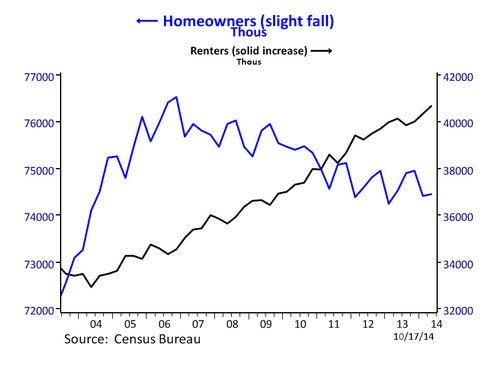

Rental fury: The trend for renting continues to grow stronger. Housing starts jump largely on the back of multi-family housing starts.

There was an odd sort of rejoicing last week in the midst of market volatility. Housing starts jumped but the people pointing at this failed to grasp that a large reason for this was because of multi-family housing starts. In other words, the demand is reflecting a nation that is becoming a renter class. This trend reflects a new workforce that has more part-time employment and less job security than the previous generation. Why would you buy a home if your employment is more volatile? The numbers are clear and we have added over 7 million renter households in the last 10 years. Right now we are at the peak of renting households. However, we peaked for homeownership back in 2006. Since 2006, we’ve actually lost about 2 million net homeowner households. No need to worry since Wall Street has taken up the slack to purchase those single family homes and convert them back into rentals for the new modern day serfs. The renting trend continues and the jump in housing starts reflects a change in home buying perception.

Deconstructing housing starts

It probably is worth digging into the housing starts data since some people were going hog-wild on data that reflects a trend towards renting. Once broken down the solid rise in housing starts was brought on by multi-family units. In other words, high density lower cost housing options. You would like to see a higher demand for single family homes if the case were to be made that households were gearing up to purchase homes. Yet this isn’t something builders are betting on.

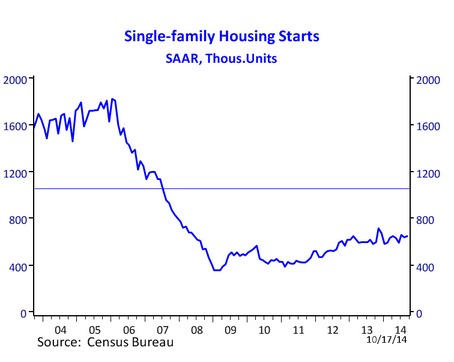

First take a look at single family housing starts:

Can you spot the so-called surge? Probably not. Since 2008 home builders have been holding steady when it comes to single family homes. After all, investors were out in the market looking for lower priced properties to churn out healthier rental yields. In places like California, many investors have already pulled back and we are seeing the vacuum that is being left. Many sellers are pulling their properties off the market thinking next spring and summer they’ll be able to lure in some new lemming.

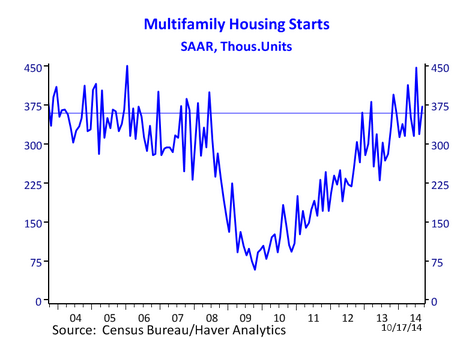

If we look into multi-family housing starts, we find an unmistakable trend:

That is what a surge looks like. This is a fury of activity to meet the demand of a renter nation. No need to spin the above chart since it speaks loudly as to what builders are viewing as the next big thing. Rents are holding steady and younger Americans are carrying large amounts of student debt and their salaries are unfortunately not all that great. That is why you have 2.3 million adults living at home with their parents in California alone.

We have added a whopping 7 million renter households in the last decade:

The number of households that rent has increased by 20 percent over the last decade. This is a strong trend. This of course is coming at the expense of creating less homeowners. This isn’t necessarily a good or bad thing. In fact, I think the crap shack addicted zip code chasers would in many cases be better off renting in the long-term. Many use the logic of “well over 30 years if you stay…†but rarely do they stay put for that long. Will you live in a 700 square foot shack for 10 years just to build some equity so you can then move into a 900 square foot shack in the endless property ladder game? This of course assumes your timing is on given real estate is now a boom and bust business. This is why in places like San Francisco, you have many high tech workers opting to rent and foregoing the chase to buy ridiculously priced properties.

It should be extremely clear that we are in a solid rental trend. You can look at the housing start data above and arrive at your own conclusion as to where this “surge†is coming from.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Did You Enjoy The Post? Subscribe to Dr. Housing Bubble’s Blog to get updated housing commentary, analysis, and information.

Subscribe to feed

Subscribe to feed

98 Responses to “Rental fury: The trend for renting continues to grow stronger. Housing starts jump largely on the back of multi-family housing starts.”

Given the realities of the economy, jobs, wages, etc. the growth of rentals is not necessarily a bad thing. Rents are usually for 12 month terms, giving the renter flexibility to move and follow jobs, or find cheaper housing, and non payment brings an eviction not a foreclosure! Landlords face the burden of supply and demand, and accept the risk that rents may go down at some point, instead of the homeowner finding themselves upside down. This will be much less disruptive to the economy!

