Parallel Universe: Housing Still Hurting on Main Street while Wall Street Celebrates.

What is occurring right now is reminiscent of what occurred after the subprime worries of February of 2007 dissipated for a few months. During this time, a few high profile companies such as New Century Financial started showing problems in their subprime portfolios and caused the DOW to drop 415 points. In this timeframe we also had Countrywide come out and state that 40 to 50 subprime units were failing on a daily basis (who would of thought that less than one year later they would be saved by Bank of America, a luxury the smaller outfits didn’t have). It seemed like we were heading much lower. Yet the market bottomed and started up once again nearly unabated until August of 2007. Let us look at the DOW since 2007:

As you can see, from February until August the market rallied. In this period we had many subprime outfits failing and the press on housing was finally starting to get a bit more realistic. Yet the market still rallied. Ben Bernanke issued a statement saying that subprime problems were “contained” and confidence once again was boosted. That is until the credit markets seized up in August. You have to love some of the quotes being said at this time and during the bubble euphoria. The reason I bring this up is that technically it looks like we are having a bear market rally like the one we saw after the February news abated. The only difference this time is that people on the street are having a hard time reconciling good news on Wall Street with their own bottom line. If they are to watch CNBC they must feel like they live in an alternate reality. Is energy not at all time highs? Housing prices are still going down. Food prices are still increasing. What reality are they living in? Before the credit crunch of August, the minor downturn in February of 2007 seemed like a temporary dip for Joe and Susie Public.

Let us now look at some history of previous U.S. recessions:

| Recession | Duration | Worst Quarter |

| Jan – July 1980 | 6 months |

-7.8 |

| July 81 – Nov 82 | 16 months |

-6.4 |

| July 90 – March 91 | 8 months |

-3 |

| March 2001 – Nov 2001 | 8 months |

-1.4 |

The reality is that we are in a recession that most likely started in December or January. Of course we won’t know officially until we have quarterly GDP data but I think if you ask any person on the street, they can easily tell you that the economy is contracting in some form. Just look at state budgets. If you look at the above, it seems that the pattern for quarterly downturns has diminished as time goes by. We also see this effect with CPI information. My take on this is that so much of the government data unfortunately does not reflect the expectations of what the average American is living. For example, how is it possible not to include actual energy and food costs in the CPI? Or what about using owners equivalent of rent instead of mortgage payments? You also get the unbelievable data spinning regarding not counting those not looking for work in unemployment data because they’ve given up. Pretty soon, we’ll have zero percent inflation and no unemployment yet people won’t be working and everything will cost more. And you wonder why there is so much confusion out there.

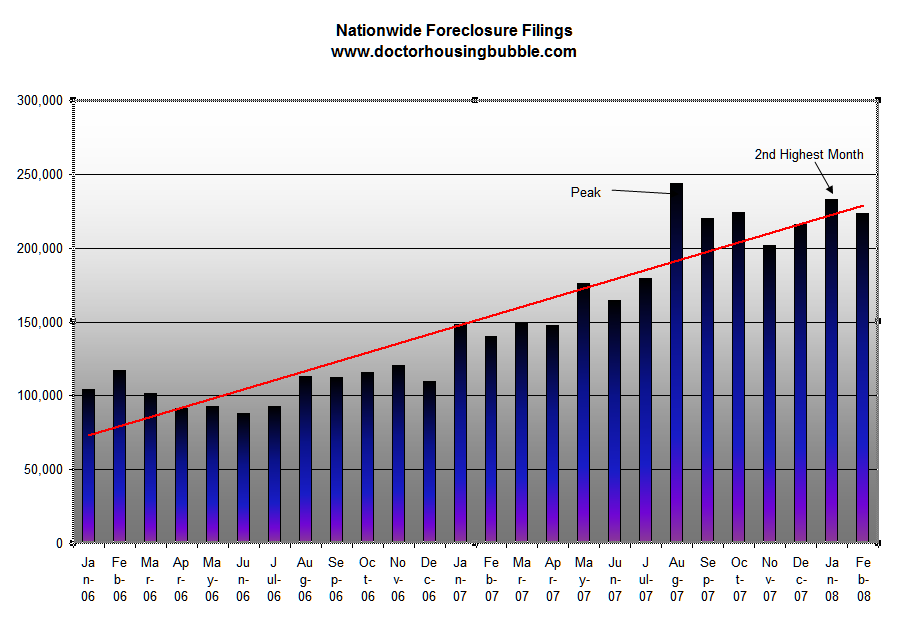

Let us look at one indicator that reflects market distress, monthly foreclosure filings:

*Click to enlarge.

The trend is clearly moving up and we are still hovering around record rates. And this in light of every imaginable concoction of bailouts including the Hope Now Alliance and others that are now waiting in the pipeline. Advance talks are now on their way about the government purchasing bad mortgages; interesting how the government isn’t looking to purchase good mortgages. We also know that the market’s current rally isn’t based on economic fundamentals but on recent historical rate cuts and the bailing out of a Wall Street Investment firm, Bear Stearns.

