SoCal housing market so hot, sellers finding the need to cut prices: One third of sellers in Orange County have found the need to cut asking price.

While the heat wave continues in SoCal drawing out the summer, there is little momentum from the 2013 real estate bonanza. Sellers with their awe inspiring wisdom are finding that no, they simply cannot ask for delusional prices on their stucco box crap shacks. As it turns out, a large number of sellers need to cut asking prices to get interest on their properties. New data shows that in Orange County, the most expensive SoCal county, one-third of sellers have chosen to drop their asking price. Some sellers of course are opting to pull their properties from the market with the hope that next spring, a new breed of sucker will be out in the market ready to plunk down $700,000 on a dumpy pad. In reality, many buyers just don’t have the cash to support current prices even with historically low interest rates. Given the option, many would buy if they had the means to do so. Instead, you have a large number of adults living with parents enjoying meals of Fancy Feast with a glass of Kool-Aid since they don’t even have the deposit for a rental, let alone a down payment for a home. The renting trend is moving along steadily. The market is so hot in SoCal that sellers are now having to lower their asking price.

Sales taking a big hit

As we have chronicled, SoCal is a boom and bust region. There hasn’t been a “normal†market here in two decades. The mania of 2013 has lost most of its legs in 2014. Things are running on fumes and when housing markets turn, you usually see it first in sales. Sales are taking a big hit.

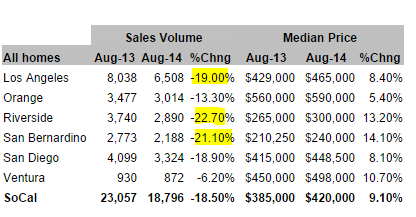

The Inland Empire has seen a big dip in sales in the 20+ percent year-over-year range for both Riverside and San Bernardino Counties. L.A. is down 19 percent and the OC is down 13 percent year-over-year:

Source: DataQuick

August sales hit a four-year low for SoCal. Imagine the curvature of a rollercoaster and that is symbolic of housing in SoCal. The headlines for well over a year on real estate have been incredibly euphoric. The opiates of housing optimism have been strong. The epic implosion of only a few years ago is now a distant memory. All those poor souls that lost their homes via foreclosure, forgotten like Civil War veterans. In SoCal, anything older than two years is like digging up the Dead Sea Scrolls. Yet this shift has been in the making for most of the year.

So it should come as no surprise that this trend shift is now being picked up:

“(LA Times) In Orange County, the region’s priciest market, about one-third of sellers have been forced to cut prices, according to data from real estate firm Redfin. Across the Southland, prices have hit a plateau this summer, with sales volume slumping as buyers got pickier.

These trends have been building all year. But home sellers — often the last to see market shifts — are finally getting the message, said Paul Reid, a Redfin agent in Temecula.â€

What a shock. Sales are imploding on already razor thin volume. Inventory still remains weak. No standoff can go on indefinitely. So some sellers are moving when the getting is good. Big investors packed their bags in 2013.

This is happening in untouchable areas like Pasadena. Take a look at this example:

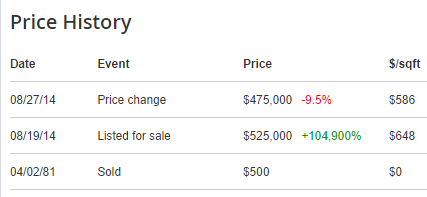

601 E Rio Grande St, Pasadena, CA 91104

2 Beds, 1 Bath, 810 square feet

Not exactly a dream home but for those house lusting hipsters, this place might work. It is around the SoCal median home price. Let us look at the ad:

“Home is located near great schools and shopping centers. Motivated seller and very easy to show.”

First of all, the schools in this area are not great. Second, if you are planning on having a family 810 square feet is going to be cramped. But maybe the price is reasonable. At first, they listed this place for $525,000:

http://www.doctorhousingbubble.com/wp-admin/post.php?post=7674&action=edit&message=10

What kind of pricing model is used when you knock off $50,000 in a matter of a week? There is little rhyme or reason in pricing homes in SoCal aside from “well she sold it for that so why can’t I!†In essence, that is model of how appraisals are done. So in a bubble, you are comparing yourself to other inflated properties. Then you have what we currently have which is a standoff, and then finally, some will budge. And guess what? This starts pushing the floor lower. Not an exact science here but easy enough to understand where cable housing shows will make potential investors drool with flipping dreams.

The boom bust cycle is unfolding again. Big dip in sales, and now finally, sellers backing off little by little. Big investors are largely out of the game in SoCal. In many cases, you will now have some Ramen eating home owner willing to sell for a nice profit to supplement the diet with some animal protein. The SoCal housing market is so hot, sellers are having to lower listing prices. That is how hot we are!

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

154 Responses to “SoCal housing market so hot, sellers finding the need to cut prices: One third of sellers in Orange County have found the need to cut asking price.”

3…2…1… for the the buffoons to start screaming “This cannot happen!!! SoCal is a world class city!!!!! This time is different! Prices will go up 30% a year, every year, forever!!! Why? Because SoCal is a world class city!!!”

Blo, on the pipe again I see.

Nobody but What?’s alter ego ever proclaimed 30% forever.

I predicted +6% yoy in January, and I’m looking good on that.

Yes, I’m probably the loudest and proudest when pointing out that LA is a world-class city. I am, by far, the minority. Most on this blog think LA is a disgraceful dump. Who is more correct, Blo?

@DFresh, prices are already falling month-to-month. That means that prices will soon inevitably start falling year-to-year. It may take several months before we see it in the annual figures, but it’s coming.

Housing IS Tanking Hard in 2014!

I stand by my predictions… what ever they were…

@DFresh, Los Angeles is a dump compared to San Diego or Irvine. Now, compared to Detroit, East St. Louis or Gary Indiana, well…..

@DFresh, here’s an interesting tidbit from DataQuick ( http://www.dqnews.com/Articles/2014/News/California/RRCA140911.aspx )

“Adjusted for inflation, last month’s payment was 35.5 percent below the typical payment in spring 1989, the peak of the prior real estate cycle. It was 47.7 percent below the current cycle’s peak in June 2006.”

***What this implies is on a nominal basis household incomes in SoCal are in decline. Hardly the signature of a world class city. If it weren’t for the interest rate manipulation by the Federal Reserve, home prices would be 1/2 the current level in SoCal.

@ErnstBlofeld – San Diego definetly has some areas with charm.

But Irvine? No soul, sterile and boring. Might as well live in Valencia.

Obviously, there are diferent tastes for everybody.

“Adjusted for inflation, last month’s payment was 35.5 percent below the typical payment in spring 1989, the peak of the prior real estate cycle. It was 47.7 percent below the current cycle’s peak in June 2006.â€

ernet blofeld: ***What this implies is on a nominal basis household incomes in SoCal are in decline. Hardly the signature of a world class city

Nominal Household incomes in LA might be declining, but to infer that from monthly household payments being cheaper now than 1989 and 2006 is ridiculous.

People like to complain about unaffordable housing prices, but LA has been unaffordable for a long time as the DQ data suggests. In fact, monthly housing payments were very affordable when the 07 bubble burst and low interest rates converged.

So, if the prices fall from insanely high to just crazy high we start seeing @Housing Tank Hards everywhere? I see no tank, sorry pal. The price are higher on YoY and will remain so in 2014. 2015’is when they flatten on YoY (I don’t expect them to increase in 2015) and 2016 where they will probably start to decline. And… I got a crystal ball, told ya already :p

Dude, once again, you’re in Seattle. pacNW market always follows SoCal but a year to 1.5 years behind. You’ve just affirmed Jim T ‘s prediction for 2014 housing prices here in SoCal.

Good job.

Seattle needn’t always follow L.A. There are significant differences.

* Seattle is said to have strong employment, with lots of well-paying, high-tech jobs (e.g., Microsoft, Amazon.

