually discuss this market intelligently.

What’s there to comment on? If you think buying a $600 per sq foot loft condo with a $500+ HOA, just blocks from skid row is a good idea, then go for it. They are not moving skid row, they may be able to contain it, but it’s not going anywhere. DT LA has the highest concentration of homeless in all the country. Also traffic in DT LA is hell on Earth. I go to DT LA at least twice a week for work and cringe every time I think about it. Don’t drink the Kool-Aid.

Another thing to consider is the age of some of these historic buildings that have been converted into condos. One of the local news stations did a piece on this recently. The city in all their wisdom streamlined many of these conversion deals and let the investors cut a lot of corners. Many of these buildings were built around the 1900’s and are in dire need of earthquake retrofitting. DT LA would be the last place I would want to be if a big one hits. That’s one reason why the HOA’s are so high. Try and buy earthquake coverage for a building over 100 years old.

I guess you got your answer from the above posts…

First Timer: You obviously aren’t from L.A. Skid Row in Downtown L.A. has been there for 100 years! Downtown has always been a dump, no matter what developers have done to “improve” the place.

Downtown is literally the Homeless Capitol of America, it’s always been that and will continue into the future. Buying a loft there for 400-500k is insane since the demographics of the area will never change.

Have you spent any time looking around? It literally stinks…..

Has the spring selling season started early? Like, the first weekend after New Year’s Day?

It seems that Redfin’s had an uncharacteristically lot of home listings, and open houses, these past two weekends. At least that’s my impression.

Lots of open houses in Eastern Ventura County. We went to a dozen or so over the last few weeks. Traffic is light still. Prices are still high but lots of small price reductions. Houses seem to go ‘pending’ on Zillow or Redfin, but reappear for sale soon thereafter – usually Realtor’s game or buyers not qualifying.

Areas we looked at: Thousand Oaks, Newbury, Oak Park, Agoura, Westlake.

Janum – I’ve noticed eastern vc list prices are way up though? Doesn’t make sense. Are you seeing closed comps and what are your thoughts on buying there now? I just transferred to a job in agoura so may be looking. Are you looking to buy?

I’ve also noticed this trend in orange county. Listing and oh have picked up. Listings that are priced correctly (relative to crazy market) in good neighborhoods go quick. At least in oc for half a mill, you can get a polished shack or a townhome and pay hoa fees up the ying yang.

Rental prices concerned, if you are lucky, you can still find landlords that are not too greedy and charge a reasonable rate. I’ve gotten lucky and also pay my rent on time every time so they haven’t touched the rent cost in the 4 years I’ve lived here.

It feels good to have affordable rent while waiting for the deflation.

STEM jobs pay more than $33 an hour to start, and the companies are bringing people in topped out to retain talent. When you combine that with the perfect weather and endless entertainment opportunities, you have a demand that is so strong that people are willing to double or triple up, and/or make horrendous commutes to get a piece of the action.

You can drink all the hater-ade you want, but the proof is in the pudding. The people ARE doing just that to live here.

Realist may come off like a shill/realtor, but there are some elements of truth amidst his hyperbole.

I’ve worked in the Aerospace biz since before the mass layoffs of the early 90s and, yes, there are a lot fewer jobs now than there were. Still, Realist is correct: in the LAX area there are still several major aerospace companies with tens of thousands of employees. And yes, we hire STEM graduates and, yes, we pay well. That said, there is no “hiring boom” going on that I can see. Smart kids from good engineering schools get jobs – the vast majority don’t even get an interview.

I do think that LA still has enough of an Aerospace industry to sustain quite a bit of wealthy suburbia. Most of my colleagues with 10+ years experience in the industry make well over $100K. Most have working spouses. You do the math. Even the inflated home prices of much of suburban LA are affordable to most of these folks.

However, while the job numbers seem to be relatively stable for now I wouldn’t call it a big growth industry either. Maybe in a couple a years if we get another Republican in the White House and start some new wars then the industry will start growing again. Lord knows W and his wars of choice were the best thing for my career since Ronnie’s Star Wars.

Almost every engineer I know clears $100k and every EAST 1553 tech can clear it simply working Saturdays. $125k+ working Sundays.

It goes in cycles, and even though its kind of down now, but not really, yes the next War will create a ton of wealth again

Yes, yes and yes.

