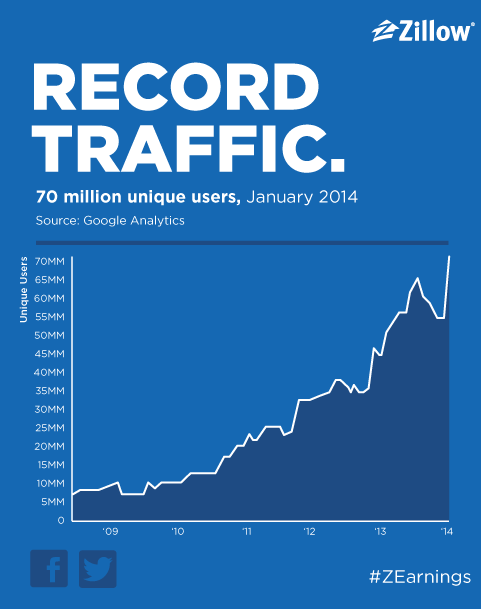

The liberation of real estate data: does having readily available real estate information encourage the boom and bust cycle? Zillow reaches 70 million unique users per month.

You can’t stop the internet when it comes to real estate data. Zillow is a great example of technology revolutionizing the way people view real estate. Some of you are old enough to remember when the closely guarded MLS was only accessible by your local real estate agent. Unless you were ready to do some digging, finding out what a home sold for took a bit of time. It was also hard to view a list of available homes for sale. That is no longer the case. When Zillow initially came out the housing bubble was still raging. My initial thought was that access to information would only serve to create bigger booms and deeper busts. Keep in mind that the entire housing system is still built upon the appraisal system. Basically each home is only as good as the last few sales. When a market is booming and people are now able to see the boom in real time the temptation to buy can ramp up. When the boom bursts as it did in 2008, you can also see how quickly things will reverse. Things are already slowing down and sales are dropping dramatically in some areas. Does access to data liberate us from the old model of buying and selling real estate?

The real estate information revolution

I love digging around in the housing data. Real estate by far is going to be the biggest purchase most Americans will ever make. In the past, this big buying decision was usually entrusted to those in the industry. It made sense if the only folks with access to the MLS were real estate agents. They held all the cards. Most people had no idea what homes were for sale until an agent drove them around to view target properties. Now, open houses are posted online and many people arrive agent free.

People are still irrational and that is why markets boom and bust. People had access to great information before the tech meltdown in the early 2000s. Zillow was around in 2006 yet the housing market had its first ever nationwide meltdown starting late in 2007 when data started becoming readily available to all. The housing market has become a speculative asset class that captures the attention of the masses. Entire mythologies are built around real estate. Confirmation bias is extreme in the industry even though we have witnessed 7,000,000 foreclosures since this crisis hit.

The appetite for real estate information is insatiable:

Zillow put out this chart showing the visitors to their site. Back in 2009 Zillow was getting about 5 million unique visitors per month. Today that number is up to 70 million. This is a massive number of people going to a site dedicated to real estate data.

It is important to understand what is going on behind the numbers. Appraisals are largely based on a “sales comparison approach†where recent sales are used as a basis for current pricing. This is great in a market with a high number of transactions and relatively stable price changes but what happens when sales dwindle or inventory flat out disappears? We are seeing some of this occur where some zip codes are reaching new peaks on low sales volume.

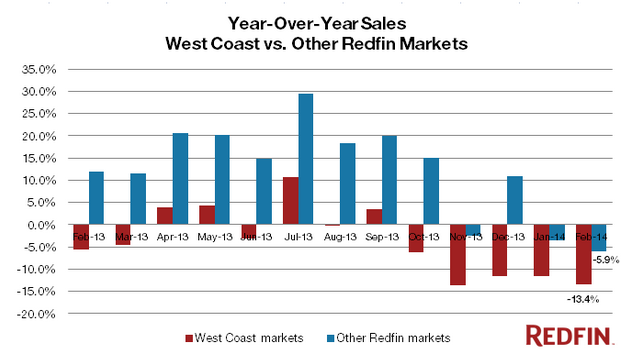

Redfin also provides some good data and we can see that sales are taking a hit in the West Coast:

Year-over-year sales in the West Coast are down 13.4 percent versus 5.9 percent nationwide. In California sales are leading the way in this year-over-year decline:

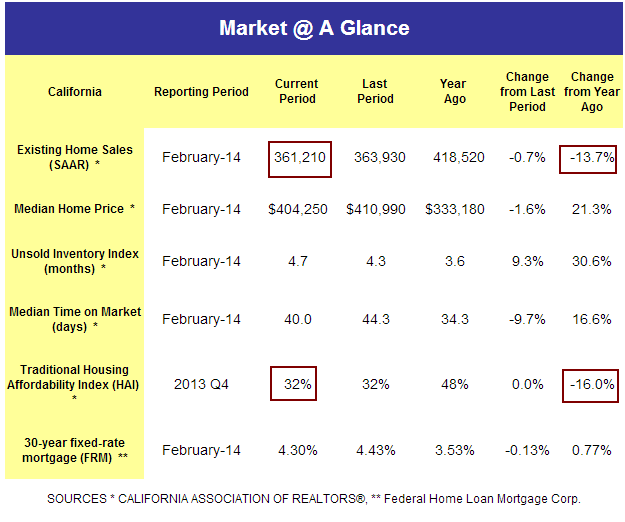

Sales in the state are down 13.7 percent year-over-year and the median home price is up 21.3 percent although this trend has stalled out for the last couple of months. Affordability in California is horrible. Only one out of three families can actually afford the median priced home. The last post was interesting and we see many young professional families with six figure incomes struggling to purchase homes in high priced areas. What is fascinating is that many of these high income households are pausing to buy because they are running the numbers. Numbers that many times are pulled from these new venues of data.

Why are these seemingly intelligent high earners balking at buying when the trend is obviously showing higher prices? I believe one of the larger ironies of having access to data is that it makes people more prone to manias and panics. The late night mantras of “real estate never goes down†or the simple minded retorts of “buying makes sense at any time†are largely lost on a tech savvy audience that can crunch the numbers and understands opportunity costs and can run the numbers on a simple Excel sheet. The days of fooling a large number of people with hollow mantras is largely gone. We can see what is going on simply by typing in a few numbers. However, it is naïve to think that greed, the fuel that sets manias ablaze is also gone.

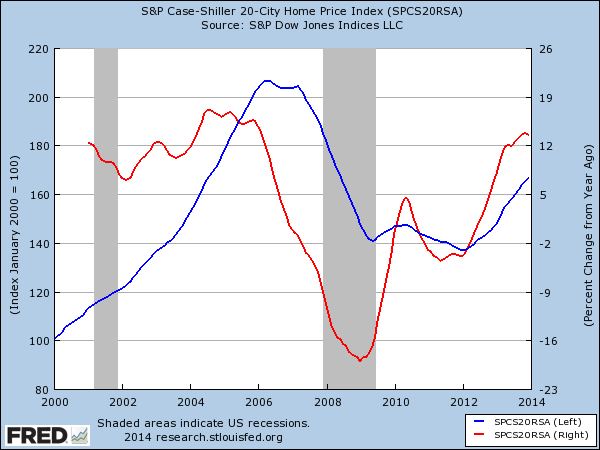

There is a bigger complexity to the system. Can the Fed really control interest rates for a very long time? Do baby boomers have adequate retirement funds to keep them going into deep old age? With sales slowing down and prices stalling out, will speculators pullback and spook the data hungry mob into changing their tune? The news cycle feeds off of the quick headline so you have to wonder what will happen when the housing market inevitably slows down as it is. Going back to the late 1990s, we have yet to see a stable market for more than a few years. Boom and bust has been the new theme:

Boom and bust seems to be a new trait of the housing market. Access to information only seems to feed the beast or starve the giant. The fact that so many in their 20s and 30s with healthy incomes that put them in the top 10 percent of households are hesitating to buy tells you something. These people want a home but are targeting markets flooded by investors, speculators, and people simply willing to mortgage their lives for a poorly built property. There are 7,000,000 reasons why people should run the numbers carefully and think deeply about making a giant purchase.

