The mortgage rate shuffle: Higher mortgage rates already having impact on housing market. 4 significant housing trends to look out for as 2013 enters the fall selling season.

Mortgage rates recently reached another multi-year high as predictions for the Fed’s triumphant taper seem more likely. We continue to hear that people are rushing out of their homes bursting out of the front door with suitcases of pre-approvals but that is clearly not the case. The housing “recovery†is being driven by investor buying. There is no denying that. There is also a clear case materializing that banks are going to eat a significant drop in refinancing revenues and with mortgage applications remaining low given the rampant run-up in prices. Again, the explanation for this is coming from the non-traditional juggernaut of investor buying. As people shuffle to purchase homes there are a few major trends that are appearing on the housing horizon as we enter the fall selling season.

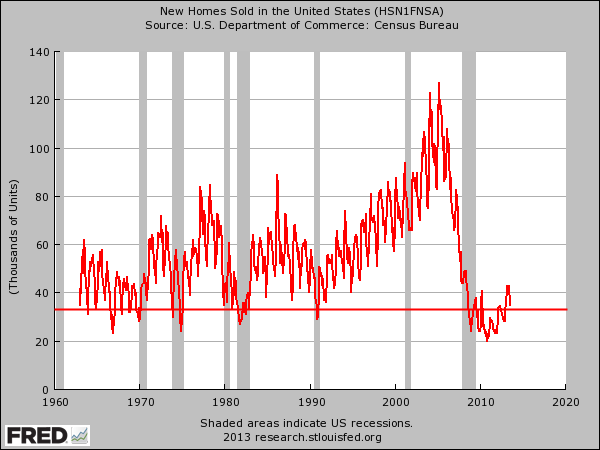

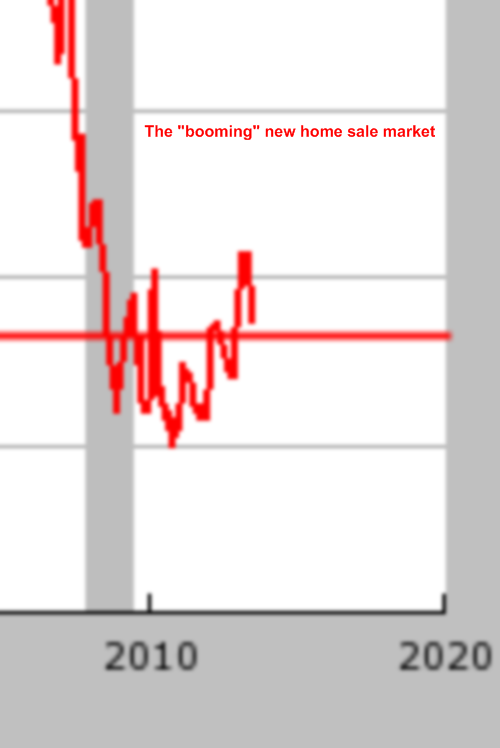

Trend 1 – There was never a recovery with new home sales

There was really no recovery in new home sales. Even if we zoom into the above chart, the bump was pathetic:

Normally what you will have in a typical healthy housing market is a mix of “used†home sales and new home sales. The new home sale portion never materialized. Investors have been eating up existing home sales at deep discounts although those discounts likely peaked or are near peaking and we are now running on mania fumes. As your history lesson in bubbles might have taught you, bubbles can last longer than you would imagine yet this thing is looking ripe especially as we look at higher rates.

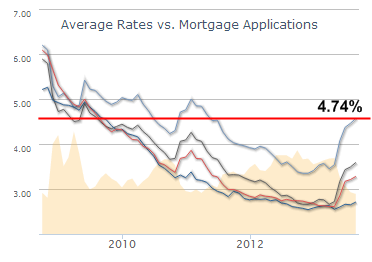

Trend 2 – Higher rates do make an impact

Mortgage rates are making multi-year highs:

By the way, these rates are still fantastic in a longer-term perspective but we have a short-term thinking financial system. The issue with this is that the market since the crash has been used to the Fed buying down rates lower and lower and this psychological expectation is now broken. With rates going up, the system changes. Sure, some people rushed out to buy but the evidence tells us that this was a small unsustainable event. What has occurred more heavily is the low rate environment has allowed big financial players to get their hands on easy/near no risk cash and pump it into buying up real assets in the form of single family properties. The Fed’s goal of helping average families? The data tells us otherwise.

Higher rates will have a bigger impact on more expensive markets where prices are already reaching levels that in some cases, were last seen during the peak of the last housing bubble. Investor buying is still incredibly high and if this segment of buyers begins to slow down, this will be a major catalyst to slow the housing market.