The only problem with the renter is that if they ever needed to do a poor timed move this could lead to a mark on their credit score which is now being added as another weight on your credit worthiness when renting or owning. So this is another double whammy if the renter does not plan their move correctly. Either way the landlord makes out like a bandit in this case. I think the rental contract by itself is really a big hurdle for all renters when trying to move about freely. If month-to-month could be the norm without concern of rental increases per year I think you would have a more robust rental community.

“Landlords face the burden of supply and demand.”

That may be true nationally. But it is the exact opposite here in desirable parts of socal…renters face the burden of supply and demand.

Supply: No more buildable land in most parts of town. Long time owners NOT selling for various reasons. Low rental vacancy rate.

Demand: Increasing population. People will stay here or move here regardless if they can afford it or not…it is different here.

I came across the following in a comment on another blog of this type and it reminded me of SoCal housing vested interests’ “this place is different” dogma. It’s rather peculiar that folks such as yourself before the last bubble popped were essentially espousing how this place wasn’t different (by way of agreeing that the writing was on the wall for this place, amongst others), are now singing the opposite tune. Very peculiar indeed. I suppose the message to logically follow from the pulpit is how this *time* is different.

—

“…Although only a few observers have noted the vested interest in error that accompanies speculative euphoria, it is, nonetheless, an extremely plausible phenomenon. Those involved with the speculation are experiencing an increase in wealth–getting rich or being further enriched. No one wishes to believe that this is fortuitous or undeserved; all wish to think that it is the result of their own superior insight or intuition. The very increase in values thus captures the thoughts and minds of those being rewarded. Speculation buys up, in a very practical way, the intelligence of those involved.

This is particularly true of the first group noted above–those who are convinced that values are going up permanently and indefinitely. But the errors of vanity of those who think they will beat the speculative game are also thus reinforced. As long as they are in, they have a strong pecuniary commitment to belief in the unique personal intelligence that tells them there will be yet more. ..Strongly reinforcing the vested interest in euphoria is the condemnation that the reputable public and financial opinion directs at those who express doubt or dissent. It is said that they are unable, because of defective imagination or other mental inadequacy, to grasp the new and rewarding circumstances that sustain and secure the increase in values…â€

-John Kenneth Galbraith

A Short History of Financial Euphoria

Mr. or Ms. Skeptic, sounds like you are still in denial. It took me a while to understand the dynamics of the socal housing market, I’m glad I finally got it. You can sit back and wait for the big crash and pick up your 3/2 SFR in prime or near prime areas for 400K…you’ll be waiting a while. I’m in the Jim Taylor camp, let housing tank HARD so I can add a beach close rental property to my portfolio.

Crackhouses in Compton sell for 250K, SFRs in very marginal areas sell for 400K plus and I’m not even going to bother talking about prime or near prime areas. Compared to 90% of the country, it is VERY different here. Keep waiting for the big crash and be sure to have your ducks in a row, there will be plenty of competition.

Lord B.,

I have “my ducks in a row” and I am still waiting for that crash so I can add to my portfolio of rental homes. By the way, I am also looking for that 3 BR, 2 BA, double garage within 2 miles from ocean for under 400k …:-)))) So, you will have serious competition when the crash comes. I just hope there will be ONLY the 2 of us because I don’t want others to step on my toes…:-))))

I hope that Skeptic and Brain of E. will be looking for under 300k when the crash comes otherwise I don’t think we’ll find enough inventory to keep all four of us happy.

You have no idea what I’m “waiting around” for or even if I think there will be a so-called crash. You’re just assuming all sorts of things.

So let’s see, you admit you were misguided before and now you got it. This time is different. Um, okay pal.

You both are silly. Brain of England lives in England and has never made any suggestion that he intends on moving to SoCal to buy a house and live in it. I never said I wanted to buy anything in SoCal.

Flyover, sounds like you have a great plan. Let’s keep this our little secret. We certainly don’t need any “unwanted” attention when those bargains present themselves at the next downturn.

Fill that war chest and keep the powder dry. 🙂

With more and more people renting, who is going to buy single family houses?

Gentrificators!

“With more and more people renting, who is going to buy single family houses?”

People won’t rent forever.

In Switzerland and Germany, where they are doing better financially than Americans, only about 40% of the people own homes. These citizens haven’t chugged any government Kool-Aid about home ownership being the key to wealth and success.

Germany is not doing better financially than Americans. Europe’s biggest economy is strongly heading to a recession driven by a slump in German exports which have sustained the continent’s largest economy.

http://www.bloomberg.com/news/2014-10-06/german-factory-orders-slump-most-since-2009-as-euro-area-falters.html

There’s a reason Germans are less likely to own houses. The government doesn’t encourage it. Unlike high-homeownership countries like Spain, Ireland and the US, Germany doesn’t let homeowners deduct mortgage-interest payments from their taxes. German banks are quite risk-averse, making mortgages harder and more expensive to get. German property prices historically rise very slowly and German rents don’t rise very fast. The tendency of German rents to rise slowly results in fewer home buyers and a lower homeownership rate.

http://qz.com/167887/germany-has-one-of-the-worlds-lowest-homeownership-rates/

In a country this size always buyers, the question going forward, job stability, good paying jobs, a willingness to buy at these prices.