It is fascinating to see the number of people being vocal about buying in high priced areas today. This was similar to the rhetoric we saw in 2006 and 2007. Some have sound arguments and others are merely using their own confirmation bias as a way to extrapolate their very unique circumstances onto the future. People seem to crave a social affirmation when buying. Those that are successful usually feel pressure from family, friends, or even their own internal dialogue that buying is simply the next best thing to do. Once they buy, the entire narrative usually develops on how marvelous of a decision it was. Some even mistake luck with market timing acumen. The rental parity argument makes sense with smaller down payments but when we are talking $100,000, $200,000, or even $300,000 for a down payment, this argument falls flat. An all-cash investor doesn’t have to worry about rental parity from day one. Make the down payment large enough and you are likely to arrive at rental parity no matter what. There are bigger things at play. How many can actually save this much? What about the lost opportunity cost in say the stock market? Can someone actually carry this nut 30 years forward? It is interesting to note the volume of e-mails I have gotten in the last couple of years of people asking for confirmation about a buying decision. My response? Go ahead and buy if you feel you absolutely need to! I’m not the one that will carry a $4,000, $5,000, or even $6,000 monthly nut deep into the future.

What is also interesting is the big trend in people opting to rent versus buy. Many have no choice but many that have the ability to buy are opting not to. Some would rather lease a nicer home versus stretching to buy in an overheated market that is creating a halo effect on neighboring cities.

Access to data is great but I think this coupled with the instant media analysis only accentuates the boom and bust cycle of real estate. There is a strong possibility that this year, prices will go negative year-over-year in some areas especially if the slowdown in sales continues. Then the feedback loop will reverse. We have not had a normal real estate market for more than 20 years so why do some think that after this incredible investor induced boom that somehow, we will calmly reach a new permanently high plateau? The biggest argument for higher prices is basically the “because the past had lower prices†group and the “real estate always goes up in good areas†group that largely uses anecdotal stories as a method of ignoring the growing strain on local incomes. I can get behind this rally in home prices if good jobs were plentiful and incomes were moving up in sync with real estate values instead of being driven up by investor speculation and Fed market manipulation. It is good to see that those in their 20s and 30s with solid household incomes are actually crunching the numbers instead of mindlessly waddling into a massive housing purchase by following some old tired mantra. Remember kids, it used to be true that “real estate never faced a nationwide price decline†until it did only a few years ago.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

95 Responses to “The liberation of real estate data: does having readily available real estate information encourage the boom and bust cycle? Zillow reaches 70 million unique users per month.”

Well, I believe that even in the age of wide access to information, many people are unable to really understand what is going on – hence they seek people who will explain the data for them. And here we come again with the typical realtor “expert”, with all the phrases which have a unique objective to convince you to buy.

There are many appealing discussions on the internet about the problem of buying in an overheated market. I believe that it is a psychological problem rather than economical one. You state in this article that it is fascinating how young and well educated people still fall into a trap of buying at overpriced locations. They are not the only ones. There is a huge amount of people who are willing to risk – it was one quarter of all Canadians in the last report of Royal Bank of Canada.

And there is no technology that will stop them from doing it again and again. Our only hope is to educate people well enough so that they are able to manage their greed, which is constantly fuelled by the environment they live in.

Information is power. Smart people will always have an advantage with easier access to info. Yeah those damn smart people…. LOL

I get the reason for the snarky snarking, but I think the point he is making is somewhat valid. I am by no means saying that realtors are anything even remotely like experts and I loathe the real estate industry and sector for what they really are, parasitic drains on society; but access to data and information does not translate in to improvement or success. The problem in our society is that we treat our whole economy like a bare-knuckle fight that not everyone knows they are in, let along should be forced to be in. We have only very few and rather pathetic protections and limitations for those who do not wish to partake in bare-knuckle economic fist-fights competing against heavy-weights on Wall Street and K-Street.

Something as life altering and lifetime as a house should be in a class of as protected, secured, and stabilized markets as possible. You shouldn’t have to compete with hedge funds that have fee government money and policy and economies of scale on their side. It’s like putting a trained warrior with any and all weapons at his disposal against a toddler in a death match. It’s grotesque!

There is a spectre haunting California, and it’s the spectre of long term unemployment and all that implies. Specifically, it’s creating pressure to keep housing costs down. Political pressure to keep people housed is slowly increasing, and the first trend is the increase in affordable housing. Affordable housing is a relatively capitalistic take on public housing… but eventually, the pressure will be on to reconsider public housing.

Recently, a Forbes blogger pointed out that houses in Germany are dirt cheap compared to the US. How is that possible? Highly regulated rental and real estate markets, and a political goal of keeping housing costs low, and living spaces in good repair. Most people rent, and landlording is a business based around labor, rather than a way to speculate in real estate.

A different world is possible, where a stagnant income doesn’t threaten one with homelessness. California Uber Alles 🙂

The German case is interesting. I try to think about housing as a macroeconomic impact. In one sense, Americans have said, “We would rather spend our income on housing more than anything else.” No one, technically, forces them to do it. Even if the fed didn’t flood the market with money, I think we still would have seen massive increases in mortgage spending–just maybe at 75% of the fed-backed level. However, this crushes the rest of the economy. If more money flows out of town via bloated mortgage payments into the pockets of the financial/investor class, then that leaves less discretionary spending for groceries, cars, education, dining out, clothing, vacations, etc.

So, people are voluntarily putting the rest of the economy under downward pressure in order to cover monthly housing payments. Everyone wants to spend more money on their own house, but they hope that everyone else will still have enough money left over from their housing payments to spend on whatever goods/services you provide so that you can continue to make your housing payment. It becomes a game of economic musical chairs with everyone gambling they will have the last seat.

So, unemployment and housing costs go up in tandem. The amount of money we let people spend on housing is fundamental to all industrial policy. I firmly believe that housing costs are crowding out the productive economy and that this has done FAR MORE damage to the domestic economy than all other impacts (e.g., trade, immigration, technology, taxes, etc.) combined.

We can quickly fix this stupidity by making it illegal for each person to own more than 1 house. Ccapitalism needs constraints, else its default is slavery, which is lowesf cost

Thanks for this info, John. It’s very good to remember that things CAN be different if people care to pass the laws that will make it so. This goes for the outrageous price of education, the outrageous tax structure, the outrageous whatever. The current cry of “freedom!” here means the loss of sensible local and national governmental structures that have done very well for the U.S. in past decades. These structures were deliberately undone. Time to reverse that.

As Gov Perry says, you all come on over. Many parts of California are speculation areas. For boring living(not once you get children) and appreciation, come to Texas. Good place to have a family. If you have a stomach for speculation, by all means, take the plunge in nice areas of California and pay three times what you would pay in Austin. As the saying goes, if you have a complaint, either do something about it, or accept it. But stop your whining. Whining is for children. Grow up.