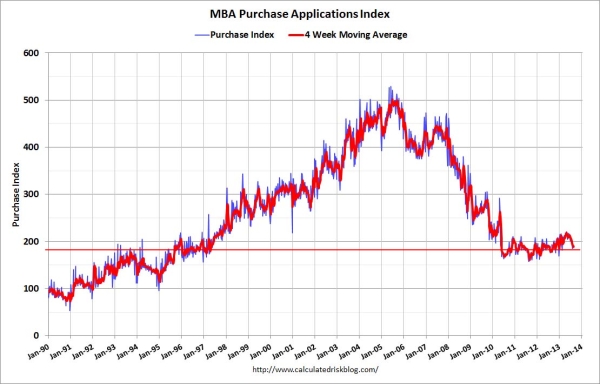

Trend 3 – Where in the world are those mortgage applications?

Keep in mind that something like half of buying in 2013 has come from investors nationwide. So this overall figure matches up with the massive drop in mortgage applications:

You have to look at multiple data items to get the bigger picture here. Investor demand is eating up what little inventory has been out in the market. Nationwide, we are seeing inventory pick-up but buying from investors is still robust. As long as this continues, you can expect a battle between investors for the limited inventory that is out there. Yet, this trend is reversing.

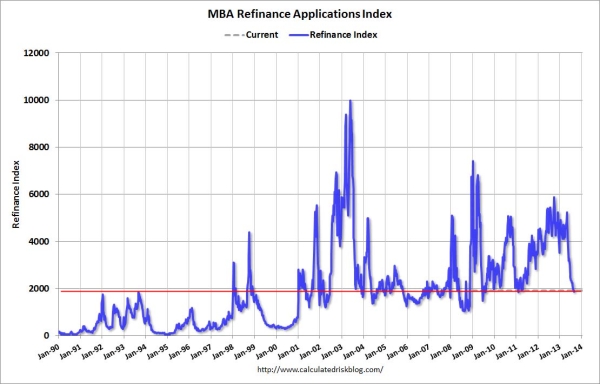

Trend 4 – Banks to take hit in refinancing gravy train

Banks were enjoying a big refinancing boom courtesy of the low rate environment but that will definitely change as rates go up:

We are seeing as much refinance activity as we did in the pre-bust days of 2007. What is fascinating with the above chart is how much refinancing occurred during the bust courtesy of the Fed. So what occurred was the Fed was helping current owners that are already heavily subsidized via tax breaks but also, were probably never going anywhere to begin with. The refinancing activity for troubled owners never showed up until late in the game and many ended up losing their homes (now probably owned by a big hedge fund).

These trends, in particular higher rates, definitely show that the current pace of higher prices in the housing market will be unsustainable. We are already starting to see inventory build-up and price reductions increase (although some of the prices being asked are ridiculous to begin with but buyers will go for the max of what the market can support). Investors have been willing to bid this game up. How much longer can this go on?

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

70 Responses to “The mortgage rate shuffle: Higher mortgage rates already having impact on housing market. 4 significant housing trends to look out for as 2013 enters the fall selling season.”

The Fed’s goal of helping average families? You have that totally wrong. The Fed has no such goal. The Board of Governors of the Federal Reserve System and the Federal Open Market Committee are of the banks, by the banks, and for banks.

True in my experience…QE meant that I could not buy a house even though I had a big down payment, a preapproved loan, great credit, etc….none of that mattered when competing with 100% cash buyers

“(Reuters, 9/6/13) While the unemployment rate fell to 7.3 percent, its lowest since December 2008, the decline reflected a drop in the share of working-age Americans who either have a job or are looking for one. That participation measure reached its lowest point since August 1978, a further sign of underlying economic weakness.”

House prices cannot continue to rise without a healthier jobs market, which is just not there.

I am a loan officer and have been pre-approved myself for over 1 year. I have been outbid on over 10 offers, usually all cash. I tried to get aggressive and the last 5 offers were over asking, but as the bids escalated I refused to continue to be sucked in. Now prices are 20% higher and rates are higher as well. Also, due to the spike in mortgage rates, my income has now dropped, so I may not be able to qualify for as much house now. Refinancing has all but dried up, and there isnt enough inventory to allow for the Purchase market to make up for that loss. Thats what you get for trying to be prudent and acting rationally. I can tell you that we are definitely becoming a nation of renters, and many not by choice. I also believe as others have pointed out here, that places like So Cal will probably continue to have these mini boom and bust cycles. I guess if you truly think you will live in the same home for 10 yr + it might still make sense. But what we have witnessed over the last 5 years has my re-thinking everything when it comes to real estate.