Buyers confidence in the ecomony, few believe in it, at this stage of housing people are not convinced there future in earnings justifies houses at these present levels.

Please stop the FHFA and Freddie Mac from restarting this madness:

Real estate and banking shill Mr. Mel Watt wants the FHFA to lower downpayment and credit requirements. The FHFA is taking public comments at:

https://www.fhfa.gov/SupervisionRegulation/Rules/Pages/2015-2017-Enterprise-Housing-Goals.aspx#SubmitForm

And can be directly emailed at:

RegComments@fhfa.gov

Subject line: Comments/R​IN 2590-AA65

If you guy are gonna spend time commenting here, please go to the FHFA and also lodge complaints. Loosening standards will have devastating long-term consequences for housing inflation.

AK

There is probably a good reason why homes were removed from the market to prop up housing. Like you say the preservation of these two GSE’s is a bad omen and will likely lead to all new immigrants/new home buyers being the ones being forced into loans they likely could never afford. Of course with rent increases across the board it almost likely will force these people to become owners. What a vicious cycle this is.

all in my opinion

I wonder about this. It’s cynical but I wouldn’t be surprised to see mass amnesty and housing policy deliberately intersect in the not too distant future. Lack of real demand has been the primary fundamental problem for years and that’s probably how the establishment is planning to address it.

Why would I do that? I thought the idea was for everyone to be able to own a home.

Hello AK. Do you think that there will be nearly enough complaints registered to prevent ThePowersThatBe from not moving forward with this?

They record and tabulate this stuff. Hey listen, it keeps a bureaucrat in business. I would do it. When they know people are looking, it makes them nervous. It will take you five minutes.

The credit and down payment standards mean little. The ONLY way they could extend the Ponzi this cycle would be to bring back no-doc loans. I suspect even that wouldn’t be enough as to many got burned last time, but it’s the only tool they have left. However to do so would require congress and a rewriting of Dodd/Frank. I don’t see that happening.

“Dear Housing Authority, please do not lessen credit restrictions and down-payment requirements. Doing so will enable more people to buy homes and I have a hard enough time competing with the current buying crowd for my crapshack, I mean my small piece of the American Dream. Thank you.”

If you think loose financing makes things more affordable, just look at college tuition and the 2004 bubble. Easy access to credit is dangerous and, sorry, if you need the loose standards, such as 3% down, you probably shouldn’t be buying it.

I would need a full term hefty negative mortgage rate to be willing to to buy in low-mid-prime at these prices.

Loosening credit criteria is not going to suddenly make that nation’s young quality earners, who don’t want epic debt, know the economy and their positions are very changeable, to want to over-reach to pay very high prices in low-mid-high prime areas, at asking prices of today. There are two sides to the lending equation; banks willing to lend, and borrowers willing to borrow. I guess looser credit is only really aimed at lower end/low value property.

AK: Done. Not that it will do any good. Who listens to the peasants these days ?

I grew up thinking only poor people rented. Then I moved to NYC and everybody rented. By the time I came to CA I had gotten over the ‘stigma’ of being a renter and realized I could afford a lot more for my money in a rental than I could if I bought. I own now but renting is far from being the end of the world people make it out to be. I saved a ton of money and was able to pay for college for my children so they have no student loan debt. I knew people who ‘owned’ houses and were carrying interest only loans on them. They stretched themselves to the limit and have nothing to show for it.

SoCal is not NYC. Completely different in so many ways. Here, in SoCal, people of any substance live on the westside(and a few other prime locations) and are not renters, and they drive the appropriate vehicle that represents their westside status.

Even the DMV rules have been rewritten for the Westsiders.

When 2 or 3 cars all approach a 4 way stop which car goes first? on the Westside it is the most expensive car not the car to the right. (funny but true if you have spent much time on the Westside).

I totally agree with you – see my comment below. All the “homeowners” I know are sucked dry by their “investments” and are stuck if they need to move.

Part of the mystique in ownership is that you appear so settled and successful that small things like jobs and relocation are nothing to you. NOTHING. You can ALWAYS find another high paying job because you are SO valuable. This is why you drive a leased bimmer, are mired in credit card debt, and have been paying your mortgage out of your 401k.

Check out this DUMP that Fannie is trying to offload for $322K:

https://www.homepath.com/listing?listingid=41163970

Now take a look at the Google streetview and satellite view:

https://maps.google.com/maps?es_sm=91&um=1&ie=UTF-8&q=4732+Topaz+St,+Los+Angeles,+California+90032&layer=c&z=17&iwloc=A&sll=34.083094,-118.188521&cbp=13,183.0,0,0,0&cbll=34.083194,-118.188515&sa=X&ei=-vRDVNGUAe2IiwKw-YHABQ&ved=0CCAQxB0wAA&output=classic&dg=oo

Obviously some updates have been made since the streetview was done but you know what probably hasn’t been updated – that city street you take to get up to the one derelict parking space, how nice. Or how about that earth mound of a “yard”. This is the sort of junk that L.A. is littered with in spades – where incomes do matter and the Chinese don’t. For our Chicago friend who asked a while back – for every one property that makes some sense here, there are at least ten more that don’t.

