Main Street Credit Crisis: Bringing Back Layaway for Purchases. The Anti-Saving Crusade Continues.

The consumerist credit machine is coming to a grinding halt. It is hard to wean yourself off an addiction that has persisted for decades, unchallenged and enabled by companies and financial engineering. The idea of buying things with money you currently don’t have isn’t a new concept. In Edward Bellamy’s novel Looking Backward the concept for a credit card was mentioned and this novel was written in 1887. Western Union issued charge cards to frequent customers as far back as 1914. The major push however came in 1966 when a group of credit issuing banks congregated together and established the now famous charge card which eventually came to be known as the Master Charge in 1969.

In the past, there was also a novel way of buying something you wanted but didn’t have the cash to buy it. It was called layaway. The concept is simple. You see an item at a store you like. You pick it out, take it to the cashier and ask them to set it aside for you. You then make monthly payments until the item is paid off and then it is all yours. Yeah, I know this method must be shocking to many since delayed gratification is a foreign concept. Given that people are looking for methods to buy things this is now making a furious comeback given the current climate:

“(Boston Globe)Â After pulling back on layaway programs for years, retailers are touting the service as a financially savvy way to buy goods this holiday season. Already, many cash-poor and credit-strapped shoppers are responding by flocking to layaway counters at stores such as Kmart, Marshalls, and Burlington Coat Factory, and using online options such as eLayaway.com.

“The response has just been tremendous,” said Tom Aiello, a spokesman at Kmart, which is running a national holiday ad campaign for its layaway service. “We know for a fact it’s a big increase over . . . last year.”

What a shocker. And this isn’t a prudent way either. What is happening is credit card companies are getting body slammed into the ground with rising defaults and restricting credit on many customers. The non-prime customers can now forget getting $20,000 credit lines simply for being able to walk and chew gun at the same time. Even prime borrowers are seeing their limits lowered. But make no mistake, this upsurge in layaway is simply a manifestation of the consumerist hamster mentality:

“People are looking to buy the things they want with noncredit based terms,” said Michael Bilello, senior vice president of business development at eLayaway.com. “The lend-and-spend boom is over.”

You being the bright and intelligent observer that you are may be asking:

“Why not just save the money in an interest savings account and then buy the item later?”

“Why not just save the money in an interest savings account and then buy the item later?”

“Good question. The consumerist hamster loves spending and is anti-saving. A savings account is like kryptonite for Superman. So, savvy marketers need to figure out a way to make it seem like you are spending and not actually saving.”

“Good question. The consumerist hamster loves spending and is anti-saving. A savings account is like kryptonite for Superman. So, savvy marketers need to figure out a way to make it seem like you are spending and not actually saving.”

“I see. So isn’t this better than using a credit card with high interest?”

“Yes it is. But it is also better to jump from a 6 story building as opposed to a 25 story building. Either way, you really need to ask yourself if you should jump.”

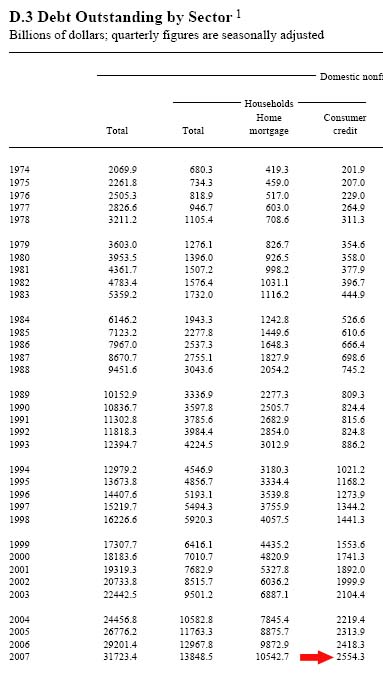

The argument I would throw out is that consumer debt is already much too high and this is a methadone approach to going off the debt treadmill. Take a look at the most recent Federal Reserve flow of funds report and look at the amount of consumer debt outstanding:

There is currently over $2.5 trillion in consumer debt outstanding! And yes, right next to it you can see that there is $10.5 trillion in mortgage debt but that is an entirely different story. Now that our government has issued the epic and largest financial bailout in history, citizens are actually having to save money to purchase things. What is this you speak of Dr. Housing Bubble about saving money to buy something? This simply makes no sense. Well, this again goes back to the silent depression that I’ve discussed various times and I suggest people read the article to get an idea regarding the psychology that is currently evolving in the current economic climate.