But aren’t your children taught in public school that Jesus had a pet dinosaur?

Thee’s a reason prices are cheap in Texas.

It’s hotter than Hades in Austin – -if you love air conditioning, by all means, head to TX. No thank you, coastal CA with rip-off rents is a better deal. But to each his/her own!

You are right Google or Apple employee. Prices in desirable(not Oxnard) areas of coastal California are not going down for obvious reasons, so you folks stop complaining and whining like little spoiled children, or papa will send you to Austin(aka Hell).

I lived in Texas for more than 20 years and wild horses couldn’t drag me back. Let me count the ways:

1.) Aggressively ignorant and intolerant people. Conservative Christionists are everywhere. They’re impossible to ignore. See Tex, Big…. example A.

2.) Terrible schools. Not so much the big universities, but your local schools are starved for money. Teachers among the lowest paid anywhere in the country.

3.) Climate & bugs. ‘Water bugs’ or ‘Palmetto bugs’ are euphemisms for giant flying cockroachs. Don’t forget months of blow dryer hot breezes too.

4.) No basements. Homes are built on a slab. Don’t forget to water your slab during droughts lest the foundation crack.

5.) You are miles, and miles, and miles from everywhere else.

6.) The highest homeowner insurance rates in the country. The reason: you are exposed to every kind of natural weather disaster, including earthquake.

7.) No zoning. While it’s one thing to have titty bars next to your house, (or mega churches), it’s quite another to have a fertilizer factory next to your school. See town of West.

I suppose I could think of others, but then I might be ‘whining’. I’m quite happy in the Midwest thank you very much.

“Midwest” = “flyover country”. Just where are you in the Midwest? How is the city that you are in better than Austin? I bet that it is cold in winter. How to you like the many snow storms that you are getting this winter?

Um, Tex, Texas is flyover country for all of the rich Mexicans going to Vail.

Well, the realtors are hoping they can get the eyes of millennials off of Zillow and onto their app so that they can turn homebuying into a facebook-style frenzy.

I just saw their latest ad on TV this weekend.

http://www.youtube.com/watch?v=09rccU4gidw

Jeeze, what a ridiculous ad. Way to capture the worst stereotypes of the “me” generation and women in general.

“OMG my super smart phone is buzzing in my Lululemon stretch pants during my hot yoga class, time for my self absorbed attention whore programming to kick in, who could it be?!? IT’S THE REAL-TURD APP NOTIFYING ME ABOUT A NEW OVERPRICED LISTING AKA AN OPPORTUNITY TO GET MY TIGHT ASS DEEPER INTO DEBT, BECAUSE THE STUDENT LOAN DEBT FROM MY USELESS ART HISTORY BA AND MASTERS WASN’T ENOUGHT!!! OUTTA THE WAY BITCH I GOT A 2 BED/2BATH SHITBOX TO SEE, POSTHASTE! OMG TIME FOR A SHITTY WINE PARTY WITH MY FAKE ASS, TRENDY INTERRACIAL COUPLE FRIENDS, LEMME SEE IF I CAN MAKE THEM JEALOUS AND CONVERT THEM INTO HOMEDEBTORS TOO…”

And can someone explain what she says or does while interrupting that dinner date?

Now that was a hilarious summation!

Sorry, I meant “Son of Me Generation”, above, i.e. Me Generation 2.0 – the Millenials/Gen Y etc.

I’ve been reading the doc”s blog for about two years now and this has got to be the most “humorist rants” I’ve enjoyed here! Nice job Craig!

Jim said beware the Ides of March, and two days later we have a 4.4 quake — the largest magnitude earthquake since the aftershocks of the Northridge quake. At least that’s what they’re saying on the radio.

Could this be a sign that (to paraphrase Silent Generation member Jim Morrison), “The whole sh*thouse is about to go up in flames.”

We don’t have earthquakes in Texas. Some people rather take their chances with a “tornado” than an earthquake.

I don’t agree with what you’re implying, Doc, that Zillow (and Trulia – I’m more a fan of the latter) promotes frantic buying and selling. A well informed public will make better decisions. These services give me that information for free, and I can closely watch the market in a way I couldn’t a decade ago. Another bit of data (this may not concern you residents of California) that Zillow and Trulia provides is property tax history, so one can be reminded that a large expense in a state like NY can literally double in a year or two.

I believe one of the big reasons that the Dot Com bubble got so big was that everyone thought that they were a day trader with their e*trade, Scottrade, etc. accounts. These online accounts provided “market insight†which was dated the minute the analyst hit enter. Everyone was a genius and they were quitting their day jobs to make the easy money of online traders. The more “players†in the game, the bigger the positive feedback loop, the bigger the market swings. This is especially the case when we have participants who have never seen a downturn. This removes the fear portion of the greed fear market dynamic. The same could be argued for the housing market.

I look at Zillow, Trulia, etc, the same way I view Sigalert.com or Google Maps, they are tools but only useful if you understand what you are looking at.

Example: It’s Thursday, 3:45pm, I am traveling from Pico/Robertson to Garbage Grove (405 and 22 intersection). Sigalert, Google Maps says the freeways are all green (full speed ahead – no slow downs, 30 minute trip based on current conditions). I know this is pure baloney because by the time I hit El Segundo the 405 is going to be be a parking lot due to all the LAX/South Bay area workers getting off at 4pm. The 30 minute trip becomes 80+ minutes. The original estimate was ass backwards wrong.

I see a lot of problems with Zillow and Trulia as well.

I check Zillow site at least once a week and they are great but not always accurate!

I have seen house next to me went to foreclosure and sold a few months ago but it was never on zillow for foreclosure also after it is sold to a investment company it never shows what it is sold until you click on the house and scroll down to the sales history..

On main page It shows last sold in 2006 but truth is; it is sold in 2013!

There are many houses in my neighborhood is in foreclosure or sold at auction for a lower price but Zillow doesn’t want you too see last sales price unless you dig deeper.

I wonder if they are hiding purchases made by investors or houses sold at Auction?

It is my understanding that the Zillow valuation model (as many other models) does not include distress sales.

Zillow is notorious for not killing listings that have changed status, either sold or taken off the market, or whatever. I find that Trulia is a bit more, ahem, truthful in that respect, but, I still wouldn’t trust them 100%. It is a good starting point to begin browsing, though.

Listen up, folks, here is how the next phase of Operation: Wealth Transfer/Land Grab is going to go down.

The BIG players in the industry, namely the Too Big To Fail Banks and the Investment/Private Equity/Hedge Fund firms and corporations they work hand in hand with, are continuing with their “off the record, off the books” informal and legal collusion for another big leg down in RE “values” in numerous markets.

This next leg down will be used to shake out as many homeowners and small guy/outsider RE investors and landlords as possible and work as another round of transfers of RE and related assets like mortgages etc. from weak hands to their strong hands. The powers that be know they have gotten just about as many buyres who were sitting on the fence posts to jump off and jump into the market as they are going to get this round, so now it’s time to reverse it and grab more assets.

How? Sell single on up to massive bundles of properties to each other and each other only at ever lower prices, in “looks legal and arms length” transactions that are truly anything but. This allows them to drop asset pricing across broad RE markets for the assets they don’t at present control, because these sham “sales” do act as market comps as they will play as arms length transactions. These are basically shady, insider short sales on a massive scale, meant to drive RE values down and trigger another huge wave of defaults and lower prices so they can come in and cherry pick more properties with all cash offers.