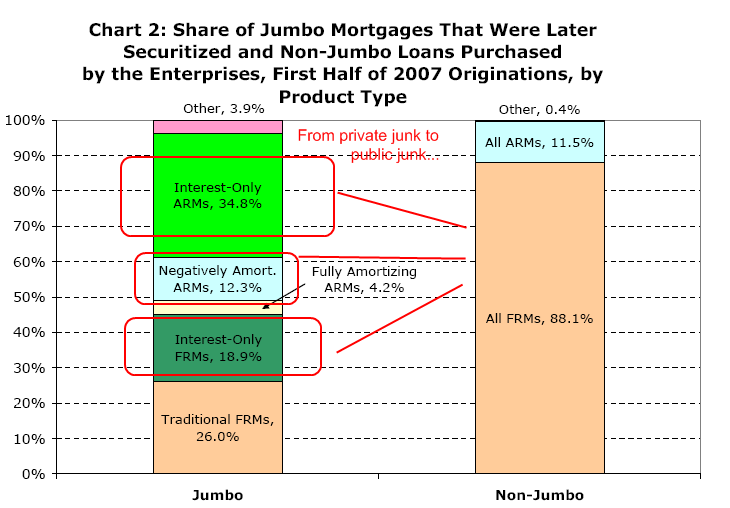

It seems like everyone is wiping the sweat from their forehead and saying, “that was a close one! If it weren’t for the government we’d be running around in leotards like cavemen.” How ironic that a firm like JP Morgan and Chase took on a $30 billion non-recourse loan from the Fed to bailout Bear Stearns. Let me ask you this, a company such as JP Morgan with a market capitalization of $161 billion, why in the world did they need that non-recourse loan? In fact, they have $123 billion in equity on their balance sheet. So tell me again why they “needed” the $30 billion from the Fed? Many that are bellowing out a sigh of relief fail to realize that the main culprit of this mess, the housing market, is still fundamentally in a major correction. All that has been done is a prolonging of the inevitable correction. Except now, the government is taking ownership of more and more of the toxic mortgages. The more time that goes by, the more shoveling of bad debt will the public be eating. Let us take a look at the jumbo market for the 1st half of 2007 before caps were raised:

As you can see, the purpose of raising caps was to shift risk from one side of the private balance sheet onto the public domain, most likely by Fannie Mae and Freddie Mac. Given, that most of these new conforming jumbo products that started this month are not interest only or Option ARMs, but how risky will these new loan products be? We keep hearing how well conforming loans have done in this housing crisis and how poorly large toxic jumbo products have done so now instead of stopping these horrible products cold, we have now institutionalized them? Forget about all this temporary rhetoric. When has anything been temporary with government? Also, the reason the conforming loan portfolios have done better is because they, uh conformed to standards! Now, we’ll just arbitrarily lift caps to $729,500 and come what may.

If you want proof of this parallel universe, today’s home sales number says it all:

“Home sales rise on biggest-ever price drop

NEW YORK (CNNMoney.com) — A record plunge in prices of existing homes produced only a modest increase in sales in February, according to the latest reading on the battered housing market by an industry trade group released Monday.

The National Association of Realtors reported that sales by homeowners rose 2.9% in February to a seasonally adjusted annual pace of 5.03 million, up from January’s reading of 4.89 million. It was the first month-over-month rise of the annualized pace since July.

The median price of a home sold during the month fell 8.2% to $195,900 from $213,500 a year earlier – the largest year-over-year price drop on record. Before the start of the current housing slump, it had been 11 years since prices declined, when compared with the same period a year earlier.”

Of course the market is taking this as good news but a drop in prices will again hurt the bottom line of builders and sellers. This is good news however for future home buyers. The issue was never about whether owning a home is a good investment. It was about prices becoming dislocated from local area economic fundamentals. The fact that sales rose because prices dropped tells you something. People need to drop prices and sales will come! Is it really that hard to understand? No need for bazooka loan products or Wizard of Oz bailouts since all that is needed is for home prices to reflect market fundamentals. Yes I know, too big to fail right? The fear of plunging into the Alice in Wonderland debt rabbit hole. Many are still in withdrawal and are hoping that the credit dope of interest only and Option ARM mortgages will once again rear their ugly heads. Not likely. Prices will continue to come down and as they do, sales will slowly start to pick up. Eventually both universes will cross and stay on one single path.

Update: The Case-Shiller 20-City Index shows a year over year drop in housing of a record 10.7 percent. Also, Consumer Confidence dropped from 76.4 in February to 64.5 in March. Again, this simply points to the major disconnect from Wall Street to Main Street.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

10 Responses to “Parallel Universe: Housing Still Hurting on Main Street while Wall Street Celebrates.”

OK then. So we all know that lowering prices will bring out some buyers. How long until sellers REALLY get religion?