Sure it does. It makes a huge difference if you offer them substantial amount more than the cash buyer. You’re probably trying to compete on the same price range and of course you can’t win against them. They’re borrowing money from the govt for 0.05% so that they can turn around buy homes and charge rent at a huge profit margin. It’s a shady way of govt bailing out the greedy.

Marco you state that you were too prudent. Based on what you say I believe you were not prudent. If your income fluctuate so much and it dropped so much recently, the fact that you were not able to buy was a blessing in disguise. Otherwise, you would have lost the house to the bank along with the down payment.

@ReplyToMarcoT: I wholeheartedly agree with your assessment. Of course if he had wont he bid on the house, moved in, and then couldn’t afford the payment.. he would’ve blamed everyone else. It was the system, it was the bank, it was everyone except him. He would’ve been the victim.

@ReplyToMarcoT: I wholeheartedly agree with your assessment. Of course if he had won the bid on the house, moved in, and then couldn’t afford the payment.. he would’ve blamed everyone else. It was the system, it was the bank, it was everyone except him. He would’ve been the victim.

Correct! No surprise there, given the share holders of the Fed are the too big to fail banks. Why wouldn’t they use the Fed to serve their own interests, isnt that what any shareholder uses a corporation for?

uhh… pretty sure the Doc’s being sarcastic on the “helping families” thing.

This.

While I don’t disagree with the Doc’s assessment… there are still some crazy stupid sales going through. Here’s an example in Westwood:

http://www.redfin.com/CA/Los-Angeles/321-S-Thurston-Ave-90049/home/6828409

The house is right next to the 405 – less than 100 feet away and no sound wall. My wife and I went to see the place on a “quiet” Sunday and when I opened the car door, I thought there was another vehicle barreling down the street behind me No, it was the roar from the 405. The house (and back yard) have an unimpeded view of the 405 and it was loud. It was loud inside the house as well.

We thought it was overpriced at $795K; the house would need a lot of soundproofing. Yet someone (or some entity) bought it for $1,011,000. I like the extra $11,000. Was this the result of two idiots engaging in a bidding war?

“I bid a meeelion dolla for that house!”

“Screw you pal, I’ll bid one millyun and 10 THOUSAND dollars!”

” Amateur! I bid a meelion dolla and 10 thousand and one thousand dolla!”

“OK buddy, you win… I think I see a rundown condo that I can overbid on.”

Maybe noisy, but that house is almost perfectly situated for UCLA students (and their rich overseas investor parents). Plenty of market still there that doesn’t necessarily respond to our quality of life issues.

Well, that’s in Westwood. Not anyone can live there… it is not a place for paycheck to paycheck folks. Westwood is for the rich, weather local or foreigners.

$1,000,000 is legit in Westwood. If you are a wage earner Westwood is not for you. It is for ballers

Even Santa Monica. I have family that bought in late 80s and they all live in Million dolla homes… and are blue collar folks whose kid now have graduated from UCLA and USC… but things change my friend.

Right, but I think Billy Joel said it best when he sang “If this is moving up, I’m moving out!”

That’s my sale you tool and it was fairly priced. Go screw yourself. I do flips like this all the time and the little effort I put in for a months work increases the value 60%. It’s a proven technique, watch and learn.

@James

Count your lucky stars you live in a society and culture that has enough ignorant people to keep an asshole like you in business.

Don’t even need all those fancy charts! Simple math tells it all.

$300k PITI @ 3.5% = $1622

$300k PITI @ 4.5% = $1795

If people could afford the extra $170/mo, they probably would have went for a larger loan as it’s the American way. So assume $300k is the max at their $1600/mo budget. When the interest rates go up to 4.5%…

$269k PITI @ 4.5% = $1637/mo

That’s a 10% price drop right there.

Better hope rated don’t go to 7%, that’s $200k PITI @ $1600/mo

Hey, we actually just bought a place on the same street..

1mil for this area is bottom dollar, lowest of the low.. just because it’s right on a highway.. Btw, nothing good insulation + windows can’t fix.

We are not AS close to the highway, but it’s totally quiet in our place.

I would never ask this in person, but since this is an anonymous forum, I’d love to know how much your house costs, how large it is, how much of it you financed, and how much you make a year. I’m trying to gain an understanding as to how people do it in this town. If I’m prying too much, I apologize. Thanks!

What about health problems associated with poor air quality near freeways?

Thurston is a winding street with some beautiful houses and indeed, just down the street or around the bend, trees, sound barriers or other houses completely attenuate the freeway noise (but not the particulates…).

This house is NOT on that part of Thurston.