* Seattle is said to have a far better educated workforce.

* Seattle doesn’t have L.A.’s problem of absorbing so many poor, illiterate immigrants.

* Seattle, and Washington, don’t have L.A. and California’s fiscal woes. Might not be perfect fiscally, but in significantly better shape than SoCal.

Because Seattle has a better educated workforce, amid high-paying jobs, I don’t see that Seattle housing need tank like L.A.’s

“Seattle is said to have strong employment, with lots of well-paying, high-tech jobs (e.g., Microsoft, Amazon. ”

Son of L

Seattle also has Boeing which is massive in terms of employment with high wage jobs. It has the top guys (headquarters) who collect the profits from Costco, Starbucks, Nordstrom etc. It has a 15 bil./yr. biotech sector…and all these money for a relatively small population (less handouts).

Per capita, it has definitely more wealth that the “world class LA”. In Seattle and WA in general I never saw bars in the windows to make houses look like jail cells. On top of that the inhabitants of those jail cells are in bondage for life to the bankers.

One blogger mentioned that rain made him depressed in the 5 years living in Portland. For me, the window bars really make me depressed regardless of sunshine. Actually, WA state has plenty of sunshine in 2/3 of the state, east of the Cascade mountains.

“Seattle is different.”

“Seattle won’t crash.”

There’s a reason PacNW historically hates Californians. Let’s see how your Seattle immunity looks in 1 – 1.5 years. History doesn’t lie.

It’s a world class dump in many regards. That’s been well known for a long time.

I am curious, have rising prices led to more housing inventory or less? The classic argument is that rising prices have lifted people from underwater and now they have listed their homes for sale.

My argument is that, especially in this investor heavy environment, rising prices have led people not to list their houses. After all, why sell now when prices will be higher in a year?

I am curious to see what happens when price appreciation is lower than the 3-4% annual carry cost of a house. I think this will actually lead to more listings as people will scramble to unload, especially given the possibility of rising interest rates.

Any way, demographics and wages in no way come close to supporting prices in Southern California and a significant price drop is inevitable; it’s just hard to say when.

3-4% annual carry cost? Pass me some of whatever it is that you’re smoking.

Yea, 3-4% carry cost. It’s called reality.

Shill… he is smoking shill…

Smoking shill would be 1%. 3-4% is simply wrong. Tax 1.25%. Insurance $600 per year. Maintenance MAYBE 1%. 4%? Please…

Really, 1%. Like Mello Roos and parcel taxes don’t happen? Like HOA’s don’t happen? Like property insurance doesn’t happen? Like maintenance doesn’t happen and things don’t break down? Like, as in many of the investor houses that sit empty till sold, the grass doesn’t have to be mown and no type of water or electricity has to stay on? Yeah, that monthly nut, not so easy to calculate.

And all that doesn’t account for the investor thinking how much return they could get if the money was in something else that doesn’t require regular upkeep.

Come on AK. You can’t count mello roos and HOA on EVERY property because every property is not subject to those costs. In fact most resale homes DO NOT have an HOA or mello roos. Additionally I accounted for homeowner’s insurance in my post at $600 per year. I recommend Wawanesa and typically that covers most stucco crap shacks in the 1500-2000 SF range.

One good plumbing break and your out an easy 5000.00.. or more. There goes the profits. Insurance typically won’t coverthe actual plumbing portion either.

Who cares about wages and demographics when everyone and their Chinese mother wants to live in a world class dump such as Los Overrated?

@AK wrote: “The classic argument is that rising prices have lifted people from underwater and now they have listed their homes for sale.”

The classic argument works when home prices are move in sync with inflation.

When home prices are increasing 10% to 30% a year and inflation (the official phony government CPI numbers) is running at under 3%, homeowners are seeing their crap shacks in Pasadena go up $50,000 a year (which is more than what the average person makes in SoCal). This is like winning the lottery.

Home listings will continue to be abnormally low as long as home prices in SoCal go up faster than the rate of inflation. When home prices start to turn negative, only then will home listing volume skyrocket as these crap shackers look to cash out before the bottom falls out of the market.

Currently we are in a plateau. The zip codes I track are seeing wild month-to-month swings caused by very low volume and the mix of houses being sold.

“When home prices are increasing 10% to 30% a year and inflation (the official phony government CPI numbers) is running at under 3%”

Ernst,

The key to get the larger picture is the word you used “phony”. If you add the over correction from the time the banking system was frozen to the REAL rate of inflation you do get 30%. By the way, the phony government numbers say that housing in general (rents included) went up by 2%. Those are phony numbers.

Ask any building material supplier how much the prices went up in the last 5 years and you’ll hear what you see with your own eyes in grocery stores and gas stations. I understand you are as frustrated as I am. However closing your eyes is not going to change the reality. The inflation is much higher. Whatever is newly built or newly remodeled cost way more than 5 years back. Add to that government regulations on zoning which pushes up the land price (way higher inflation that 2% PHONY government numbers) and you get the picture. RE prices don’t go up every year 2%. There are years when they go up 30%, some 0%, some 2 or 5% but overall they are slightly higher than the REAL rate of inflation.

I am with you; it sucks, but that is the cruel reality of fiat currency. The new housing prices buy the same or less food, gas, tuition, health care, etc. than 5 years ago. We can argue that the real value went down but the nominal price went up. That is the problem with the dollar shrinking in its purchasing power. It is not house prices going up but the dollar getting smaller on the international market. That makes US RE cheaper for foreign investors.

How long until the market bottoms out…again?

Assuming that we go in to a recession in 2014, 4 to 6 years for housing prices in SoCal to bottom out.

Now that the Federal Reserve has used QE to pull the garbage off of the balance sheets of its member banks, the market cannot collapse as quickly as it did in 2008.

The downward movement in housing prices will make watching paint dry look like a fast action sport.

In the US $3.5 Trillion of QE, and US equity markets rising in value by $14 Trillion since the 2008-09 lows. China has been buying QE and ECB bonds at a lick of $40bn a month, but it is claimed that’s fallen right away now. (US and China tighten in lockstep – Telegraph.co.uk ‎- 4 days ago ).

If volatility comes back, I hope there are occasional opportunity for better housing prices, at crashed prices, at much lower prices. Without it dragged out over years.

I suspect there will be many an opportunity to buy at big discounts from today’s prices, not long into a correction.

methinks those who predict doom in the housing markets do protest too loudly. Bubbles will always form in the housing market because even the average person who wouldn’t set foot in the stock market sees betting (speculating) on real estate as a good way of securing their financial future and they are willing to pay whatever it takes because like all speculators, they believe eventually be worth much more than they pay. However it is only the big bubbles that do the damage. Think of earthquakes. We in SoCal regular get rattled but relatively little misery is created by this. The misery is created by the big ones that do billions of dollars worth of damage not the ones that just rattle your house for a few seconds. Size matters when it comes to earthquakes and real estate asset bubbles !

So if you want to get worried it should be because you think another big one is coming not simply another 3 second shake. If you look at it from this perspective I think you will conclude that it is simply very unlikely we will get anything like the 2008 bubble in the foreseeable future. Why ? For starters, the banks with the help of the Feds have succeeded in eliminating a lot of the most toxic assets. Not all of them for sure but enough that we would see the events of 2008 repeat themselves anytime soon. Also, banks have become extremely conservative in lending, not even giving loans to people who would have been considered reasonable risks (based on credit history and income) in the past so there has not been any significant re-inflating of the bubble.

So whither home prices in the near future ? I don’t see any big drops in prices for the reasons stated above. With much fewer people in financial distress they will just continue to sit on their homes waiting for things to turn around rather than panic selling or being forced to sell by the banks. It’s hard for me to see underlying demand shrinking much either. Most people still see home ownership as one of the best investments they can make and the high price of rentals plus the tax breaks of home ownership just intensify the underlying demand so it is just waiting for real demand to match underlying demand, that is for banks to start lending again and then prices will slowly start to climb until eventually we get to the next big bubble.