Was looking around last night and virtually all the homes listed were priced as if it was still 2006…. 50 yr old 800 sq ft shacks in working class ‘hoods for 500k +/- with NO GRANITE COUNTER TOPS!! However, I did notice that several had faux wood paneling and that fuzzy, bordello style wall paper throughout.

Anyway, are sellers peeing into the wind, or just clueless (or both)?

Thanks for this article. I have been unable to refinance. I have good credit, have not been late on any payments, & have paid the fully amortized payment. Raising loan caps doesn’t do much of anything if values are dropping. I don’t plan on going into foreclosure however a refi or loan modification would be great – though I don’t see that happening at this time. Hopefully something gives soon???

Hey Nicole,

Check out my blog http://homesaver-bef.blogspot.com/. The company I work for can do all the negotiating for you to get a modification agreement with a payment that fits your current budget and property value.

Great article. I agree with Steve. I periodically look at home prices on the internet and notice that sellers are still on drugs and in denial. I remember looking for a house in Orange County about 2 years into the bubble, and to get back “down” to that level, the prices have to drop by at least another 30-40%. We have a LONG way to go. I think buyers will stay on the sidelines, like me, until that happens. Also, i think more people are changing their views and realizing the benefits of renting. Lower monthly rent vs. mortgage. No maintenance costs. Freedom to move somewhere else with ease. Now that the “a house is an investment” and the “prices always go up” mentality has been removed, home prices can find a equilibrium with incomes.

Nicole, I guess this exemplifies what others have been saying here…that these moves may be nothing more than postering if lenders aren’t going to lend or the borrowers can’t qualify.

If it’s not too personal, what is the reasong you’re given for being denied a refi?

Thanks and good luck.

“Was looking around last night and virtually all the homes listed were priced as if it was still 2006…. 50 yr old 800 sq ft shacks in working class ‘hoods for 500k +/- with NO GRANITE COUNTER TOPS!!”

Let them; they’ll just go down with the ship after the selling season is over and they’re still stuck with the house. They’ll be foreclosed on and the bank will eventually sell it. A disappointing 2008 spring selling season will be the wakeup call that the housing bubble is over. Banks in Las Vegas are finally starting to let houses go for pre-bubble prices and it’s crushing comps.

Finally, I see a little bit of good news. I live in Encino, a desireable area of the San Fernando Valley.

They built this “luxury” condo complex across the street from us. The original

asking price for the units were (depending on size) from $699K to $799. They

didn’t get a single offer. They put the units up for auction. Again, not a single

offer. Then they put them up for lease with the average rent of $3,000. They

didn’t rent out a single unit. The other day when I passed it there was a large banner hanging there saying “HUGE PRICE REDUCTIONS”. I checked their

website and yes, they have have slashed prices 50%. They are now going

for a little over $400K. Let’s see if anyone buys them now.

As far as houses in this neighborhood… they are just sitting there month after month after month with the same price tag. Don’t they get it… lower the price if you want to sell.

A Realtor accuiantance of mine said that most owners refuse to lower the prices.

Read in a book how they determined loans not that long ago.

Most mortgage companies would not lend more than 2 to 2 1/2 times your annual income. So if you make $50,000 a year you should not qualify for more than $100,000 to a $125,000 loan. Wow!

So a couple lets say have a combined income of $100,000 a year, they could not afford a house more than $250,000.

Thanks Eric! That’s what I’m looking for here in the L.A. area. Once the banks realize they either dump properties and take their lumps or they become landlords of empty homes, I think we’ll see the real correction. Seems many sellers are like bad investors, riding a stock the whole way down (Bear Stearns?)…waiting for it to come back. Just my opinion.

According to few sources, including this site, home sales are presently skewed to the high end of the market (i.e., a larger percentage of expensive homes are being sold since the rich are so far ok in this non-recession recession). That would imply that the median is skewed which means middle and lower end home prices are much lower. This interpretation is made using unfounded guesses, but what the heck.

In any case, the government is going to continue to bail out and buy out the banks and the funds. The only ones who won’t get bailed out are the home “owners”. Instead, look for new laws similar to the recent credit card laws. Soon, trust me, walking away will be impossible, or at least, illegal. Meanwhile, our taxes will continue to finance yachts and Ferraris for Wall Street.

We live in a “starter” neighborhood in the SF East Bay, and are just now seeing auctions. A house nearby that was priced at $500k in 2006 is now going to be auctioned ($139k will be the opening bid). Our house appraised at $400k for a re-fi several months ago. If $139k becomes a comparable standard for our neighborhood’s property values, we might be stuck in our house for a long time, but we also might be able to get our property taxes lowered (we paid $280k in 2002 so $139k would be about half that).

Of course if enough people get lower assessments, the state will really be hit hard. Over the past several years, the State of California has added a lot of new programs, and has expanded greatly. Rather than cutting back in a rational manner they do all they can to preserve union jobs and perks. Does anyone out there know of an effective organization that is bringing attention to the mismanagement at the State level?

Leave a Reply