Aerospace is hiring, even with a light sprinkling of layoffs, most of which are in administrative positions. But EEs, CS, math and physics grads are welcome. Nothing like the 80s, but much more than in the great downsizing of the 90s. The main boomers have started retiring in bulk, taking decades of experience with them. We at the tail end of the BB are suddenly getting a lot of love, particularly since we don’t have the “golden” pensions which, combined with low interest rates, are pulling the older boomers out the door. (In addition to grandma’s CDs paying diddly squat, this exodus of experienced talent is another unintended consequence of keeping interest rates artificially low).

Sustaining aerospace in SoCal: Yes. Manufacturing has moved out, but engineering and R&D are still here, and we’ve survived multiple rounds of layoffs since the early 90s. Many have shown an unwillingness to transfer to flyover states despite some pretty hefty incentives over the years, and it’s somewhat difficult to find people with expertise in satellites and various exotic specialties. And (though I absolutely do not know any insider information), it seems logical to me that the big contractors would want to keep a meaningful presence in CA in order to maintain some influence with our congresscritters.

And yes, it’s not a growth industry (at least in SoCal), but LA needs to be workable for people across the spectrum; otherwise, it’ll get bad. (I don’t currently think it’s bad, but my perspective may be atypical).

I can afford to stay, but I don’t want to live in a small island of prosperity surrounded by unhappy people. If I cashed out my equity and moved to a place with bad weather and a nicer lifestyle, I could retire next week, and that’s awfully tempting.

The numbers are telling me something. (New posting-name for me, more in keeping with my international mind).

_____

Don’t make the mistake that cost Boeing employees $98 million

-MarketWatch (WSJ) – Nov 28, 2014

[..]An employee with a base pay of $60,000 is eligible to earn a 75% match on up to $400 a month. The monthly match, $300, amounts to a raise in pay of $3,600 a year. That’s the equivalent of a 6% raise — something I doubt employees would turn down if it were offered to them in those terms.

[..]A survey conducted this year by Harris Poll for Wells Fargo found that middle-class U.S. residents aged 25 to 75 have set aside a median of only $20,000 for their retirement. One-third of them reported they are not contributing at all to a 401(k), an IRA or any other retirement plan — that’s far worse than the Boeing statistics. Of those who are saving, the median amount reported was $125 a month. About half of those who were in their 50s told the pollsters they expect to work until age 80 because they will have inadequate savings to retire.

http://www.marketwatch.com/story/boeing-employees-push-away-98-million-in-401k-match-2014-11-12

A lot of home listings and open houses in January seems unusual. That usually happens in the Spring. We may have a glut in inventory this year, considering the low number of sales and mortgage applications.

Our government made a huge mistake in 2008/2009 when they chose to prop up the banks rather than let the R.E. market crash as happened with the Savings & Loan “Crisis” in the late 80s/early 90s. The S&L crisis allowed a price correction that benefited the middle class. Propping up the banks in the 21st Century has created this high-cost housing madness. Yes, a R.E. Market Crash is painful, but it allows true price discovery and is more beneficial in the long run. Bank failures are a good thing. Save the depositors, not the shareholders.

The S&L’s didn’t won the FED. The Big 4 Banks ARE the FED! That’s why the crash was halted. But now the inventory is in the hands of private equity. No parachute for Bust 2.0. The FED NEEDS a RE bust anyway as it’s the quickest way to put disposable income in consumer hands. We have world wide demand side weakness that can only be solved by an increase in consumer spending. That can’t happen while RE is draining monthly budgets.

You’re right to point to the S&L bust. The consumer prosperity that followed is hopefully what the current bust will lead to.

Ever wonder if that was the govt’s plan? To shift the risk to private holdings vs. banks?

Me personally – I will continue to rent my gorgeous 3 brd house at 40% under what it would cost me to buy it – and happily wait to purchase a similar home from a deperate specuvestor 🙂

Good luck guys. You give me hope. There is something a lot to be said in the mindset of ‘Love SoCal and Forget the Housing Bubble’ whilst this madness rages, enjoying life and taking happiness where you can, building financial positioned to turn things on shocked specuvators and complacent equity rich owners, when the crash does arrive.