Unfortunately, I have no idea when this will happen as it appears banks are in no hurry to up their mortgage lending. The Fed has made it too easy for them to make money without taking big risks and they have diversified into making money other ways.

It appears that little house in Pasadena has bars on the windows. Looks like 475k for a 810 Sq ft prison cell.

That’s good comedy right there..the $500 initial sold price made me laugh out loud. I know it was a long time ago but 104900 % gain is pretty hilarious and goes to show how many lemmings are out there. Think I am going to list my 78 Pinto as classic for $100k as well..good stuff

A quick mortgage loan calculation for a $500 home in 1981, $0 down, 30 year mortgage @ 17%, mo payment $7.65. That was just 33 short years ago. You can barely buy a Subway sandwich for 7 bucks nowadays.

I’m assuming that $500 entry is either a “default” entry or someone sold their house to their kid way back when.

Thanks DHB

Your analysis would portend a positive feedback loop pushing prices lower.

My question is how will this reverberate through the economy? With so many cash buyers a “All-in”, how will it show up in the macroeconomy?

Last time it was defaulting mortgages? This time will inventory just sit waiting for prices to go up putting more pressure on renters?

Confounding times .

Did you not hear the good news that this time is different? Everything will be fine, do not worry, government will take care of.

Permanently High Plateau!!!

There is such thing in the bubble economy. If it no longer goes up, then I will definitely go down. The investors and the big money will need to find another way to generate 10% + a year returns…

I meant NO such thing….

“Given the option, many would buy if they had the means to do so”. Like I said, the pendulum went from, give everybody a loan, to give nobody a loan now.

But, isn’t, that good. Isn’t it supposed to create moar worthy borrowers that won’t walk away in the event SHTF?

Please spell Moar correctly. This is getting ridiculous.

@marco so your big contribution is spelling/grammer police? Do me a favor and shut the F up…

@Whatever,

and your contribution is to be a sarcastic one-trick pony.

Shut the F. up yourself!

These houses with only one bathroom should be going at a premium considering the drought conditions in CA.

But but many of the “experts” here said that’s impossible because housing will keep going up because the economy and the wealth our great fuhrer bla bla bla!?

This also happened after the summer of 2012, I know because I was flipping some properties and we quickly lowered below everyone to get out with some profit. The run-up into the summer was nice. Then as winter approached we saw rates keep dropping and prices dropped a little but held steady, so we had no choice but to go all in. Also what I did see then that Im not seeing now, is the instituional big money coming in. I stopped going to auctions when the $20/hr employees showed up buying 10-20 properties at then .90- 100 cents on the dollar. But it gave us a great signal to buy anything in sight that was discounted. The drop in 2012, never turned into much of a drop because thr banksters and government didnt let it. So I wouldnt hold my breathe this time around either. The market indicators don’t mean much anymore, just like in the stock market. Gotta watch what the .gov and their pals do, to get a more accurate read on housing.

Or, given three price crashes in SoCal in the last 25 year, we may be heading for crash #4. It ain’t different this time and it ain’t the “permanently high plateau.” Government may be able to change how things appear for a while, but can’t change how things actually are in this stagnant economy.

I am not convinced that it is possible to have a real crash during a fake recovery in a fake economy…

I agree with @What? America has never seen historically low interest rates for historically prolonged period of time combined with money printing at “official” rate of 85 bil a month. All we have is reinflated bubble that is called “recovery”. The reason why the prices grew to this level is the exactly the reason why they won’t collapse. We cannot have real price discovery in the fake economy!

C’mon guys. The data has been there for a year that housing is struggling. Low volumes, virtually nonexistent mortgage apps and a dearth of first time buyers. A few hundred thousand people selling one overpriced home to buy another is not a sustainable economy. That’s with the trillions printed. Credit bubbles always find a way to unravel.

Remember the low rates can be seen either as artificial or as a realistic reflection of how sh!tty the economy is. I suspect there is a decent element of the latter, which certainly argues against rapidly inflating home prices.

Certainly, nothing stopped the centrally planned housing bubble of 2001-2006 from popping. What makes you think this centrally planned bubble is different.

We are almost certainly toward the later stages of this economic boom cycle. It is crazy talk to speak of a permanently high plateau. The fireworks will come sooner than expected from a source that is unexpected.

@AK you missed my point…

@ What: I am not convinced that it is possible to have a real crash during a fake recovery in a fake economy…

EXACTLY.

What?

I got your point that this thing is all a charade and why assume market fundamentals matter. My point was reality always catches up to the fake economy. Last time we had a fake economy with HELOCs et al., the fed couldn’t keep reality at bay. They won’t this time either.

Can you make some sarcastic comments about antigraft legislation and Xi going after “Naked Officials”?

Can y

“Gotta watch what the .gov and their pals do, to get a more accurate read on housing.

If only I could be a fly on their wall. my guess is if housing prices do come down the large institutional investors will be right back first in line again. And then it will go up and then when it comes back down they again will be first in line, this could go on for decades.

+1

Prices can sit in this state for far longer than any of us can wait around. Let’s say you wait around for 5 years to save 10% on a $500k house. How much is 5 years of your life worth to you? $50k or $10k a year?

Market “fundamentals” exited stage left in 2000 and haven’t been seen since.

the govt. has used their 3 card monte trick….there are not 4 cards….

When rates goes up, pricing will go down….this is not rocket science….

The fed put was the best ever….don’t expect it again….too many other issues to deal with…

Now when is that FASB 157-8 being re-implemented…..this tells you the prop is still in play if they can’t go back to accounting practices no longer supporting price nirvana

There are problems in China. Electrical usage is down over 2%. This means that there is no real growth in manufacturing. For many years, the local managers have lied, now they can no longer do that. The Party is looking for these types of corrupt officials to have show trials. The real imposition will be in China. Sorry SoCal, no more hot Chinese money.

Gotta ask this. How hot was the summer? What were the air conditioning needs? What percentage of households replaced cathode ray tubes with LCD screens? No joke, has a large impact on power consumption in our media-driven society.

The housing market ship is sinking now after a long run up and overvaluation. The first rats off the sinking ship will swim the farthest and safest. We are seeing pretty good correction and reversion to the mean where I live but since the prices did not triple, our prices need not correct as dramatically.

What a crap shack. I guess the bars on the windows are to keep out the graduates of the “good local schools!”

Amateurs are going to look at the slight ups and downs in the market on a short timescale and cry that the sky is falling. Truth is, the market has never been better! It’s the perfect time to buy or sell a home. Ask me about getting full list price out of your home. Nobody ever got rich by being a naysayer! Time to dip your toes in the water… come on in, the water’s fine!!

YES!!!!

@get rich*ard, I want to ask you about getting the full list price out of my home. Before I do I’d like to know which real estate agency you work for and what your commission is. Did you sell real estate in the early ’90s and in 2011? How’d that work out for your clients?

After You GetRich*ard go ahead and purchase; then let me know how that works for you. In the 90’s the SoCal market was going down, then bottomed for most of the decade. The last downturn was about 5 years. This market is poised to do the same for @ least 3 years, in my opion. If those Orange County sellers that took their properties off the market plan on relisting in 2015, they will most likely be disappointed.

Richard is just being dick…take it easy on him…

“prices” in “Southern California” is like “weather” on “planet earth.”

SoCal is local, local, local. A patchwork of neighborhoods. Stong hands have gotten even stronger since the last buying opportunity in 1997.

So, no, Manhattan Beach prices are not going to react to a meteor hitting the earth the same as Lawndale prices.

And, wages?

* The global 1% wanna have a presence in SoCal…and there are tens of millions of these people. It’s about WEALTH, not WAGES.