Now I know that layaway is better than charging up a credit card. Yesterday on NPR I heard some girl talking about putting some $400 stilletos on layaway. Yes, $400 shoes on layaway. Welcome to the weird and wacky world of folks addicted to spending. And maybe that is the bigger issue. Debt is simply the tool that is used to outwardly express our nation’s addiction to spending. The consumption hungry beast that rests in the belly of many Americans. That beast is getting a furious smack down however.

The latest U.S. GDP report showed that GDP fell by 0.3% in third quarter:

![]()

You may be asking yourself, “what happened in late 2007 to turn this thing around?” We were already heading into a recession at this time but we strapped on our consumption nation thinking caps on and issued a stimulus to the nation to get things going again. Those stimulus Wal-Mart rebate checks helped plug the dam for 2 quarter but the third quarter was too much. Just wait until we look at the forth quarter which is going to see the economic beat down we just took. Keep in mind the official definition of a recession is two consecutive quarters of declining GDP. One is in the bag. We are well on our way to achieving that. It is interesting to note that Wall Street’s press secretary the Wall Street Journal had a survey in January that had economists stating that we only had a 42% chance of a recession. In another separate survey, 42% of all economists have undergone a lobotomy in the past 10 years. They have found there way a bit and issued a WSJ Economic Forecast survey in October saying the probability of a recession is now at 89.3%. This is like saying there is a 89.3% probability that the sun will rise tomorrow.

Consumers are tapped out. Seeing that consumption is 70% of our GDP and consumption is contracting, logically you would realize that GDP would subsequently follow suit. Some people simply lack this foresight. The Conference Board issued their consumer confidence report and it fell to 31, the lowest reading we have seen in the 41-year history of the index.

My suggestion for anyone considering putting something on layaway is this. Open up a savings account. You can even get an online one that pays a decent rate and set it to automatically deduct a certain portion from your paycheck each month. When you reach your desired amount, if you still hope to buy the item withdraw the money and do it. Why lock yourself in to that single item? You are giving the store a free loan. Why not earn some interest and forget the layaway? My guess is that many people will actually enjoy having a nice sum of money saved up and the impulse to buy that said item may have already passed.

Hamsters of the world unite!

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

21 Responses to “Main Street Credit Crisis: Bringing Back Layaway for Purchases. The Anti-Saving Crusade Continues.”

Doc,

What you say makes perfect sense. I was listening to some folks describe their experiences during the depression and you cannot help but be moved. (A dollar down and a dollar a week) The great tinkle-down theory has been exposed and most people aren’t buying it anymore. Even CNBC and Faux News have been rather dour and flirting with supply-side blasphemy lately. The paradigm is truly shifting.

My concern it that the Depression occurred when we had trade surplusses, piles of gold, industry that was the envy of the world, agriculture enough to feed the whole world, practically, railroads, shipping, ports, oil enough to export. Most of that is not so any more. My fear is that we transcend the depression right into another Dark Ages. We can’t stop a recession that’s already here, and we can probably only forestall and intensify the next depression, but we really need to prevent another Dark Ages–a total collapse of the constructs of society. The PTB (Paulson,Treasury, Bernanke) have already done things that a year ago would seem unimaginable, and things are still getting worse. I wonder how many rabbits are in their hats now–they’re already starting to pull skunks.

BTW–2 quarters is not exactly the definition of a recession–they just have developed the habit of not declaring a recession until there are significant signs of a recovery. Not declaring one when it is already a foregone conclusion should be more frightening then just saying it, because it indicates that we are going for another round of limbo.

Capitalism needs regulation, redistribution, jubilee. The algorithm is always the same: all wealth migrates to the few, wealth becomes a toy, the masses suffer while the few live lavish, oppulent lifestyles, the model collapses. War crushes the whole thing and we start over. We’re smarter than that and we can do better next time–but what have we learned?

It’s a good idea to resist those hamster impulses, although one point should be made.

With inflation at an admitted 5%, and more like 8% using the older models, it doesn’t make as much sense to save money at 3 something per cent.

Had house prices been included in the inflation model, rising prices would have triggered interest rate rises-cooling off the housing market and encouraging saving.

“Keep in mind the official definition of a recession is two consecutive quarters of declining GDP.”

No, the standard definition of a recession is not two consecutive quarters of declining GDP. The National Bureau of Economic Research (NBER) defines a recession as”a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP growth, real personal income, employment (non-farm payrolls), industrial production, and wholesale-retail sales.”

The March 2001 to November 2001 recession did not meet the definition of two consecutive quarters of declining GDP, but the NBER declared it a recession.

