The Boomerang Generation: Older Millennials are pushing increase of young adults living at home.

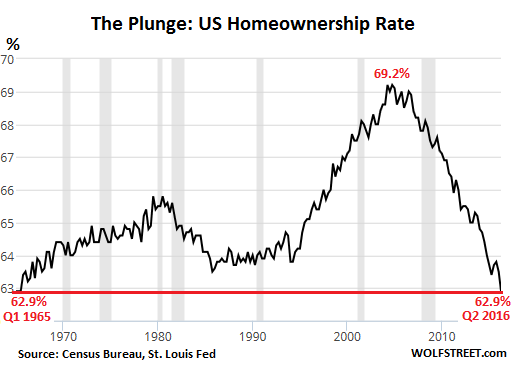

The latest homeownership rate figures show an interesting dichotomy to the housing market. While prices are up, the homeownership rate is down. And down significantly. The homeownership rate is now at levels last seen 50 years ago (the latest figures are the lowest in a generation – each update seems to bring a new low). This flies in the face of all the house humping that is being pushed out into the market. What we do know is that Millennials are simply not buying numbers in any “pent up demand†form. In fact, a record number of Millennials are living at home with at least one parent. The data is interesting since the drive is being pushed by older Millennials, those that should be buying. Younger Millennials are likely in college accumulating back breaking levels of debt. There has been research showing that student debt is a hindrance to buying a home. So are we simply creating a new generation of boomerang kids?

The homeownership rate at another low

I know it bugs some people but the reality is, the homeownership rate is now at a 50 year record low. This flies in the face of the thesis that this move up in housing values is coming from some economic miracle. The volume of home sales is tepid at best and weak for new homes. What you have is the after effects of a manipulated market. But people are waking up to the game and you see this in our very unique political season.

Here is the clear indication of where homeownership is going:

It seems like we will have three classes of people in this market:

First, those that can buy and will buy

Second, those that can rent and will rent

Third, those that can’t buy or rent and will live at home

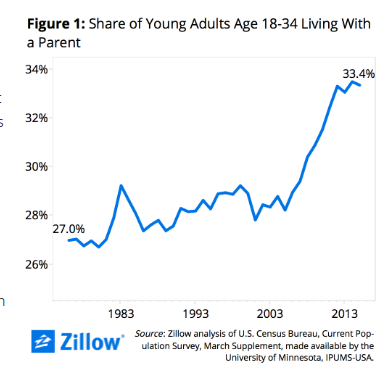

That third category is where many Millennials are falling. Take a look at the latest data:

Does that look like pent up demand? And this trend started in the early 2000s thanks to financial products that turned the entire housing market into a casino. This big change has created a system where it is hard to determine where the new normal is. Taco Tuesday baby boomers are now griping that their kids can’t buy a home in the area they live in. And many are having grown adults living at home making lower wages and carrying large levels of student debt.

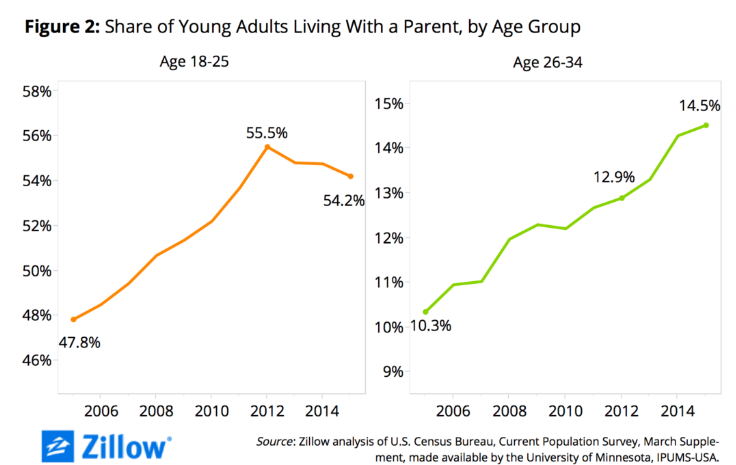

You can see this clearly when we break out the Millennials by age:

As it turns out, the big push is coming from older Millennials. This makes sense in the context that never in our history have we had so many people going to college as a percent of the population. College students for the most part are renters and living away from home. But once the college experience is over, millions are finding their way back home at an age range that was prime for home buying.

It will be telling if this continue. What is certain is that this likely will encourage higher rents if the economy grows or even maintains. But rents also react quickly to economic downturns in the form of vacancies. These Millennials will likely move out into a rental before buying. The 10,000,000 new renter households over the last decade gives good evidence to this transition.

If this was true pent up demand, they would have been buying since 2009 (the recession officially ended 7 full years ago). Yet the house humping continues and in Los Angeles, the homeownership rate is even lower with the majority of people being renters. It is not even close:

53.6 percent of L.A. County households rent. Back in 2010 it was only 51.8 percent. So the trend to renting and living at home is happening and Millennials are a big part of this change.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

171 Responses to “The Boomerang Generation: Older Millennials are pushing increase of young adults living at home.”

1. only americans should be allowed to buy

2. only individuals should be allowed to buy

3. no property tax for the house you live in.

4. 5% property tax rate for second home, 10% for third etc.

Too socialistic for my tastes. Just bar foreigners from buying and you’ll see the numbers come back to reality. Or at the very least limit it. Why the hell are Chinese nationals allowed to buy 2 or 3 homes in all cash in Irvine, CA? Something doesn’t smell right there. As long as they’re allowed to launder their money via all cash real estate transactions, you’ll get the market we have today. Till then, prices will continue climbing until either regulations tighten up or the cost/benefit of laundering money through outrageously over-priced real estate reaches it’s threshold.

The lights have officially been turned back on.

“U.S. Title Insurers Required to Identify High-End Cash Buyers in Six Major Metropolitan Areas”

https://www.fincen.gov/news_room/nr/html/20160727.html

The same thing has been going on in the Glendora and Claremont areas for a couple of years now and the amount of building has exceeded that of the last building bubble. These are half million $ (that being the low end) plus homes the majority of which are not being bought by the domestic buyer.

Don’t bet on anyone stopping foreigners from buying U.S. real estate … it is part of the con making up this GDP numbers … we’d be in minus growth without those purchases! And, besides, who is going to keep those property taxes flowing into California’s coffers, feeding all those fat politicians? Believe me, no one in Washington, Sacramento, L.A., S.F., etc., care that you can’t afford a home, or are paying 50% of your income on rent, as long as they get their pockets lined!

Why are the Chinese allowed to buy? Simple, I’m a seller I want the maximum return on my “investment.” Why would I vote for any politician trying to stop someone from giving me MORE money than an American can?

Or implement a 15% tax on foreigners purchasing property, like they just did in Vancouver. http://www.zerohedge.com/news/2016-08-03/deals-are-collapsing-vancouvers-housing-bubble-has-just-burst

@JNS You’re absolutley right. Those tax dollars are coming in at numbers that domestic buyers just can’t cough up. However, if the only language politicians speak is “money” how about getting them pass a tax on foreign buyers with increasing brackets for every additional home they buy? Vancouver just passed a 15% tax on foreign buyers effective immediately. Why can’t the state do something similar? It’ll pump more money into the property tax account, stabilize the real estate market to a more realistic level and allow more domestic players to enter the market. Sure they market might come down a bit which will affect the short term tax account but it’ll avoid a complete crash (or soften the blow) or at best stagnate the market enough for inflation to catch up without undergoing a crash in the first place. A great long term solution if you ask me. As for taxing the domestic buyers for purchasing multiple properties…I’m sorry, I thought this was America!

‘All cash’ is a money laundering scheme for criminals too, very handy as no-one is asking where the million or two in cash came from.

But when I take 2000 euros to bank they demand an explanation for its existence or otherwise no way and ‘ECB (EU central bank) requires us to do this, it’s similar system in the US’.

Yea, right.