* What’s the HH income of a Chinese national who buys a townhome for his little emperor to go to school at UCI?

* Already documented that people are willing to spend more of their HH income on housing in SoCal (It’s different here)

* Prop 13 lottery winners don’t make crap and still live in their million dollar crap shacks. Tell me how a “wage” matters.

* People renting out rooms, guest homes like crazy. Does this income get reported?

Another tidbit on wages; in my neighborhood, I notice there are lots of neighbors who are out going for walks in the middle of day or constantly coming or going in their car and I found out from a neighbor that there are several on my block who are retired government works (city, county, state, whatever). They must have purchased their homes a long time ago to be able to be in their mid 50’s and retired. They too will not show up as substantial wage earners… (I live in Baldwin Hills / Baldwin Vista area where homes were quite cheap in the 70’s and 80’s, now selling for $550K – $850K depending on street elevation and view.

Those gubbmint workers have a pension, and that pension is tied to the stock market. If stock market tanks, pensions tank, period. Those retirees are living high on the hog for now. I mean no disrespect or any ill will towards anyone, they are just trying to get the best deal they can for themselves, but that pension party will not last forever. One of two options: either the market crashes and pensions will crash along with it, or the Fed will kill the dollar to the point that those pensions become so watered down that they are worth far less than they used to be. As usual, those who live in the same residence for 30 years will be fine.

I have the same thing in my neighborhood except they are not old/retirees, they are in their 30s, 40, and 50s.

I go to school to pick up my son and 80% of the parents there are men, and they are definitely coming or going from work.

I come home for lunch and cars everywhere. People walking their dog, washing their cars. I think “do these people work”? My area is far from cheap. it takes a fat salary to support this lifestyle.

I went to look at a rental the other day, and the dude was breaking his lease because he was buying. He kept going on about he just had to have his dream home…. This guy couldn’t have been a day over 25. I see him in car line at school, and he drives straight home and stays there all day. I looked him up on lInkedin, lo and behold his occupation is “entrepreneur”. His car is permanently in his driveway. What’s he doing to make money? Posting youtube videos and collecting ad money? Average income in my zip is $118,000.

And yet all these people seem to not work.

TJ: “Those gubbmint workers have a pension, and that pension is tied to the stock market. If stock market tanks, pensions tank, period.”

Are you sure about that?

It’s my understanding that many govt workers have a guaranteed, fixed pension. So if the stock market tanks, any shortfalls in the pension trust fund will be subsidized with taxes. Which will then have to be raised.

@Calgirl I temporary moved back to Santa Monica (my home town) and noticed the same thing. No one went to work! People milling around the neighborhood like it was a Sunday afternoon. Not one parking space to be found on the street. No rush hour traffic leaving the neighborhood. It did not make any sense. Santa Monica was an aerospace town when I was a kid. Most went to work in the morning and the neighborhood was dead until after 5 pm. Strange times…

CalGirl, I’m probably the exact type of person that you’re speaking of. I’m in my 30s, and I still look like a relatively young musician with long hair, tattoos, etc., but I run my company in the TV industry from my home office, so I have a pretty flexible schedule that allows me to go out during the day. My wife stays at home with our 2 year old, and it’s great, because I get to see them periodically throughout the day.

What, you didn’t visit Santa Monica long enough. There is plenty of rush hour traffic during 4 – 7 p.m. Cars backed up on the California incline. Could take 5 – 10 minutes just to get from the top of the incline to the PCH.

I’ve seen gridlock along Broadway as cars try to get to Cloverfield to get on the 10. On rare occasions I’ve even seen gridlock on Arizona, when there’s trouble on one of the major arteries. And try going east on Wilshire or San Vicente. And on the 10 going east, it’s usually a parking lot from around 20th street to the 405 interchange.

For many years now, locals have complained about congestion. Just this past Monday, local pundit Bill Bauer wrote a piece in the Santa Monica Daily Press in which he called SM traffic “the most congested in Southern California”: http://smdp.com/santa-monica-lost-way/141904

I think Bauer exaggerates. I’m sure Downtown L.A. is at least as bad. But traffic is pretty brutal in SM through much of the day.

The increasing traffic, and the development projects that bring in more people and traffic, have for years been hotly debated among locals, and in letters to the editor of the SMDP.

Why don’t you write a LTE and tell them how pleasantly surprised you were at the lack of rush hour traffic. The response should be amusing.

SOL you missed the point as usual. A) your definition of “locals” is most likely different than mine. B) the traffic is not workers going to work rather “entrepreneurs” and “producers” wondering around the city “acting” busy. C) In 2008 I was on a project in OC and my daily commute was south on Lincoln to the 10 east to the 405 south and I was shocked that I could get to OC in less than an hour in “rush hour traffic”.

Wow,

DFresh, do us a favor and go to redfin, type in “Irvine, CA.” Look at sales prices for the last year (_completely flat_). Look up inventory in Irvine and come back and tell us what you saw.

Next, look up Japan 1990 to maybe draw some historical parallels to what societies do during and after their own national real estate bubble bursts. Next, pull up the GDP of China.

And, while you are at it, try to come up with a thesis as to why Manhattan, NJ, Atlanta and Buffalo, NY are all having similar price booms as well. Are the Chinese going to those places as well? No, California is not different.

I think the D is for dither. Lots of fresh dithering. About as fresh as horse manure.

Sounds like a lot of work to me…

Sorry I lived in Santa Monica for years and there is most assuredly rush hour traffic leaving the neighborhood, tons of it. I was working in Burbank and living in Santa Monica and it was a total reverse commute. In the morning as I was cruising east on the 10, I’d look to my left and see a parking lot crawling to Santa Monica. Coming home at night I’d look to my left and see a parking lot heading east. I’m not sure where all these commuters to Santa Monica live, I’m guessing the valley. Not sure what they do, maybe work service jobs?

What you say only applies to small segment of market where prices are over 1.5 Million dollars…SoCal is not the only place to park wealth fr Chinese or other foreigners…there are many many other places both on both U.S. Coasts plus Canada. Ask any of the new home sellers…the Chinese money has dried away during last two months….as they found out that they will lose money after they pay mello-roos and taxes at the current prices! Lastly, you can see many seller selling at even loss after paying agent’s commission..trust me…buying a home at $1.5 Million and selling after 3 or even 5 years is going to make you lose money…as the prices are way inflated…this is not what I say but what experts say about OC and to some degree LA market.

Well, just like Calgirl it has happened to me too. Our landlord would like to try their hand at an overpriced sale. They are really hoping that we will stay for all the repairs and showings, however that isn’t going to happen. I will not pay their mortgage while they play the lottery and mess with my time and privacy.

From my initial searches it looks like the rental market in LA is way better than it was 2 years ago. Even the market to buy is much better. And I’m talking quality and quantity. Prices are still whatever, and all over the map.

I’m also in a very similar position to Calgirl in that I have saved quite a bit. Yes renters actually do that!

In addition to looking here, I am actually thinking about leaving the state as my business could now be done from anywhere that has decent internet and I would be close to not needing much of a mortgage, depending on where and what I choose.

Interesting times indeed. My latest observation is the increase of open houses and sales that are pushing potential plans for the property. I went to one where the kid showed us around and said things like “this COULD be a master bedroom and it COULD even have a deck and a walk in closet”.

Oh really? Your price COULD be lower since I don’t see it here NOW!

Also I quite enjoy watching these fools that are moving into areas that are supposedly gentrifying, but paying the post gentrification price to get in. Whats the point?

Looking forward to my next landing spot.

I laughed at your post. Can you negotiate a reduced rent for the repairs and showings? What a pain in the ass either way though. Be careful about moving to another state. I moved to Portland. Tried to make it work for 5 years. Got so depressed I had to move or kill myself. Took a huge financial bath selling my house in 2010. Arrogant little f*&k buyers demanded everything. I hated them. Now I’m one of them looking to piss off some seller.