This not only allows them to continue to control the properties already in their possession, but (1) gives them paper losses for tax purposes, (2) lowers property tax rates via reassessment, and (3) again, tanks the market for everyone else and allows them to make another massive land/property grab at a discount.

No one will be able to buy the properties these firms will trade with each other except for the other firms…hell, many of these properties may end up trading hands with two “separate” legal entities but the truth will be that these “separate” legal entities will be subsidiaries, shell corporations, etc. of the same hedge fund, private equity firm, financial corporation etc. So they will never trade hands at all. Maybe if they offer some insane deal for it, as the insiders will just figure it will be theirs again eventually when this new owner inevitably defaults.

And no outsider will be able to even see these properties listed for sale or even if they do and make a competing offer, 99.99% chance they will never get the property.

Actually, I’m thinking this has already been occurring….the trading back and forth among the corps/powers that be, making transactions look normal, but in order to cause the prices to run away like they have in order to inflate prices.

Now that’s not to say they won’t reverse things and go in the direction you just stated.

After all, it is/was called “Operation Twist”

Problem with your opinion: who pays for all the friction cost?….excise tax, title insurance, escrow fees, etc, etc. These are substantial costs and add up really fast.

Title Insurance and escrow fees are negligible when you also own various title insurance and escrow companies, or do volume business to get a massively reduced rate to handle the transactions.

Another interesting post. I’m a fan of Redfin – so much so that we even used one of their agents when starting to look for a home. Unfortunately, we found that in the competitive market where we’ve been looking to buy, there is rampant and blatant discrimination against the Redfin agents by the traditional agents. We’ve had friends start with Redfin agents and have the same experience too. Traditional agents make up all kinds of lame excuses, but it’s pretty clear that Redfin is a consumer-friendly disruptor that they would like to see go away – putting downward pressure on commissions (since Redfin refunds half back to you – pretty significant when you’re talking about pricey homes!) and providing amazing access to the MLS as well as sales history. I also feel like Redfin offers the additional benefit of taking away some of the conflict-of-interest between the buyer and agent, in part due to the above and in part b/c the agents are salaried.

I don’t know that the access to information is fueling the cycle, though. Most people I know still don’t have a good understanding of the economics, and are fueled by emotion. Seems to me that it’s more about a combination of increased willingness to take on large debt burdens and government manipulation of pricing (e.g. through sustained low interest rates, tax incentives, etc.). Where I come from (suburban upper midwest), people just aren’t willing to leverage themselves to the hilt – and the “cycle” has been a lot more modest.

When I’ve spoken to realtors at open houses, they have visibly flinched when I mention I saw the property on Redfin. This has happened multiple times. From the realtor perspective, open data is not a win.

However, I agree that data can be misinterpreted or misunderstood. In some cases, I’m sure sales information can fuel the desire to buy. That’s why I would say the data we have is necessary but not sufficient to create an equitable market.

I think they’re quickly learning that the value that they’re adding is not worth the commission they’re demanding, especially from relatively sophisticated buyers. Heck, I often learn about listings before our agents send them to me. The only way to add value now is to control access – your offer won’t win, unless you have a traditional agent. Ultimately that’s dangerous to them, but still working in the multiple-offer bidding war situations. Should be interesting to see what happens when the market softens.

@CAperson

Agents for Buyers and Sellers hate Redfin. Why?

(1) Redfin cuts commissions and lowers agents’ takes which RE agents and the NAR hate.

But (2) Redfin also regularly sends no nothing sloppy stand-ins to take care of all parts of the transaction, creating headaches and down-the-line liabilities (which can be Major) for the sellers and their agents. Arbitration, lawsuits, legal fees and costs are expensive, time consuming and a royal pain in the ass.

(3) Redfin’s agents operate as if they have no responsibility for anything. They are all on salary (which is a fraction of what they would make in a non-discount, regular RE brokerage if they were any good) and are all fungible. There is no continuity from start to finish in the transaction. They have no “skin” in the game.

(4) Buyers in the long run (once they’ve moved in and get to know their new home) can get awfully pissed that they were incompetently advised and/or represented (if they were advised or represented at all). No real “skin” in the game. Arbitration, lawsuits, legal fees and costs are expensive, time consuming and a royal pain in the ass.

Redfin is cheap and it cuts commissions, which sounds good for buyers and sellers on the surface but you also get what you pay for. Until they clean up their act they will continue to be vilified by realtors and the NAR and to be treated as the lesser option, which won’t help you get that house. It sucks but that’s what’s really happening. You have experienced it yourself.

p.s. Currently, Redfin gets MLS listings in real time (bad if you’re an agent trying to prove you have the “latest real time” info first, through the area MLS — but the MLS is currently actively lobbying to delay IDX listing info to internet sites like Redfin).

Thanks for that information. Hmm. Curious, how did you learn about these issues?

Two of my friends recently bought properties where the listing agents caused serious problems that almost resulted in litigation, both sides were traditional agents. And when my bro bought six years ago he had an experience with a traditional agent (not in CA) that was pretty shady. I’m not really sure what to think.

I do know, though, that if the agents who bad mouthed Redfin to me had cited any of these kinds of facts, I might have had a different impression. Instead it was several bitchy little comments (e.g. “If you want to work with a professional agent, then call me. I don’t waste my time.”) that led me to think it was just a threat to their business.

I don’t quite understand your comment. We are all pretty savvy about how real estate agents earn their money on this blog. A listing agent is going to make the same amount of money whether a buyer’s agent is a Redfin agent or another buyer’s agent. Unless they are going to double end the transaction, they earn the same.

From the complaints I’ve heard about Redfin, part of the issue becomes a less aggressive agent when they earn half as much. No surprises there.

There are other programs that do something similar for buyers and the same complaints abound from those buyers even though no one necessarily knows up front that the agent is giving money back to the buyer in those situations.

Why would you think that someone is going to work just as hard for half the money? That is just unrealistic in my view.

Not really. It’s pretty simple economics. Here’s the math, for the sake of making it simple, for a 1M home, with standard 6% commission.

Listing agent is traditional, gets 30K

Buyer’s agent is traditional, gets 30K

Buyer’s agent is Redfin, they take only 15K and refund 15K to the buyer – effectively saving the buyer 15K on the purchase. Maybe the buyer could even increase her offer by 15K to beat out similarly situated competitors with traditional agents.

I’m fairly certain the selling side works similarly, but I haven’t had direct experience with that. Everyone in the industry knows how Redfin works.

Either way, many agents work both sides, and there is a lot of back-scratching. They know that letting Redfin get a toe-hold in the market will put downward pressure on them all to cut their commission in order to remain competitive.

Sure, our Redfin agent was not awesome, and I think many of them do move on once they have some experience – but I assume that’s to capture more of the profit. The Redfin agents aren’t “working half as hard” – they basically rely on you to do the legwork, and then they come in to negotiate the deal.

We made offers on two places last fall. On one of them, we submitted an offer with 25% down and above list in a multiple situation, and didn’t even get a counter. Listing agent flat-out lied to our agent, and the place sold for 1% more than we offered. That’s not the way a listing agent would behave if he cared about repeat business, and frankly, question whether he even violated his duty to his client.

RE agents work as hard for less money? You assume that they work… I had a RE agent roommate many years ago and I can attest that they rarely get out of bed never mind work…

Hi CAperson –

Your response is part of my point. If you readily admit that your Redfin agent was “not awesome,” why in a competitive environment would a listing agent want to work with them? If you have your choice of buyer’s agents (let’s say you are not double ending the deal) why would you want to work with one who is “not awesome” and is relying on the buyer to pick up the slack?

