The Foreclosure Story Number 2: $136,000 a Year Income to Foreclosure.

You may remember the foreclosure story I wrote in July of this year about a professional real estate couple with a combined income of $130,000 a year. Most people welcomed the story since it provided a detailed look of a couple living in Orange County and how the real estate downturn will be a double-whammy for many. First, the declining market cut deep into their high income and second, when it came time to unload their house they were unable to do it because of a softening market and lost it to foreclosure. It happened in what seemed a flash. Many people outside of Southern California had doubts about this story. A few e-mails read like, “how is it possible for someone making $130,000 a year to go into foreclosure?†I can understand how someone in North Dakota has doubts of the massive spending here in Southern California but many on this site will attest to this reality of hyper-consumerism. Keep in mind the story was written the month before the August credit event of the decade. Most don’t doubt this story anymore. In addition, their high class living and massive debt was simply unsupportable. It was a Ponzi scheme and all that was needed was a tiny bump to knock everything off kilter.

If I get the chance, I try to watch CNBC on the weekends since they have some interesting programs. Yesterday I happened to catch the Suze Orman show and it was as if the foreclosure story part two was airing. Imagine a woman in a very elegant gray suit on a split screen with the host of the show. She looked like she was in her early to mid thirties. I wasn’t sure what to expect but when I heard “Los Angeles Real Estate Professional†I decided to watch the segment. Suze does a great job of getting the important details from people and making them feel comfortable no matter how dire their financial situation. No doubt her bachelor’s degree in social work serves her well since financial management has a lot to do with emotions. Either way, the shell of the story is that this real estate professional made $136,000 in 2006 and was expecting to make $40,000 in 2007. This was a compelling story so I wrote down all the details:

Profession: 10 year real estate professional in Los Angeles

Expected income: $40,000

Previous Foreclosure: Rental home (lost due to tenants going through a divorce)

Three Mortgages on Primary Residence

Mortgage #1 – $1,700 month

Mortgage #2 – $600

Mortgage #3 – $440 (for pool addition)

*One of the mortgages is a pay option.

Right from the start of the segment, I was shaking my head. These numbers were simply unsupportable. Suze asked her if she had any savings. She responded that she had spent all her 401(k) and other savings trying to stay afloat. I did feel bad for this person. She was a divorced mother trying to support her kids. My empathy went away quickly when I realized that she had taken out a 3rd mortgage on her home for a pool addition. It was obvious that this person was living a life that she could not support. When asked how much she owed on the home, she said $600,000. Then Suze asked her what she would be able to sell the current place for and the response was $550,000. I’m assuming this is an estimate since the home was not on the market and we know how quickly prices are falling. The area wasn’t disclosed but I imagine it was in the Los Angeles area. When the host mentioned selling the place and renting, you can tell that the guest paused and was not keen on this idea. Suze was trying to drive the point home that she was living well beyond her means and as she said, “you are already bankrupt†even before she files officially. The next response took me a back. “I’ll find a comparable job soon†with the implication that she can jump into another real estate job and be back to her six-figure income. Unfortunately, this market isn’t coming back for many years. And the reality is that she is pulling in $40,000 a year and with her current debt load, there is absolutely no way she can stay afloat. I’m glad to hear that Suze was recommending a short sale and possibly, get this, leaving Southern California. I’m not sure if the guest was pleased with the advice Suze had provided.

Analyzing the Industry

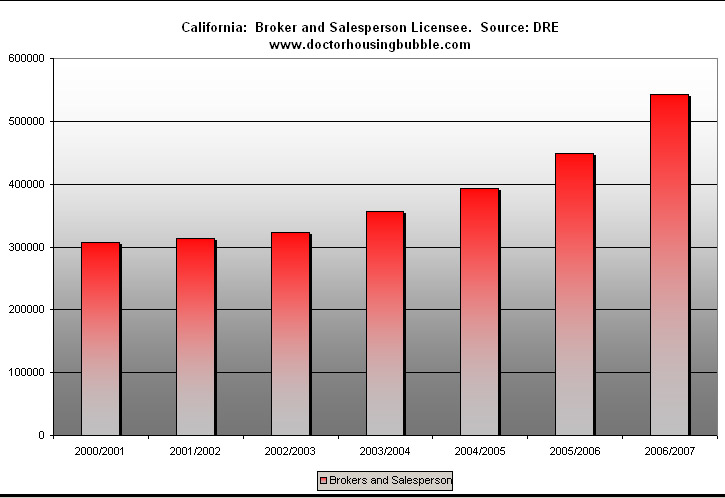

I’m not sure what will happen to the real estate professional on the show. Her expectation that things will pick up quickly demonstrate that she is not ready to move on both mentally and financially. In the interview, not once did she admit any responsibility for her financial situation. Her questions had the underlying expectation of “I will once again be back to a six-figure income so what can I do right now to maintain my style of life into the future?†It is important to understand that the real estate profession has been a national obsession, but here in California it has been the prime focal point for many. Let us take a look at the number of broker and real estate licenses issued here in the state:

From 2000 to 2007, we go from 307,051 licensees to the current number of 543,194. This is a 76 percent increase in only seven years. During this same time span, the California population went from 33,871,648 in 2000 to 37,700,000 in 2007. This increase represents an 11 percent jump. What we are seeing is a massive saturation in the industry. What this also tells us is that states like California are now heavily relying on a solid real estate market. Since California has done relatively well until this past month (at least on paper), we now know that every county in Southern California is negative year over year. What is also interesting to note is how many industries will be impacted by this coming real estate bear market. Here is data from 2004 – which of course was the start of the hyper-bubble so these numbers will be higher – showing the representation of industries employing people in California:

Total Paid Employees Statewide all Industries: 13,264,918

Construction: 834,742

Finance and Insurance: 699,086

Real Estate and Rental and Leasing: 302,014

Manufacturing: 1,476,211

*Source: Census.gov

These industries have a very close connection to housing. Excluding manufacturing, these 3 sectors make up approximately 14 percent of all California employment. Adding in manufacturing, these 4 sectors make up 1 out of every 4 jobs. You can understand why only a few down months has already shown up in budget shortfalls for the state. The state won’t see the major damage of the industry until tax returns are filed in 2008 for this current year. You can also imagine the number of people that will reassess their tax bills to account for the declining market. What will affect the California economy as well, as demonstrated in the CNBC interview, is that many of these high paying jobs will no longer be viable sources for employment. Even if people decide to stay in the industry, they will take radical cuts in their pay. With higher inventory, lower prices, and a glut of workers, the market has reached its critical tipping point. Like the often quoted 2 million jobs lost from the technology bust, this will have a much deeper impact since many of these people will have a hard time transferring their skills into another industry. Since their jobs depend on a healthy housing market directly, the employment numbers still look positive because it is a lagging indicator. Many of the technology workers had college degrees that helped blunt the force of finding a new career. As we know, the barrier for entry for a broker or an agent is nearly non-existent. What other industry will provide a comparable salary? The answer is there isn’t and this will also take a major blow at our consumerist society by; lower tax revenues, less disposable income (thus the link to manufacturing), and a self-feeding cycle of creditors offering less credit for fear of further defaults.

There are many sites digging deep into the details of the mortgage backed security debacle, the nuts and bolts of CDOs, and all other things mustered up by financial engineering. They sometimes miss the forest for the trees and if they would spend one weekend driving to these development ghost towns or looking at how agents and brokers operate in the inner city, they would quickly realize how prevalent the problem really is. No amount of financial alchemy is going to make a frog into a prince. I think many economist and financial gurus have missed one major caveat that cannot be measured in numbers, that of emotion. Whether the emotion is greed, envy, or security these things propelled the housing market into another dimension. I don’t doubt that many people bought homes to raise families and settle their roots. It is an American mental archetype that a “successful†family will have a home with a picket fence and 2 children. Just watch all the commercials for the Christmas shopping season. You’ll see a father pulling into a driveway while his wife and 2 kids throw snowballs (even though it never snows here in LA) at him and he slowly unravels a bag of diamonds for his wife. She slowly stops, offers him a slight smile and all is well in fantasyland. Marketers know what drives sales. And what about cars and car insurance? More money. The housing industry and Wall Street exploited this desire for many years whether it financially made sense or not. They got their fill of greed while folks on the street got this illusion of security and prosperity, real or imagined. Whether people like our guest on CNBC realize that the game is up, is another matter of personal self-reflection and coming to terms to a reality that is now vastly different. Unless you’ve lived in a high priced metro area, it is hard to understand this mass hysteria and irrational exuberance that centered around the real estate nucleus. But even now, the air is full of doubt and many people seem to say “real estate will go up again†more to reassure their own insecurity.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information

Subscribe to feed

Subscribe to feed

22 Responses to “The Foreclosure Story Number 2: $136,000 a Year Income to Foreclosure.”

Dear DR,

Thank you for another excellent article on point. This scene is going to be played out many, many times (probably more than a million and I won’t count the “investors”) over the next few years. This lady is just now passing the Shock and Denial phase. Next will be the Anger phase of her financial destruction. It will take a few months. Following that (probably due to the foreclosure or short sale) she will get into Depression and Detachment. However, she may have already skipped over these three and gone directly to Dialogue and Bargaining in a desire to reach out to Suze and tell her story. She will try to find some meaning for what has happened and finally Acceptance will be hers as soon as she has a new plan in place. Ultimately she will return to a Meaningful Life with some new-found self esteem in another career in perhaps another location. God bless her and all those who are destined to follow this path into the unknown.