They have offered a prorated rent on the days the work is happening, but I’m not going to do it. They told me they hope I stay for a long time when my lease expired but less than a half year later they drop this on me without any warning. Not even a “hey we are thinking of selling in the fall.” Therefore I am not going to assist them in shooting for the moon by staying for what could be a long listing. Honestly I believe they need me here until the day they sell. They freaked out when I paid a few days late when I unexpected had leave town at the turn of the month for a death in our family. I was surprised that he couldn’t afford to float a month’s rent for 4 days. The landlord is broke!

I bet we’ll see a lot of this now. Houses peak above water a little bit and the folks renting out until that day all want to try to sell now. The inventory is clearly piling up all over Los Angeles.

Yet people say that Portland is so green, and lush, and verdant. Great mass transit. A sophisticated city, yet with a small town feel. Pedestrian and biker friendly.

Of course, they also say it’s full of homeless youth, druggies, and strip joints.

Sonofalandlord, most of the good is true. I’ve been in LA 15 years, and my wife was born here, but we’re moving to Portland next summer. I can’t think of a US city I’d rather live in at any cost. Granted, it should be said that my wife and I can’t stand warm weather and sunshine, despite being Californians. 55 degrees and overcast is where it’s at, for us.

Welcome to the club! My cheap landlords put my rental on Craigslist, too stingy to even pay $500 for a FSBO listing let alone $30k in realtor fees.

If your landlord is broke, mine is more broke. I pointed out to them the repairs they would HAVE to make for it even to pass appraisal. Cracked windows, no insect screens, dishwasher on its last legs, wood floors with missing bits and trim, etc, etc (all of this was present when I leased the place),. They refuse to spend a penny.

My landlord’s sucker parents have been carrying this place for 10 years. I went to the county and looked up their loan docs. OMG – IO loan at 7.10% taken 10 yrs ago. I calculated the difference to be $1,200 a month between what I pay and what it costs them to carry it every month. BEFORE repairs. 10 years this has been going on. $144,000 IN THE RED just to avoid a foreclosure.

How’s that for a “smart investment”?

So far not a single call or showing, No surprise – $80,000 above appraised value. I assume they are just trying and holding out hope some greater fool will come along and buy their “dream home” aka fixer upper. People are high…

“My cheap landlords put my rental on Craigslist, too stingy to even pay $500 for a FSBO listing let alone $30k in realtor fees.”

I had to read this 3 times to get my arms around it!!! I thought at first that you meant that they were trying to rent while selling (you see this a lot on craigslist). OMFG!!! They are LISTING the HOUSE on f’ing craigslist!!!! ROTFLMAO!!! Please stop! I can’t breath…

Consider the possibility that they actually got a loan mod with a significant rate/payment reduction which is what has enabled them to keep carrying it.

Delusional sellers are all the craze right now. Properly priced homes are still selling in my market while the overpriced junkers sit. Inventory shot up briefly because sellers got too greedy after seeing prices increase in 2013. Now they are starting to pull their properties off market and inventory is dropping down. I don’t know about up north, but that is what is happening near me in So Cal.

CAB if they got a loan mod, it was probably fraudulent. Good luck getting a loan mod on an investment property. The rules are very clear, homeowner occupied.

Reading stories like this makes me cringe. Not having to deal with this crap (being evicted from your rental) is why some people are willing to pay a premium to own. This is especially a nightmare when you have a kids. Hopefully everything works out for you.

I would agree with you if we were anywhere near rental parity/parody baaawk!!! The fact that it would cost me twice as much to look at the waves from my rental if I was to purchase makes buying a really bad idea BAAAAWK…

Its hardly an eviction. Really they want me to bail them out. Reading stories of foreclosures make me cringe and wonder why people paid a premium to lose their down payment.

if i made a comfortable living from home, i would definitely move to hawaii.

you have the right idea, there was a 30 year drought in California back in the day…when there were a mere couple hundred thousand people, now with a water system made to support 17 million not 39 million it would behoove you to look in states where you have water, own it and don’t have to worry about it. I was going to be buy second home in the the sierra foothills, I’ve now changed that thinking and buying up in the ever flowing water of the columbia river basin.

Without water, every home and mansion in California is worth zero….No rain this year will make discussion about house prices a moot issue. The messed up psyche of southern Californians with their big green lawns is rediculous. At some point Northern California will tell Southerners to find their own water, you are not getting jack from us.

it will happen. The central valley will collapse economically without a good rainy winter, everything you buy will be beyond what you imagined in price. Water is life… Wake up people….their is no el nino…god is not going to save it….civilizations move when water dries up. It will be no different.

worrying about housing in today’s world is rediculous….it will go up and down..it will not go up without water…..get ready, Mother nature is a bitch when she see’s the wrath of what stupid humans have done to this once great state….

Peak California has passed…..enjoy your nice mansion while carrying an uzi while hunting for water…..

We will march on into the Oregon Territory before we give up our swimming pools and green lawns in the desert. I hear that they have plenty of what we want, WATER. Since California is burning from the north to the south, time to get ready to invade the Oregon Territory because they do not want to share their water with us. We already took the water from Nevada and Arizona, onto Oregon, then Washington and then BC.

The Observer: “Oh really? Your price COULD be lower since I don’t see it here NOW! ”

_____

Haha. Also Good anecdotes – thanks.

At least it looks like yet another investor wobbling about prospect of the value of their property, and another looking to sell up. Good luck The Observer.

tolucatom – in booms when prices are running up and away, it’s claimed buyers wear rose-tinted-specs when viewing houses, telling themselves problems here and there not really an issue.. in the frenzy to get a house/better house. When things slow, buyers can be so much choosier, as you have experienced. Your turn to make owners pay. Sellers on the market are (will be soon be) “waiting to give you their money” via ever lower house prices, accepting ever lower offers (in my opinion).

Brain wrote:

“When things slow, buyers can be so much choosier, as you have experienced. Your turn to make owners pay. Sellers on the market are (will be soon be) “waiting to give you their money†via ever lower house prices, accepting ever lower offers (in my opinion)”

Sadly, though, this didn’t really happen in SoCal last time. By and large home owners simply took away their toys and left the playroom. Yes, there were a few deals to be had, but inventory was pitiful for years. I have no doubt that SoCal housing prices will turn negative (if they haven’t already), but it may take quite some time before most current owners actually capitulate and sell for lower prices than they’ve grown to expect.

On a different note – nothing like a 110+ F heat wave (45C for Brain) to kill my desire for a larger home in these parts. Just thinking of cooling that huge volume of air in those 2 story monstrosities I once so coveted puts me off my feed….

I see two markets in SoCal pulled by different fundamentals. One is people both locally and around the world that want a piece of the pie.

The other are people that earn a living based on wages. Those are the people that depend on financing to buy a house, and are generally Inland as well but not always.

I see coastal falling 5 to 10% and Inland falling 20% or more whenever it happens. The shenanigans of the Fed make predictions nearly impossible except for the fact we know that mathematically things just arent right

This market is dependent on interest rates,

Have anyone noticed the abundance of ‘survival shows’ on TV. People living off the land, building debris-huts. Killing and gutting whatever they can trap. Why this sudden interest in survival? Does this portend our future, and in some unconscious way?

Post Ebola mad max escape from LA style

Naked and Afraid…a sign of times!!

Hello Jim. A ‘tanking’ does not appear eminent for 2014 but here is a rational explanation of a decrease expected in 2015:

http://www.advisorperspectives.com/dshort/guest/Michael-Lombardi-140915-Home-Prices.php

My money is on a return of our favorite monster – ’70’s era stagflation. Everything is pointing to it.