Now if the listing agent is double ending the deal it’s my understanding that they don’t want a Redfin agent or any other agent PERIOD. That possibility is just a part of real estate in CA. If they’re not double ending, then I would think they would want to work with an awesome agent who wouldn’t increase their workload. That is why people try to work with awesome agents… so their offers will be accepted!

Those are the complaints I hear from realtors… that other agents did not hustle enough… so it doesn’t have to be some conspiracy about not letting Redfin get a toe hold… it can be as simple as wanting or expecting the other agent to be as awesome as the offered commission implies. If I know that agent is getting $30,000 for the sale — I know I would expect to see some hustle from them! That is how it has been explained to me.

Also, if you are raising your price and raising your loan amount because of a rebate, that may or may not be a smart thing to do. You are right that there may be shenanigans… but put yourself in the mind of that listing agent… they may be calling other buyers to get them to raise their offers to beat yours, but that could just as simply be because they don’t want to do your agent’s work.

Real estate is like any other field… when people are paid less they do less. Always.

Maybe they should not earn what they earn, but if you are working in the field why would you agree to give up half of whatever you make and do the same amount of work?

That’s my take.

You’re not understanding the point. The 30K goes to the buyer’s side, regardless. Real estate is not rocket science. There are a lot of really terrible and lazy traditional agents as well. And again you’re ignoring that they basically share the work with their client, so they are doing “less work” but it’s the stuff that some of us don’t need them to do, anyway.

Theoretically it’s none of the listing agent’s business how the commission is split on the other side. We didn’t offer more *because* we would get a rebate; we offered more to position ourselves competitively. Seriously, I negotiate for a living and I work with clients. But my profession isn’t a cartel.

I had a traditional agent that sucked major donkey balls, so what?

Should they get $6K on a sale where I’ve done all the legwork? Naa.

@CAperson: “You’re not understanding the point. The 30K goes to the buyer’s side, regardless. Real estate is not rocket science. There are a lot of really terrible and lazy traditional agents as well.”

(a) Yes, there are some terrible and lazy agents out there. RF seems to have a lot of them… on low salary – Think “Wal-mart” of real estate. But also understand this: RF’s reduced commission + buyer/seller kickback as a model threatens realtors’ traditional 5-6% commission structure on the macro level. RE Agents represent buyers and sellers depending on whatever is happening in the “market” so anything that threatens to derail their 5-6% is a non-starter at best, a war-cry at worst.

@CAperson: “Theoretically it’s none of the listing agent’s business how the commission is split on the other side. We didn’t offer more *because* we would get a rebate; we offered more to position ourselves competitively. Seriously, I negotiate for a living and I work with clients. But my profession isn’t a cartel.”

See response (a), above. Also, you are not likely to position yourself more competitively by shaking the PTB-SOP tree. That requires a smack down of the industry as a whole, which will take more than RF and its flawed Wal-Mart approach. Homes aren’t the same as cheap disposable crap. They are so far overpriced right now it’s laughable and nauseating at the same time. Hopefully Jim Taylor is right that “housing [will] tank in 2014” and real people will be able to get nice homes in good areas at affordable (rental parity) prices again. Until then, don’t freak out. Wait it out. These prices can not sustain.

For sellers of crappy houses in marginal areas with loads of issues that won’t be fixed &/or may not be disclosed, a discount no-nothing, do-little, “kick-back” Wal-mart approach with no skin in the game may be the best or only option. But caveat emptor… (buyer beware)

Redfin has the best search functions, allowing you to search a neighborhood instead of just a zip code or city. You can draw lines around a search area. You can filter by recency of sale, exclude lots/lands/multi family etc and you can download all data into an Excel file. This was very helpful for us to value homes, allowing me to run regression models and build my own estimate based usually on lot size and sq ft. for any particular area we had a potential home offer.

We just submitted a fair offer for a property to a listing agent. We called her up and asked to view the property and she sent her associate. Then when we submitted the offer we struck out all language in the contract that had any reference to buyers agent and clearly stated in our offer letter that our offer price was equivalent to X/0.97 because we represented ourselves. We did all the work, including drafting our own offer, but she still sent back a snotty remark that “now we didn’t need an agent” after someone had shown us the property. I carefully pointed out that we always ask the listing agent to show us potential homes and that it’s not our problem she got someone else to do her work. That’s between them. She scoffed she already had offers over list, but I quickly retorted we also had a nice rental already lined up in case it didn’t work out. Dispassion is great.

Captain Credit Crunch —

Did you get the house?

The Redfin website can be quite useful for checking listings…but FWIW the forums cannot be trusted, they are heavily censored, often without any notice or explanation, and frequently not for good reasons (like profanity, personal attacks, etc.)..so you are not seeing an open exchange of ideas and opinions like here.

Hi CA Person –

I don’t think we are in disagreement since you’ve admitted you wouldn’t use a non-aggressive agent again…

I do have a friend who worked with an agent where they were getting a rebate and they did increase the workload of the other side. In fact, multiple times during the home search they seriously considered switching.

An example, once they got in contract, they never wanted to be present for any inspections. Well the owner wanted a licensed agent present (seems reasonable since home inspectors aren’t even licensed in CA), so that meant the listing agent had to be there each time. She was in essence doing the other side’s work.

So, yes if I was that other agent and I knew $30,000 was being paid to you (whether you decide to give it to the buyer or not) I would be upset if I had to deal directly with your client and perform your tasks. Her agent was even slow about drafting documents, and she ended up asking the other agent to do that as well.

What I understood from your point about raising your offer was that you felt that having a rebate gave you more room to do so. However, that is just spending more and of course someone else can do the same. The issue I’ve heard is that with using a non-aggressive agent is that the listing agent will not want to work with an agent who does not uphold their end of the bargain. Raising your offer does not fix that problem. They can just go and get someone else to raise their offer to in this environment — which sounds like what happened to you.

Why not just represent yourself and offer the buyer end of the commission back to the seller on the face of the offer. The listing agent may still end up doing most of the work…. but there is no arguing against the appeal of that to the seller… and not much room for the listing agent to dance around it unless they just don’t present your offer. That way you are not playing the increase your offer again and again game.

Even at the level of the Federal Reserve Bank one sees that real estate’s connection to our national liquidity engine is not fully comprehended.

This best explains the Cargo-Cult nature of the Keynesian Faith.

By its acts, it’s obvious that the PTB think that debt-monies created by Federal deficit spending can be equated to debt-monies created by the commercial banking system of the nation.

Such a credo dribbles from the lips of one ‘expert’ after another.

It’s embedded in MMT.

As for popular economics: note the constant refrain that the Renminbi has some prospect of replacing the US Dollar as International Money/ the Reserve Currency of the planet.

There is no possibility of this ever happening — until China has a wholesome revolution.

The ONE absolute requirement for all reserve currencies is that the nation sponsoring said currency has to run perpetual deficits on a global basis — in perpetuity.

99% of the punditry has not figured that out. This is true across the political spectrum.

Until a nation is willing to absorb the nasty unemployment statistics that necessarily follow from running perpetual deficits, its currency can’t be accumulated in alien hands. Until they do so, the currency only serves its domestic turf. Currency transactions only occur in the context of specific trading. (goods, services or capital) Having no deficit, the accounts net off, globally. Alien currency traders are only able to establish longs only if yet other traders are holding net short positions.

QED.

Generations ago (1974) the prospect that the Yen might be utilized as a reserve currency — even if only within its trading bloc — had Tokyo freaking out.