Walk by it. Not only is the noise awful, the hillside under the house was being maintained/strengthened by the city. I don’t need to pay $1M to know what it’s like living off the 5 or 10 down in the ghetto.

Some rich parent may have bought it for their spoiled You See Lots of Asians student. At least the kid can have wild parties at the house until dawn and never bother the neighbors with the noise…

We are on the brink of buying a SFR in Long Beach in a nice neighborhood. It is a short sale offered by Wells Fargo for $650k. Our biggest question is, “Is this a good time to buy?”, followed quickly with, “Will there ever be a good time to buy again?”. What do you think, Dr. Housing Bubble? Thanks

Kris, I know you are trying to get Doc’s opinion, and I will put my 2c out there. Good time to buy is when everyone including their mother-in-law are selling. A place to live is a very basic need for anyone. If you can find something you like within your reach, why wait? Reading the charts will confuse you. If you take a look at those last two charts, don’t you see it’s going down and pointing to zero? They may make a bit sense to aggregates, but They do not make much sense to individual.

@Kristen — No one on this blog can answer your questions with any dependable degree of accuracy. Period.

You need to make the best decision for YOUR situation. The relevant components of that decision would include:

— buying a house at a price you can comfortably afford…..even with a job loss.

— you can reasonably foresee that you’ll be in the home for 10+ years (b/c selling costs are high and will eat you alive for short-term ownership).

— not over-investing in the dang thing with all the stupid bells & whistles people need to buy in order to feel accepted by their peer group. In other words, don’t install an A kitchen in a C house, while leaving everything else at the C level. You’ll lose money.

Trust your own gut on this big purchase and *remain sensible*, that’s all you need to think about.

PRC,

Horsesh** people can’t predict what’s going to happen. The numbers are right in front of our faces. This is another bubble and it’s popping as we speak. An absolutely horrible time to buy. Here’s one question I pose: if one is an investor and can get a treasury bond for a now 3% return (versus 1.5% back in the spring) compared to buying investment property where one can hope to get a 3-4% return, which one would you choose?

@Gordon – No Reply link in your comment box so, posting here. Your response is very simplistic. You are without a huge amount of detail related to Kristen’s circumstances and you will not be the one holding the bag for however choices work out for her.

You also do not have the full picture on the investor buying. Neither do I, but I know there’s more to the story of this unprecedented institutional buying of residential real estate. The big fund companies have likely gotten guarantees from the Fed, ETC….and have probably got their asses better covered than any you people know.

Here’s the story to read today, folks. And I keep thinking THIS is one of the reasons so much money is flowing into hard assets. Some have been asserting for years that this type of thing is coming the USA way…. that it’s only a matter of time.

http://www.zerohedge.com/news/2013-09-06/poland-confiscates-half-private-pension-funds-cut-sovereign-debt-load

You can also keyword search: cyprus banking crisis for more possibilities of what could be in store for us. In that country the Feds skimmed straight off of bank deposits. So, it is indeed possible that if someone overpays by 5 – 10% on their home by buying now, it could be the CHEAPER deal b/c you have to live somewhere and rather than let .GOV confiscate your money and provide you with “future guarantees”. Bleeehh.

This has also been my hunch. “Cash is trash” and is better tied up in a hard asset so if/then/when a dramatic currency debasement happens or retirement accounts get confiscated. Real estate for the big players, gold/silver for the small folks as far as investments go.

Anyone who has researched Agenda 21 or stuff about the UN knows a one world currency is the end goal for the bankers. In order for that to happen my guess would be the central banks would need to bring all currencies to roughly the same value and then switch over to a new monetary system. Something tells me we will see WW3 before that happens.

This also makes me wonder if gun confiscation is priority so there isn’t a massive civil meltdown if/then/when something like this happens. Or maybe all of this gun hype is set up to get more people to buy guns so when chaos ensues, the military doesn’t have to round us up because we’ll all be shooting at ourselves from lack of food/water supply. It only takes 9 missed meals before a human becomes aggressive – chew on that next time you’re in the grocery store.

None of these major events are by mistake – it’s a well laid out plan that has been in place for years. Just look at all of the people against the Syrian war, pissed at Obama and Communist Putin is in a way on the same side as the American people. It’s clear as day what’s happening. USSA here we come – Putin the Communist Dictator as the savior! As George Carlin put it “it’s a big club, and you and I are not in it”

Short sale + 650K + Long Beach = Head exploding

lol

@Niner — you’ve been quite the researcher. Thought you’d appreciate this 2 min video….it’s an eye-opener. And doesn’t seem like a stretch to me. Particularly given all the ‘expectation conditioning’ coming out of the White House the last couple of weeks related to the next country on the list.