Some light digging of the history on this craptastic lil’ charmer reports it was foreclosed with $225K on the books (and that’s all we know of, there could be subordinates). $225K at most is what this crapper is worth today but no doubt, some moron will lever into this junk on the back of publicly guaranteed liquidity.

Interestingly, it appears that the previous sale was $123K back in 2001. Assuming that some sales history isn’t missing, that would mean the idiot who foreclosed on this place could have ran up one hell of a HELOC or cash out refi at some point or two back in the last bubble. I personally have been an observer to that very scenario in this part of town.

Considering the view location this is one of the more reasonable “homes of genius” I’ve seen. If you figure what a one bedroom in that hood would rent for your only a few hundred above that at the asking price (which they probably won’t get). If you had guaranteed permits before close it would be a good teardown purchase in the 200’s. But 300k is close enough to gull retard that I see your point.

@ skeptic re: homepath –

this one will likely get swooped up. Homepath always lists notoriously high and drops the price if they get not bites. some advantages for those looking to leverage the crap out of themselves:

3% down

Easy 3% offered to pay buyer’s CC’s

No MI

No appraisal required

First 15 days property is only available to owner occupants

Look like loosening will happen as early as this week. Tremendous pressure by builders and NAR to lower standards has led to the revised guidelines that may spur some buying.

Overall the fundamentals are still very weak, short sale and past forclusures on your record, forget looking for a house you will be turned down.

Suspect credit with low down, good job, you may get a look but not at the prevailing rate but much higher rate, which will most likely disqualify you anyway.

The golden rule of good credit, good stable well paying job, some money in the bank, sizable down payment gets you a house, still lot of folks who can’t meet that criteria.

Robert,

From what I have heard from mortgage dealers is that this will likely affect borrowers at the margin of qualifying and won’t create wholesale categories of newly eligible borrowers. We won’t know for sure for a while. Anyway, a new economic disaster is bound to hit and override and such fine tweaks before they cause any real change.

the very last thing a Community Bank would think of asking a regulator to support would be a residential subdivision,despite 5 + yrs & zero contiguous lot development. At the same time ZERO, SFD FTHB inventory? Why? Instead of FC inventory clearing HARP , delayed FC et all stall clearing the first round of FCs. Meantime, after 4 yrs to FC, FNMA , FHLMC,HUD et all sell the FC in 5 days, at .42 cents on the dollar. Six mos inventory SFD is “in balance.” You get the picture. Unlike a mortgage, the rent is still due.A renter can’t take cash out of an apartment.Having your three neighbors take cash out on their apartments, then move in the night won’t impact the value of your apartment.Rent will suck until the supply/demand favors the renter. Landord’s market for now. Could one argue we should have let the original terms of the debt/title instrument drive the balance of inventory SFD’s, not unlike rent? What if the saying ” the mortgage is still due” were true? Homeownership would be a better proposition with a market “in balance.”

“The rent is still due…” The bad news: Those running BIG GOVT believe you’re entitled to “shelter…”Watch what you wish for on the rental program. Upward mobility is a tough nut when your car has a range of 100 miles and 60% of one’s income AFTER taxes goes to the landlord and power company. The younger generation needs to consider the value of the dollar, & the percentage that goes to the govt, & “landlord.” A housing correction should last mos in an efficient market, not generations. One last question: Are the AG’s and states with Judicial FC’s that result in 1100 days to evict and one week to sell REO really doing their constituents any favors ? We’ll see..We’re getting closer every day to mortgage as a high margin,low volume proposition.

Structurally, things look great for TBTF Banks and Landlords.

I used to by and flip houses till about 15 years ago . I would find a house in real bad shape fix and flip it with a year. The hard part was finding the houses and getting them at a real low price . Now I’m surrounded by houses , hundreds of them that could be flipped but I feel there is another leg down coming so why bother.

Just curious, where do you live? Zip code?

Hi Doc. So much for the dead-cat bounce everyone was predicting for home prices on this site back in 2010, 2011.

And yet some are still saying ‘housing to tank hard in 2014’.

of course a broken clock is right twice a day – perhaps housing will tank hard in … 2016.

There you go, housing to tank hard in 2016!!!

Those waiting for better house price/rental value, only have to be right once. Those complacent about forever house price inflation and higher prices, have to continue to be right all of the time.

_____

“Demand is intrinsically linked to affordability, and that’s linked to how much banks are prepared to lend and how much people are prepared to borrow. Demand for housing is a very flexible thing. Saying something isn’t going to happen because it hasn’t happened yet doesn’t really make any sense.

That’s like saying because I haven’t died yet I won’t, but I guess I probably will. And a housing crash is much the same. Something not happening simply makes it more likely that it will, rather than it won’t. If the conditions are in place, and the conditions are in place.