They were bright enough to comprehend that such a status REQUIRED Japan to shift employment away from Nippon — and towards Malaysia, Indonesia, Korea, et. al.

Active measures were taken to nip the trend in the bud. This national financial policy made the international news: Business Week, The Economist, Forbes, Fortune, WSJ, et. al. all ran blurbs on the matter. Even then, the financial media didn’t get the connection to Japanese unemployment statistics. Tokyo DID.

The policy was a total success — even to this day. No-one even runs the Yen up the flag-pole as a replacement for the US Dollar.

As you might guess, the Yen actually is the logical replacement for the dollar.

That such is so — and not perceived by the chattering class — is an indication as to just how dull the ink-stained-wretches are.

%%%

At some point, after making every mistake in the book, the truth will be outed, by accident.

I strongly suspect that this ‘nexus of education’ will occur only after the PTB do a bang-up job of crashing the system.

It’s at such a point that DC will have its ‘King Lear’ moment — that burning comprehension that only comes in extremis.

But, for now, DC can just paper over folly.

“The ONE absolute requirement for all reserve currencies is that the nation sponsoring said currency has to run perpetual deficits on a global basis — in perpetuity.”

I am glad you said this before me because I was about to state this in a prior post where someone was claiming that China of all countries was going to become the world reserve currency and I thought to myself that will never happen because of what you stated. I was actually worried that I would have to defend the statement and decided against it. Sometimes basic math is the hardest to support on this blog…

Blert, thanks for posting. I wish I could understand all of this, as I usually grasp about 1/4th of your comments but still make sure to read them through. Cheers!

Wars and gold holdings have a big impact as to who becomes a reserve currency i.e. WW2 Bretton Woods..

@Blert: What you write is incontrovertibly so, and if I recall correctly, was quite literally in my college Econ 101. To be fair it was phrased differently, that the consumers of the issuer of a world reserve currency would inevitably have to absorb the world’s excess production, generating sustained trade deficits as well as fiscal deficits. Of course, you clearly understand how that plays out, so no need to rehash it here.

However, this tells me that the situation is well understood by the PTB – they just don’t mind throwing us under the bus. I would submit that the real difference between (modern) Tokyo and DC is that in Tokyo, they operate on at least some belief that as a government, they have some duty to be of service to most of their citizens rather than just a few. In DC, once you get past all the talk, less so. Otherwise, would we even consider the Pacific trade agreement now under discussion? This is simply a continuation of the policies which have gutted the middle class in order to maintain reserve currency status and to further enrich the owning classes.

So riddle me this, if you please: understanding the cost on citizens, why on earth should I want to maintain the USD as the world’s reserve currency? Does it buy us as a nation anything more than 1) some modicum of international power 2) an elixir for Washington egos 3) ease of international financial predation for the few? Does the world even need a reserve currency any longer, since BW is now dead as a doornail? I’m not seeing it. China? if you think you can pull it off, be my guest.

Uhhhh…deficits actually are the source of employment usually as they inject money into the economy that producers and households are requesting. As our country grows and the users of our currency grow, the money supply must increase or we’d have a stagnant economy. Evidence of this is in how the price of everything went up with the Baby Boom generation. We added a whole lot of people who needed money to buy things. Their needs outstripped domestic production resulting in trade deficits. As Baby Boom unwinds, we should see lower trade deficits and lower budget deficits. As for unemployment, the rate is higher now when you include the broader measures, but the total # of working people is a lot higher now than it was 30 years ago.

The reason unemployment is so high right now is because instead of focusing on re-training workers to match employer needs, we’re afraid of deficit spending so this idea gets thrown out. If we could train our citizens to be IT people, skilled tradespeople and other in demand fields, workers could get pricing power in the job market. The old economy’s skills are not needed in the new economy and we need to get people’s skills up-to-date. If we could do this, our GDP would go up a large amount in a short time and our deficits over GDP would start to look small.

“Uhhhh…deficits actually are the source of employment..” You got the wrong kind of deficit. Trade deficits in no way create jobs in the country that has a trade deficit. Yes it creates jobs in the country with trade surplus.

So, US trade deficits are a source of employment for the surplus trading partner. There I fixed it for you… I am not going to waste my time with the rest of your dissertation because your first sentence is incorrect. Like I said basic math seems to be the hardest point to support on this site…

Where is truly matters about world reserve currency is in commodity sales, ie oil and gas. That is why we are able to export our inflation overseas. But, does the world really need a reserve currency? Transactions for oil/gas have already been done without the dollar between using swap lines. Who are the major producers of commodities? CHina and Russia plus Saudia Arabia. China and Russia will trade with each other in either rubles or RNB. Iran was able to do this last year when sanctions were put on them, they traded oil for Gold with Turkey and Dubai as a go between. Reserve currency may or may not stay but Reserve Money will always be gold. I’m sure any of the commodity producing countries will be willing to take Gold.

Seems the only thing the internet really only gives anybody is confirmation bias. Maybe that’s why Amazon sells out of rose colored glasses.

Violations of Anti-trust? price-fixing? RICO? Or??? Take it to the Atty General or Justice Dept. or Wikileaks or investigative media with facts backed by solid evidence. Do something, anyway, if it’s true. Channel your inner Erin Brockovich. Help make Jim Taylor’s prediction come true!!!

@insider, I agree that the scenario you describe is a likely next step. However, I think that a prerequisite for this is to have taken an ample number of borrowes who would be inclined to strategically default (ninjas / HELOCabusers) “out of the trade”, replacing them with borrowers who won’t – those who have good credit, 20% down payments, demonstrable steady income – so that banks don’t suffer losses in the process. This was the primary purpose for re-inflating the bubble and the attendant hype. I’m not sure that this has yet sufficiently occurred, so the next leg down still feels 2-3 years away, probably after the next wave of helocs / mods fail.

Can I borrow your crystal ball? For some reason mine appears to not work with the current “market”…

@what: That’s because they’ve taken the market away. There is no market anymore. In its place, there are manipulations designed by the Fed to save bank bond and equity holders, to alleviate further balance-sheet driven catastrophes, as well as to enrich their buddies in the financial predation sector (as usual) to the detriment of ordinary folks. How can you call it a market without unimpeded price discovery? How can you call it a market when it is only fueled by easy / cheap money (for the few) and “conscious parallel action” (as they say in anti-trust ) to artificially constrain supply?

Hence the quotes around “market”…

What, I’ve noticed you ask for everyone’s crystal ball except Jim Taylor. Why does he get a pass, especially since we’re now crossed his invisible threshold and we’re still here?

What makes you think Jim Taylor’s prognostication is wrong? The housing market has stalled out, there is substantial weakness, price drops, and lack of completed sales/transactions. He merely said to “beware the Ides of March” and that “Housing will tank hard in 2014”. Even if he had said “housing will tank hard starting March 15”, it’s only been 4 days. Hardly enough time to see and confirm the market has tanked. Hindsight will let us know, give it a few months/year.

NJ it’s not about replacing the borrowers, it’s about replacing the LENDERS. Move the shit “assets” to Fannie Freddie and the FED then liquidate. Once again being the reserve currency comes in handy… As I said earlier they are going to tank residential RE to support commercial paper. The consumer HAS to have more disposable income you save the over built retail sector from going under. They aren’t getting raises so lower rents/mortgages are the only way. The only way you can make retail earnings come within a country mile of justifying stock values is to get discretional spending up by tanking residential RE costs for Joe 6P. Now I wouldn’t be suprised if there’s another “echo bubble” within a few years as bubbles are now America’s only industry and there is so much inventory, but the next crash is already happening. Sales volume is non existent and FED officials are talking about a “soft landing” for the economy. 2007 Deja Vu… The reality is we’ve been in a grand recession since 2000 and while the serial bubbles have enriched a few, the 80% have seen a steady decline in standard of living.