Follow the money. Americans are broke and cannot afford to buy. In this situation houses will need to become cheaper, hence lower property taxes collected by the city, city revenue decreases.. Cities would rather sell the properties to a higher bidder who will be forced into larger sums of property tax payments which will pad the pockets of the city the home was sold in. It’s a no brainier. If you can’t afford to buy, figure out a way to make more money and stop whining

1) Only Americans should be allowed to buy

2) Only individuals should be allowed to buy

3) No tax on the house you live in

4) 50% tax on 2nd, 3rd, etc homes.

If there were no property tax, then another one, probably a municipal income tax, would implemented immediately. Somebody has to pay for the roads, schools, police, parks, town programs, and all those cushy pensions of municipal workers.

Or it becomes the old west with horse and buggy living again.

1. only americans should be allowed to buy

2. only individuals should be allowed to buy

3. no property tax. Recording/Stamp Tax for Real Estate Transactions

4. no income tax or flat rate income tax. Replace with V.A.T. Those who consume pay. The tax finances payroll, pension, etc.

Whatcha think?

1. only americans should be allowed to buy

2. only individuals should be allowed to buy

3. no property tax, but land value tax: https://en.wikipedia.org/wiki/Land_value_tax

4. no income tax or flat rate income tax. Replace with FAIR Tax and prebate: https://fairtaxer.com/fairtax/the-fairtax-prebate/

Lots of good suggestions, I’d add to the top of everybodys list

0. Only americans are allowed to contribute to political campaigns and only americans are allowed to VOTE!

Without that, all the other restrictions that people want aren’t going to happen. This is the reason are jobs are gone, every institution is broken and corrupt, are economy is a jenga ponzi scheme, and every asset is priced at at least several times what it is worth.

re: tahoe1780

The whole point of Fair Tax, in theory, is that its simple and cheap to administer. If you have to do prebates and other such things to make it less regressive, which you do, it loses any advantage over the current tax system.

So agree! But that would never happen…

Not as easy as it sounds. Foreigners buy properties via LLC. And with tiered LLC, it’s very difficult and expensive to trace.

What I propose is the following: Raise property taxes to 5%. If you can prove U.S citizenship, you get a tax break down to 1.2%.

re: polish paul

‘1. only americans should be allowed to buy 2. only individuals should be allowed to buy’

The problem isn’t foreigners buying its the bubble prices. Prices bubbled just fine without foreigners in the mid-2000’s. Laws to suppress home price bubbles, strong regulators to go after RE/mortgage/banking fraud, and improving renter rights would be much more effective.

I don’t like the vulture funds buying up homes and effecting home prices either but if all the above was done their effect on the market would be minimal if not made entirely irrelevant.

‘3. no property tax for the house you live in.’

This would destroy local and state govt. funding. Quality infrastructure, schools, and policing cost heaps of money!! They’d have to crank taxes elsewhere to compensate for that, like sales tax, which is grossly regressive. You actually want a progressive tax on housing where the poor/middle class pays less than the rich and the rich get taxed extra for 2nd homes and such kind’ve like you bring up with point 4.

Super low property taxes also largely benefit the rich only and will aid the formation of bubbles (see Prop13 in CA) which is all kinds of bad for the economy and anyone who isn’t rich.

Just heard on the radio, 100 BILLION dollars in foreign money going into US real estate. Be interesting to see if that money ends up buying up land in podunk areas now that the govt is starting to scrutinize the big cities.

We just need something like the “bounty” the IRS offers for those who turn in tax cheaters. A citizen discovers a foreigner owning property, turns ’em in, property is seized and sold to an American, and the citizen who informed get a reward. Very simple. That would work in podunk towns as well as in big cities.

But… but… there’s just a shortage of inventory, or something.

The only argument I can see against a bubble is that we’re entering a new feudal state. There are a ton of landlords out there that snatch up a lot of property for rental income. Converse to the charts above, I’m thinking that the amount of single family homes that are rented instead of owner occupied must be at an all time high.

The question is… is this sustainable? We know that investors are now bowing out because at these price levels, the rents don’t warrant the investment. But if the market drops 10%-15%, do prospective landlords jump back in? If not, where?

Yes, it is sustainable. In Germany, which has a standard of living at least equal to America’s, home ownership is 40%. There is no need to have such a high percentage of home ownership as the US does.

But, there are very specific reasons why Germany has more renters than owners, World War 2 being the biggest! After the allies basically leveled the entire country, they had to rebuild and the new government provided incredible amounts of subsidies to provide housing for the war torn population. http://qz.com/167887/germany-has-one-of-the-worlds-lowest-homeownership-rates/

re: Eddie89

That there are specific reasons why Germany has a lower home ownership rate doesn’t matter to his point at all. Which was that high home ownership rates aren’t needed. And he/she is right. Its not.

If it was politically feasible the US could also restructure its housing laws such that it was like Germany’s and you’d see renters rise dramatically as owners fell without issue. There is no actual economic or legal NEED for people to own their homes. People LIKE to do so is all.

40% isn’t much but you have to remember that Germany (by population) is basically a big city, like Manhattan or something: Amount of suburbs is very, very low compared to US and owning an apartment (vs. house) isn’t very popular in US either.

Single family home is more or less something you see in countryside and that shows in home ownership ratio, there aren’t so many people living in countryside.

I can’t say if one is better than the other, but structural differences explain much of the difference.

The fact remains that Germans are not possessed by the lemming-like urge to buy a house, and they have a high standard of living a a good economy. America also subsidizes housing with tax breaks for builders and buyers, subsidized guaranteed mortgages, subsidized housing for renters, etc. America does not need 65% of the people owning houses. Too many of them will lose the house and make a mess out of their life with a small financial problem.

I am a small time landlord with “5 doors” in OKC and I can barely make it. Turnover, taxes, insurance and maintenance can knock down a 9%+ ROI real quick. I own my properties but it is not the easy street people think it is. I look forward to selling most of my properties someday and earning a solid 6.5% on my money with a lifetime annuity. Remember it is not how much money you can save but how much income your savings will generate. A lot of upper income professionals are buying rental properties not realizing the real rate of return is often far less than annuity income!

Yeah I see the same thing. I am a professional and I see a lot of colleagues jumping into the real estate game. Its too late for them and they have no idea that their ROI is going to be bad and perhaps even negative…

Hi, Kevco:

Please advise where one may get: “…earning a solid 6.5% on my money with a lifetime annuity.”?

George

Kevco….not sure what you’re doing wrong, if you own the properties, this is a straight cash flow situation. Turn overs don’t cost much if you don’t have a mortgage, and don’t raise the rent on good tenants, so what if they are below market, maybe they will stick around.

These one story stucco Crapshacks are pretty durable in this climate, a small furnace, a water heater, and a garbage disposal is the only mechanical equipment they need.

I own my properties but it is not the easy street people think it is.

Very true. Inexperienced folk think that landlords just kick back, enjoy life, and the rent checks just roll in. That rent checks are pure profit, no expenses, always rolling in every month, never late or unpaid, just pouring in like clockwork.

I’d agree that being a landlord isn’t easy, but speaking from my personal experience the returns are better than other investments, if only because I suck at picking stocks. But I too look forward to the day (15+ years from now) when I can just sell all of my rentals and put the money into something I don’t have to maintain.

Tell us more about this 6.5% annuity return, including how that percentage is calculated… I am unaware of any annuities paying that kind of rate that are available today.

I would also like to know about this magical annuity that pays 6.5%. Where may I find this financial instrument? Please tell me so I can retire.

In my opinion, the hardest part about being a landlord is finding the right property. You want a property that provide years of returns without causing headaches. Buying in low-income neighborhoods usually means high turnovers and headaches. High end homes are hard to cash flow positive because of the high purchase price, are more difficult to rent out, and tend to get hit harder when the market turns. I always look for small detached SFH in working class neighborhoods with lots of trucks and service industry vehicles parked in the driveways. Plumbers, electricians, cable men, post offices workers etc. I also avoid older homes which usually require more maintenance as well as high HOA’s and Mello-Roos areas. Taxes and HOA’s still have to be paid, even if the property is vacant. Doing a proper inspection and having the know-how to make minor repairs yourself will save a landlord much $$$. Just my two cents.

re: Kevco

Huh?! Avg. property tax in Oklahoma County is effectively 1.05%.

https://smartasset.com/taxes/oklahoma-property-tax-calculator

Avg. home price for Oklahoma city in 2016 is $130K according to Zillow. Insurance costs is about $5.2K for Oklahoma city so around 4% of home value. Maintenance is 1% of property value typically. If you’re really getting a 9% ROI x5 you’re doing fine.