@Calgirl

Of course it was the FEDs plan. If the REO-to-Rent scheme was such a great idea the banks would have held the properties themselves. It’s not like mark to market was stopping them anymore. You’re rental mirrors mine. I’m renting a house in Rowland Heights that was bought in 2006 for $600k and needs a lot of work. The owner put 300k down and is at best breaking even on my $2000 a month rent. While my case is extreme MOST properties are so over rental parity the unsustainablility of it all is obvious. We’re three months away from the FED raising rates. Mortgage rates will follow. Capitulating sellers will increase inventory. No CA RE run up has NOT been followed my a downturn. Late 70’s, Late 80’s, Housing Bubble 1.0. All were followed by a downward adjustment. We probably have a year or so to go before real deals are to be had. But unlike the brief windows in 2010/11 that the banks slammed shut, I expect we’ll have a drop followed by a protracted flat period. The properties won’t be in the hands of banks who use FED $ to hold them back. Boomers funding there retirements should keep a decent flow of properties as well. We’ll find out in the spring if 2015 = 2007 or 2008. Either way the upward selling momentum is dead and so is Bubble 2.0. We’re just timing the correction now…

@NZ

That is on the highly optimistic side of financial projecting, but I like it.

It has dragged on for so long (non-prime crash.. followed by even more house price inflation), that many of us are numb, worn out and feel it will be without end. While that has also fueled the confidence of many speculators too, feeling they are supported, taking larger risks.

After the recent ECB bank stress tests, the ECB has suddenly gone very confident for doing QE. In part I wonder if it’s in order to have Euro banks financially positioned for the Fed raising rates.. partly in order so that savers don’t panic.. with plenty of liquidity in Euro banking system, vs prime real estate in all locations being super high valued, and allow a wider real estate correction.

Although central banks can’t print capital, they can only provide liquidity by creating debt. Only the market can create capital, by valuing assets above liabilities. Although market participants can create value if they are plain handed liquidity at expense of Gov solvency worsening.

ZZZzzzz…the American Dream is a myth. Get over it.

you have to be asleep to believe in it …. keep dreaming

House hunting in Phoenix. Every listing I have seen is priced at least 20% above the peak comps from 2006-2008. And these houses need work, they have origional fixtures from the 1980’s, former rental homes.

Who in their right mind would set the neighborhood all time sales record for a 30 year rented, beat up former rental that needs to be completely gutted?

James…I agree, the condition of homes compared to the touch job of on line photo’s is amazing. Gosh almighty folks, can’t you at least paint the garage doors, clean the windows, shampoo the carpets, pull some weeds before asking these overinflated prices?

Why should they, when they sell themselves?

I totally agree with what is being presented in this article. It is become relatively impossible for lower middle class individuals to rent places. I am currently living in Canada but i have lived in a few different provinces in the country. and over the past few years I have noticed the same trend. where average 2 bedroom apartments rent almost double in two years going from $1000- $2000 for the same apartment. with no advancements in the quality of the apartments. I am fortunate enough to have a stable job to sustain living in places such as this but the majority of the younger tenants in my building have either had to move back in with their parents, move out, or really stretch the amount of money that they are brining in monthly in order to pay for the basic necessities. There should be some sort of regulated body to at least keep these rent prices in a reasonable amount for the basic working person and limit the amount of scamming these land lord thieves can pull out of our pockets

Rent control drives up prices. You front load the monthly fee to cover future losses.

Don’t worry. The energy and commodities bust will take care of those overpriced rentals in Canada soon enough

Here is a 450 square foot Co-Op property in central Tucson that just sold for $12,900. See the sold listing at http://www.realtor.com/realestateandhomes-detail/1458-S-Palo-Verde-Ave-Apt-K212_Tucson_AZ_85713_M13347-33767. (There are 3 others like it that sold for $7000-9000, but they were in worse condition.) I lived in this area for over 10 years. The problem is not crime and it’s not the location, which is one of the most convenient in town. The issue is that you generally can’t take out a loan to buy the place and you can’t rent the place to someone else. You’re just buying a place to live with money that you have. Many people can afford to retire now. All they need to do is downsize and move.

Vegas Landlord, you got me thinking with the link to that little Tucson co-op.

With about $8K worth of work and decorating, that little studio would make a nice winter-time pied-a-terre for a Chicago snowbird. Chicago is the greatest place on earth to be in spring, summer, and fall, but I’d love to clear the hell out of this place come January, once I retire. A little place like this would be a low-cost getaway that I could do what I want with. I looked at a few other listings in the same area, all under $20K, and some are cute- a little imagination, and they could be very livable.