Markets are driven at the margin. They’re driven by people who have to buy or people who have to sell. So when you get to the point when there are people who must sell, and that will come, then prices fall across the board because not many people have to be forced to sell at a low price to push values down.”

– Merryn Somerset Webb

_____

Housing IS Tanking Hard in 2014!

Yellen said herself months ago she was concerned about housing. Just wait its going to be an epic collapse. Yes the bounce was far more than anyone expected, but did anyone else expect the Fed Balance sheet to expand by a factor of 4 since the crisis? Pretty amazing stuff.

You only have a little over 20% of 2014 left for housing to tank hard. And the buying season is already past.

QE follows the law of diminishing returns. The drug analogy is spot on. You need more and more QE just to keep the market levitated. This is why I think we could see a Housing Bust alongside a slightly nominal rising stock market. We All know the fed is directly intervening in the market, crushing short positions. I don’t see how they can do this in housing. The banks have moved so many properties to private hands (greater fools) who will need to sell and there is no mechanism for the Fed to support those specuvestors. If we are to take the HELOC numbers at face value we are basically right back where we were in 2007. Now I wouldn’t be surprised if there is another incentive program launched as in 2010, but that will only help marginal buyers get on the property ladder it will not maintain bubble prices. 2010 prices minus 5-10% due to mortgage rates a point or so higher is my guess for 2016. Uber prime areas go back to 2011/2012 prices as you have to account for the ocean of liquidity dropped on the 1%ers in the last 5 years. Of course I’m of the thought that if you’re not “in the club” those areas are shit places to live anyway? I’d rather live in the IE and enjoy LA and OC amenities on weekends than work 80 hours a week to have the same home/car/lifestyle. And if I get really desperate to live by the water, Oceanside is pretty nice and affordable.

@Jim Tank, housing is not tanking at all. Stop making a fool of yourself… The topic says the the rents are going up and the demand increases. Builders are also pulling back on the single family homes, aka less supply, to the rental multifamilies…

if the price of the rent goes up and the demand is high, more people will be looking at ownership vs rent. Moreover, the interest rates are at the new lows… Housing not to tank at least for the next few years.

MOAR QE in 2015!!! And the QE will help to keep the prices elevated for the next couple of years!

The last time I checked here, in Bellevue WA, the rentals are sky high, and still very very few vacancies… We wanted to move this year to a better place (rental of course), but the prices keep up still. Our current rent is cheap, but the place sucks! Anyways better that paying twice as much for a similar dump…

Beware of the ideAs of March of 2016 🙂 🙂 🙂

@NihilistZerO wrote: “QE follows the law of diminishing returns..I think we could see a Housing Bust alongside a slightly nominal rising stock market….”

I’ll take the other side and argue that once QE ends the stock crashes badly. A crashing stock market takes down the high priced desirable coastal areas. Insiders selling stocks, exercising stock options and grants thanks to QE elevating the stock markets may very well have been the source of the bigger chunk of the all cash buyers of the last few years.

In the midwest and south, home prices are very reasonable. 2/1 starter homes there are in the $100K range, 3/2 are below $200K. Housing inflation appears to have been in areas where stock options/grants/sellers were most likely to buy in to.

I’ve been a homeowner 3 times and all those times it was not what it was cracked up to be. Pretty much bled me dry with mortgage payments, property taxes, mello roos, repairs, and updates.

I have now been a renter for a number of years since offloading my last house before the big crash and I must say, its not so bad. The rental I’ve been in for the past 3 yrs is now on the market “for sale by owner” – ridiculously overpriced and not a single showing in 2 months. Owners bought in the height of the bubble on an interest only loan and still owe $405k. Appraised value now = $325. Anyway I decided not to hang around and found another rental right up the street. Same rent per month but MUCH nicer. It was the landlord’s home until she got married so its nicely upgraded and no cutting corners or DIY “upgrades” and she’s rented it out for the past 3 ys. Its decorated in my taste and will suit me fine for a few more years. What I am paying in rent vs. what it would cost me to buy the place is so far apart in $$ I have no desire to buy. Unless the market corrects 25%. And of course, the HVAC or hot water goes out, I pick up the phone, and not at my expense.

I move in a week! I can attest to not feeling any stigma whatsoever for being a “renter”.

You’re a smart lady Calgirl. Enjoy your new superior home at the same rental price you were previously paying, and where the rent-vs-buy equation is still way in your favor. I wonder how your previous landlord will fare, in getting a tenant, whilst also trying to sell it and expect tenant to allow/do viewings. Hope it is a place you can call a home for the long-term as this house price crash plays out during next 3 years (or perhaps sooner if isolated opportunities for buying come along next year or so).

I have a co-worker who did a short sale of his home in 2010. He has had to move his family to 3 different rentals in the years because the landlords decided to sell their homes as the market recovered. He and his wife are tired of the expense and the hassles of moving. They can’t afford to buy another house as they’ve been priced out of the market in the areas that they want to live in.

I was a homeowner 3 times, then I changed to renting as I closed in on retirement. What peace of mind! Repairs? Call the landlord. Previously, I ended up over $60,000 upside down in my mortgage when property values slid backwards for 10 years. I had to go through foreclosure and bankruptcy. I am now retired, living comfortably on the other side of the planet. As a renter, I was able to save several hundred thousand dollars. Life is good now.