I also happened to watch the Suze Orman show and had the same string of emotions you did. As soon as the guest mentioned that she had been in the real estate industry for 10 years, I knew that it was all over for her. She has absolutely no clue about the cyclical nature of real estate (“What?!? But doesn’t real estate only ever go up in price?!?”), and will learn a very hard lesson. It’s obvious that she hasn’t learned that lesson yet.

At some point Suze should have just told her that she is being irresponsible and if she is going to act that way she should do it right. So my advice to her is to max out all credit cards. Heck apply for more credit cards if needed. Since bankruptcy is around the corner, she may as well go out in style and really stick it to the banks.

It’s almost over guys.. Just a few more months before the unwind shifts into high gear. How is Citibank going raise billions when all their customers are maxing out the plastic?

What’s in your wallet?

For awhile I would go to open houses more out of morbid curiosity than anything but also looking for ideas of what to pay in the downturn. You don’t have an idea of when to buy if you don’t look at the prices while they are high. Anyway I stopped looking because I felt sorry for the R they are completely clueless and think this is a short term aberation not the new reality. When you see the sadness of it you almost feel sorry for them because some were honest “most weren’t”. Anyway I guess I am just an old softy

Thank’s Dr Bubble.

I enjoy reading your blog. You give a rational voice in the mid of irresponsible pump-up scheme by lender and realtors.

First best lesson I ever had in personal finance: spend less than you earn. Not even. Not more. Second: neither a borrower or a lender be. (Learned that the hard way wth some money lent to a friend with a chronic debt condition. Finally realized a) I was never getting the money back and b) her money problems were not solvable with money.) Anyway, there is example after example that you don’t have to be a Rockefeller to sock some away or to sleep well at night. Conversely, having a high income never has been a guarantee. God, remember our beloved MC Hammer? Those parachute pants earned him millions- he had platinum records, a kids animated show, income from his massive sold out concerts. But the dude went bankrupt pretty darn fast. All he had to do was consistently overspend, justify it, and overspend again. Speaking of justification, my favorite word from this whole housing bubble era is “leverage”. I guess it must have first gotten into the popular venacular from the likes of Trump, but pretty soon you had every average schmuck talking about their credit load with that word. They’d have balances due on 3 mortgages, 2 car loans and every type of plastic, manuevering from rate to rate. House of cards? -No… just “leveraging” their purchase power. Know what I mean, Doc?

Thanks again for yet another good analysis of what is in store.

–

Wonders are what cities like LA are going to do to support their liberal habits with a diminishing tax base.

Dr:

This is a true story:

20 Years ago, my mom owned a craft business, where she would make and sell fairly high-priced crafts. As part of her sales, she used to do private parties in people’s homes.

One time, she did a showing in a home in what has historically been the richest neighborhood in the Detroit Area. You know the type: old homes, old money. I won’t divulge the name of the city, other than to say that the homes were built by the auto and lumber magnets who built the city (and country).

Cut to the chase: when the host decided she wanted to purchase something, she had no cash. She locked herself in the closet while she scraped together change, checks and anything else she could find to purchase a $100 craft.

The moral of the story: Housing is not wealth. With the best home in the country and $3 you can buy a cup of coffee.

The value of a home is not what you tell your neighbors it is. It is not what the city says it is when you pay your taxes. It isn’t even what the Realtor says when your next door neighbor sells their house.

The value of the home is exactly equal to the little numbers written on the check you are handed when you sell it.

Now more than ever, it’s all about being liquid. Cash is king.

The age of “no personal responsibility” is an amazing thing to behold. People so savvy they have finances so complicated they rival a small foreign country’s annual budget, then, when the bills come in they realized they were only as sophisticated as a five year old and how can this be happening to them. But, in a couple of years the market will get better ( I hear this over and over by people underwater in their finances). They are market predictors at the same time they can’t by groceries. Absurdity, yikes.