By the time we pull the trigger in Syria, I’m guessing most people will consider it a foregone conclusion, just like it’s intended that they see it.

http://www.youtube.com/watch?feature=player_embedded&v=9RC1Mepk_Sw

I lived in LB for many years. LB has many pockets..of decent places and some horrific pockets of completely scary ghetto places. On top of that the school system in LB was a major factor of us moving out. LBUSD is good for putting spin and trying to make themselves sound much better than they are. The truth is thousands have exited that school district over the past 10 years.

Does anyone have any sources for how the bond market “works”, in particular why interest rates are rising despite FED interference, and how to tell if they’ve lost control of it (pumping more $ won’t work anymore) ? The whole thing is a mystery to me but I hope interest rates rising means lower prices in the future, I guess it may cause an inflection of investor sentiment which is driving this madness.

Max, interest rate is the price of money. When interest rate is low, money is cheap. Everything else money can buy will go up in price. When interest rate goes up, money is more expensive. Everything else SHOULD go down in price. That’s really about it.

Now, in recession, demand is low, people lose jobs, money is dear. In theory, the interest rate should be higher, so that everything else is cheaper, and people with money can buy stuff cheap. But in reality, our Federal Reserve is fighting with last breath to lower the rate to zero or even negative, and supply with unlimited money to the banks, and desperately trying to raise price of everything. So, interest rate is lower in every recession to support asset price. That’s reality, in the past, present and will be in the future.

Fed will not lose control. Who can fight with Fed that has a finger on the print button? Who can fight with US ? It comes back to US dollar. The value of USD is the question. But take a look around, what else is there? Aussie dollar? There is big capital flow from one country to another, and US is always the one to go when in trouble.

Real estate in CA is in recovery. Nobody likes the price to shoot up so fast. But nobody liked the price to go down so violently either 6 years ago. So the price at the low 6 years ago was NOT normal. Market has its own momentum and mechanics. In order for the price to go down, it will have to be a forced sale. Otherwise, the price will not go down, not in a dramatic way. Currently, the momentum is going up, like what Robert Shiller says. Future is unknown to anyone. You need a place to live. If you find something within your reach, get it. Do not read too much into the charts. Those charts are not reality. After all, it is a place to live, a very basic necessity.

“Nobody liked the price to go down so violently either 6 years ago.” Are you out of your mind? What buyer doesn’t want prices to go down? All you are doing is arguing that high prices are good for everyone. BS. Low housing costs are in everyione’s interest! Sure, some may lose money from overpaying (which is what I view as the current state of affairs…house costs not in line with income). I’d say everyone can benefit from low cost, affordable housing. The “extram money” that would be wasted sitting stuck in a house could go into the economy in a different place, and all would be well. High costs of housing are the problem, not a fait accompli or a solution.

Prices won’t go down?

That is a laugh. When banks finally have to dump their foreclosures on the market and supply exceeds demand, prices will drop. When Wall Street sees they can make more money in another investment rather than REO-to-Rent, they will sell and prices will drop, when interest rates go up so much that folks cannot afford the payments, prices will drop. When families realize their jobs are not secure for 5 years, let alone the life of a 30 year loan, priced will drop. What planet are you on?

“But nobody liked the price to go down so violently either 6 years ago. So the price at the low 6 years ago was NOT normal.” ?

The price should’ve not been that high and inflated to begin with. Psychologically you may think is good after it was so high. a 600K house in Santa Clarita is not normal just because it dropped from 850K

When I sell a car I always start with a high price, and while negotiating I reduce it substantially so it seems like a deal, but in the end it’s just a fair price. but the buyer thinks they got a deal…

>>Nobody likes the price to shoot up so fast. But nobody liked the price to go down so violently either 6 years ago.<>> In the classic assets mania, markets outrun any rational valuation based on yield or cash returns. Real estate comes to sell at absurd prices on the expectation they will appreciate to still more absurd prices.

And they do. They defy gravity, moving from one lofty new high to another, month after month, year after year, long enough to lure otherwise prudent people into mortgaging their gains to reinvest in the inflated assets on margin. Before the market can top, near enough everyone who could conceivably be drawn in must have already become a buyer. And debt levels supporting the asset prices must be many times higher than any that could conceivably be serviced out of the cash flow yielded by the investments themselves.

Then comes the bust. Just as everyone has come to count on the idea that the lofty asset valuations were permanent, there is a crash. This tends to happen fifteen to twenty years after the inital property rights shock.<<<<

Try the website zerohedge at:

http://www.zerohedge.com/news/2013-09-05/10-year-breath-away-300-just-50bps-left-until-disorderly-rotation

The reader comments at the bottom of the articles are usually entertaining…

One can find no one better explaining the current state of bonds than Bill Fleckenstein – http://money.msn.com/bill-fleckenstein/post–is-the-end-of-an-error-coming-soon

@Maximus

A.) Bonds are loans.