I have more money now I rent than I’ve had in 15 yrs of “home ownership”. I save minimum 35% of my take-home salary. I don’t have to worry about fixing the roof, plumbing, appliances, HVAC, etc. Its all included in my rent. I don’t stress about going underwater on my mortgage, because I have no mortgage. I own my 5 yo car outright, have not a single penny of school debt or credit card debt. I owe nobody anything. Its a great feeling. I’m free to move if I don’t like my neighbors, don’t like the neighborhood, or just feel like new surroundings.

I’ve been lucky my current landlord, even though he’s a halfwit for trying to sell it at an inflated price, knows not to whack up the rent on a good, long term tenant. My new landlord has 70% equity in the home I’ve leased and she has no intention to sell it. She said its a nice cash flow for her. So far I’ve been lucky.

In the past, many moons ago, I’ve had the landlord from HELL.. I moved out due to the harassment and sued his azz in court and won, plus triple damages. Since I’ve been looking around for a new rental these past few months, I found another one I liked, got an application form and on it, it asked “have you ever taken legal action against a landlord”? I called the property manager and said what the hell is this? Are you discriminating because I exercised my LEGAL and constitutional right to recover money STOLEN from me by a crooked landlord? Then I told him to shove the rental up his azz.

Be choosy about renting the right property, under the right circumstances, from the right landlord and usually its a good bet. I do a complete background check on the mortgage status of the property, and the owners themselves. I search court records for legal actions taken against or by them, just like they search on me. I’m a fraud investigator for an insurance company so I know how to find out everything I need to. The average person can do it to without access to specialized tools, if they know where to look.

@Valence. Moving 3 times in 3 yrs does suck for sure. That’s just bad luck moreso than the norm for renting IMO.

@Calgirl — excellent post. I had the inverse of your bad landlord: bought a new home and had the developer/builder from Hell. Shoddy workmanship and construction defects causing water intrusion. After a parade of the builder’s fix it guys who would only do half-@ss cheap cosmetic repairs that didn’t fix the problems, I got a lawyer and filed suit. Builder saw the light and settled prior to court. Paid me more than enough cash so I could hire my own independent contractor to tear the house open and fix it right.

From that experience I concluded that it’s riskier to buy a new mass-produced house than buying a new car. At least with a new car you have the Lemon Law on your side!

RSpring,

There is a VERY BIG difference between a house built to pass inspections (minimum building code) and one built based on BEST building practice. Usually you get what you pay for. That is the reason the rich order the construction based on quality not price.

The minimum building code makes very unrealistic assumptions. The best building practice start from very realistic assumptions. You were happy to get paid by the builder – maybe he didn’t even pass the minimum building code. Normally, in most states the builder does not have any liability from the legal point of view. If he does, and he met the local building code, you can’t win anything.

The builder is not under obligation by law to build beyond minimum building code. I am saying this to warn you for the future. You can’t expect to buy a Ferrari for the price of a Ford Pinto. Both are safe to drive on the freeway, have 4 wheels and a wheel steering but you can’t expect quality from something built on low budget. That is the reality of life.

It is like people on this blog who want to buy on the Westside for the price of Rialto. Or those who apply the RE dynamic in an area of blue color workers to one where only high paying celebrities, investors and wealthy people buy. In the first area prices depend on average income and in the second are prices depend on wealth (the average income is totally irrelevant).

“It is like people on this blog who want to buy on the Westside for the price of Rialto. Or those who apply the RE dynamic in an area of blue color workers to one where only high paying celebrities, investors and wealthy people buy. ”

That’s a chicken shit comment. No one on here has made any such suggestion. What has been suggested is that areas such as the Westside are subject to corrections as well as any other area. No one has said that they expect Bel Aire to have dynamics similar to Compton. Stop the hyperbolic insanity.

“I don’t have to worry about fixing the roof, plumbing, appliances, HVAC, etc. Its all included in my rent. I don’t stress about going underwater on my mortgage, because I have no mortgage. I own my 5 yo car outright, have not a single penny of school debt or credit card debt. I owe nobody anything. Its a great feeling. I’m free to move if I don’t like my neighbors, don’t like the neighborhood, or just feel like new surroundings.”

Some of the intangibles of renting.

Your perspective is appreciated and important here because it’s one of comprehensive experience. You’ve been there and back again. We see a lot of folks commenting who have either a) always been a renter and bought their first house during a recent dip or b) bought many moons ago and haven’t rented since. They regale us with trivial platitudes of “wisdom”, however shallow those may be.

“Be choosy about renting the right property, under the right circumstances, from the right landlord and usually its a good bet.”

Just like buying a house, you either approach it with blinders on or take the effort and time necessary to subject it to diligent scrutiny. Of course, experience counts for a lot – not everyone has that.