Annuities also aren’t returning 6.5% either. There are ones that CLAIM 6-12% returns but those are essentially scams since that would require return rates as good or better than the stock market. The typical average for annuities is still around 3-4%.

Insurance cost is 5.2K? WTF?

While annuities have their place one should mention that that “6.5% annual return” usually comes by surrendering your principal. Also most annuities you can purchase these days are not inflation adjusted. Real estate holdings, while they suffer from the boom and bust of the real estate market, do tend to rise in value with inflation and allow you to retain your principal. I’m not saying annuities can’t be useful, but I’d be very careful in recommending them as a replacement for other forms of income investment.

@Lord Blankfein

He is in tornado alley so costs are relatively high. Here is a by city break down for the whole state he is in.

http://www.valuepenguin.com/sites/default/files/OklahomaHome.001.jpg

What we also know is that “investors” have been highly active in this cycle due to lowered yield on more traditional assets and inflation hedging.

Those planning to keep all of their eggs in that basket need rates to stay low. That’s why they comment here with language to that effect. They tell us that no one could have foreseen the unprecedented reaction by central banks, but in the same breath insinuate that they foresee central banks not raising rates.

We’ll see.

Sometimes I do envy these flippers. In at $560K, listing at $918K. And what do you think he put into it, $50K? Also, it looks like a manufactured home. Is it?:

https://www.redfin.com/CA/Los-Angeles/1234-N-Beverly-Glen-Blvd-90077/home/6830355

They did add 500+ sq ft. If you consider it costs approximately $200/sq ft, that is at least $100,000 for the addition. The flippers will still get a healthy profit if they get their asking, but to be fair to them they did a lot more than just $50k of ugly green paint in this flip.

Am I just paranoid but how it comes to my mind that they didn’t bother to ask any permissions to do that addition?

Of course it’s not inspected by city nor insured as it officially doesn’t even exist.

It looks like what’s called a “pre-fab” home at the very least. Halves of the house are built then put on trucks and taken to the site, and the final assembly is done. Typically very crappy construction.

When in doubt, look for the VIN plate. That will mean it’s an RV. A pre-fab is (theoretically) a step up.

Is that a washer/dryer stack in the kitchen? The photos really leave something to be desired. Really does look like a manufactured home. Doesn’t look like a 900K home to me, but the area is desirable. I’m sure it will sell.

La’r your observations are astute and present the reality of landlordship. Thank you for your sharing your knowledge today here.

Envy today, pity tomorrow. Unless this time REALLY is different.

The biggest problem with flips is the work you can’t easily see that they didn’t do.

I almost bought a house right about there. That area is impossible. You’re isolated from markets, restaurants, etc but you have non-stop urban noise, pollution, etc. One of the bedrooms is right on BG – I guarantee it — which means so much for enjoying soft summer canyon breeze. It’s like posh adjacent for almost a mil.

Google street view shows large trees just beside the house on the street side. I can only imagine what kind of damage the roots have done to the foundations.

Assuming there are ones of course, pre-fab houses didn’t have much and built in 1947, hmm.

Housing To Tank Hard Soon!

This is what happens when you have an economy dependent on real estate to save the day. All our resources are being poured in and manipulated to keep this “miracle” going instead of focusing on the building blocks of our economy: jobs and wages. Let the market determine the interest rates and prices and take away these ridiculous financial products that encourage market gambling.

You might want to send your comment to those living in Fedland. An entity with no accountability that makes decisions based on whatever data they deem important for their decision making process.

At the time the economy was floundering I spoke with a construction company and they said that housing is what really keeps the economy going. It’s a manufacturing job.

Stop wasting time partying with friends and coworkers. Save some money and find a wife/husband for duel income. Living with parents is not good. Dont you feel like a loser.

…”duel income” …ahhaha!! Let’s hope it doesn’t come to that.

“find husband/wife”

or, you know, a roommate?

marrying a person to save on rent… truly a great proposition…

People marry for a lot worse reasons.

Living with parents is not good but marriage might be even worse. Marriage is only a good deal for a woman.

What I wrote in 2010 for my 2011 Housing Prediction article

“The longer term consequences of an unstable residential real estate market may be more serious than just the destruction of individual wealth. The ideal of middle class home ownership may be at stake. The census bureau reported a 7% decline in national rental vacancy rates in 2010, along with an overall decline of 0.7% in home ownership rates compared to a year ago. There were fewer “organic†buyers, more renters and more investment buyers in the market in 2010 and I expect this trend to continue into 2011. Are we at the beginning of a sociological movement away from middle class home ownership and towards a cultural split between the investment property landlords and their renters both of whom may have less personal investment in neighborhood security, local schools and shared public facilities compared to primary homeowners.â€

Ages 25-34 demographics are staying at home at the highest % now in this cycle

So, these are forever renters most likely

In fact, for years based on my own model work the real home ownership rate was always between 62.2% – 62.7% because census counts delinquents as owners and we have a massive demographic profile for renting and not owning ( Ages 17-29 and Ages 49-65) massive

The first time under 63% could have been forecast years ago with proper modeling work

Charts here to prove my thesis worked out

Homeownership Rates Fall Again!

https://loganmohtashami.com/2016/07/28/homeownership-rates-fall-again/

Good job on that prediction. My gut reaction is that this is just going to continue as I can’t see anything that will bring us out of it. By that I mean – we’ve outsourced manufacturing and service, plus the US just isn’t creating high-paying jobs like it used to from say, WWII to the 80s-90s. If we’re not doing the manufacturing here, then the innovation within those businesses doesn’t positively impact employees here.

It’s anecdotal, but I know that we’re losing middle and upper-middle class jobs in the tech business based on what I see in my industry. More robust software and more offshoring have resulted in fewer programmers and DBAs. When robotics/automation start taking tangible numbers of service jobs (Starbucks, TGI Fridays, Amazon warehouses, etc.), things are just going to get even more ugly for middle income workers. Even those whose job isn’t lost directly will face the pressure of decreasing wages due to an oversupply of labor. I just can’t see how this will turn out any differently.

So if millennials are spending 50% of their income on rentals now, don’t be surprised to hear Dr. HB reporting that they’re spending 60% of their income on rentals 5 years from now…

Lot of those job you are describing are done by immigrants and many here illegality particularly in California. Amazon open up a warehouse in Santa Ana. In fact if robots did those jobs about 2 million people would return back to Mexico similar to what happen when the housing bubble burst with construction.

The thing about manufacturing is there are also a lot of crappy jobs. Years ago in Orange County I worked at jobs were most of the workers were in the US illegality. Many of these jobs are now in Mexico or China, is it so bad that low skilled jobs that are not done by the native born here go overseas. Two, the tech revolution is now seeing lots of development in Tijuana and many folks hired are Americans that started tech firms. The Mexicans don’t have the skills yet. There are more openings for tech jobs in TJ than Los Angeles, but you have to put up with higher crime.

So how much real estate did you buy in 2011? Are you retired now?

The Middle Class has been brutally hammered in California for the last 40 years. All the auto plants left except Tesla Ina plant that used to be NUMMI, that used to be Toyota that used to be GM. Remember Ford in Maywood? GM in Van Nuys? How about all the aerospace plants on the Westside? Hughes Aircraft ? McDonnell Douglas? All the construction jobs used to be solidly Middle Class too. I had an uncle that used to build 2 or 3 houses at a time and had a small team. Quality houses and they put their kids through school on that income. Silicon Valley was a small part of the replacement until they decided to move the work to Thailand and hire visa enabled kids from India for everything they couldn’t move at less than 1/2 the price.

I need to look up the exact numbers but when I saw it a few months ago I was horrified. The Middle Class is 1/2 of what it used to be. We are becoming a nation of insulated wealthy and struggling masses. This isn’t good. The only thing separating Tijuana from San Diego is the quality of government. One is nice and one not so much. We’re on our way. It takes a while but you can watch it sliding. My folks raised a large family on a single income in an attractive large (4000 sq ft) Westside house and he didn’t have a college education. Struggling anxious people don’t buy houses. I wish I knew how to turn it around.