The July 1990 to March 1991 recession did meet the definition of two consecutive quarters of declining GDP.

From the NBER website:

Q: The financial press often states the definition of a recession as two consecutive quarters of decline in real GDP. How does that relate to the NBER’s recession dating procedure?

A: Most of the recessions identified by our procedures do consist of two or more quarters of declining real GDP, but not all of them. But our procedure differs in a number of ways. First, we use monthly indicators to arrive at a monthly chronology. Second, we use indicators subject to much less frequent revision. Third, we consider the depth of the decline in economic activity. Recall that our definition includes the phrase, “a significant decline in activity.â€

Q: Isn’t a recession a period of diminished economic activity?

A: It’s more accurate to say that a recession—the way we use the word—is a period of diminishing activity rather than diminished activity. We identify a month when the economy reached a peak of activity and a later month when the economy reached a trough. The time in between is a recession, a period when the economy is contracting. The following period is an expansion. Economic activity is below normal or diminished for some part of the recession and for some part of the following expansion as well. Some call the period of diminished activity a slump.

http://www.nber.org/cycles/november2001/

Excellent point Doug. Fed targets and policies should be like an oar to steer. Now they’re like a pole just to try not to go over the waterfall until hellicopter Ben comes to the rescue. Too bad they don’t understand the physchological paralysis setting in can’t be fixed by dolling out more golden parachutes.

With interest rates as they are the difference between a savings account and layaway is going to be almost trivial for most purchases. Ok, so you get two free tall Starbuck’s lattes for your effort for saving up 6 months for those stilletos.

And in the meantime you have taken the risk of your bank going bankrupt while you were saving up. Yes, I know, the FDIC will cover it, but those stilletos might end up waiting a long time indeed while you wait for an FDIC payout.

Maybe the best alternative of all is the Bank of Mattress.

Doctor, I’m sure you’ve seen this, but just in case…

Credit Card Bond Sales at Zero, First Time Since 1993

Nov. 5 (Bloomberg) — Credit card companies were shut out of the market for bonds backed by customer payments in October for the first time in more than 15 years, as investors shunned the debt amid the global credit freeze.

.

There’s also the risk that the store where you laid-away goes out of business during the wait. Plus, I’m guessing that those stilletos might be out of fashion by the time she gets them.

DHB – I saw you posted at CR not long back. Been pretty crazy over there lately, what with the election. Hopefully we can get back to the regularly scheduled end-of-the-world-as-we-know-it now the election is over.

js,

A good point, but still the thing about the shoes is that if you think savings first, you will get in the habit of saving even if your interest is negligible. A big chunk of cash suddenly seems more precious than the rush of an impulsive purchase. It’s a counter to the consumerist drive that every purchase is a small fraction of your annual gross income. Saving changes the way we think and behave, and in turn, if you don’t buy $400 shoes, the other girls in the office won’t think they need new shoes, for instance. Our whole philosophy matures and we think about things that really are important.

If someone breaks into your house and steals your undocumented cash, you will never get that back. And in depressions, unfortunately, theft will be a growing concern.

Actually, Doug R., a gold-based monetary system would have done a far better job of restraining the excesses than the inclusion of house prices in the inflation statistics. A gold-based system would have required a stable gold price–which, if I recall, was nearer to $300 per ounce in ’03 than $1,000 per ounce (or even the current $700). Interest rates would have had to increase substantially to keep a stable price level as measured in gold units–which would have required far earlier increases in interest rates than our once-upon-a-time Randian gold-bug Mr. Greenspan encouraged.

Dr. HB, home mortgage debt is part of the same story–and a potentially far bigger one in regards to consumer debt. Using the statistics in your post, the latter increased by only 12% or so since 2002, while the former rocketed by about 75%. While I don’t know how much of this was based on bubble-supporting purchases vs. bubble-induced HELOCs, since so many were using their homes as substitute credit cards, increased consumption debt embedded in that 75% figure could be far greater in absolute dollars than the more pure credit card debt increase. Since homes will likely revert to ’02 prices (or worse), the forced liquidation of that debt, along with reduced spending resulting from the impossibility of replicating it, will likely do more to correct the excesses than a reduction in credit card debt. And we Austrian economists know what “correct the excesses” means.

BTW, you may want to suggest that we read a few of the great economists who, had they been alive today, would have warned us about this bubble. Perhaps you can point to the specific books; it’s been so long since I read them, I can only recall the names (Von Mises, Hayek, Hazlitt and the like).

But if we enter a deflationary period that 3% savings rate suddenly looks pretty alright yeah?