@NZ: “NJ it’s not about replacing the borrowers, it’s about replacing the LENDERS.” – It’s both; some loans were packaged into RMBS, some were “credit enhanced” by Fannie / Freddie, some were not.

“Once again being the reserve currency comes in handy…” – You’ll have to help me out with that, I still don’t see what this buys us.

– I agree that the retail sector is overbuilt, but I don’t see why the fed should crash RE just to save retail stock prices. In fact, the opposite seems more plausible in achieving that objective. Inflate RE, let folks support the lifestyle they can no longer afford due to falling real wages by HELOC extraction. Rinse, repeat.

“but the next crash is already happening.” I would really like to believe that were true – as I am among those on the sidelines, keeping my powder dry until there is more reasonable pricing in the market, (and I expect to wait for quite a while) but I am not seeing a crash right now. Yes, sales volumes are plummeting, but prices are holding more or less since last June. Without desperate selling or foreclosures getting processed free of bank obstruction, prices won’t crash. And the banking cartel has perfected the art of managing the flow of inventory and selling to insiders such that prices don’t crash. In order to crash, sellers would broadly have to be accepting dramatically lower prices. The fact is that most of them can’t, as a high proportion of sellers / would-be sellers are near / underwater – at least 50% of sellers fall into this category.On the distressed side, banks can do well by bleeding the borrower dry in a designed-to-fail loan modification. They collect interest and front-loaded fees now (against extended amortization periods), and then when nominal prices return to peak values by pure dint of inflation in 3 or 4 years, the bank will take the house at that time (without realizing any loss) when the borrower can again no longer make the payments as their interest rate ratchets back up to the rate on the note (after having paid many thousands in interest and fees).

I think the thing to appreciate is that since FASB rolled over and M2M went out the window, banks no longer have any incentive or requirement to foreclose or do a short sale. What they don’t want to do is a) take the property on their books as a REO because what they *really* don’t want to do is b) sell it at a loss. So they are now allowed to – and are quite content to – wait it out until the bubble is slowly deflated by inflation, and distressed borrowers have been taken for all they can.

I heard a statistic on the radio that Los Angeles is over-retailed even if you strip out all online shopping. You might be right about that one.

I think you’re also right that residential is going to tank. Demographics and consumer spending don’t support it.

Happy St. Patrick’s Day everyone, hope you don’t have to resort to eating canned corned beef, or worse, a St. Paddy’s Day dinner feast based on canned corned dog food mystery meat.

Is it Purina Cat Food Taco Tuesday yet?!?

Hey Dr. H.B., how about tackling Silicon Beach tomfoolery?!? Based on the numerous candid personal anecdotes and comments in the replies and responses on your previous article, many in your readership (myself included) are in tech both up north in San Jose/Silicon Valley/the Peninsula/SF Bay area in general, as well as down here.

Here’s a great starting point, a Venice shit shack asking $1.5 million. Check out that great “work studio” where no doubt the next great technological leap, the next Google or Apple will come from, working away at that “desk” with a tube TV and VCR.

http://la.curbed.com/archives/2014/03/silicon_beach_gets_stupid_how_much_would_you_pay_for_this_hideous_shack.php

@ Craiglister. As a lifelong resident of the westside (until I purchased a house in Baldwin Hills) I am not surprised by this shack in Venice ‘silicone beach’. You watch… it will probably sell soon at a price near asking.

Here are some articles that espouse the ‘silicone beach’ designation:

http://articles.latimes.com/2013/nov/30/business/la-fi-silicon-beach-real-estate-20131130

http://www.ft.com/cms/s/2/cb79bb38-8e8a-11e3-98c6-00144feab7de.html#axzz2wHMxzn4f

“…In the past 12 months property in Venice, Marina del Rey and Santa Monica – areas dotted with hundreds of new tech start-ups – has experienced double-digit price growth and a dwindling supply of inventory. Homes are also spending considerably less time on the market and selling well above asking prices, according to estate agents.The influx of internet wealth is swelling house prices in one of the most competitive and expensive property markets in the US. Observers say it is reminiscent of the real estate boom that swept Silicon Valley during the dotcom frenzy of the late 1990s. In turn, this is sparking fears of a property bubble not unlike the one that burst following the internet collapse of the early 2000s.

“Homes are selling very quickly and for more than listing prices,†says Gregory Bega, an estate agent with Sotheby’s International Realty. He recently listed for sale a three-bedroom home in Venice at $11.5m, which found a tech-industry buyer in less than a week. “The hyper sales pace means a much more competitive marketplace for buyers.â€

The area known as Silicon Beach covers approximately a four-mile stretch west of the 405 freeway, along the LA coast. It includes the areas of Santa Monica, Venice and Marina del Rey, stretching as far south as Playa Vista.

Initially populated by dozens of smaller tech start-ups seeking to escape high rents and competition in the San Francisco Bay area, it has rapidly expanded to include offices of behemoths such as Facebook, Google and Microsoft. Google recently opened a new 100,000 sq ft campus in Venice and is negotiating leases on another 100,000 sq ft, according to commercial real estate agents. Microsoft has a 20,000 sq ft office space in Playa Vista with more than 100 employees. They join emerging companies such as social media video app Viddy and Hulu, the video streaming site.

The tech growth coincides with a sharp rise in start-ups across Los Angeles, where more than 700 computer and technology firms now operate, estimates Sean Arian, vice-president for emerging technology at the Los Angeles Chamber of Commerce. Startup Genome, a research project that compiles data on start-ups around the world, ranks Los Angeles third, behind Silicon Valley and Tel Aviv, among the world’s top start-up locations.

The median price paid for homes in Venice, Playa Vista and Marina del Rey rose 14.7 per cent to $917,500 in the fourth quarter of 2013 compared with a year earlier, according to figures compiled by DataQuick, a real estate information services firm. Prices in these areas are up 24.6 per cent since 2011.

“The market is up but there’s still room to grow,†says Kenneth Rosen, chairman of the Fisher Center for Real Estate and Urban Economics at the University of California, Berkeley. Rosen says talk of a bubble is premature because home prices are only now approaching pre-recession levels. “The market is essentially regaining its footing after significant softening after the banking crisis,†he says. “Low interest rates and limited inventory are actually helping the market stabilise.â€

Tami Pardee, owner of Pardee Properties, says the boardwalk community of Venice, with its eclectic atmosphere and sandy beaches, is a popular area for younger tech employees to live. Bobby Murphy, the 25-year-old co-founder of photo messaging app Snapchat, recently bought a two-bedroom house in Venice just blocks from the start-up’s headquarters for $2.1m, nearly double the median price of neighbourhood homes….

Google Fiber arrived in Kansas City. It has helped establish Tech Villages. The good thing about housing in this new tech village is that most of the houses are less than $100k. LOL….Kansas City is going to kick Silocon Beach butt.

http://www.kcstartupvillage.org/villagers/startups/

————–

The house is the pet project of Web designer and Kansas City local Ben Barreth, who did the insane last fall and cashed in his savings and liquidated his retirement account to put a down payment on a $48,000 house in the city’s Startup Village. Why? Barreth, a husband and father of two small children, wanted to be among the first to buy a house in a Google Fiber neighborhood. His plan: to offer rent-free accommodations and access to Google’s superfast 1Gbps service to entrepreneurs for a three-month period.