“The Middle Class has been brutally hammered in California for the last 40 years”

You’ve explained pretty well why there is a lack of demand in the western world, all the jobs that pay enough to have an American/western lifestyle have been outsourced. This is not rocket science. I was watching some talking head trying to explain the lack of demand and this c*$cksucker had the gall to say….i shit you not…”The reason for the lack of demand is Americans aren’t borrowing enough”

There is no longer any future in America when you have “experts” telling us this sort of nonsense.

Addiction to cheap and easy credit is hard to break after 7+ years of Fed-induced supply side economics. Wealth conjured out of investor over-speculation and over-investment sprinkled with some forward-demand rather than real, sustainable consumer demand.

“middle class” is what exactly? i have no idea.

Chomsky gets it better: class is basically those that give orders and those that receive them.

So “middle class” maybe just means:

Class of people that are at the complete bottom of the receiving, but certainly are not giving the orders.

Economically speaking, no idea what “middle class” means, esp. when people are crying about “kids can’t afford school” “can’t afford a SFH” “can’t afford a new car and new TV”

.. “can’t afford full healthcare for all” .. maybe if you didn’t have kids you’d be ok, maybe if you care less about SFH its all good, maybe a new car should be shunned for public transit + uber rides .. we all eat ok, right? we sure suck down that debt.

when is it really just stupid money vs. smart money wronged by the system?

when is it the system doing us over vs. stupid doing us over?

no simple answer, not even a definition. we do know it can get much worse, could get better .. lost.

I meant:

Class of people that are Not at the complete bottom of the receiving, but certainly are not giving the orders.

IF it is a seller’s market… where are all the sellers?

article from MarketWatch and comments on the shrinking inventory

http://www.marketwatch.com/story/its-a-sellers-real-estate-market-but-whos-selling-2016-08-03

There is very simple way to stop this hiking.

First – restore Glass-Steagall Act.

Second – do not allow any mortgage backed securities. The loan originator should own mortgage until it payed off (how it was before 1978, when Solomon Browsers created this kind of securities).

Alex I wish you were right. Those with money have enough power that they don’t care what party or who is in office. They have the lobbyists and the cash to make sure they are safe. Lobbyists can sit in Congress during vote taking now. Talk about a short leash. People in Congress spend over 1/2 their time working on their re- election. There’s little time for the people’s business. Maybe that’s one reason little gets done. Glass Steigel was killed by Barney Frank and Chris Dodd working with Bill Clinton so Hillary is very unlikely to re-regulate. Rope in Goldman-Sachs? How likely is that. I wish I had more hope that Trump would do more but I’m pessimistic. What to do?

The Graham Leech Bliley bill repealed Glass-Stiegel; November 1999.

‘What we do know is that Millennials are simply not buying numbers in any “pent up demand†form’

well we were told here by lord_blankcheck that “young people buying homes in the area is a ‘silly’ argument and is meaningless……”somebody is buying those home, with all cash, and millennials will just have to move if they want a home” …..he said something similar to that regarding my “which one of your kids can afford to buy the house you live in” comment.

boomers are going to have to sell….en mass…. eventually, but to who?

Why do they have to sell eventually? Lots of those boomers will either give the home to their kids or to the bank (perhaps via reverse mortgage). Keep in mind that the kids don’t have to live in it, if they don’t want to live there they can just rent it out.

Saying “going to have to sell” is a bit absolutist… Sure some will, but not all, and none of us know what that percentage will be nor when it will happen.

The percentage that rents does not include that large numbers of adult children that live with their Mama. When you add that amount, it is probably closer to 60% or more. This is very Italian. In Italy, 30 year old men live with their dear Mama who takes care of them better than any wife.

Millenial here. Expensive housing is not the only reason why millenials aren’t buying; there are plenty of us with high-paying jobs and in dual income situations. The idea of spending so much to live in the same house around the same people and frequenting the same local spots over and over just seems so unappealing. Those values appeal to older generations that want everything to stay the same. They are happy inside their stucco box as long as its behind some gates or in a desirable school district- hopefully with not too many minorities (Asians are OK).

No thanks. I’d rather have the flexibility to move and travel. Humans were nomadic for thousands of years. Although food is no longer scarce and a long winter wont kill too many of us, I believe that we have evolved to seek out opportunities by moving around.

In every generation, a certain percentage of people decide not to buy. When they reach their 40s, they realize they made the biggest financial mistake possible, and they never recover. Take a walk through a large apartment building and look at all the 40 somethings. That can be your future too.

Past performance is no guarantee of future success. Real estate today is far from a safe financial bet compared to 20+ years ago. Close 40% of incomes going to housing costs is not a good plan for retirement.

Yet you’re the 40 something spending time putting others down on the Internet. That doesn’t seem like a great future.

There’s an old saying from the 50’s involving life insurance, “buy term and invest the rest.” This was a disparaging remark against whole life policies. The same can be said for housing in this current era. I’m young enough to be a borderline millennial, I have the money to buy, but I don’t.

If you hunt around for rentals and live below your means, you can accumulate far more in this era. I don’t want to saddle myself with a mortgage. They dangle out the tax credits and interest deductions for sure. But for what? I live in California. Right now I would say houses are overvalued by about 200k. Just as in 2007. So if you told me to buy a share of stock that I think is MINIMALLY 20% overvalued and give me even a 5% discount, is that a good deal? Then I have to go to Home Depot and live in DIY hell? Then I get a property tax bill and a hazard insurance bill? No Thank you.

Nothing worse than a smug person (likely baby boomer) telling me that I’ll be “trapped in an apartment” if I don’t BUY NOW. Reminds me of all those infomercials. Don’t worry baby boomers, your time will come to sell. When you get stage four cancer and need to sell, I will be there to buy. I won’t buy your ugly hot rod though.

I’m also an older Millenial renter and I agree with what you say about flexibility. What keeps me from buying is the feeling that real estate isn’t a safe bet like it was for my parents. The risk of a $700k house losing half it’s value in the next downturn is very, very scary to me.

Exactly. It’s not. The Fed is 100% culpable for this,. The politicians are 100% culpable for the Fed. We as voters are 100% culpable for the politicians.

Yeah, I’m not technically a millennial, but I’m still in my 30s. As a small business owner who is doing well at the moment, I have a hard time grasping the concept of taking $100K+ in liquid cash and throwing it into a house, when my rent is only 13% of my income. It’s one thing to buy a few decades ago with a four figure downpayment, but a six figure downpayment is hard to swallow. Heck, every boomer relative that tells us to buy ends up admitting they put like twenty-five cents down with the GI bill, or whatever. Sure, they’ve won the lottery on a California house, but I’m not feeling that lucky.

p.s. to add to the above, outside of a tiny car loan that I haven’t bothered to pay off, because the interest rate is so low, we’re debt free, and we’re still finding it insane to buy at these prices.

While all this sounds good, you are still not addressing the realities that student loan debt has on the decision making process. You seem to not realize that in the past people graduated with little to no student loan debt which means they could afford to buy a house AND travel the world. You make it seem like if you bought a house in the past you were somehow tied to the house unable to buy a plane ticket and enjoy yourself. If you have to pay $1000 per month for student loan payments then those choices get a lot narrower.

In the 90s, I purchased beach close homes in OC and the South Bay. Now I am in my 40s, and I will be retiring at the end of the year. I will be working a part time job at Home Depot, and will spend 4 to 5 days a week at the beach. Corona Del Mar and Newport Beach to be exact. I purchased properties when II was in my 20s. You should too.

Prices were a lot different 20 years ago. You made a great choice and congrats. Not going to workout the same today.

Well, in the late 1990’s OC housing at 250,000 with higher interest rates is the same as 500,000, cheaper than 657,000 but it wasn’t cheap. There are 1 bedroom older condos even in South OC for 250,000 to 400,000, you have to look around.