There isn’t the additional supply to push prices down and there isn’t enough healthy employment growth to push prices up. The crash was precipitated by the NINJA loans which artificially pushed up prices as demand outstripped supply. These same NINJA (or near-NINJA) buyers were an important causal event for the crash when they stopped buying and then stopped paying. We have no such triggering buyers or events right now. Prices won’t crash because of QE and the house horny buyers that still exist and have a few bucks. Prices will start flying when (if) employment picks up.

Welcome to the Carter Malaise Redux.

“My money is on a return of our favorite monster – ’70′s era stagflation. Everything is pointing to it.”

I’ll take that bet. In the 1970’s we had a manufacturing base and China was still in the dark ages. We are now in a world economy. The only way for wage inflation to happen in the US is to have income parity with a Vietnamese guy in the jungle working for a bowl of rice a day (add fish sauce for overtime pay).

We don’t have income parity, but we do have the Fed to make up the difference (for now.)

@TJ The fed has failed miserably at creating real inflation. They have created some price inflation but no wage inflation after years of zirp and trillions of QE. I am not sure what tricks the Fed has left up their sleeve but I am willing to bet that it will not create wage inflation for the reason I stated above. Unless… they find a way to export wage inflation to the jungles of Vietnam… hmmmm

@What?: “The fed has failed miserably at creating real inflation. They have created some price inflation but no wage inflation after years of zirp and trillions of QE. I am not sure what tricks the Fed has left up their sleeve but I am willing to bet that it will not create wage inflation for the reason I stated above. Unless… they find a way to export wage inflation to the jungles of Vietnam… hmmmm”

Raise the federal minimum wage. 14 states have already done so in 2014. The bottom 10% earners are the only income group to see their wage rise in the past year.

“Raise the federal minimum wage. 14 states have already done so in 2014. The bottom 10% earners are the only income group to see their wage rise in the past year.”

Jack in the box,

It sounds like you missed your 3rd grade math class. X dollars available for wages divided by Y number of employees. X is fixed for the reason I stated above. Actually it is falling but never mind that. The result will be a further fall in Y (worker participation). That has been the fed’s goal all along. My money is still on the opposite side of the 1970’s style stagflation bet…

Jack skipped out on civics class as well. States have no power to legislate federal law.

Stagflation is SUCH a catchy term that it keeps popping up for those who can’t figure out the direction with so many cross-currents underway.

1) Stagflation HUGELY turned on a wildly ramping energy tax. No-one ever uttered the word until OPEC’s bite bled the Western world’s economies.

The West tried to print its way out of it: all of the fiat powers started running massive central government deficits. (USA, Britain, West Germany, France, et. al.)

Even Japan called OPEC the “great shock” — they even turned the expression into pidgin: “shoku.”

This time around, America is wildly ramping its crude oil production. Canada is wildly ramping its syncrude AND crude oil production. (The Bakken crosses the 49th parallel.)

The result is that Washington and Ottawa are seeing ‘magic revenues’ dropping down from Heaven.

If Barry Soetoro hadn’t punked the economy, he’d be on a Clintonian high, right now.

Many of the stock market leaders are linked to this crude oil surge. (Others are flying on their hidden/ not so hidden connection to 0-care spending.)

The rest of the market is gradually being punked. Central government interference/ direction is now entirely dominating the winners/ losers selection.

So STAGFLATION is bad terminology.

%%%%

You’re looking at a cross flow of hyper-inflation and deflation/ credit contraction.

System wide pricing can’t deflate so long as the central government keeps jacking up Big Academe and the Insurance/Medicine/Pharma/Legal Cartel. For those, in that sector, times are still rolling right along.

The other sector that’s doing well: the Security/Insecurity Sector. This sector is ramping away even faster than the Insurance Cartel. Every sub-sector is in a hiring boom. You’d think it was WWIV.

The investment rules for the 1970s must lead to bankruptcy. Ask Carleton Sheets!

blert: “You’re looking at a cross flow of hyper-inflation and deflation/ credit contraction. System wide pricing can’t deflate so long as the central government keeps jacking up Big Academe and the Insurance/Medicine/Pharma/Legal Cartel. For those, in that sector, times are still rolling right along.”

Deflation and credit contraction all the way for me. Markets can be self-balancing. Fresh volume lending on much lower house prices good for the economy.

And deflation to break up overleveraged companies. My brother and his colleagues would like to takeover the over-expanded firm they work for… currently run by the 3 guys who set it up 3 decades ago, who overexpanded in 2006… alive with forbearance, and the olides still pulling the big incomes out of the company. Let it go under, let them buy it for 30% current value. 10 new people getting higher income, instead of 3 oldies who already have high-end housing bought decades ago. Sell off the non-core parts to other younger interests.

Not that I like to cite this source, but the Soetoro thing is dubious: http://www.snopes.com/politics/obama/birthers/studentid.asp

Hackman…

Snopes consists of not much more than the opinions of a married couple living in the San Fernando Valley — who are HARD LINE to the LEFT.

They’ve spent all of their ‘corrective’ energies going after the GOP — and shielding their pals in the Left.

That’s right, they’re just a hyper-liberal husband and wife.

As for Soetoro, logic dictates that he HAD to obtain Indonesian citizenship to attend public school there. Foreign nationals are not permitted.

Not every nation has America’s ideas about open borders.

Barry’s admission documents make absolutely PERFECT sense if he used his international status.

No-one would ask if his mother was a native born American citizen. They’d key on his adopted father.

A classic device for stopping a true rumor is to put out forged evidence — yourself.

Then, you debunk your own forgery — via Snopes — and discredit the real documents that have hit the Web.

Soetoro’s admissions documents are wholly different than Snopes’ linked submission — which is so absurdly easy to debunk than it looks like it was ginned up for just such a debunking.

Such trade craft is taught by the KGB/ SVR as well as every other agit-prop school.

[If you’re not aware, the KGB/ SVR is NOT a spy organization — it’s an INFLUENCE organization. It’s specialty is manipulating public opinions of target populations. If the KGB/ SVR were ever to run across a military secret it would instantly hand it over to the REAL spies: the GRU.

In “The Falcon and the Snowman” the American traitors are ONLY talking to the GRU. That he’s pitched to them — and the general movie audience as being a KGB agent — is absolutely classic Soviet dis-information.

The GRU is normally NEVER fingered in the American popular press. It’s ALWAYS identified as being ‘the KGB.’ This is why the KGB is assumed to be a spy outfit. ]

BTW, the GRU HATES the KGB — and vice versa. In Stalin’s day he used one to liquidate the other — repeatedly. It’s a rare Westerner who knows any of this, even though it’s in the open literature.

Hackman…

The birthers may have the last laugh:

Kenya — the government — has never backed away from claiming that Barry was born there. He even has a resolution passed by the Kenyan legislature saluting that fact.

Barry’s best buddy, the Hawaiian Governor immediately went to the records to prove the birthers wrong – the moment he came to office. He discovered that no such evidences existed. If anything, the stuff out on the Internet figured to be totally fraudulent. So, he started swallowing his words. He entirely recanted his position over the next 96 hours!

Stanley Ann Dunham obtained a US passport in 1960/61. The US State Department has already posted to the Web her RENEWAL which was duly issued in 1965. The officials still are hiding her original application. Working back — using the existing laws and procedures — Stanley Ann HAD to have had her original issued in 60/61.

Yet, she never needed one unless she was to leave North America. Both Mexico and Canada would’ve accepted any American state ID for short visits. (Still do.)

There’s only one point on the compass that needed a passport for Stanley Ann.

You guessed it.

BTW, in 1961 abortions were rare — traveling to a far location for an embarrassing birth was as common as blue skies. This latter reality is entirely lost on the younger generations. Today, it is never done.