If your startup does well in KC then this is what $2 million will buy. 9000 sq foot on a lake.

http://www.reeceandnichols.com/homes-for-sale/KS/Lake-Quivira/66217/233-Apache-Trail-West-Street-106786761

Dow/S&P roar, RE can surely only go higher and sunny skies again today, maybe another rerun of the Love Boat will air later today; the episode concludes with most passengers departing the boat having learned valuable life lessons from the trip. Some wise advice from Doc, a hat tip from the Captain, a hug from Julie. Isaac tells a joke, Gopher says something stupid. I’ve got nothing more to offer to the blog, it’s time to move on. Thanks for the great posts, Doc. Best of luck to all.

Drinks

Drinks, I always enjoyed reading your posts. Sorry to see you go, good luck in the future. This blog has definitely changed lately (not in a good way) and I too will likely be calling it a day here shortly. It’s just time to move on…

Another bear bites the dust. I believe the housing/stock market bear should be put on the endangered protected list…

Markets tend to finally tank when there are no more bears to capitulate. Careful what you wish for.

you’ve got the wrong tv show in mind.

Fantasy Island might be a better metaphor.

The case of not owning a home?

http://finance.yahoo.com/blogs/daily-ticker/renting-vs–owning-a-home-143539176.html

If you are a person who wants to feel a part of the neighborhood then maybe you should rent. Nothing like knowing your neighbor when you share a wall. Honestly I have rented many places and always knew my neighbors. Some I liked more than others, but only a few were complete jerks. Thank goodness for a third party mediator other than the police to deal with the jerks.

Fed set to roll out new low-rate pledge:

http://www.marketwatch.com/story/its-pledge-week-at-the-fed-2014-03-17

Translation: we’re all screwed because low interest rates are here to stay

On this general topic, I get frustrated by the main RE sites. Even though they have historical data, they price history window they show only allows a 10 year max.

That was interesting data during the first run, but at this point the window is 2014. So the ‘baseline’ they present is mid-boom, thus ‘normalizing’ the high prices. I’ve looked at housing in a few locales where prices boomed from 1999-2006 but never really busted. And the chart makes it look as if this blue collar area has always run 300k, even if it was 125k 15 years ago.

Now, the fact that in 2004 that same window showed 1994-2004 data suggests pretty strongly that they already have what they would need to allow at least a max window of 15-20 years for a longer term view.

Wish we could edit. In my ranting I made a few misspellings and errors.

The window is of course, 2004-2014, and one of those ‘they’s should be a ‘the.’

Zillow in particular has a lot of inaccurate information. They don’t receive all listings, and they don’t update in real time. It usually takes 3-6 weeks to update the a property has closed and sold. Transaction histories are frequently inaccurate.

But the abundance of information is a good thing — and it make the despised and overrated “REALTOR” more and more obsolete. The MLS still has the most accurate info, but the only inhibitor to having to pay RE “professional” the absurd 6% commish is the lock box. But basically all a buyer’s realtor does is get in the car and log in the internet a few times. A seller’s realtor is completely useless in this the internet age.

The more info available to individuals, hopefully they become more accurate and reliable at 3rd party sites, the more and more pressure it puts on the NAR. It will allow private individuals to have more access and control over the buying/selling process, with the utlimate goal of weeding out senseless commissions paid and better decision making among the parties involved in the transaction

I’ve had verbal fist-fights with real estate sector apologists and I can tell you they are convinced that they provide a value that is worth 6% of every transaction, and that it is not what it really is…. an economic drain by parasites.

In this day and age a real estate transaction should be no more than 2% total transfer cost. The very nature of the fact that the commission is a percentage is clear proof that the whole thing is a ridiculous racketeering scheme. What is the difference between transacting a $600,000 and a $800,000 except for $12,000 in commission being drained out of the seller and buyer’s pockets. So there’s a slight difference between retail and jumbo loans and high value loans, but it’s not a percentage and it’s not a substantial amount.

It’s a fraud! Plain and simple.

@Dan I agree. When I was in the industrial real estate business (leasing of warehouses, factories, etc) I noticed that often times the larger the transaction the more sophisticated the lessor and lessee… meaning the less headaches and problems with the lease transaction yet the broker still made 5% commission. It would be interesting to hear from any residential brokers – perhaps the ultra expensive homes are actually easier transactions (among the wealthy buyers and sellers) than the cheap homes (first time buyers and sellers) yet the commission is the same.

Remember that like Lloyd Blankfein (no relation to Lord Blankfein) from Goldman Sachs, RE agents are doing God’s work…

2% is close to the norm in many countries, the UK for example, and they seem to get by. Except that the agents aren’t driving BMWs.

Trust Zillow is like trusting Tour Factory Pictures, every home looks great then you go to see it and you wonder is this really the same home I just saw on the internet?

The Internet has made already lazy agents even more lazy. Look I was a part owner in a car dealership everyone said their car was excellent then they drove it in for appraisal, of course like Zillow estimates home, and Tour Factory, it was rarely the case.

Nothing takes the place as leg work in life, drive clients around and really show houses, teat drive the heck out of the car you are buying, the internet is a small tool only, never ever base your #1 and 2 most important buying decisions in life on the computer in front of you?

Little “r” – your sleaze is showing… “I was a part owner in a car dealership” From used car salesman to RE agent. Not much of a jump really. How are sales these days???

Never a RE agent but sometimes you have to have one, not all folks are smart like you??? Some actually learn to trust people in their life, they are excellent agents and professional sales consultants, they are bad doctors and lawyers, but I can assure you.

Going thru life trusting no one is also a slippery slope, trust your instincts, research, whatever, but many times just getting another persons perspective is invaluable, unless yourv

I see there is a lot of dislike for RE agents, all I can say is this, we sold our home last year and we were saved by our agent, staright up no joke, if your going to have a jab at someone have ago at the lenders who say their clients are “Approved” and 26 days into the transaction they come back and tell they are not after all and its no big deal.. We had already had our moving plan in place, movers ready to go, removed all contigencies on our new home and the buyer came back and wanted their deposit back and threatened to sue us if we didnt’, this is when you thank your lucky stars when you have someone that can hold this all together in a situation like this. No Zillow blog or stupid “App” can prepare you for this..too many sleepness nights and stress overload nearly did us in.

my buddy just sold his 2009 built home, as he got a job promotion to the Bay Area, so when he put it on the market, he needed to sell quick.

After it was on the market, I asked him if his agent was going to hold an open house. He replied, “I don’t think so.” I said, “why?”. He responded, “I think he’s too busy”. The house sold two weeks later, his realtor filled out some paperwork, took some pictures of the house, did no leg work, no marketing etc and walked away with his commission.

There’s no way around it: you have to be a scumbag to look yourself in the mirror with a straight face after doing jack for your client. Homes sell themselves, folks, in the internet age. Realtors go away, realtors go away. Realtors don’t find listings anymore now that buyers have the internet, they merely hold onto that lock box key with grim death because without that exclusive access, they’re toast — and they know it.

>>Trust Zillow is like trusting Tour Factory Pictures, every home looks great then you go to see it and you wonder is this really the same home I just saw on the internet?<<

Every photo appears to be photo-shopped (except the amateur, blurry ones). I saw one house photo in which the colors were so over-saturated, it looked like a Disney cartoon. Grass so green, sky so blue, the house's door so red, it looked a neon gingerbread house.

I'm guessing the greater the photo-shopping, the crappier it looks in real life.

Leave a Reply