Your genius has worked out so wonderfully that your retirement strategy also consists of putting others down on a housing bubble blog comment forum.

What are you talking about? He’s not putting anyone down. He’s sharing his experiences and offering advice to the generation after his. I thought that’s what this forum was about? And to add to that, he’s not far off. If the middle class is shrinking (and there are PLENTY of indications that this is the case) wouldn’t you think that the price of getting rich increases over time? Think about it, 20 years back the middle class was much stronger and most people had the opportunity to purchase homes just about anywhere including areas like LA and OC. It was cheaper to get rich back then. Now, the price of wealth accumulation has skyrocketed and it takes much more capital to make less money. Don’t think this next crash is going to be as dramatic as the last. Buy now and you might regret it in the next 5 year but you definitely won’t regret it in the next 20 years.

When I was in my 20s, I was fortunate in that an older person put me on the track. I want to share my experience with the next generation. Nothing wrong with that.

Of course this poster is putting people down.

“Take a walk through a large apartment building and look at all the 40 somethings. That can be your future too.”

Clearly the inference in that statement is that people in their 40’s who live in an apartment are losers.

Resentment of landlords has nothing to do with envy and everything to do with the impact that their actions have on everyone else.

If you have two homes, someone, somewhere goes without.

I don’t want to people-farm anyone. Even if I were transported back in time to the 90s, I would only buy 1 home.

This always makes me laugh…. JT’s comment made me think of it.

http://i.imgbox.com/4cnUdL5y.jpg

I will transcribe it here: (it’s satire by the way)

my name is nora (May 9, 2016): I always say if you want to own a home so badly go back in time and buy in the 70s. Jeez Louise.

———-

hat/tip to Bear Goggles & dgul: You’ve just touched on something that I think is a fundamental failing in our culture. The inability to distinguish between productive and parasitic activity within a market economy. We’ve been brainwashed by neoliberalism to think that any distinction between activities within a market economy is marxism.

If I create a new product that improves people’s lives and enriches me in the process, then I have achieved the pinnacle of capitalism’s promise. I have – by helping myself – helped others. If I buy finite resource with 100% borrowed money and then rent it back to someone who’s only disadvantage is that they not have access to as much debt as me, then I am engaging in completely parasitic and monopolistic behaviour. The idea that it is difficult/ unwise to distinguish between these two activities is a blindspot in our culture that never ceases to shock and depress me.

dgul: What country do you want to live in? One where any extra money is invested in property, although little new property is actually created? Where the government has to intervene to prop up the property market, because so much ‘retirement’ money is stuck in property that there would be a catastrophe if prices reduced? Where businesses galore are created to support the property industry (lettings agents, cleaning services, etc), but where no-one is actually any better off than before?

Or do you want to live in a country that encourages investing money in productive enterprise, where property can be left to look after itself, and where businesses are created that actually improve the quality of life for people? And where, perhaps, the government can step in to support employers if the economy hits the rails?

Because it is the real companies that create value, not the pretend property investment businesses, which only serve to inflate asset prices and transfer wealth from one set of people to another without any actual benefit to anyone (apart from the HPI chasing older or leveraged chasing property owner side).

Galaxy Brain: If you have two homes, someone, somewhere goes without.

Not if you rent out your second home to them.

Landlords provide — rather than deprive — homes to people.

By your logic, if a grocer has 1,000 cans of soup for sale, then 999 people must go without. So I guess the grocer should only stock one can, for himself.

son of a landlord, we will have to agree to disagree…. I will quickly set out my position, but I expect you to hold to yours, for I don’t expect you to embrace ‘the bad guy’ side of things.

Landlords ‘provide’ homes??? Have you built the homes you rent out to other people….?

It’s a sweet argument…. property investors as the “good guys” – ‘providing’ a house for rent and answering the rental demand created by the high prices and tight credit. Using a frustrated would-be buyers wages to service their investment debt (or live on from older long-wave landlord investors).

When two individuals want the same thing and only one afford the market price the act of buying is implicitly an act of outbidding. We can see property-investors have outbid would-be homeowners in this market, for many years.

Individuals who ‘invest’ in property – and owners who would normally sell up, but who hold onto properties to rent out instead – PREVENT THE MARKET FROM CLEARING, AND FROM PROPER PRICE DISCOVERY FROM OCCURRING…>>> thus significantly contributing to the situation with high house prices<<>>For the most part, landlords have created the demand they pretend to service. <<<

They provide nothing to the tenant that the tenant would not have had without them.

Yes, there probably is a residual, natural demand, but it would almost certainly be tiny. Holiday rentals and student accommodation would probably still exist in a free-market.

Most people who rent do so because they can't afford to buy, not because they don't want to, and they can't afford to buy because landlords and property investors have gone hard into the market (often at very high prices).

It is utterly specious to try and compare the rent-seeking activities of landlords with the productive service sector industries – entertainment, transport and so on.

Very few people can afford to ignore the value of their home, whatever their age, it's a key factor in everyone's decisions about housing.

We live in a market economy, of sorts. The selling point of a market economy is that selfish decisions should lead to an optimal allocation of resources.

The distribution of housing is not optimal. Why? Something is brewing in the market. If something can't go of forever, it will stop.

Life is turbulent to its very essence. Human societies, like all complex systems, are constantly fluctuating. This fundamental ebb and flow is the source of cycles in human affairs, including economic cycles. As Emerson says, there is a "deep remedial force that underlies all facts." At every point where something goes up, nature is constantly compensating by finding a way to bring it down. "Superinduce magnetism at one end of a needle; the opposite magnetism takes place at the other end. If the south attracts, the north repels. To empty here, you must condense there." Nature keeps its accounts in balance.

He only left out the part about that small loan of a million dollars.

So JT, please be specific for us. Can you point to a property or two that you think that somebody in their 20s should buy right now where the intent would be to rent it out?

I agree with your general sentiment, but I’m skeptical that somebody in their 20s can pull it off. It wasn’t until I was in my mid 40s that I had the cash to begin investing in rentals.

In my 20s, I was a software developer who did short time contract work. The income was good. I was very careful with that money. I was able to save enough to purchase homes with small down payments. For quite a few years, the rents were less than the payments, so I was kicking in the difference. Eventually, rents rose and that problem went away. Now, the rents are, on average, 2000 higher than the payments, and the gain on each property is astronomical. I think you can repeat this … I would be picking up stuff in Dana Point and San Clemente. I see good stuff down there in the 700K range … that will be worth many times that in 20 years.

re: jt

$700K home means $140K downpayment and $200K/yr income to support. Assuming no other debt (LOL). How many 20-somethings, or even millenials, do you think can actually afford that?

BTW median millenial wages by state in 2015: http://www.businessinsider.com/millennial-median-wage-map-2015-12

All median millenial wages are less than half of $100K, even in higher paying states. Highest is $43K in Washington DC of all places.

To be in the top 1% of millenial income you need to get about $106K/yr+ and there are only about 750,000 of them nationwide. 40% of all millenials earn less than $10K/yr. Earning $60K/yr would put you in the top 10% of millenial income earners.

http://fusion.net/story/41833/wealth-gap-calculator-are-you-in-the-millennial-one-percent/

So basically nearly no one in their 20’s-mid 30’s can afford a $700K home. Only way it’d ‘work’ is with a NINJA loan and if you see those being given out then you’re in a bubble and that $700K home really is worth much less than that.

You’re also pretty much guaranteed to lose the home with a NINJA loan so there is no possible way what you’re recommending makes any sense. As others have noted the economy of the 90’s or 70’s or 50’s was very different from today’s. Buying a home is neither possible nor the sure thing it once was.

Okay. Can Dr. Housing Bubble please do an archive search and get back to us on how many times jt has POSTED THIS STORY ON THIS BLOG! We heard you already. Do you have any additional information or at least another “story” or is your life really that hum drum?

People keep denying its an issue, lots of ‘bootstraps’ talk in previous threads, so it only makes sense for this blog to keep focusing on the issue from different angles.

What’s the employee discount at Home Depot?