B.) The ten year treasury is known as the “benchmark” and quoted almost every day. Most mortgage backed securities are chopped up into ten year bonds and thus competes directly with the benchmark ten year treasury. Whichever direction the ten year treasury goes, the 30 year mortgage rates follow within 30 to 60 days. As a general rule, the 30 year mortgage rates are about 200 basis points (2 percentage points) higher than the 10 year treasury rate. With the 10 year treasury closing in at 3% this means that the 30 year mortgage rates will be hitting 5% within the next 1 to 2 months.

C.) The Federal Reserve’s QE at best knocked the interest rates down by 50 basis points (i.e. 1/2 of one percent). The official purpose of QE was to stimulate the economy and help with unemployment. The real purpose of QE was to get garbage mortgage backed securities off of the balance sheets of the banks since no one in their right mind would purchase these radioactive “assets”. Thanks to artificially constricted inventory banks have been able to liquidate a number of these toxic loans from 2004 to 2008. But there are still millions of bad loans lurking out there in the shadow inventory.

D.) The Federal Reserve controls the Federal Funds Rate (aka the overnight rate). This affects savings account, money market, certificate of deposit and short term interest (i.e. credit card, car loans) rates. Under normal circumstances this should not affect long term rates however since money is fungible (and nothing more than a journal entry in today’s electronic banking world) banks will use the overnight loans to roll over and float bad mortgages.

E.) The biggest factor in the very low interest rates of the last 10 years are baby boomers and their retirement funds. When the stock market crashed in the year 2000, baby boomers pulled their money out of stocks and put them into bonds. This is a very normal investment strategy (invest in the stock market when you are young and rotate into bonds as one nears retirement. This is cash preservation.) Now that baby boomers are retiring, they will be pulling money out of the bond market. As baby boomers age you can expect interest rates to slowly go back up to historical averages simply because as boomers drawn down their retirement and pension funds there will be less money chasing after bonds and other assets.

More anecdotal data to suggest this is all coming to pass!

Each day now, I get at least one and maybe even two or three Trulia/Redfin Alerts, all with price [reductions] in the I.E. region which I am currently tracking.

This corresponds also with a report a few days ago from a forum member in the greater Sacramento area, who reported the same–increased inventory, lowering of prices and longer time on the market. While there will still be some areas/neighborhoods which will be slower to react/respond to the new trajectory, many other modest areas are already showing the shift in direction.

The fundamentals are just not there!

I will be really interesting to track this, going into the fall/winter, and on into next spring.

While I’d love for this to happen, I don’t see any reduction in asking prices yet. In my little chunk of whitebread eastern Ventura County (that the wife rightfully refers to as Stepford Oaks) prices just seem to keep rising. I should be pleased as my little 40 year old 1200 sqft crapbox is now apparently worth half a million bucks again – and any place I’d consider moving to is now a cool $750K.

Unfortunately bears on this forum like myself have been wrong time and again – and may very well be wrong this time too. If Ma and Pa baby boomer don’t decide to sell en masse inventories could be constrained enough to prop up prices even in the face of increasing rates. We’ll just have to see over the next year or two.

Oh well, it was fun to dream about moving for a few years there. I guess I’m going back into hibernation until bubble 2.0 pops (if ever).

It will take a while for sellers and RE ‘professionals’ to admit that higher mortgage rates are going to translate into lower selling prices. Sellers and agents are going to be very resistant to dropping prices and admitting that RE is slowing down. It will happen but will take months. You DO NOT want to be a buyer now. You get stuck with unrealistic selling prices and high mortgage rates.

Apolitical scientist, I am right there with you regarding being a long time bear who was wrong time and again. I finally realized the “great collapse” wasn’t going to come and pulled the trigger about a year ago. The desirable areas in coastal California are a unique case study and these areas truly ARE different. The regular economic laws we constantly hear on this blog (local incomes, jobs, etc) DO NOT apply to these areas. The powers of supply and demand and the various forms of wealth of people buying in these areas will trump the standard economic laws that are present in most other parts of the country.

As you say, baby boomers aren’t selling and the limited number of properties that come to market in the desirable areas have no problem getting bought. There still is plenty of money out there. I do not see this changing anytime soon. Coastal California RE is now a global market, this truly sucks for the local middle upper class.