I used layaway before at KMart but it was not because I could not pay for it. I bought both my sons Honda Racing bikes from KMart and did not want to bring them home before Christmas. So I put on layaway for $5 so they could store them until I picked them up christmas eve. So layaway, is great for hiding gifts for kids.

DHB, your posts are awesome… (currently, I am working in Japan and yours and other blogs are a good way of getting an honest economic picture of America)

I am a good example of what can happen when you save money to buy things… As a typical GenXer, all my friends were driving BMWs, Lexus, Audis, etc and I wanted to be part of the crowd. A few years ago I decided that I wanted to buy either a BMW 3 series or Lexus IS and started saving money for it. But when I reach my goal of $20,000 for a down payment, I had changed my mind. The idea of giving all that money I worked so hard to save to a car dealer for an item that loses value from the time of purchase was not sitting well with me. Instead, I opted to buy a cheaper car with better mpg.

Lay away only makes sense if it is done to buy a once in a life time 75-90% off sale item you really need but don’t have the money for. Otherwise save and make the interest or only buy what you can pay cash for. I only buy what is on sale and then only what I need, and I am allergic to credit unless its at 0%.

…a good word for credit cards – i have had one for 30 years and have never paid interest. It is a convenience not to have carry cash around. The downside is that everything costs a litle bit more, to enable the retailer to send 3% to the card company, but my paying cash would not fix that.

The argument for consumer debt is that the interest payment is a sort of rent – I get the item before I have actually paid for it, so the seller charges me something for its use. To me, this seems like a reasonable deal.

The true evil of credit cards is 18% interest – I am always astonished that Congress lets them get away with it. If the interest rate was 5% (say), there would be less of a problem.

Love the article. Love the hyperbole.

Dr. HB you should really consider writing a book. Would be very entertaining.

Wrong rodent. We aren’t hampsters, but lemmings.

Personally I think we are all frogs, tucked neatly in our warm pot of water, enjoying it’s ever rising temperature…until, “sniff”, is that dipping sauce I smell?

Got that right Bob. The loan sharking that Congress allows at 18% is horrible. Unfotunately there are a lot of folks that don’t have a great deal of education, but are we really a society that feels it’s OK to prey on the less educated? I don’t want to be part of a society that thinks like that. In the end, they will default. Some folks know better and still are foolish, some simply can’t do the math.

DHB’s point is crucial: for many, money isn’t worth anything unless it’s specifically targeted for spending. Savings is the largest line item in our monthly budget–more even than our PITI. I’ve talked to so many people who can’t understand why one would have savings, unless it were “for” something.

~

“For” retirement, for instance, which means a massive end-of-life shopping spree. Golf carts, RVs, bionic knees, grandchildren gifts, and so on. That’s considered the aim and goal of a life of work! Having a total cashectomy in a few years or decades of full-time consumption. It’s American Potlatch I guess. But it appeals to me not at all.

~

We save because we save. We have no idea how, or whether, we’ll be spending this money. We’re banking current income against future interests or uncertainties.

~

Another element comes in here. If you have savings, it means you had a surplus of income. I.e., you spent less than you earned. Among our more progressive friends and even relatives, that makes us bad. I.e., we “had more than we needed.” I.e., we should be giving it to others. I.e., them or their sprogs.

~

So the entire culture of savings for its own sake has been shredded and remains vital only among those of us who save for its own sake. In the interest of full disclosure, I have no idea why anyone spends money on the holidays; gifts of care, attention, presence, or one’s own skills can be given, if giving is important. But again, that Display-Shopping, or American Potlatch, thing is pretty strong among many in the US.

~

While one can argue that layaway is better than credit, it still, as you point out, buys into (!) the idea that money is for spending on Stuff. Maybe at bottom people know that our fiat currency is unbacked and fragile, and only means something when they translate it into something material.

~

Savings represents both the ability to defer gratification and some measure of faith in our currency. I have to say, DHB, there are times when I watch dollar devaluation undo everything we’ve saved (the hidden tax) and wonder why we didn’t go out and buy a boat or a cow or something. But then anything you buy has hidden costs, so the money leaks away anyway. This is why money is a terrible basis for an economic system.

~

rose

The only money spent that won’t leak away is that spent on experiences. The stock market can crash, the housing market can crash, the dollar can depreciate and your fancy car can too. But they can’t take away the memories of the vacation you took and all the other experiences you have had.

If you lay away then you’re an unsecurred creditor of the store. Circuit City, anyone?

Leave a Reply