JT is right, Later On you will regret wasting away those years as a Nomad. I am 36 years old and have been retired for 5 years. Nobody helped me get to where I am, 100% self made. As soon as I graduated college I lived with a poor relative and worked 7 days a week saving money and living in the hood. My friends all lived in San Francisco and spent all of their money going out and on sweet apartments. They felt sorry for me and thought I had made a huge mistake by not ‘living it up’ in SF and traveling all over the world on little vacations like they did. I even second guessed it at times myself and would go on occasional weekend visits to SF and party like a rockstar then go back to the grind in the ghettos of Sacramento. Well, now all of them are in the same apartments, working the same shitty jobs, and don’t own any real estate. I own apartment complexes that pay me passive income and my life is amazing. I farm all day and make furniture and grow 27 varieties of bamboo. My wife doesn’t work and I spend all day with our 3 month old daughter. I would suggest busting your ass in your 20’s while all of your friends are binge drinking and blowing their money. It works wonders I promise.

I’m 18 and I’ve been retired 13 years. I lived off of poor relatives while building my newspaper route into a huge pot operation. I now farm all day while buzzed on the 27 varieties of pot I grow. You should get off your butts at 13, go live off of poor relatives, live in the “hood”, make friends with Easy-money, and C-note while you’re in the “hood”, work your butt off and you can be retired like me at 18. Get busy. “On the internet people post the most outrageous things because they assume everyone is a sucker.”

Tolucatom – that sounds like “underground hero and visionary” Ran Prieur, who basically slacked off all his adult life, writing about dumpster diving, camping in the woods, living off of admirers who sent him money and housed him, cooked him dinners etc., while he waited things out until his Mom died (RIP; she was undoubtedly a very nice lady) and now Ran lives off of what she left him as well as the stocks/bonds he was set up with all the time.

Now all he writes about is smoking dope, listening to rather awful “edgy” bands, and occasionally a bit about food.

Live like British royalty off of what generations before you left you!

Pretty sure anyone with an amazing (whatever that means) life isn’t telling people about how amazing it is. Just sayin’

The point that JT fails to grasp is that, unless asset prices return to economic reality, his retirement plan is unlikely to be repeated. The game is currently rigged in favor of the have’s and maintaining economic. Stratification. I’m sure that many are diligent savers and prudent spenders who have the wherewithal to invest wisely for the long term. The cost of entry into the RE investment world is simply too risky at this moment.

The other part of the equation is investors and your average homeowner buying the last few years hoping for normalization and not having to dump at a minutes notice. otherwise we would likely see 2008-09 all over again.

Mr Miyagi,

If I may ask how did you get the capital at such a young age to purchase apartments. What kind of work do you do? Did you go to college? Did you graduate with debt. I am just interested in how people are able to break into the housing market so young…much less buying apartment complexes

Dream – You sound like a sourpuss LEWZER who didn’t choose the right parents! Boooo!

I do appreciate your defied gratificaiton and sacrifice. I have done similar. But at the same time you only get your 20’s once so I now appreciate yours and my friends approach more too. I think I would tell someone in their 20’s to be balanced. Don’t spend freely and wastelfuly, but don’t completely miss out either. I think the end result is very important, but the journey is important too.

And then there’s those of us who went to college, busted our asses working 2 jobs/7 days a week throughout our 20s AND 30s, never take vacations, barely eat out, or drive fancy cars or have the luxuries traditionally considered “middle class” AND STILL can’t afford to buy anything at these prices in So Cal. The playing field fundamentally CHANGED after the year 2000 and the older generations and many who post here just don’t freaking get it.

Move! I grew up on the beaches of So. Cal.! Believe me, that was great, but I moved several decades ago … the cost of living in So. Cal. was still relatively more expensive than many other parts of the country! Is living paycheck to paycheck and never having enough money to save for retirement, let alone buying a home really worth it? Some find ways to manage, but I have lots of examples of people who by simply moving away, found financial breathing room and are now much more comfortable! As a result of moving away, I two homes, one a really nice mountain/lake home in the inland northwest, have a boat 2 miles away in the marina, enough financial stability to live quite well, and travel frequently! I would not have been able to do any of this staying stuck in Cali!

SoCalRulez – Such is life in a class-based society. If you didn’t choose the right parents, tough. And for your parents to have money, *their* parents have to have had money also; it’s like the stages of a moon rocket.

Otherwise, yes, you can be smart, hard-working, all sorts of things but Class will sit on you like a huge weight and keep you down.

JT,

This is not 1990’s so your experience does not apply. Have a nice retirement.

Aint it great going back to the prosperous 30’s in America?

Before too long, we’ll see 3 generations living in the same house. Just like the Waltons!

G’night Ma, G’night Pa, G’night Grampa, G’night Grandma, G’night Sue Ellen, G’night John Boy, G’night Elizabeth.

When I was a kid in the Starving Seventies, I didn’t realize the “schtick” of The Waltons was that they were poor. They had a house, a car, enough to eat, didn’t have to time their movements with those of the local gangs. I thought they had life really good.

These days it’s more like multiple generations living in the same homeless camp – it’s not that uncommon now.

You forgot to mention the 4th class of people who will buy in this market…those international “investors” who want to launder their money and park it in supposedly safe assets like U.S. real estate. This has only compounded the disconnect between house prices and local incomes.

The problem is that sooner or later everyone sits down to a banquet of consequences. I think we are now seeing this play out on a global scale. If the government was really concerned about housing affordability, they would expand the FinCEN geographic targeting orders (GTO’s) nationwide. Of course that would mean popping all of the bubbles and ending the party.

http://aaronlayman.com/2016/08/houstons-luxury-condo-market-could-get-pummeled-fincen-expansion/

I think my point as well as JT’s (if I can guess for him) is that working hard when you are young can afford a great life later and at a young age. Very cynical to assume anyone giving advice to someone a bit younger than them is manufacturing their story because it is the ‘internet.’ On that note, I’m going to weld with my 80 year old neighbor friend right now instead of go to work. All because I busted my ass in my 20’s, caught a few breaks, and invested wisely. Yep, my life is great indeed, sorry if that hurts you! On another note, this market is going to implode soon, great Sac area deals (priced astronomically) are going pending so quickly. I truly feel for renters and first time buyers. This is brutal and hopefully something changes soon.

‘Hard work’ and ‘busting your ass’ are no longer effective since wages haven’t been going up with inflation or productivity increases for too many decades.

People have to stop with the ‘bootstraps’ BS and actually start looking at the data. The earnings and high paying jobs just aren’t there for millenials to improve themselves enough. I posted a ton of information up thread in response to jt if you want to look.

Wages definitely haven’t kept up with the financial excesses that have transformed real estate into a speculative commodity market. I doubt that JT had to compete against the deep (borrowed) liquidity of hedge funds and foreign investors.

In addition, the today’s high rents are simply a reflection of the bubble prices that landlords had to pay for their properties.

Working hard will only enable you to die young and worn out. If you do physical labor and work hard, you’ll die, worn-out and sad, in your 50s, with a 50/50 chance you’ll die in a homeless camp.

The ways to get ahead now are to firstly, be born into a family with money. That’s the surest way. Next is to become a supreme con-artist. There are lot of con-artist-y things you can do that should be illegal but aren’t, they’re just things no decent person would touch. Do those things. Con old people out of money, sell used cars, run various shady but not actually illegal financial scams. Be good at being personable, and schmooze it up with potential patrons and victims alike. Last on the list comes doing the things that are actually illegal, like drug-running and human trafficking. If you’re slick, and a member of the ethnicity in power (on the Mainland US, that would be white, in Hawaii it’s Japanese or Chinese, other places it will be other groups) you can go quite a while w/o getting caught. Chances are you’ll still die in your 50s but you’ll have a hell of a lot more fun than the guy who wore himself out doing physical labor.

The post war surge in home ownership was an aberration. We are far more likely to slide back to less than 50% of the population owning their home than we are to ever get back to 68%.

Student debt is a convenient excuse but at an average of $30,000 it is only the equivalent of a new mid sized auto. The real problem is stagnating incomes especially for those with less than a college degree. That $30,000 in student debt is only the down payment on a $150,000 home and areas with $150,000 homes don’t offer many jobs that pay enough to finance that!