Hibernating bears will eventually be right despite the glad flash happy spin realturd decade plus bull run. Where are all the incomes that can afford a 2000 sq. ft. tract home popout in SoCal suburbia with a 30 year fixed and jack diddly down? Are they all betting on income inflation in the next 5-10-15 years. Awfully bullisshhhh….it would be nice see incomes come in line with the current fantasy world of house poor shlub valuations.

I’ll hibernate and eventually leave the state.

I have several older friends who are on the upper edge of the boomer generation and have retired or close to retirement. Oddly enough none of them who are homeowners have talked about selling their home and downsizing… have we overestimated what the 10,000 boomers who are retiring every day will do with their owned/occupied home?

Boomers I know are just looking for one last big score. Their lives were marked by always rising home prices, increasing stock markets, reliable pensions, and relatively good employment opportunities. They don’t understand the concept of losing financially because for the most part, it hasn’t happened to them.

I know people in that generation who have put homes on the market recently only to remove them when they see the prices offered are a lot lower than expected.

Let us get this straight! The “bears” on this forum DID get it right! We were 100% correct that a bubble was forming and was going to crash and it did.

What happened afterward was a changing of the rules of capitalism. If the rules had not been changed it would have played out to the T as we predicted. Whenever you CHANGE THE RULES, the outcome will be different and when the rules are changed like never before, as they have, the outcome is unknown.

Capitalism was put to bed in 2009 and something different replaced it. The printing of close to 4 trillion dollars for asset purchases and the suspension of market to market accounting certainly changed the out come we were expecting. Rather than a collapse in the bubble, the collapse has been made to look as a buying opportunity and now prices are only back to so called “fair value”. That is what suspension of Capitalism along with 4 trillion (and counting) will buy.

That said…..It would be very foolish of you to think for a second the outcome of all this is going to be a Hollywood happy ending.

I’ve been watching Thousand Oaks and things are starting to change. Though I haven’t seen much in terms of a major reduction in list prices, homes aren’t selling nearly as fast as they were a few months ago and only the best priced inventory seems to be moving. One strange thing I’ve noticed about Thousand Oaks is that a lot of the homes for sale are empty, that’s be the case all year.

As far as the baby boomers, I think the issue there is that a lot of them are postponing retirement. From the ones I know, even when they do retire they often take up side jobs to supplement their income. But…..as their health starts to fail this will come to and an end and they will have to sale. As the boomers start to hit their 70’s in the next few years I think they will start to put more downward pressure on California real estate.

>> If Ma and Pa baby boomer don’t decide to sell en masse inventories could be constrained enough to prop up prices even in the face of increasing rates. We’ll just have to see over the next year or two.<< The banks and the country surely needs it to happen. A 50% house price crash, then 30 year mortgages at. If they write $3 trillion in new mortgages to younger people buying Ma and Pa's crashed house price down 50% from new peak, the banks get $6 trillion back over 30 years at something like 6.3% mortgage rate. Plus a much healthier mortgage book for the banks, fewer mortgages going to turn bad with lower purchase prices, with younger buyers more able to afford their repayments, and have money left over to spend in the economy.

>> If Ma and Pa baby boomer don’t decide to sell en masse inventories could be constrained enough to prop up prices even in the face of increasing rates. We’ll just have to see over the next year or two.<< All these houses owned outright are REALLY BAD for the banks. No one is paying any mortgage debt to them on all these houses owned outright. There will come a time the banks want to force a crash so younger people, in their millions, can afford to buy and take mortgages out on them.

It’s still about rent parity. As long as it’s cheaper to own than rent, people will be pulling the trigger.

And…..as long as it is cheaper to rent by 50%, people like me will not pull the trigger.

You must live in Phoenix if you can own cheaper than renting and if that is the case, prices are still much below peak. The people on this board mostly live in Ca. where peak prices have been exceeded and almost every case it is cheaper to rent than to own and in extreme cases such as mine, by as much as 50%.

AND……here is a common example http://www.ziprealty.com/property/4082-MOUNT-ACADIA-BLVD-SAN-DIEGO-CA-92111/10060845/detail

The seller states the unit is currently rented for 1800 a month ( I am aware of a recently rented unit for 1850 so it is fair market value more or less) and you can buy it as an investment for only 2650 a month plus upkeep! Or, you could be the renter in the unit, give up your 1800 a month with no upkeep and plop down 39K (opportunity cost lost) so that you end up with a payment of 2650 a month payment plus upkeep.

What a deal! For only 39K of your hard earned savings you can increase your monthly cost to live 850.00 a month, plus upkeep.

I am willing to call the housing bubblet burst. The housing bubble was the centerpiece of the fed’s QE program that they spent trillions on-it help rich investors buy homes and to bid them up. No sooner does the Fed start talking about tapering QE rates rise and mortgage apps start to fall-end of housing bubblet.