Thank you for another trenchant glimpse at our economic dysfunction. I am sorry for saying this but it is chicken soup for my soul. I am a very financially conservative person. So Living in this speculative hell that Greenspan has created has been very hard for me. I feel very sorry for all of the all of the financially incompetent citizens that have grown up during this period. I would like to tell each and every one of these reckless young speculators that this is not how a normal economy functions. A societies’ wealth comes form savings from it’s citizens. Not government savings. Not speculation. Not credit. Not even higher productivity. Something must be saved by the citizens for the future. It has come to the point where our country has lost its direction. The Great Depression was terrible in many ways but it created of our countries’ greatest generation. The citizens created during this period fought in our last real war. They saved an average of 25% during this period. The following generations have spent this savings and now we are living on debt. It appears to me that the only way that we can save our society is to let the country float naturally into this coming recession. People need to learn the consequences of easy money and reckless spending. Unfortunately the reality is that the Federal Reserve will probably bail out the speculator once again. This will produce nothing but debt and financially incompetent citizens.

The situation in southern CA is similar to Florida, Las Vegas, and Phoenix, to name a few. Duane LeGate, president of HouseBuyerNetwork.com has been calling these bust markets since 2005. His ability to call them 6-9 months out has been right on target. It is difficult for most to swallow the warning signs, just like the woman who was on Suze’s show. However, unless we do, we can not even begin to think about rectifying the error of our former (hopefully) ways.

In my personal opinion, a major problem is the lack of true leadership. All one has to do is look at Wall Street and the demise of Neal and Prince, et al. to see that we are painfully bankrupt in leadership skills. Unfortunately these are the most public signs of lack of leadership but it is pervasive throughout society. It can be found in every industry and at all levels.It is a disease, that if left un-checked might cause a deeper and more protracted collapse of our society.

Well, I am glad I live in an area of the country where housing will not go through a slump, since we never went through the boom. Like politics, all real estate is local. *Malcolm* is right: cash is king.

Honestly, if anyone has three mortgages on their house they deserve what’s coming to them! Did this woman not have a clue as to what was coming? It was the perfect storm–I don’t have any financial or real estate degrees but even someone like me could see it! I agree with the other posters here that she needs to learn her lesson, and it looks like she’s going to learn it the hard way.

Hi from Grand Forks North Dakota. I laughed at the first part of the story…but yes we do have plenty of spenders up here. My wife and I cannot believe all the folks with two cars…two snowmobiles…plus a boat. Incomes up our way are generally lower than national average and housing costs just a tad below but we do have plenty of folks here with debt up to the eyeball and one paycheck away from being in real trouble. We do indeed have a bubble up here….not nearly as great of course….but prices overall have gone up about 40,000 to 50,000 for both new and previously owned homes since 2002. We built a 3500 sq ft home for $64/sq ft in 2003 and now it is close to $90/sq ft for new. Median home price is 167,000 this summer when prices peaked. Houses are on the market for a much longer time now than in the past few years and prices are starting to come down. Foreclosures and short sales however are rare from what records I can see. Over the past 5 years…about 60 new homes were built per year.

Very sad story that will be told over and over before this is over. But what should we expect? US government policies for years, but at an extreme since 2002 , have said….don’t save, borrow all you can, consume all you can, invest like you are in Vegas, and the government will cover the risk. Couple that with normal human greed and manic behaviors and you have what we have today. It is sad we have not had more responsible leadership in this country, particularily since 2000. We are only in the 1st inning here, but you could see this all coming 10 miles away.

Hey, came here from Kos for the first time. Just wanted to comment on your implication that a saturated agent market would make it more difficult for this particular agent to return to 3 figures again. Not that I don’t agree whole-heartedly with your assessment that she and her family’s core problem is that they live beyond their means… I just wanted to point out that the total number of real estate agents has less of an impact on how much the top earners make… the pot doesn’t get divided evenly. Roughly 7% of agents make most of the money, and when the market improves and more jump in part-time, they just fight it out amongst the other 93%. The top earners have social connections that keep them going strong as the market goes up and down. Their expertise is more valuable in a down market and the sales gravitate to them as a result. The part-timers with less experience are the ones that get hit, but they were never successful in the first place. So, if this person was really in the 7% at one time (I can’t tell from the article) then she could return there again, even in a down market. If she never was successful, just lucky in an up market, then there is almost no chance of building the expertise and network needed to succeed given her current situation.

But I would say to most people in this situation: Sell half your belongings on ebay and move to a more affordable locale.