America is fracturing into three pieces.An affluent corporate/governmental sector, a low wage worker drone sector and a underclass that is sustained by entitlement spending. Only the top tier corporate/governmental sector has the income and job security to buy a median priced home.

I feel that for the most part (not exclusively) there are two types of people on this forum. People that have done very well in real estate and made lots of money, and people that have not yet are bitter and hoping for a zombie apocalypse so that there will be wealth equality finally. Those in the bitter camp will never have the ability to accept that opportunity exists at all times in the world, they minimize the success of others by saying that times are different now and it is harder to build wealth etc. All bull%$^ of course and a they will always be poor and bitter.

If you’re looking to shoehorn everyone into two categories, it’s more like the following.

On one hand there are the commenters who’ve either profited or not from real estate and stick to ideas regarding the present.

On the other we have commenters who’ve either profited or not from real estate and project their personal past onto predictions regarding everyone else’s future.

Utter nonsense. I was another software engineer that bought in my mid 20’s, worked nights and weekends remodeling, sold the house for 3.5x what I paid. I got lucky that I bought when I did, but luck had little to do with my timing when I sold – I did my homework. Yes, you can make money with RE, but a lot of research is needed along with a lot of hard work to pay for it and frankly a bit of luck.

mid 90s: time to buy

mid 2000s: time to sell

~2012: time to buy

Now: time to sell, IMO.

I post because I want to pass on info to younger people or just people who are wondering WTF is going on with RE prices. Calling people bitter or losers because they think theres something wrong with prices makes you look like a scumbag shill. Plenty of shills everywhere, they make up most of government and the corporate oligarchy.

I’ve been following RE for 20 years now and currently prices are insane in a lot of markets – maybe all when you compare incomes, I don’t have the time to look at things across the nation. This will not end well. Again, this is all based on my research. If somebody wants to pony up 3/4 of a million on a 40 year old house, go right ahead. I will not stand in your way to getting rich, lol!

That “opportunity” in the here-and-now is allowing others to take the balance sheet risk as owners/investors in real-estate at these SoCal prices, imo – and perhaps the ‘mad-gainz’ winners can see they’re stuck with something very illiquid, where the gainz fall hard back.

In previous asset-bubbles, just as everyone has come to count on the idea that the lofty asset valuations are permanent, there is a crash.

Markets are driven at the margin. They’re driven by people who have to buy or people who have to sell. So when you get to the point when there are people who must sell, and that will come, then prices fall across the board because not many people have to be forced to sell at a low price to push values down

I think there are a fair proportion of boomers in the professional classes – and some younger ones who have been bankrolled by bubbly conditions – who have have been shielded from the vicissitudes of the world for two generations or more They are about to find out how the world works.

What annoys many people is many older owners are literally lottery winners. )Being given $1-1.5 million pounds for nothing – from house price inflation – can most definitely be classed as a lottery win.) And are not even cashing it in !!

There is also the belief that they are somehow deserving of it – which is ********.

We need more of this to change the market.

http://www.latimes.com/business/la-fi-downtown-apartments-20160719-snap-story.html

Mmmm hmmm.

“As new apartments flood downtown L.A., landlords offer sweet deals”

http://www.latimes.com/business/la-fi-downtown-apartments-20160719-snap-story.html

“To sign a 12-month lease for a roughly $2,200 studio, Mendelson said he got a month’s free rent and six months of free parking.

Later, when he wanted to switch units, he was able to negotiate free parking for a year — after living rent free for the month of June.”

Guess what won’t get factored into the rent price indexes? This guy’s free month of rent and 18 months of free parking.

Typical and hilariously so, this article skirts around the real issue – demand – by artfully interjecting “balance of doubt” quotes from those with much at stake.

And it’s not just DTLA. It’s also happening on the west side.

Expect the shills to come out with smoke and mirrors as this unfolding development exposes the biggest risk in the rent parody equations some have mortgaged their bets with.

You forgot about this part of the article:

“In other Los Angeles neighborhoods, where development has been more subdued, rents are climbing faster and deals are few and far between.”

So the guy paying $2,200 a month for a studio got a free months rent and free parking space. If I was paying $2,200 for a studio in DT LA I would ask for more then that. You do understand that all the examples you are showing are ALL high end uber-expensive apartments. Or do you not realize that?

You do understand that all of these examples are relevant to demonstrating that rents are not soaring nor skyrocketing in Los Angeles. Or do you not realize that?

I got a good chuckle after reading that. Dude sure did get himself a sweet deal paying $2200 per month for a studio and free parking. I wonder what 2 bedroom apartments rent for. Anybody who has been to DTLA lately has seen the cranes and high rises under construction to meet demand. This is one of the few areas in the city where units are actually coming on line. There is simply no place to build in many other areas; thus, the supply and demand conundrum.

FYI – there are actually over 10,000 residential units being built in DTLA these days. Shocking!

http://therealdeal.com/la/2016/04/07/these-are-the-biggest-under-construction-projects-in-los-angeles-county/

You know, it’s also funny how some point to so-called highly desirable areas as a benchmark for purchasing, yet are easily dismissive of it on the rental side of the equation, all the while pointing to rental parody.

I used to fall for those deals too. Then I realized it’s still a studio at $2,200…in downtown. And I remember what the cost was to live downtown 2 years ago, 3 years ago…

It’s like those furniture stores that are always ‘going out of business’ and knocking down prices. A $300 table that has a price tag of $600 with 50% off! GREAT DEAL! Except it was always a $300 table…

I’ve kept looking and rents are still high and rising compared to when I looked 8 months ago, and to when I moved before that at the end of 2014. No sign of slowing down rents.

Look at Marina 41 in MDR, the old Archstone marina. Equity Residential has a team of people and a computer system dedicated solely to calculating market rent based on who knows how many factors. 4 Years ago a 1-bed hovered around $2k. Last year when looked at it, it was at $2,300. Currently they sit at $2,500. This is all for the cheapest units.

But I bet if they put up “2,800/month, one month free!” you’d probably think you were getting a deal, eh? After all, you got a free month!

Hotel California just doesn’t get it. He’s probably the same guy that signed up for Trump University and bought the non-stick pan from the infomercials.

I get it perfectly well. I get that if demand and incomes were supportive of “skyrocketing” rents, there would be no need for free rent offers, period. I also get that soaring rents is the default backstop many use to justify paying a premium for real estate. I’m careful with my capital. It’s the reason why I visit this blog. But enough about me.

What’s occurring is not some isolated run of the mill bait and switch scheme which results in no impact to the rent price level.

There is a significant amount of new units which have come on line in the past 12-18 months in the “hot” areas of L.A. Free rent offers (effective reductions) were extremely rare, if not completely absent for the past several years. This is a more recent turn of events which has helped to put the brakes on rent increases.

I’ve not claimed rents are falling but I am claiming increases have stalled. We shall get confirmation soon enough over the coming months if this is a trend which will hold, or not. As of now, it’s not looking so great for soaring rents.

Speaking of Equity Re, they are offering a free month of rent at their new Altitude development in Westchester. It’s yet another example demonstrating that actual incomes and demand are not supporting their price increase models.

“In other Los Angeles neighborhoods, where development has been more subdued, rents are climbing faster and deals are few and far between.”

Therefore, soaring and skyrocketing?

Immediately following that quote in the article…

“According to real estate website Zillow, the median rent for all multifamily units citywide rose 7.2% in June to $2,446, compared with a year earlier, while the median climbed 3% downtown to $2,437 a month, where many units are studios.”

Clearly the Zillow data is their source and I bet they aren’t capturing this guy’s effective 5% rent reduction.

I would consider a 7.2% rent increase as “skyrocketing.” The 3% increase may not seem bad, it is absolute murder when compounded over a long period of time. This is exactly why people buy when they are anywhere close to rental parity. You will effectively have the same monthly payment for your house until it is paid off…renters can not say that!

Except the 7.2% number is about as reliable as official Chinese government GDP figures and real rents move up and down in cycles over the years.

The promotion of a homeowner’s monthly payment as being fixed without also mentioning that all other costs of ownership increase with inflation over time is less than honest.