There ARE alternatives to moving to one of the highest-cost areas in the country just for the weather, especially if you are retired.

We’ve noticed the same, SonOfALandlord. I can’t keep up with all of the new listings that have popped up since January 1. Stark contrast to the incredibly tight inventory we saw before Christmas. There is actually a decent selection now in many neighborhoods – including some of the more popular choices.

You can have your traffic and your ridiculous home and gasoline prices and your drought. I got the Hell out of there. Good luck to those who are still trapped.

And can you indulge us on what you traded the gas and traffic for? Because I’m sure you gained crappy weather and increased boredom in a smaller area.

We sold off our 1956’s era track home in Rolling Hills Estates for $1.5M and escaped to a town called Cool which is located in Northern California between Sacramento and Lake Tahoe. We purchased an updated 4 bedroom 2.5 bath home with a horse barn on four wooded acres for $450K. We’ve now got clean air and plenty of water. We don’t miss LA at all!

I hear ya. We traded in our pre-WWII 2/1 crapshack in LA for a updated 3/3 on over an an acre with fruit trees in rural Northern San Diego County. It’s beautiful and better then LA in every way. Even the weather is better. My only regret is that I didn’t do it sooner.

Does the boom of quasi-illegal vacation rentals have anything to do with the rising rent prices?

No one really know what will happen to the housing and rental market, even in the near future. My lease is up in May so hopefully a dip in the market will keep my rent the same for next year.

The rainfall is not any more regular than the home prices. Nobody knows the future.

First, What? where are you 🙂

Now as for these rental statistics, if you get 2 $15 an hour earners the rental percentage of income is closer to 50%. That seems reasonable for a major metro. The relevant issue with Housing Bubble 2.0 is how it has driven up said rents by closing off purchasing to the majority of the populace. Absent a hyper-manipulated market there would be homes that people could squeeze into (see 2010 before HB 2.0) and rental vacancies would force lower rents. You’d also have people who would buy in the IE and Metrolink into LA and the OC. This is why I feel the inflation in the inland areas and suburbs is the worst. The specuvestors have removed all escape routes from the madness of LA and OC prime. Once the specuvestors capitulate in the suburbs and Inland areas the dominoes will fall toward prime SoCal.

To gauge this economy based on high end restaurants packed on the weekends, housing area where out of 21 homes built 17 sold at avg price of 1.3m, Porsche dealer with people buzzing around and some cars on back order due to sells, makes you wonder not all are hurting, that is for sure?

The 5% like yourself are doing just fine. You only need $2 million in assets to be part of the 5%

ben….I think 15m or so are in this 5% certainly a big number in a smaller country, in America with 320 million population not so much. I read many years ago that capitalism should afford a 70-30 ratio as to quality of life and income distribution, in other words a good ratio of excellent standard of living for the 70%.

In the 21st century this of course is not even close. The actual gap has widen so much that even a 75-25 most likely will not happen even during years of prosperity. Most likely in the next 50 years if we last, somewhere around 12% can truly say they will be set in life with little worries the other 88% could and probably be much worse off then even now. This is disturbing at best, it leads this nation and other advance nations to wonder, back in the 20th century why didn’t we plan better for the over whelming majority of people, we all know the answer of greed, power, all about me, but the answer still begs, what was better then capitalism?

If you have the money for a 20% DP and a stable job, then buying a house might make sense regardless of what is currently happening in the housing market. I wasn’t able to buy until I was 43. As my wife and I chugged along (repaying student loans, saving DP, raising 2 kids), I thought buying a house was insane. We thought we would see the market crash where we wanted to buy (Point Fermin, San Pedro), but it never really did. So last year we took the plunge and we’re very happy. The only problem is my age! We had to do a 15 year loan because I sure as hell don’t want to be working at 73 unless I want to! Anyway, my point is that buying at a younger age (as long as you have the DP, no debt, and a secure job) makes sense because you are probably not traveling the world instead of buying the house. You’re probably just chugging along.

That’s a sad life!!

When people are asked what they regret most in life, I don’t think “not owning a home” is high, if at all, on that list. Usually it’s traveling, spending more time with family, etc… I’d rather live and not own than chug along and own… Chugging along, the new american dream!

some people like running in the hamster wheel

My post is for the worker bees, eMan. if you’re single, a world traveler, trustafarian, etc., just move along to the next post.

you dont really say why it might make sense to buy a house right now for someone in their 30s

Acronyms are everywhere in the written and spoken word these days I get tired of looking up the meaning of acronyms.