Prices in Dakota going from $64 to $90/sq foot doesnt sound like a bubble to me. The price of copper, steel, cement etc is far higher now than in 2003. Replacement costs must be far higher now than in 2003.

She owe’s $600k but only pays $2740/month? That don’t sound right even with a pay option.

Interesting post about the professional on the show. When people living the good life hit the ditch financially, denial is probably the most common psychological posture. When somebody loses a regular 9-5 job, he doesn’t typically take steps to minimize his expenditures immediately. Or maybe he just does simple triage and trims around the edges – cut out the daily trips to Starbucks. The person keeps putting off making big decisions about major expenditures because of uprooting the lifestyle.

Unfortunately by the time the urgency of performing major triage finally sinks in, the person is already financially sunk. In the dotcom downturn in 2001-2003, there were stories about charities seeing cash poor laid off dot com execs driving up in BMWers and Audis and wanting a few grand to pay their expenses for the month. Mortgage, car payments, kids’ school tuition, etc. Such charities are used to helping a struggling low-income single mom with some food or a little money – nothing like that. Of course some got huffy if they were turned down because they had donated to the charity before so they felt entitled.

“Aid groups see more requests from from once affluent Collin agencies say high-dollar relief sought by some is unrealistic”, Dallas Morning News, May 20, 2003, April M. Washington.

Excerpt:

http://atrios.blogspot.com/2003_05_18_archive.html#200329694

Thanks, Doctor, for another dose of that hard medicine. When all of this was happening I asked myself many times “how can these people afford this”? Everywhere I looked there were new SUVs, granite countertops, and TV shows that highlight the most extreme spending possible – biggest boats, fanciest cars, monster houses. As a technology professional I make a pretty good buck but I really started to think I was missing something profound until I understood that these people were simply spending future earnings (debt) and had zero intention of ever paying it back. Just like the US gov’t has no intention of paying back 9 trillion in debt. We need a change. We need to abolish the Federal Reserve and all of the big government that complacency built.

We need Ron Paul in 2008. Google for Ron Paul and listen to what he says and then think about it a little bit. Or, vote for one of the standard plastic candidates because it’s somehow more politically correct than voting for the guy who is speaking the truth.

In the late 1980’s many people with sub prime loans walked away from their homes/mortgages. Check the Dallas stats to see what the effects were on housing following the unprecedented bank and S&L failures and decline in market values. The repossession and write down of property values so they could be sold again caused a tremendous decline in property values of the neighboring properties.With the additional incentive of not facing taxes on the forgiveness of debt, that is just another incentive to take on a risky mortgage that you can’t pay. Why not, you have everything to gain and nothing to lose.

This woman’s want to purchase a home was a simple math equation that she made more complicated than it had to be. She made $130,000 last year; I’m willing to bet she finally broke the six figure salary mark during the housing craze these last few years. But, I’ll give her the benefit of the doubt and assume she made that type of money when she initially purchased the home. Typically a buyer can afford a mortgage of up to 33% of his/her monthly household take home pay (and that’s assuming there are no significant outstanding debts like student loans, high credit card balances, etc.). $130,000 divded by 12 times 33% equals $3575.00. Based on the three mortgages listed in the article, she was paying $2,740.00 (exluding taxes and insurance) per month. So, theoretically, she should have been able to afford the three mortgages. But like so many people, she probably had other significant bills like auto, insurance, Starbucks habit, etc. She leveraged her financial future on the mistaken assumption that the housing market would not drop in price. I am a law enforcement officer; let’s suppose I decide to commit a crime because the end result would yield me a great amount of money–enough to change my lifestyle. I have the inside track on how officers think and conduct their investigation. Now, let’s say I got caught and was convicted. The judge sentences me to 15 years in prison (remember, this is hypothetical). My response is “I thought I would only get probation since I was a law inforcement officer. I also am sure I will get my conviction overturned on appeal…just because it’s rare that officers are sentenced to prison. The Real Estate version of my response is “I’ll find a comparable job soonâ€. My point to all of this is this person did not fully understand the historical nature of her “field of expertise”, for a lack of a better phrase.

Even if the market “bottoms out” in ’09, it does not mean that prices will shoot right back up; prices my just stagnate for a couple/few years until the economy picks back up. I am so tired of hearing of the “people waiting on the sidelines” to swoop in an purchase the over supply of homes available. I think those people are very few and the majority of people who wanted in on the great home ownership dream actually purchased within the last few years. Besides, if we are in a Recession, layoffs are coming, which will cause housing prices to futher drop or, in the best case scenario, stagnate.

Leave a Reply