It turns out that her mother and father had a direct pipeline into Kenya — due to their employer. It was their employer that hooked the Dunhams up with Obama, Senior in the first place. That’s how they ever met. That’s the tabooed connection.

the 70’s were about wage growth, not wealth growth…..please give me a 12% CD, I’m all over it…..2015 is not the 70’s, we are in the last throes of the debt pusher game….it will not end well…

Peak California…..is in the rear view mirror….delusions are fun…enjoy them while they last…signed ex s. californian…..

the fed, they can print until oblivion but when it falls into the debt pushers hands only, well you get bubbles and those bubbles break…..they always do….if you find one that doesn’t I’ll buy you a couple Ninkasi Total Dominations for your enjoyment…

Blert, totally agree re Snopes. And you’re right, it is just a little too easily debunked to be serious. What do you make of the National Review debunking? http://www.nationalreview.com/corner/265767/pdf-layers-obamas-birth-certificate-nathan-goulding Will the truth ever come to light?

So we are in that living with parents category and are in the process of trying to buy a short sell in Ontario, CA. We are waiting on the banks approval but wondering are we making the right choice. Do we buy this short sell or do we rent for a while until prices come down? Thoughts? What would you do?

If you can afford it by traditional measures, plan to stay for 7+ years and have job stability, then yes. If you are stretching your budget, then no.

wait….

where you going to get your water if it doesn’t flow? the odds now are for correction on many fronts….the fed cannot worry about housing anymore….they have some different issues to deal with now…..

Jen,

We looked at numerous short sales and put in cash offers on a really cool home, with a backyard to die for. We pulled the plug on the offer. One, the price was absurd for the amount of work it needed. Two, we didn’t get any compensation for the damn wait. As it turned out, the bank came back to the “winner” asking for more money. It closed $60K higher than their offer. We walked and eventually found a better home from a Dementia Trust, $125K cheaper, listed as a fixer in the MLS. The short sale had a fantastic pool/spa combo, much nicer than the home we bought, but our floor plan is 10X’s better, and is within walking distance to a shopping area (WalMart, Target TJ’s, Big Lots, etc…). Just a data point for you. Short Sales aren’t always a good deal.

Laura: “with a backyard to die for. … a fantastic pool/spa combo,”

I wondered what qualifies a backyard as “to die for” material. A pool/spa combo? That’s it?

I’ve seen houses with spas. It’s always a negative for me. Just something I’d have to pay to remove.

I’d read on Truila that specialty features sometimes make a house an especially difficult sell. A homeowner might spend money on something they regard as an asset, but which some potential buyers will see as a problem.

Not everyone wants a rock garden complete with Buddha shrine, or a built-in hot tub, or sauna, or sound-proofed audio recording studio. I actually toured a house that had a built-in recording studio. Kinda limits the buying pool to musicians.

Depends. In the IE a pimped out rock pool and spa demands a premium. Do you have any idea how much it actually costs to put in a pool and spa nowadays? It’s insane. What was 30K less than a decade ago now costs $60K.

They are predicting a fed funds rate of 4 percent by 2018.

What would a 30 percent payment increase do to California bubbles?

Now it is interesting that the stock market is not pricing a 4 percent rate while precious metals are.

Something is going to pop and something is going to dump. Somehow I don’t see 4 percent fed funds in this decade or anything near it.

It could happen for 4-6 months and then every speculator will whine and cry to his rep…and they will demand money printing to help the sheeple…..the fed will act only after the popped bubble…they make bubbles to deflate them….they play both sides….not one side like most of the american sheeple…..

no way price gains continue, that bubble is done….the fed fix is over…..next thing to worry about is here…

When will this ever end? When can a HH with an annual HH income of $200K- $300K will every be able to buy a decent home in a decent neighborhood in L.A.? Right now all that HH can hope for is some crap shack in a crime-riddled neighborhood…

Dude, anybody making between 200 and 300K in this city can buy in nice areas (obviously not Malibu or Newport Coast super prime areas). It goes without saying that these people will have nice down payments and even if they are ultra conservative and borrow 3x annual income, they can easily afford 700K to 1.1M houses. Even the bears here can point you to some nice areas with nice houses in this range. If not, let me know and I can help you.

@Alex, you sound like a Troll. If you’ve got a household income of $200K per year, you’ll qualify for a $900K mortgage. Assuming 25% down payment (a big if since most Americans have no savings), then that means a $1.25 million home. This will get you a house almost anywhere in SoCal including Manhattan Beach.

Actually Ernst, a first time home buyer with no equity in their early to mid thirties with children has probably only been making big money for a few years.

On the way to this point in life they paid off student loans etc… and most of their saving is bundled up in 401K and other retirement plans. Saving and additional 200k to 300K for a 20% down payment on a modest home in a desirable LA neighborhood is not all that easy.

I pay over 30K a year iin child care each year (ony $6 k of that is pretax) for my three kids even though one is in school. (I do not reccomend having twins)

Those same $1 million dollar homes on historical norms would have been closer to $400K – to $450 K if not lower, that is a 10 – 20% down payment that IS achievable. See Larchmont neighborhood in windsor square to see the pricing i am speaking of.

Alex is in the same boat as myself and many of my peers. I pay 15% gross for my living expenses right now, i cant imagine extending myself to 305 to 40% just because i can

Let us remember that the original poster said “a DECENT home in a decent neighborhood” Not just a decent neighborhood.

With $1.2 million in Manhattan Beach you are looking at a Chevron Refinery adjacent 856sq ft shit hole built in 1950. Or for $1.18 you can get a 1376sq ft stucco shit box built in 1951 with and I quote, “Granite (from Spain) counter tops.” It has a “private master suite” – yeah right. show me the 1300sq ft house with a “master suite”. Or you’ve got an East Manhattan (Artesia Blvd close piece of crap built in 1953.

@Ruprecht The Scoundrel

Which definition of “decent” do you people mean?

1960s definition: 1200 square feet, 3 bedrooms, 1-1/2 baths, 1 car garage.

2000s definition: 3000 square feet, 5 bedrooms, 5 bathrooms, helicopter landing pad, olympic swimming pool, tennis court, 10 car garage.

@ernst

And in the 1960s definition of ‘decent’ did that mean an utterly outdated shack built around 1890 that was 5x the salary that a very highly paid white collar professional would make?

In Manhattan Beach, you’d have 6 options at or under $1.2million and I don’t think any 1%er would consider them decent just like in 1960 no (then) 1%er would consider a 3 bed 1 and 1/2 bath shack built in 1890 decent.

3612 N Poinsettia Ave, Manhattan Beach, CA 90266

2 beds, 1 bath, 865 sqft! $1.2 million. Chevron refinery/LAX flight path adjacent.

I completely agree. At $130k a year it’s frustrating that a decent house in a decent neighborhood is out of reach.

End of the day, It’s the Unemployment Rate, You’re city’s unemployment rate goes up, your home price goes down. Inverse relationship..

What does a made up propaganda marketing scheme like that have to do with anything?

Most people I know in SoCal buying have a HH income of $200K-400K. It is very common to earn that with two incomes. It’s not that hard in CA to earn over 100K or very close. This, two people with two good jobs equal $200K.

Mix and match:

Hollywood industry types.

IT Computer professionals.

Nurses.

Doctors.

Lawyers.

Business owners.

Software sales.

Other corporate sales.

Hookers (many make 500k year, $500 hour * 3 clients a day * 6 days week * 52 weeks a year = 468K cash! Per year)

So for all of you whiners about not being able to afford a home may be troubles to know that the 19 year old hooker is able to afford a home in Santa Monica with cash after saving a few years.

Sucks but true. Working hard at an average household income job isn’t going to get you anywhere in CA except broke.

I wanna move to Southern California so bad, I just can’t do it now ~ deep inhale~ ~long sigh~ WtF

if your dad moved to a nice part of LA in the early 60’s and he bought an apartment building in a nice part you would be all set

Is that deep inhale actually a bong hit?

Polo, Negative.

I’ve been wanting to move to LA for many years, but it’s ridiculous to try and move there now.