I’m going to give up looking for the definitions of acronyms. I find that it’s just not worth my time.

Acronyms guarantee that only your colleagues will understand. No one in the general public understands without spending the time seeking a definition. The practice exposes a geocentric nature.

Today I learned what STEM means . STEM means that Scientists Technicians Engineers and Mathematicians, Some of our nations brightest don’t know that high school drop outs with a general education equivalency certificate and a commercial drivers license can earn you easily six figures.

Why on Gods green earth would you want to haul loads OTR and put up with all those struggles (I researched the field as a youth) when you can make the same $ in climate control, in the same place daily, in a low pressure creative aerospace environment? With awesome benefits and discounts to boot.

Lot Lizards?

STEM actually stands for Science, Technology, Engineering and Math as areas of study, not the actual occupations, but you got the gist of it. Your statement about six-figure salaries of some truckers is correct as well, but I’d advise against turning that into general advice that people could use in career planning, because there are a limited number of such jobs, which has some similarity to firefighters and police, who can also earn a lot of overtime. If you look at the median salaries of people with a high-school-equivalent education vs those with Bachelor’s degrees (here: http://www.bls.gov/emp/ep_chart_001.htm), the median weekly salary of HS grads was $651 in 2013, whereas it was $1108 for those with Bachelor’s degrees.

Also, trucking has one of the highest death rates of all occupations — 22 per 100,000 FTE (Full-Time Equivalent) jobs. That’s too exciting for me. Yesterday, I attended three meetings, proposed extending a design to cover more test points, explained a memory cache concern to some junior people and verified some test results. At one of the meetings, someone shot me a short look of irritation, but otherwise, I escaped without injury.

interesting new data point on creeping mortgage default rates in december: http://www.housingwire.com/articles/32653-experian-more-americans-miss-monthly-mortgage-payment

I think the reason rents are going up so much, is because code enforcement is trying to raise money by citing for repairs etc. and if not done in so much time, they can try to collect fines up to $1,000 per day, like they did in the eighties when they were short of money, of course the fines were a lot less per day back then. Also the eviction courts are taking forever to evict the bad tenants, since they consolidated the courts. Since they cut back the number Courts evictions take four months instead of 30 days to evict a tenant, even when there is no trial.

In addition, you have the service animal and/or the emotional support animal scam now targeting landlords. Then the IRS wants the rents to raise because they want to collect an Obama tax on your rents to pay for Obamacare. When the government tells you they want affordable housing, just like affordable health care, they mean just the opposite. It is the government that is making things more expensive.

I’ve been reading your blog for several years. In that time if I had have bought in SoCal I would have enjoyed a 20% increase on my property, or a 100% return on funds invested. While it offers satisfaction to criticize the thinking of those who do decide the time is right to buy, fundamentally real estate is a sound investment. You are right in pointing out that most buyers forget that real estate follows cycles, however we are still on the side of fair value. With a fixed rate mortgage and taking a long time horizon lol cycles smooth out.

It makes much more finabcually prudent for a hipster overcommit and eat purina than be at the mercy of landlords and spend income on consumption. Besides in 20 years time you won’t remember what you ate in 2015 however you will know very clearly if the roof above your head at night is yours.

The real reason rents are going up is the government raising taxes and inspection fees, fines, and the Courts are not allowing landlords to keep any of security deposits even if the tenant didn’t pay any rent when they moved. Calling it a last months rent, when reality it is a security deposit. Even if you send the accounting in 21 days and have proof of such the courts are so libral they just award the tenant a judgment against the landlord even if they damaged you apartment. The courts just listen to the tenants side and don’t even let the lordlord talk especially in small claims court. In addition there are a lot of friviolous lawsuits like emotional support pets and/or service animals,mold and bedbugs etc. That is the real reason rents are going up The Govenor stopped the frivolous lawsuits against small business, now he needs to stop these suits against landlord.. Another thing evictions can take a long time since they closed a lot of the courthouses in Ca. The sherriff can take over a month to get a date to evict even if you have a judgment. So now the attornys stipulate with the tenants giving more time for the tenants to move while not collecting rent. No wonder rents are going up.

Leave a Reply