My overall experience when I was a renter in LA, LA, LAnd was pretty good. From the time I left home (1984) to the time I bought a house (2012) I was a tenant in 7 different apartments, mostly in Santa Monica or WLA. Of all those places I only had 1 bad experience with a landlord who bought the 11 unit bldg I was living in near 10th and Wilshire Blvd. He attempted to get all the tenants to pay for trash and sewage and water but when I reported him to the rent control board, he was served with a registered letter 2 days later informing him he was in violation of rent laws. Other than that, no psycho landlords or nutty neighbors. Had one landlord on Barrington Ave and Gateway Blvd who would slap a 3-day notice to vacate on the front door on the 2nd day of the month if rent was not paid by the 1st day of each month.

Rip USA long live USSA !

An era has ended in 2007. Millions lost their homes and many lost their millions.

You can’t print jobs you can’t print profits. Wages stagnate and jobs get outsourced for profit gains. Corporations and once legendary US retailers close hundreds of stores lay off thousands and buys back millions in shares so they meet or beat their PE.

People vote in a president twice who has no experience no track record no birth record neither black neither white. RIP USA.

Seriously? Ever think about just turning off FAUX news and getting an education?

Janus wants you to watch the state run news media propaganda and never question what big government tells you. Ebola is not a problem according to Obama who claims he shook hands, hugged and kissed the nurses at the hospital (but not the doctors).

As for SoCal real estate, we’re cautious in the short term and bullish in the long term.

Where is he exactly wrong Janum?

Well, there’s the attempt to pin decades of tax policy and Fed decisions on one president, an “empty suit community organizing” charge that could easily be tweaked to apply to other politicians, and then there’s the birther charge bolstered by a “half breed” insult. I don’t keep track of usernames, but KLG’s post is so over-the-top that it has to have been satire.

Welcome to hope and change brought to you by Democrats. Now, only the wealthy or high income with good credit scores get to live in desirable areas. The rules have changed such that everyone else has been forced out from desirable areas. Obama and the Democrats took good care of the halves.

“The game is rigged. The Republicans rigged it.” – Elizabeth Warren

If anyone knows what they’re talking about it’s her. She’s spearheaded the fight against Wall Street special interests against all Republican resistance. This is worth reading —

http://www.washingtonpost.com/blogs/post-politics/wp/2014/10/18/warren-in-minnesota-the-game-is-rigged/

The Dems were just as guilty of rigging the game. Most of it was done under Clinton

hoping and saving my change got me my place.

I’m not one for censorship, but I wish sites like this and zerohedge would perma-ban anyone still parroting the Team Red/Team Blue bullshit. They bring nothing to the conversation and do not deserve to sit at the adult table.

8 years of Bush and 8 years of Obama = a 16 year total war on Americans. How can anyone STILL be blind to this fact??? The cognitive dissonance is astounding…

Left, right, left, right, ….the lemmings march over the cliff…!!!!

Someone said that if ignorance/stupidity would hurt, there would be less stupid people. I am of the opinion that it hurts but the stupid can not connect the dots, they can’t understand cause and effect, therefore, they continue on the same path. Just my 2c…

Amen

Bernanke, the author of QE, is a republican appointed by a republican.

Yes, I have no doubt yelled will institute a qe at some point but if you think republicans are the answer to the middle class being on life support, well….. ( as Ronald Reagan, the lord and savior would say), YOU HAVE NOT BEEN PAYING ATTENTION.

Left, right, left, right, ….the lemmings march over the cliff…!!!!

And Bush didn’t take care of the haves?

Bush Old – Repub, Willy Clinton – Dem, Bush Jr. – Repub , Obama – Dem. America has been in decline for the last 30 years. You tell me the Republicans are better then democrats or democrats are better than republicans? Seriously, get a brain!!! The both parties are just as bad, it has never been about Dems vs Repubs, it was always evil vs evil. I despite the both parties. The only candidate from the Repubs that I considered worthy of becoming a new president was Ron Paul and he is out of the game now… Obama vs McCain? Obama vs Robme? Hitlary vs ??? What a f…ing great choice… This country is screwed…

jt – Open your eyes. Both parties cater only to the 0.1%. Neither party is going to “save” the middle class. Everybody says they’re going to do it, but once in office they just cater to the folks that paid their way to office. That’s neither you nor I.

The feds will do anything and everything to keep the housing market going. They have too much to lose. Fannie Mae and Freddie Mac gobbled up over 90% of the mortgages in this country. There is no way the feds can afford a meltdown. I wouldn’t be surprised to see negative interest rates like in Europe before the Feds let the housing market crash. As it stands now, we are dipping under 4% for the first time in almost 2 years. Bubble 2.5 here we come!

I’m hearing talk of 3.6

Told you, some folks are delusional or just don’t get it. It is not over yet, the ECB just announced its own QE, the FED is about to announce QE4… The fundamentals no longer matter. What can be manipulated (stocks, bonds, housing, gold, etc) will be manipulated until it won’t. The FED hasn’t run out of bullets yet!

Here it goes, Housing Bubble 2.5. The ponzy must go on…

Interest rates are trending down to 2013-2012 levels. I suspect this is in the interests of the Fed in their goal to create the populist perception of wealth through an inflated stock market as well as inflated housing prices.

You are correct. It’s not having the effect the current Administration was looking for. The Republicans will take the Senate despite their efforts to do everything they could to avoid it, including artificially propping up housing values.