The Chinese way of doing business, I guess. “SHOE COMPANY: Our CEO Just Disappeared And Most Of The Money Is Gone”

Read more: http://www.businessinsider.com/shoe-company-ceo-coo-go-missing-2014-9#ixzz3DVKw85Sy

A hot foot, no doubt.

“The typical household income barely budged in a sign of the continuing sluggish economic recovery from the Great Recession, the Census Bureau said Tuesday”

http://www.latimes.com/business/la-fi-poverty-rate-census-household-income-economy-20140916-story.html

Hold on to something… we’re crashinggg. Well, perhaps not quite yet, but it seems all the preparation has been done. I can hear creaking too….

US main banks with $2.5 Trillion reserves, reflation years seeing dumb money chase overvalued assets for yield and on bull-sentiment, and settling outstanding mortgages in the banking system in the process. Now tighter lending. All the low-mid-to-high price ‘dead money’ equity locked into housing in good areas.. that the banks will want to get fresh debt on, at much lower house prices, that more younger people can afford, in my opinion.

______

‘Scared’ lenders, declining affordability making mortgages tough to obtain

September 16, 2014

It’s possible for would-be home buyers to get a loan, but it sure has gotten harder, and that’s because of lenders who are scared of legal and financial risks, as well as declining affordability, experts said Tuesday at a housing-policy summit in Washington.

“Lenders are running scared,†said Paulina McGrath, president of Republic State Mortgage, a Houston-based mortgage banker. “You have lenders constantly having to look over their shoulders.â€

http://blogs.marketwatch.com/capitolreport/2014/09/16/scared-lenders-declining-affordability-making-mortgages-tough-to-obtain/

_____

September 16, 2014,

Lenders’ willingness to back mortgages for younger and older would-be borrowers is being cut by regulatory, legal and financial uncertainty, said Jonathan Smoke, chief economist for Realtor.com, the National Association of Realtors’s site.

____

Citi, Goldman Sachs, others release stress tests

Published: Sept 15, 2014

[..]For instance, Bank of America’s latest adverse scenario features a U.S. economy with home prices declining 25%, compared with a 21% predicted drop a year ago. It also includes a 5.9% decline in Eurozone real GDP, compared with a 5% decline in the year-ago scenario.

http://www.marketwatch.com/story/citi-goldman-sachs-others-release-stress-tests-2014-09-15

Doc: ‘In SoCal, anything older than two years is like digging up the Dead Sea Scrolls.’

Haha. It’s true here also. People have forgotten. Prices reflated so quickly and it’s back to forever house price inflation, and people treating money/savings at an irrelevance, whilst they chase yield, buying investment property at painfully high prices. They need to have a hard lesson, one they won’t forget quite as quickly.

That’s one scary looking house. From my European perspective, from outside, it looks like a poverty shack in some backward country. Some of these sellers will crack, and accept ever lower prices, bringing down values for all the other owners. We’ve got them under siege.

Do we really believe banks are just going to spend the next 5, 10 years.. just sitting back and looking at all those hyper-expensive houses, with probably the majority owned-outright, or by the older equity rich? No, imo, they want to get fresh debt on those houses… even if it means values have to crash, so younger buyers can afford it. 30 year loans very profitable for banks, and of course, the quality of the mortgages likely to be rated high (A-grade), when new borrowers are not having to service jumbo mortgages. Having money left over to spend in the economy. I think it’s coming… complacent older home-owners better watch out, prices can fall as well as go up.

_____

US mortgage applications fall to lowest since Dec 2000: MBA

Reuters ‎- 6 days ago

NEW YORK (Reuters) – Applications for U.S. home mortgages fell last week to the lowest since December 2000 as interest rates rose for the …

Re: US mortgage applications fall to lowest since Dec 2000: MBA

Have a look at this chart re applications 2000-2014…. and slumping hard 2014 (although she suggests possible other reasons to explain it). Debt revulsion against such high house prices in my opinion, harder to qualify for mortgages.

_____

Mortgage gauge hits 14-year low, but that doesn’t mean housing is dead

September 10, 2014

http://blogs.marketwatch.com/capitolreport/2014/09/10/mortgage-gauge-hits-14-year-low-but-that-doesnt-mean-housing-is-dead/

(The chart in the link above.)

_____

All that equity in older homeowners homes… need to write fresh debt against it. Look what Deputy Governor of the Bank of England recently stated. I think it’s a clue to future Western policy. A transfer of housing wealth back to younger people by house price crash, and banks then doing volume lending, as more of us willing to buy on lower house prices.

_____

June 11, 2014

Broadbent identified risks in the UK’s housing market as the greatest threat to the country’s economic outlook. He went on to say that the Bank will not directly intervene on house prices, but is instead only interested in “the rate of growth of mortgages, which is today very low”.

– (Broadbent – Deputy Governor Bank of England.)

_____

These are some of the totally complacent older homeowners who have no scars from house price inflation years, just their minds warped up.. always knowing its latest peak value. No scars like so many of us renters. Older owners who need to learn some hard lessons, in a house price crash.

_____

Daily Mail. September 2014

Average house price to hit $780,000 by 2040, says leading think tank

Kilo Charlie, My World, 9 hours ago

We purchased a property in 1983 for $72,000………today it’s worth $650,000 plus. It’s certainly possible and quite likely.

Sam, 3 hours ago

Bought house in 74 for $16k added extention about $8k now valued at $480k you do the math.

Thanks for your contributions — seriously.

“These are some of the totally complacent older homeowners who have no scars from house price inflation years, just their minds warped up.. always knowing its latest peak value. No scars like so many of us renters”

Brain,

Did it ever occur to you that those boomers millionairs didn’t get old for nothing? Maybe they learned something in their lifetime the younger ones still have to learn. You may go to school but being young and green doesn’t mean you know everything. As you advance in age, you’ll see that there is a big difference between what you learn in school and what life teaches you.

There is no substitute to experience. As you advance in age you’ll agree with that statement more and more. It looks that you are still at that age when you have a crystal ball and know the future.

Thanks tolucatom – just trying to add some reasons to keep belief, for those who are saver-renters, or waiting to upsize at better value.

Flyover… I’m not ageist. Perhaps you are being too sensitive? I’m not grouping all older owners/people together. Just giving examples of how there are many complacent older owners, and on the cusp of what may be the biggest house price crash of low-to-high prime the world has even seen…. they still expect their homes to x50 again by 2040.

I’m sorry but the only ‘experience’ these older homeowners have (the ones I quoted, of which there were many similar comments left on that article), is one of decades of house price inflation…. and many of them love it… they feel wealthy and superior.

That is what life has taught them… house price inflation to infinity? They need new experiences, including a time where house prices fall hard back. I don’t need a crystal ball to know that prices are already outrageously overvalued for younger generations, and that a lot is now converging, for market softening, now the banks are better capitalized.

To the loonies (up above) who believe that the housing market isn’t going to have a major downward correction, I say take your heads out of the sand and smell the coffee! The housing market is a manipulated SCAM, and a big-time correction is coming. Housing started to correct normally around 2007, but the banks and the federal government did everything in order to re-inflate the housing bubble. All bubbles come to an end! Plus, if you add in a poor economy, a lack of jobs that pay well, and an aging baby boomer population, a ticking time bomb awaits the housing market. Wake up you housing optimists/dreamers! The Grim Reaper is in back of the housing market. The hour of death is uncertain however.

It’s not easy to smell the coffee when you’re breathing in all of those exhaust fumes from the 405, jet fuel fumes from LAX, and refinery emissions from Chevron.

Even the Bulls know it’s coming but are still full of optimism

http://www.zerohedge.com/news/2014-09-17/goldmans-former-head-housing-research-predicts-housing-crash-within-three-years

Sold my 1700sf condo in bev hills adjacent for $730 in april. neighbor listed his for 739 a month ago, dropped to 699. His condo isn’t as nice, but it is still sitting 32 days later.

Leave a Reply