Why people buy based on rental parody is the belief that there is some sort of definitive “hack” or shortcut one can take to reduce the real cost of housing.

Hotel California I would like to know your situation. Are you a owner, investor, or renter? Judging by your posts you seem desperate to justify renting vs. owning, going so far as to try and create cracks in the market where there are none.

The bottom line, which you can not argue, is that renting in the populated cities of S. Cali is expensive. VERY expensive. And it keeps going up. I’m not going to argue whether the term “soaring” can be applied, but generally increasing YOY. Can one pay a mortgage equal to your rent? That depends on where you want to live and how much you have to put down. (I’m not saying now is a good time to buy) But most people will say they would rather own and grow equity then rent. But owning isn’t for everyone. Some people can not afford to buy and for others renting seems to suit their lifestyle better then owning. Though I don’t think anyone wants to be retired and still renting. To me few years ago it was a no-brainer to buy vs. rent. But today because of high RE prices I believe it’s a much harder decision.

Judging by your posts you seem desperate to divert the debate to the personal level, going so far as to draw parallels between false accusations regarding my intentions and the truth of the issues being debated.

I’m either onto something, or not.

Alien Land Laws:

https://en.wikipedia.org/wiki/Alien_land_laws

Fujii v. California (1952) — The Supreme Court ruled that California’s 1920 Alien Land Law, and others like it, violated the equal protection clause of the 14th Amendment. Although enforcement of the California law had essentially stopped after the Oyama decision in 1948, the ruling in that case had not addressed the constitutionality of the law but only the individual rights of Fred Oyama. The Fujii ruling dealt directly with the legislation itself, therefore nullifying alien land laws.

Masaoka v. California (1952) — Issued three months after the Fujii decision officially branded such laws unconstitutional, the Supreme Court upheld a lower court’s ruling against California’s Alien Land Law.[12]

You people aren’t very bright. There were once laws that prevented Asian non-citizens from buying land. They were all ruled unconstitional. These laws are gone, but anti-Asian racism lives on.

The Constitution needs to be amended to bring those laws, great laws, back. Simple as that.

“Paradigm shift” was a buzz world a decade or two ago in military publications. Then it was about abandoning WW2 and Cold War mentality and strategies and adopting new technology to future conflicts. We need to do the same for housing and the young.

Before WW2 and especially during it, young workers did not buy houses. They lived in boarding houses. Chicago’s Allerton Hotel,e.g.,was built as a nice boarding house for unmarried office workers in the 1920’s. As late as the 1960’s one could get a room in Pacific Heights in San Francisco in a ‘boarding house’. Around Washington during WW2 huge numbers of women workers were housed in them. Today they seem to exist only in skid rows or cheap motels. We need to revisit the concept as a way station between a full amenity apartment or home. Hell, many college graduates just spent a few years living in college dorms that did not have a private kitchen and bath. No reason why they can’t continue to live in such accommodations until their incomes and savings allow them to find more private housing.

The days are gone when someone can move from the Midwest flyover country and sell a house and then buy a same size house in S. CA for the same price. The last time I saw this was in the early 70’s. However, I know a few people brave enough to buy a house in S.CA in 2009/2010 when dire predictions were flying of a further apocalyptic economic crash. That was only 6 years ago. They are doing OK with the interest rates falling further. I see the housing prices at peaks now and I don’t see the interest rates falling much further. How can they unless they are negative? I wouldn’t buy now. There may be a local 20% dip in the next few years so I’d wait to buy then. I would buy though. Rents are unbounded and I’d hate to be retired and have a 200+% rent increase.

Bob, I agree with all of that, but here’s the problem – that same 200% rent increase also informs the 200% price increase of insurance, major home repairs, and other ownership expenses.

What I’ve noticed is that retirees mostly fit into the camp of either having money or not, regardless of their home ownership status. I know of retired homeowners whose property is in a massive state of deferred maintenance because they have no money. I also know of retired renters who live a nice lifestyle thanks to sources of capital other than real estate.

I don’t claim that purchasing a home never makes sense, but I do rail against the notion that it’s as black and white as is often suggested.

Interesting observation. However, it’s not a crisis. It’s supply and demand. Don’t like it? Move to Idaho. It’s beautiful there. Los Angeles sucks. Traffic sucks.

Idaho is awful. We all have very short may-fly like lives and I would rather be a may-fly in coastal CA than hick country with bad weather and diabetic mouth breathers who vote for people like Cruz.

30 miles east of Spokane is such a nice area to live in Idaho. A lot of former LAPD retirees.

The German housing boom is starting to look ‘like a bubble’:

http://www.marketwatch.com/story/the-german-housing-boom-is-starting-to-look-like-a-bubble-2016-08-05

Check out the charts though. Rent has barely risen since 2000?

Remember how Bernanke reassured us in the run-up to the prior bubble that “we’ve never had a decline in house prices on a nationwide basis” and then it ended up actually being the one thing which really was “different this time”?

Wouldn’t it be interesting if what’s different this time ends up being the bursting of a global housing price bubble?

We have to come to terms with the fact, that when you stand in line at the grocery store, and take a look at the random set of people in line, most of them are renters. To be a home owner you have to be, to one degree or another, put together. The reason the middle class is dying is economic, but it’s also social.

The country has socially imploded and is full of Honey boo boo like characters who, even if they were able to buy a home would never have the wherewithal to paint the house, mow the lawn, or even take out the garbage.

The ones who do are home owners, more likely, Asian immigrants in CA.

JR, the honey boo boo crowd can afford to buy in most parts of the country where a typical house is 150K. Buying in coastal CA obviously requires a totally different buyer. You need to be making good money and have good saving and investment habits…even then there are no guarantees. This is what separates the contenders from the pretenders.

I am not really sure what your saying? Basically, when I go to the grocery store and look around at the white hipsters playing pokeman they are renters and because they are the spineless wishy washy millennials that they are they can’t be homeowners because of their appearance and attitude? But the asian immigrants who look and act more focused and driven, in your words “put together” are or could be more likely to be homeowners. Your basing your generalizations a lot on appearances. One interesting thing about Los Angeles, the definition of what it means OR looks like “making it” is not always clear….the guy with ironic t-shirt and backwards baseball hat who drives a 2005 Prius for all you know could be the founder of a incredibly profitable tech company or showrunner for a 1/2 hour comedy, yet the girl driving a Benz SUV, with a $1500 outfit on might be struggling to pay her overpriced $3k month apt., living on top ramen, and just holding on in the hopes she can meet the guy driving the Prius, get married, quit her $20 an hour marketing job. How about all the people in LA (many of whom are Asian immigrants), who drive around in BMWs, talk on their phones loudly about their lives, wear fancy clothes, go out 4 nights a week…but in reality they are one round of drinks at the bar away from bankruptcy. Fake it till you make it….Don’t judge a book by its cover. I probably look the person you are so quick to judge at the grocery store line, white guy who hasn’t shaved in a month and I don’t even own a hair comb, with a beat up 2012 Prius (paid off btw), a masters degree (which i am slowly but surely paying off), and ZZ Top T shirt (they still rock)…yet I am in a union and have a 6 figure salary in the film industry (stable even in a recession), my wife is in the upper $80ks at a college (also recession proof), we rent on the westside (yes my street is nicer than yours) and have a giant down payment in the bank waiting for the next good time to buy…who knows…when maybe I will buy next door to you. I am not an Asian immigrant, but I promise to mow the lawn (when I feel like it).

You are to be commended for working Union!

Most of those hipsters are working for $10 an hour in a book shop or a coffee house because they’re fun places to hang out, do a little work, and their friends hang out there. They’re buying houses and fancy cars because of their parents’ money. Their parents bought houses in the 1970s or so and are riding herd over 6-12 rentals, paying 1970s level property tax, and lavishing gobs of money on their kids.

A few, a very few, are making more than say $15 an hour in “computers” but almost all of those will be stocking shelves at Safeway by the time they’re 45 years old.

There are a very few, very tiny, portion of people making 1% wages in “computers” – most 1%’ers own multiple rentals, put in a lifetime with the Boilermaker’s Union, or something like that if they made their own money at all.