To get it going again the fed needs to double down on QE.

Would love to believe the DR but here in Orange County, homes are still very short of supply and still moving off market very quickly. We are literally picking at the bottom of the barrel right now (homes right next to Freeway, etc etc.). We are looking at the $500K price range for single family house and have been outbid with ALL CASH buyers for anything that looks decent.

@G

Only because this is totally anon. 🙂

We make just over 400k between the 2 of us.

House was 1.4mil. We put 300k down and financed the rest @ 2.5% 7/1ARM.

My payment is $4425/month + insurance + tax = just under 6k.

If you figure tax benefit and loan paydown schedule it’s actually much cheaper vs. our rental that we used to pay 4k/month for.

Thanks so much for getting back to me, Mik. That gives me some perspective.

Mik, thanks for sharing. As I have suspected, there is still plenty of money out there. In these super desirable areas, we are seeing all cash, huge downs, wealthy parents helping kids, people with very healthy incomes, etc. For the people waiting for the big collapse so they can waltz into these areas and buy on the cheap with their 150K income, that’s simply not going to happen.

As a little anecdotal evidence, a house just sold down the street for 800K. I met the new owners, a DINK couple (pharmacist and engineer). Likely around 300K income. That’s your competition here in desirable parts of CA. The amount of money that exists in some pockets is staggering.

LB, wish I had a dollar for every time you use the term “desirable area” in your posts on this blog.

Drinks, you’d be a rich man if that was the case. I think we can all agree that most of LA sucks in a big way. There is no way in hell I would even consider living in most of these areas. Everybody wants to live in the desirable areas, but not everybody can afford them and then the substitution effect comes into play. I want to live Malibu (too expensive), Palos Verdes (too expensive), Torrance (too expensive)…before you know it you end up in Norwalk or the IE where the numbers make sense. I think everybody on this blog wants to live in the “desirable” areas, so let’s focus on that. Flyover country is a far better alternative if you are stuck being on fringe in a so-so area. Let’s just leave it at that.

they are simply making their robbery complete. The equity, or I should say would be equity that would have belonged to the borrower over a long. Of time instead was jacked up to bubble prices by the banks so that they could sell their mortgage backed securities at huge inflated underlying asset value and now are like vultures coming and picking the bones they made trillions of dollars on there saft during the bubble years and now are simply collecting up the bones to use as the assets that are backing the over quadrillion derivatives that are currently outstanding. What will be interesting is with when interest rates go up it will start to become profitable for the banks to begin lending again. And when I say lending I mean creating purchase-money contracts so they can securitize them and rip us all off again. Its all rigged its all manipulated laws were created for changed years ago over a decade ago in order for them to perpetrate this massive transfer of wealth. It was planned! And executed! We are the victims of the biggest transfer of wealth done purposefully and intentionally by our big banks.

When the rates and soft market force a big enough price drop, will the investors be left hold the bag of steaming overpriced real assets or will the fed bail them out too?

Will they be TBTF part II? Can’t wait to see easy corporate/fund money eat the losses as home prices become in line with the salaries of those who will actually live in them.

I am probably dreaming in the new “financially planned and managed economy” here in the USA. We don’t have Stalinist production goals, instead we just have goals for bank solvency using interest rates. How many more Nobel prize economists will it take to fix this mess?

De regulation has done wonders. Sure glad glass-steagle is gone and forgotten.

Maybe with a bit of stagflation in the future we can get back to some Volker era rates in the teens. That would put the squash on those investment properties either for rent or purchase.

whoa, this is nuts… check out this flip by my quick calculation is a 60%+ mark up in like 3-4 months

http://www.zillow.com/homedetails/16211-Via-Pacifica-Rancho-Santa-Fe-CA-92091/16766938_zpid/

San Diego

On the market for 3 weeks. Looks like they will be left holding the bag……LMFAO.

I remember the year 1980 when interest rates were way up and prices were rising way over the mid ’70s. Inflation was the key, and it was roaring out of control. Then they put the brakes on inflation, and eventually rates dropped. In the long term prices went up even with lower inflation. We bought in ’80 for $78K and sold in ’90 for $156K.

with cash buyers bidding up home prices the banks are content with the current market. they could care less about the “working man” and his little down payment. now wait for the cash buyers to dry up and then you will see a change in the market.

What will happen in October when the market is historically at its lowest? Especially with sequester and the need to raise the debt ceiling we may see the perfect storm for the fed to say never mind to QE and fan the flames for more housig hysteria and mania.

I would say it can’t continue, but there seems to be a boundless appetite for screwing the average Joe.

You are absolutely correct yakyak.

Leave a Reply