It doesn’t matter if (R) or (D) is in power. Bush appointed Bernanke, Obama kept him and appointed Yellen, who is just Bernanke warmed over. Obama continued most of the Bush tax cuts and extended Bush’s TARP bailouts. While Obama talks left he walks like a supply-sider. When it comes to monetary policy and economics, Obama has been Bush’s 3rd and 4th term.

The reason everything continues the same is because the real government (made up by the FED and CFR) is the same. Just because the public figure changed does not mean that the FED or the Council of Foreign Relations changed their policy.

A good example was with the attack on Syria last year – when all the electorate from the left and the right wrote to their representative that they are against, the president found himself isolated. Fast forward one year, after the approach was changed, they attacked Syria without anyone saying anything (without a small minority which understands how things work). I blame Obama because he was the president but I am 100% sure that if Bush, McCain, Clinton or Romney were presidents the same line would have continued.

Why? Because all were from the same CFR. I am convinced though that if someone like Ron Paul or Ben Carson would have been there, he would have opposed the attack. That is why everyone outside of the real government faces the full force of the MSM controlled by few people and all from their group get a pass regardless if the letter after their name is D or R.

This is a great thread. I keep reading because there is not 20 posts yet from the guy from Seattle.

Thumbs up to that 🙂

Hahaha. In his case, less is definitely moar.

There is nothing wrong with renting as long as you have some kind of savings account for everyday life, and a 401k for retirement.

September numbers are in. YoY inventory is up, sales are down. Sound familiar?

http://www.calculatedriskblog.com/2014/10/existing-home-sales-in-september-517.html

Dom you are failing to mention that is a national survey and more importantly that existing home sales posted yet another YoY price increase of 5.6%. I’m willing to bet SoCal shows a higher YoY increase.

But keep going with that tank hard in 2014 meme and I’m sure it will come true, just like everyone on this blog was posting in 2011-12 that there is another leg down coming and you better not buy or you’ll catch the dreaded falling knife…because that strategy was just genius.

And that 1.7% MoM decrease in volume, man that is just HUGE! It’s tanking for SURE now!!!

So my husband and I currently own our home in Los Angeles and are looking for a rental property. What areas are good for purchasing a rental property. Or does the city even matter…

New to rental property’s

Stay out of the ghetto areas which is 90% to 95% of LA county

Good answer Ben!… 100% correct for those who understand RE.

Let’s see what the numbers look like for October-December in SoCal. In early 2006 prices were high but sales dropped substantially; and what followed was depreciating prices.

Yes Dennis, let’s. In early to mid 07 all the credit criminals that purchased with 100% financing stated loans stopped paying which triggered the implosion. All the first payment defaults and buybacks started hitting.

Let’s see if that happens this time around. I contend that any substantial decrease in prices i.e. SoCal greater than 3% YoY will need to be precipitated by some type of black swan event. Barring that, no tanking coming until at least 2016.

DID YOU SEE THE NEWS?

The Fed’s are working with banks to get Fannie and Freddie to buy 3% down loans. So lending standards will be loosened again. DHB you should do an article on this.

I now retract my previous statement (for better or worse), of a 10% decline coming. Who knows if prices will go up, but they should remain stable now as the party will probably continue for a year or more. Especially with rates falling agian

The news I just saw was…

September unemployment falls in 31 states

http://www.usatoday.com/story/money/business/2014/10/21/unemployment-rates-september/17658235/?utm_source=feedblitz&utm_medium=FeedBlitzRss&utm_campaign=usatodaycommoney-topstories

and–

Existing home sales hit highest level in 2014.

http://www.usatoday.com/story/money/business/2014/10/21/september-existing-home-sales/17654655/?utm_source=feedblitz&utm_medium=FeedBlitzRss&utm_campaign=usatodaycommoney-topstories

What does this mean???

“What does this mean???”

It means that midterm elections are coming soon, the Minister of Propaganda provided the numbers the Democrats requested because they will be adjusted after the elections same as in the previous elections. Some things never change.

The sheeple have to feel good at least about the numbers if not in real life when they go to the booth. Since “mesiah”s appointed czars said so, it must be so. Did he ever lied to the sheeple???!!!!…..

I see your point CAB. Considering the increase in inventory, sales will need to rise for prices to hold. There are more restrictions on lending, so we’ll see if there are enough qualified buyers.

Hi Dennis – This is where I think you are mistaken “Considering the increase in inventory” in my market in SoCal there is a 4 month supply. AZN $ still coming, no matter the level of shadyness, it’s still there. Sales would not have to increase for prices to simply hold. More restrictions on lending? Look at the recent news about lenders restrictions on mortgage buybacks getting loosened, lower credit scores being accepted and down payment requirements being reduced. Those things coupled with mortgage rates that are actually lower YoY seem to point to a flat or slightly increasing market. I don’t think there will be any meaningful correction until at least 2016.

The Mortgage Industry Is Strangling the Housing Market and Blaming the Government

http://www.newrepublic.com/article/119918/mel-watts-2014-mba-speech-and-assault-housing-regulations

Leave a Reply